Mechanical Linkage Market Size and Growth Forecast 2026-2030

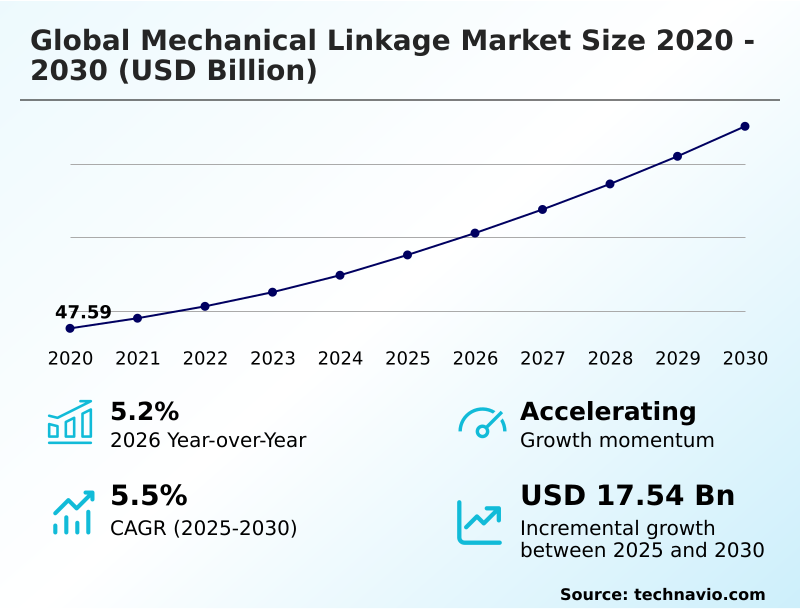

The Mechanical Linkage Market size was valued at USD 57.60 billion in 2025 growing at a CAGR of 5.5% during the forecast period 2026-2030.

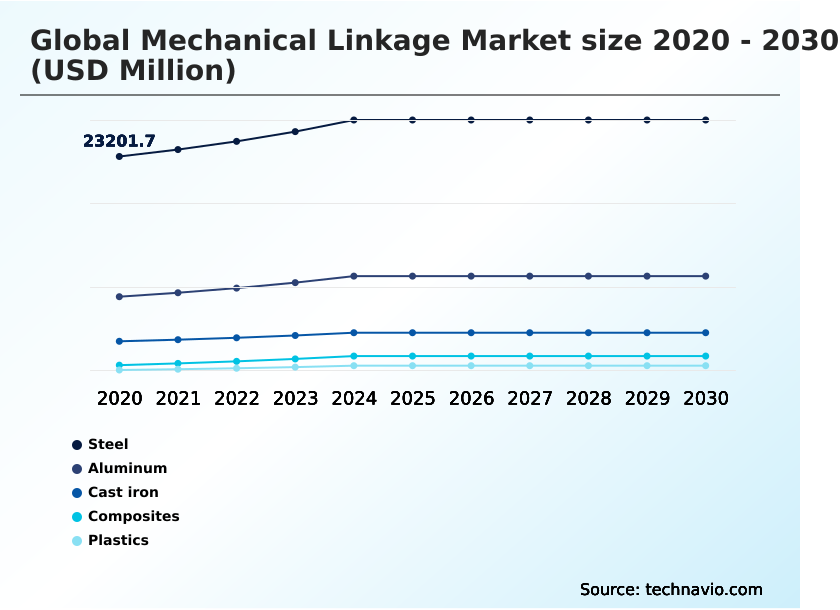

APAC accounts for 46.1% of incremental growth during the forecast period. The Steel segment by Material was valued at USD 26.54 billion in 2024, while the Original equipment manufacturers segment holds the largest revenue share by End-user.

The market is projected to grow by USD 27.54 billion from 2020 to 2030, with USD 17.54 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Mechanical Linkage Market Overview

The mechanical linkage market is defined by a critical need for precision and durability in motion control systems, with APAC contributing over 46% to the market's incremental growth. A key dynamic is the push for industrial automation, where custom linkage assemblies form the backbone of articulated robotic arms and other kinematic mechanisms. This requires components with exceptional fatigue resistance and structural rigidity. For instance, in a high-volume automotive plant, redesigning steering and suspension systems for electric vehicles with lightweight composite linkages and advanced aluminum alloys can reduce unsprung mass, improving vehicle dynamics while adhering to ISO 26262 functional safety standards. The trend towards mechatronics integration is also significant, with manufacturers embedding sensors for predictive maintenance. However, the market faces headwinds from the emergence of purely electromechanical actuators and supply chain vulnerabilities tied to high-strength steel and specialty polymer sourcing. Decision-makers must balance the proven reliability of mechanical actuation against the digital integration benefits of alternatives, making total cost of ownership a central procurement consideration.

Drivers, Trends, and Challenges in the Mechanical Linkage Market

The strategic imperative for operational efficiency and compliance is reshaping procurement criteria across the mechanical linkage market. Demand for high precision linkages for robotics is intensifying as manufacturers automate to mitigate labor costs, with a focus on multi-bar linkages that ensure repeatability under ISO 9283 standards.

Concurrently, the aerospace sector's push for fuel efficiency drives adoption of lightweight composite linkages for aerospace applications, where every kilogram saved has a direct impact on operational costs.

For example, a commercial aircraft manufacturer replacing metallic flight control linkages with carbon fiber reinforced polymer equivalents can achieve weight savings that translate to lower fuel burn over the aircraft's lifespan, which is a significant factor, given that fuel can account for over 20% of an airline's operating expenses.

In heavy industries, the focus is on durability, with heavy duty linkages for construction equipment specified to withstand extreme operational stress.

The shift is also apparent in regulated sectors; the demand for lubrication free linkages for food processing is driven by FDA food contact material regulations, while automakers are specifying custom steering linkages for electric vehicles to accommodate unique chassis layouts and weight distributions, influencing the entire supply chain.

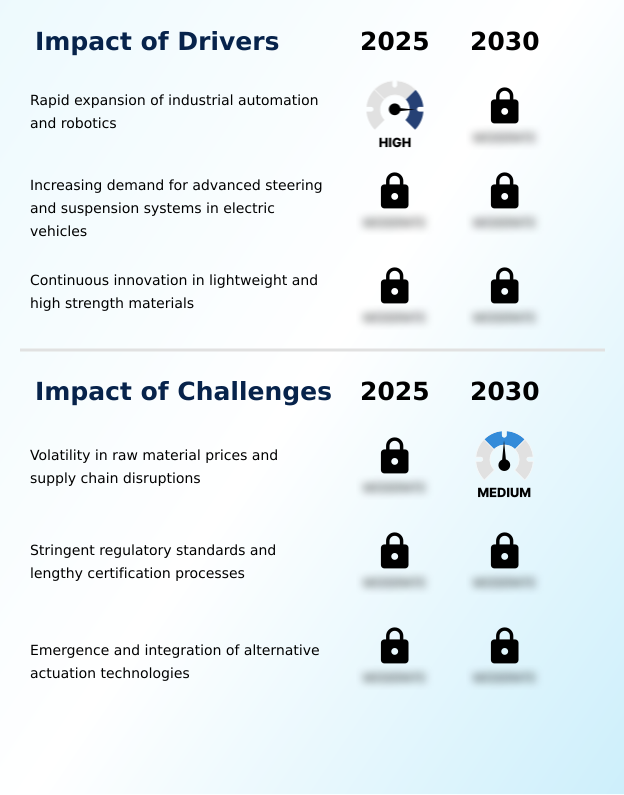

Primary Growth Driver: The rapid expansion of industrial automation and robotics across the global manufacturing landscape is a key driver for the mechanical linkage market.

The market is primarily driven by the relentless expansion of industrial automation and the transformative shift in the automotive sector.

In manufacturing, the demand for precision linkages for articulated robotic arms and other motion control systems is surging as industries pursue higher efficiency, with APAC's market growing at a notable 6.6%.

These kinematic mechanisms are essential for translating motor inputs into precise, repeatable movements. In parallel, the global transition to electric vehicles is creating new requirements for specialized powertrain components and driveline components.

The unique chassis architecture of EVs necessitates a complete redesign of steering and suspension systems, demanding high-strength steel and aluminum alloys to manage different weight distributions and dynamic forces.

This evolution ensures that robust, high-performance mechanical actuation will remain a critical element in next-generation manufacturing and mobility.

Emerging Market Trend: The integration of smart sensors and Internet of Things (IoT) technologies into mechanical actuation systems is a prominent trend. This shift enables continuous performance monitoring and real-time data analytics for predictive maintenance.

A significant market trend is the convergence of advanced materials and manufacturing processes. The adoption of additive manufacturing is enabling the production of highly optimized kinematic mechanisms using topology optimization software, resulting in lightweight composite linkages with superior structural rigidity. This is particularly impactful in aerospace and robotics, where weight and performance are critical.

Simultaneously, the industry is moving towards greater operational intelligence through the integration of smart sensors. Embedding diagnostic tools within custom linkage assemblies allows for predictive maintenance, a substantial shift from traditional reactive repairs. This is driven by the need to minimize downtime in high-stakes environments.

Furthermore, there is a clear trend towards sustainability with the development of self-lubricating polymers and lubrication-free linkages, reducing environmental impact and maintenance requirements in sectors like food processing and pharmaceuticals.

Key Industry Challenge: Volatility in raw material prices and persistent supply chain disruptions represent a key challenge impacting production costs and stability in the mechanical linkage market.

The market faces significant challenges from both supply-side volatility and technological competition. Fluctuations in the price of raw materials like high-strength steel and aluminum alloys create instability in production costs, a risk compounded by a concentrated global supply chain for specialized materials. Any disruption can have a cascading impact on assembly operations worldwide.

A more fundamental challenge is the emergence of alternative technologies. Purely electromechanical actuators offer seamless digital integration and advanced programmability, which is highly attractive in the context of smart factories. This forces traditional mechanical linkage manufacturers to invest heavily in mechatronics integration, combining their mechanical expertise with electronics and software.

To remain competitive, they must demonstrate that their products offer superior fatigue resistance, corrosion resistance, and a lower total cost of ownership, reinventing their value proposition for the digital era.

Explore Full Market Dynamics Analysis Request Free Sample

Mechanical Linkage Market Segmentation

The mechanical linkage industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Material Segment Analysis

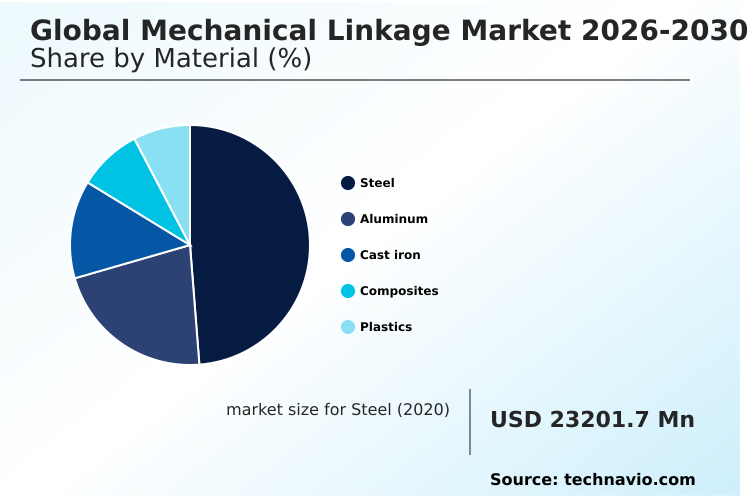

The steel segment is estimated to witness significant growth during the forecast period.

Steel remains the dominant material segment, constituting nearly half of the market due to its unparalleled tensile strength and cost-effectiveness.

The material’s versatility, enhanced through alloying processes to create high-strength steel variants, ensures superior structural rigidity and fatigue resistance in heavy-duty applications. For environments requiring enhanced corrosion resistance, stainless steel alloys are specified, particularly in marine and chemical processing sectors.

Despite the material's weight, the exceptional cost-to-lifespan ratio of carbon steel and alloy steel makes them the primary choice for powertrain components and industrial machinery.

Continuous advancements in heat treatment and surface hardening allow steel-based kinematic mechanisms to operate reliably in high operational stress environments, solidifying their position as the foundational material for mechanical power transmission.

The Steel segment was valued at USD 26.54 billion in 2024 and showed a gradual increase during the forecast period.

Mechanical Linkage Market by Region: APAC Leads with 46.1% Growth Share

APAC is estimated to contribute 46.1% to the growth of the global market during the forecast period.

The geographic landscape is dominated by APAC, which accounts for 46.1% of the incremental growth, driven by its massive manufacturing output in China, Japan, and South Korea.

This region's demand is centered on industrial automation, requiring vast quantities of precision linkages for articulated robotic arms and powertrain components for the automotive sector.

North America, while growing at a more moderate pace, is a key market for high-value applications, including aerospace and defense, where lightweight composite linkages and components meeting stringent FAA standards are required.

Europe, led by Germany's advanced automotive engineering sector, focuses on high-performance steering and suspension systems and is a leader in adopting lubrication-free linkages to comply with strict EU environmental directives like REACH.

The use of heavy-duty linkages in construction and mining remains a significant driver in the Middle East, Africa, and South America.

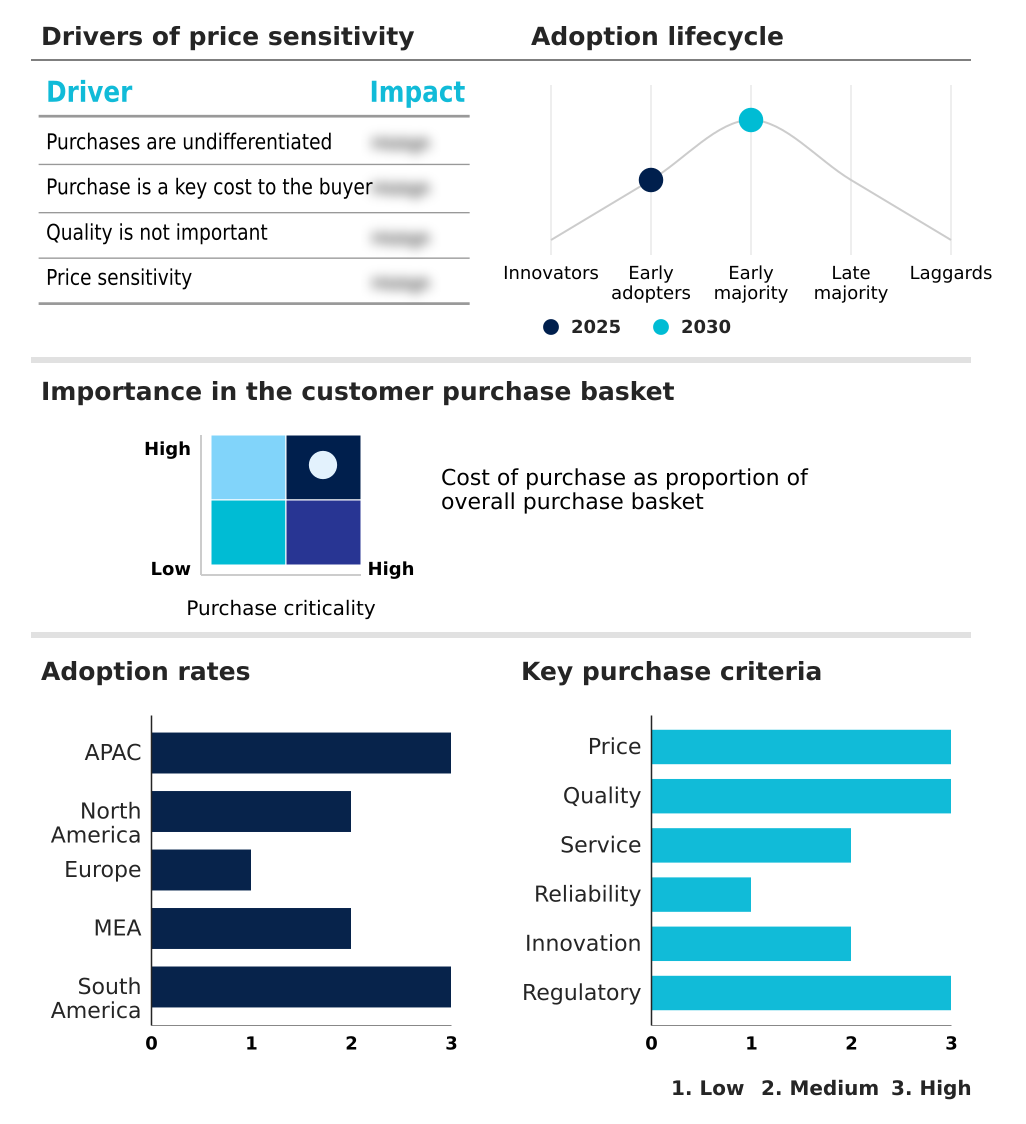

Customer Landscape Analysis for the Mechanical Linkage Market

The mechanical linkage market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the mechanical linkage market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Mechanical Linkage Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the mechanical linkage market industry.

AB SKF - Provides mechanical linkage solutions featuring an extensive portfolio of standard rod ends and spherical plain bearings for diverse industrial and automotive applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB SKF

- Aurora Bearing Company

- Curtiss Wright Corp.

- DURBAL GmbH

- Eaton Corp. Plc

- GKN Automotive Ltd.

- igus SE and Co. KG

- Kaman Corp.

- MinebeaMitsumi Inc.

- Moog Inc.

- NSK Ltd.

- NTN Corp.

- Parker Hannifin Corp.

- RBC Bearings Inc.

- Regal Rexnord Corp.

- Schaeffler AG

- The Timken Co.

- Tuthill Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Mechanical Linkage Market

- In January 2025, igus announced the acquisition of elko Verbindungstechnik GmbH to strengthen its assembly capabilities within the drive technology sector.

- In August 2025, Schaeffler India announced the expansion of its large-size industrial bearings portfolio with the introduction of Made-in-India spherical roller bearings and cast steel housings.

- In October 2025, SoftBank Group Corp. announced a definitive agreement to acquire ABB Ltd.'s robotics business, impacting the demand for precision linkages in articulated robotic arms.

- In December 2025, ZF Friedrichshafen AG announced an agreement to divest its Advanced Driver Assistance Systems (ADAS) division to Harman International, realigning its focus within automotive technology operations.

Research Analyst Overview: Mechanical Linkage Market

Procurement decisions are shifting from a component-level focus to a system-level evaluation of performance and compliance. The integration of sensors into mechanical linkages, a key aspect of mechatronics integration, is no longer a niche capability but an emerging standard for predictive maintenance in industrial automation.

This trend is compelling boardroom-level investment in new engineering skill sets to develop smart motion control systems that provide real-time data on operational stress and wear. For instance, a manufacturer of articulated robotic arms must now ensure its kinematic mechanisms, including rod end bearings and spherical plain bearings, comply with functional safety standards like ISO 13849.

This requires a deeper understanding of electronics and software, not just mechanical engineering. With the OEM segment representing a significant portion of the market, suppliers that can offer certified, pre-integrated custom linkage assemblies with embedded diagnostics will command a premium and secure stronger, long-term partnerships.

The ability to provide a complete mechanical actuation solution, rather than just a part, is becoming the key differentiator.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Mechanical Linkage Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.5% |

| Market growth 2026-2030 | USD 17538.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.2% |

| Key countries | China, India, Japan, South Korea, Indonesia, Australia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Turkey, Israel, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Mechanical Linkage Market: Key Questions Answered in This Report

-

What is the expected growth of the Mechanical Linkage Market between 2026 and 2030?

-

The Mechanical Linkage Market is expected to grow by USD 17.54 billion during 2026-2030, registering a CAGR of 5.5%. Year-over-year growth in 2026 is estimated at 5.2%%. This acceleration is shaped by rapid expansion of industrial automation and robotics, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Material (Steel, Aluminum, Cast iron, Composites, and Plastics), End-user (Original equipment manufacturers, and Aftermarket), Application (Automotive systems, Industrial machinery, Agricultural equipment, Construction equipment, and Others) and Geography (APAC, North America, Europe, Middle East and Africa, South America). Among these, the Steel segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, North America, Europe, Middle East and Africa and South America. APAC is estimated to contribute 46.1% to market growth during the forecast period. Country-level analysis includes China, India, Japan, South Korea, Indonesia, Australia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Turkey, Israel, Brazil, Argentina and Colombia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is rapid expansion of industrial automation and robotics, which is accelerating investment and industry demand. The main challenge is volatility in raw material prices and supply chain disruptions, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Mechanical Linkage Market?

-

Key vendors include AB SKF, Aurora Bearing Company, Curtiss Wright Corp., DURBAL GmbH, Eaton Corp. Plc, GKN Automotive Ltd., igus SE and Co. KG, Kaman Corp., MinebeaMitsumi Inc., Moog Inc., NSK Ltd., NTN Corp., Parker Hannifin Corp., RBC Bearings Inc., Regal Rexnord Corp., Schaeffler AG, The Timken Co. and Tuthill Corp.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Mechanical Linkage Market Research Insights

Market dynamics are increasingly shaped by the dual pressures of regulatory compliance and technological substitution. The push for sustainability, underscored by regulations like the EU's RoHS directive, is accelerating the adoption of self-lubricating polymers and lubrication-free linkages, particularly in applications where contamination is a critical risk.

For example, in a semiconductor fabrication cleanroom, acetal resin-based kinematic mechanisms are preferred over lubricated metal parts to prevent outgassing and particulate generation. This trend offers a distinct advantage over traditional mechanical systems that require frequent maintenance. At the same time, the market is navigating competition from fully electromechanical actuators that offer easier digital integration.

This forces manufacturers to focus on enhancing the tribological performance and vibration damping of their offerings. Original equipment manufacturers, who constitute the larger end-user segment compared to the aftermarket, are therefore scrutinizing the total cost of ownership, weighing the durability of mechanical solutions against the programmability of electronic alternatives.

We can help! Our analysts can customize this mechanical linkage market research report to meet your requirements.

RIA -

RIA -