Military Mobile Computing Systems Market Size 2024-2028

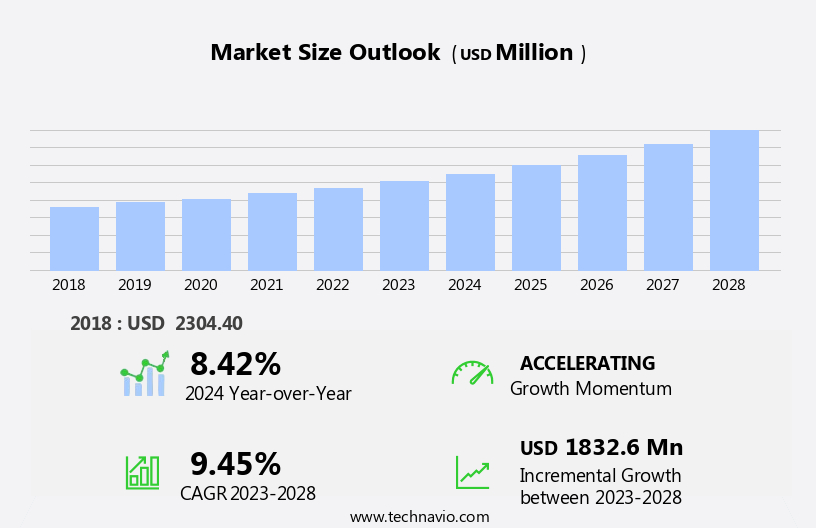

The military mobile computing systems market size is forecast to increase by USD 1.83 billion at a CAGR of 9.45% between 2023 and 2028.

What will be the Size of the Military Mobile Computing Systems Market During the Forecast Period?

How is this Military Mobile Computing Systems Industry segmented and which is the largest segment?

The military mobile computing systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Component

- Products

- Services

- Device

- Radio

- Smartphones

- Tablets

- PCs and laptops

- Geography

- North America

- US

- Europe

- UK

- APAC

- China

- India

- South America

- Middle East and Africa

- North America

By Component Insights

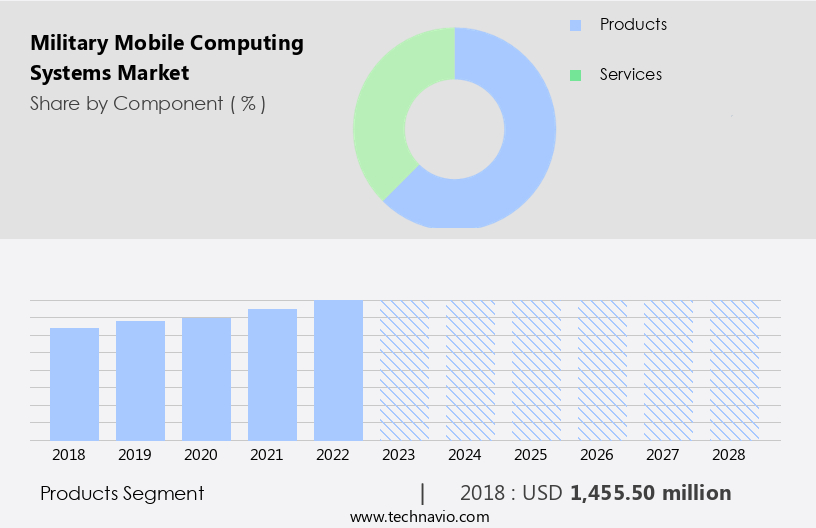

The products segment is estimated to witness significant growth during the forecast period. The military and defense sector's reliance on mobile computing systems has grown significantly due to the need for secure communication and data management in mission-critical operations. With most military missions conducted in remote areas, rugged mobile computing solutions are essential for transmitting and receiving information without disruption or interception. The US Department of Defense (DoD) is driving the adoption of rugged mobile computing In the defense industry, as commercial technologies are being ruggedized for military use. The integration of Artificial Intelligence (AI) technology, digital infrastructure, and advanced sensors in military equipment is also fueling market growth. Furthermore, the increasing focus on cybersecurity advancements, ML and big data analytics, and cloud computing as cost-effective and flexible solutions for joint operations and coalition efforts is shaping the defense landscape.

Military organizations require high computational power, data sovereignty, and security measures to address emerging threats, data breaches, unauthorized access, and cyber threats. The MCC ecosystem, including mission planning, threat detection, network connectivity, and real-time communication, is critical for operational strategies and situational awareness.

Get a glance at the market report of various segments Request Free Sample

The Products segment was valued at USD 1.46 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

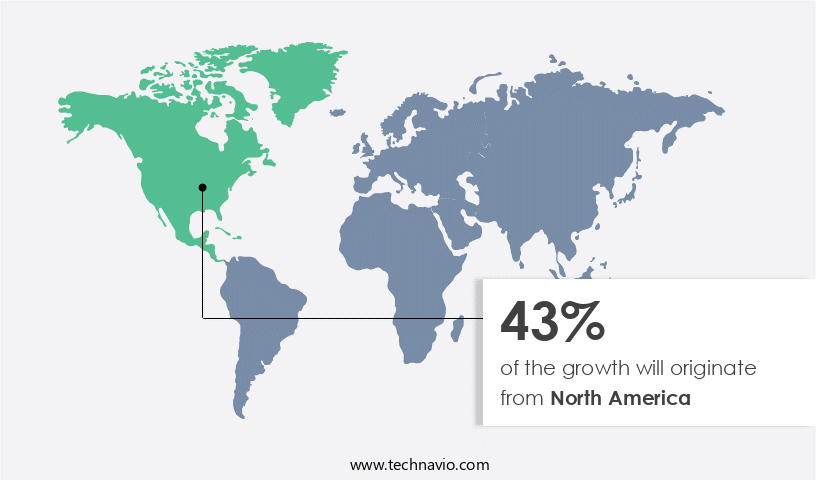

North America is estimated to contribute 43% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The North American defense industry, led by the US, is characterized by significant technological advancements and substantial investments in military mobile computing systems. The US military's reliance on these systems is crucial for mission-critical applications, including Intelligence, Surveillance, Reconnaissance (ISR), Data management, and ML-driven Big data analytics. With a defense budget exceeding USD750 billion in 2022, the US is the largest buyer of military equipment worldwide. The US Department of Defense (DoD) grants over 80% of its budget through the National Defense Authorization Act (NDAA), while the remaining funds support overseas contingency operations. These investments fuel the development of technologically advanced military computers, rugged tablets, laptops, handhelds, wearables, and avionics computers for use in airborne platforms, naval vessels, military aircraft, ground segments, commercial ships, and national navy.

The integration of AI, cybersecurity advancements, and cloud computing into military systems ensures enhanced safety purposes, interoperability, and cost-effective solutions for joint operations and coalition efforts In the defense landscape. However, with the increasing use of these systems, there are growing concerns regarding cybersecurity, data sovereignty, and insider threats, necessitating robust security measures, encryption mechanisms, access controls, intrusion detection, and prevention systems.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Military Mobile Computing Systems Industry?

- Greater focus on ISR operations is the key driver of the market.Military mobile computing systems play a crucial role In the defense sector, particularly in intelligence, surveillance, and reconnaissance (ISR) operations. ISR activities, which include real-time monitoring and information gathering, are essential for situational awareness and informed decision-making in high-risk military situations. These operations generate vast amounts of data from various sources, such as satellites, unmanned aerial vehicles (UAVs), ground sensors, and reconnaissance aircraft. Military computers, including rugged laptops, handhelds, wearables, and avionics computers, are integral to ISR operations. They enable mission-critical applications, such as data management, threat detection, and network connectivity, in war zones and military bases. Technologically advanced computers, including AI and ML-powered systems, are increasingly being adopted for predictive modeling and advanced analytics.

The military equipment landscape is evolving, with emerging threats necessitating cybersecurity advancements. Military organizations require cost-effective and flexible solutions to ensure data sovereignty, confidentiality, integrity, and security. Cloud computing provides a potential solution, offering scalability, interoperability, and real-time data analysis capabilities. However, it also raises concerns regarding cyber threats, data breaches, unauthorized access, and insider threats. Security measures such as encryption mechanisms, access controls, intrusion detection, and prevention systems are essential In the military context. Military computer software, including security policies, security audits, and security culture, plays a vital role in mitigating risks. The MCC ecosystem, which includes mission planning, threat detection, and network infrastructure, is a critical component of military operations.

The international market for military mobile computing systems is dynamic, with startups and private companies driving innovation alongside tech giants. The defense budget continues to prioritize cybersecurity focus, with encryption and security standards becoming increasingly important. The military computer industry is characterized by rapid prototyping, experimentation, and equipment performance optimization, as well as operational strategies to address emerging threats.

What are the market trends shaping the Military Mobile Computing Systems market?

- Ongoing digitization of battlefield operations is the upcoming market trend.Military mobile computing systems play a pivotal role In the defense sector, enabling modern armed forces to digitize battlefields through integrated and updated components. These systems are transforming military tactics with advanced technologies such as AI, biosensors, and 3D printable weaponry. Military computers, including rugged tablets and laptops, are integral to mission-critical applications like data management, intelligence, surveillance, and reconnaissance. Networked technologies, including avionics computers and pre-integrated forms, enhance military capabilities by providing real-time data analysis and advanced analytics for threat detection and predictive modeling. They enable military organizations to maintain situational awareness through sensors and surveillance systems, including social media and situational awareness displays.

Military equipment, including tanks and guided missile systems, benefit from these advanced technologies, enabling crews to make informed decisions and coordinate weapons purchases and border road development. The international market for military computer software, including portable computers and wearables, is growing, offering flexible and cost-effective solutions for military organizations. The defense landscape is evolving, with emerging threats requiring cybersecurity advancements, rapid prototyping, and experimentation for equipment performance and operational strategies. Cybersecurity concerns, including data breaches, unauthorized access, and cyber threats, necessitate robust security measures such as encryption mechanisms, access controls, intrusion detection, and prevention systems. Military bases and military aircraft, naval platforms, and ground segments rely on cloud computing and virtualized computing resources for network infrastructure, internet connectivity, and bandwidth capacity.

The air force segment is a significant market for tech giants, with a growing defense budget and cybersecurity focus. The MCC ecosystem, including mission planning, threat detection, and network connectivity, is essential for joint operations and coalition efforts.

What challenges does the Military Mobile Computing Systems Industry face during its growth?

- Cyber security threats associated with military communication systems is a key challenge affecting the industry growth.Military mobile computing systems play a crucial role in ensuring effective communication and data transmission between various military platforms, including armored vehicles and unmanned aerial vehicles (UAVs). These systems employ advanced technologies such as Artificial Intelligence (AI), biosensors, and 3D printable weaponry to enhance military capabilities. However, the reliance on these technologies also brings about significant security concerns. For instance, UAVs and unmanned armored vehicles, which lack onboard manual support, heavily rely on the parameters transmitted by onboard sensors to determine flight parameters. Any external interference affecting these data transmissions could have catastrophic consequences. Unencrypted wireless networks, such as Wi-Fi, pose a significant threat to military drones, as both devices cannot verify the integrity of the transmitted data.

The defense sector is witnessing a shift towards technologically advanced computers, including rugged, embedded, portable, and mission-critical computers, to address the increasing demand for cost-effective and flexible solutions in mission-critical applications. Military organizations are investing in cloud computing, ML, and big data analytics to improve data management, intelligence, surveillance, and reconnaissance capabilities. Cybersecurity advancements, including encryption, security policies, access controls, and intrusion detection, are essential to protect against cyber threats, data breaches, unauthorized access, and insider threats. The military landscape is continually evolving, with joint operations, coalition efforts, and emerging threats requiring advanced analytics, real-time data analysis, and predictive modeling.

The MCC ecosystem plays a vital role in mission planning, threat detection, network connectivity, and data transmission, enabling real-time communication and access to cloud resources and networking capabilities. Air Force segment, tech giants, and defense budgets are focusing on cybersecurity focus, encryption, and security standards to safeguard military data centers, cloud service providers, and virtualized computing resources. The need for security policies, security audits, and a strong security culture is paramount to mitigate cyberattacks, data sovereignty concerns, and security measures.

Exclusive Customer Landscape

The military mobile computing systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the military mobile computing systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, military mobile computing systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

ASELSAN AS - The company specializes in providing military mobile computing system solutions, encompassing a range of offerings such as Military Computers and Hand Held Terminals, Battlefield Management Systems, and Electronic Warfare and Information Systems. These advanced technologies enable military personnel to access real-time data and communication capabilities, enhancing operational efficiency and effectiveness in diverse terrain and environments. Military Computers and Hand Held Terminals offer ruggedized, portable solutions for mission-critical data processing and transmission. Battlefield Management Systems provide situational awareness and coordination capabilities, enabling effective command and control in dynamic environments. Electronic Warfare and Information Systems offer advanced intelligence, surveillance, and reconnaissance capabilities, providing valuable insights to inform strategic decision-making. Overall, these solutions enable military forces to maintain a technological edge on the battlefield and respond effectively to evolving threats.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ASELSAN AS

- BAE Systems Plc

- Collins Aerospace

- Curtiss Wright Corp.

- Elbit Systems Ltd.

- Getac Holdings Corp.

- Inmarsat Global Ltd.

- Israel Aerospace Industries Ltd.

- L3Harris Technologies Inc.

- Leonardo Spa

- Lockheed Martin Corp.

- Miltope

- Northrop Grumman Corp.

- Panasonic Holdings Corp.

- Rolta India Ltd.

- Saab AB

- Samsung Electronics Co. Ltd.

- Thales Group

- Viasat Inc.

- Zebra Technologies Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a diverse range of technologies and applications designed to meet the unique demands of modern armed forces. These systems are integral to various military platforms, including ground segments such as tanks and armored vehicles, as well as airborne and naval platforms like military aircraft and commercial ships. Military mobile computing systems are essential for mission-critical applications, including data management, intelligence, surveillance, and reconnaissance. They enable real-time data analysis, advanced analytics, and predictive modeling, enhancing situational awareness and operational strategies. The market is characterized by its technologically advanced offerings, with a focus on rugged, portable, and embedded computers, as well as rugged tablets and laptops.

The defense sector is increasingly adopting cloud computing as a cost-effective and flexible solution for its digital infrastructure. This shift towards cloud services has led to the emergence of pre-integrated forms of military computers, ensuring interoperability and joint operations among coalition efforts. However, the defense landscape faces numerous challenges, including cybersecurity advancements and emerging threats. Military organizations require robust cybersecurity measures to safeguard sensitive data from data breaches, unauthorized access, and cyberattacks. Security concerns extend to insider threats, confidentiality, integrity, and data sovereignty. As a result, there is a growing emphasis on security policies, security audits, security culture, encryption mechanisms, intrusion detection, and prevention systems.

The market for military mobile computing systems is driven by the need for rapid prototyping and experimentation to enhance equipment performance and operational strategies. ML and big data analytics are increasingly being utilized to analyze vast amounts of data in real-time, providing valuable insights for military decision-making. The market is not limited to traditional military organizations but also includes tech giants and private companies, contributing to the development of military computer software, avionics computers, and other advanced technologies. The international market for military mobile computing systems is vast and dynamic, with ongoing advancements in AI technology, biosensors, and 3D printable weaponry shaping the future of military computing.

The military bases of today are increasingly connected, with network infrastructure and internet connectivity enabling real-time communication and data transmission. Virtual private networks and dedicated communication channels provide secure connectivity solutions, while public clouds and virtualized computing resources offer flexible and cost-effective options. In conclusion, the market is a critical component of the defense sector, driving innovation and enabling mission-critical applications in various military platforms. The market is characterized by its focus on advanced technologies, cybersecurity, and interoperability, ensuring the modern armed forces remain technologically superior and prepared for emerging threats.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

183 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.45% |

|

Market growth 2024-2028 |

USD 1832.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.42 |

|

Key countries |

US, China, Russia, India, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Military Mobile Computing Systems Market Research and Growth Report?

- CAGR of the Military Mobile Computing Systems industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the military mobile computing systems market growth of industry companies

We can help! Our analysts can customize this military mobile computing systems market research report to meet your requirements.

RIA -

RIA -