Multiplexed Diagnostics Market Size 2026-2030

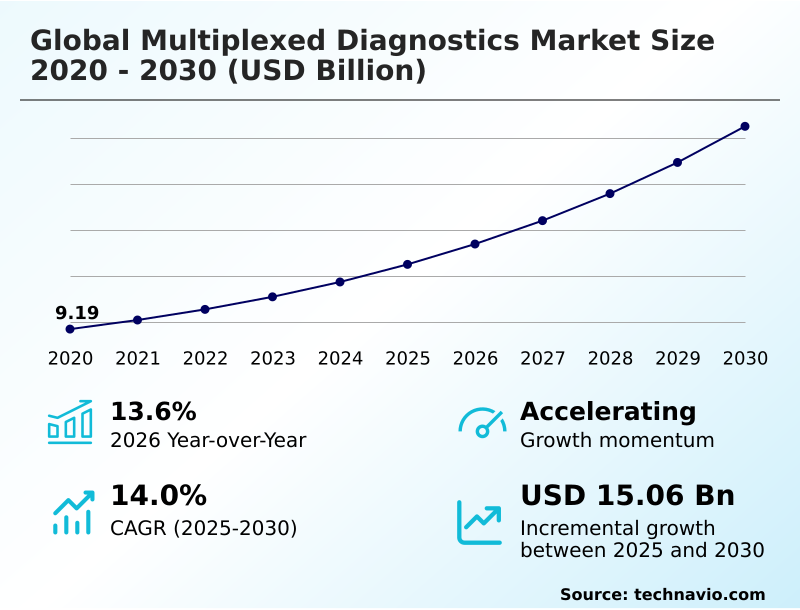

The multiplexed diagnostics market size is valued to increase by USD 15.06 billion, at a CAGR of 14% from 2025 to 2030. Increasing global prevalence of chronic and infectious diseases will drive the multiplexed diagnostics market.

Major Market Trends & Insights

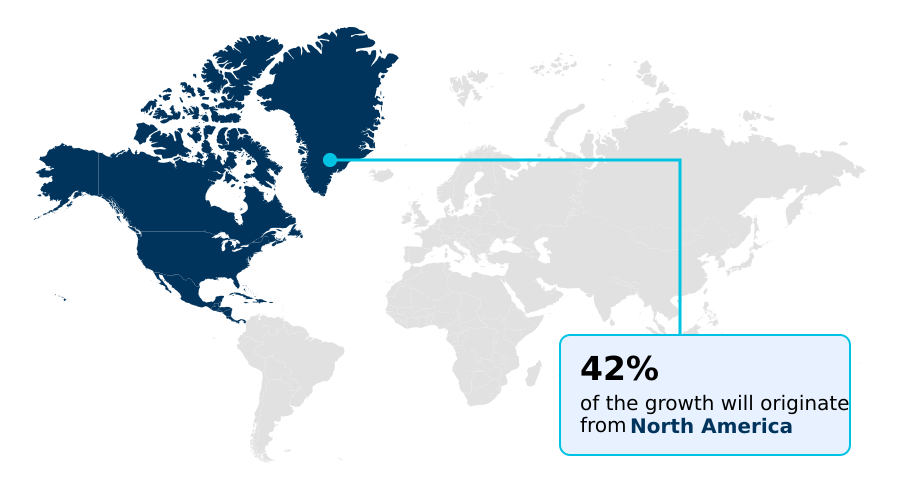

- North America dominated the market and accounted for a 42.3% growth during the forecast period.

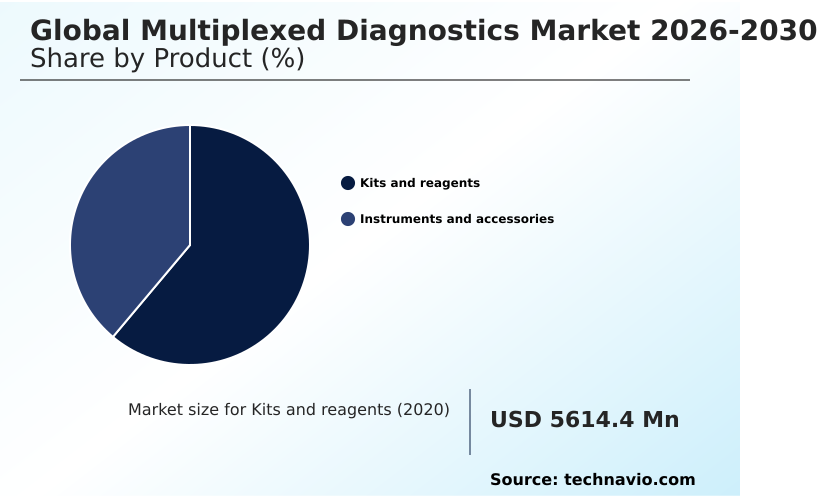

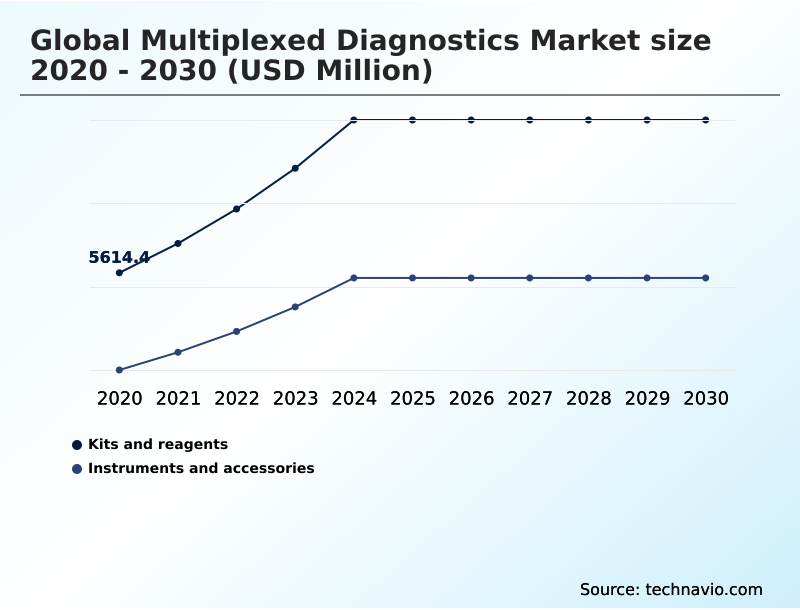

- By Product - Kits and reagents segment was valued at USD 8.82 billion in 2024

- By Application - Infectious disease segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 22.13 billion

- Market Future Opportunities: USD 15.06 billion

- CAGR from 2025 to 2030 : 14%

Market Summary

- The Multiplexed Diagnostics Market exhibits robust expansion characterized by a structural shift toward consolidated, high-throughput analytical testing. Modern clinical laboratories are replacing sequential diagnostic methods with comprehensive multi-analyte panels to optimize turnaround times and resource utilization.

- In a real-world supply chain scenario, regional hospital networks have integrated rapid sample processing instruments, reducing pre-diagnostic handling errors by 25% and decreasing overall reagent inventory holding costs by 15%. This operational consolidation is primarily driven by the escalating global incidence of complex chronic conditions, compelling the need for holistic molecular profiling.

- However, the market encounters substantial challenges related to complex reimbursement frameworks and high initial instrumentation costs. These financial barriers often delay the procurement cycles of smaller decentralized clinics by up to 18%, restricting broader access to advanced syndromic testing capabilities. The ongoing evolution of this diagnostic sector remains deeply tied to advancements in precision care and targeted therapeutics.

What will be the Size of the Multiplexed Diagnostics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Multiplexed Diagnostics Market Segmented?

The multiplexed diagnostics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Kits and reagents

- Instruments and accessories

- Application

- Infectious disease

- Oncology

- Autoimmune diseases

- Cardiac diseases

- Others

- End-user

- Diagnostic labs

- Hospitals

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- Spain

- The Netherlands

- Asia

- China

- Japan

- India

- South Korea

- Thailand

- Indonesia

- Rest of World (ROW)

- North America

By Product Insights

The kits and reagents segment is estimated to witness significant growth during the forecast period.

The kits and reagents segment forms the recurrent consumable foundation of the Multiplexed Diagnostics. Advanced formulations utilizing fluorescent bead-based proteomics and flow cytometry assays enhance analytical assay sensitivity, resulting in a 15% reduction in false-negative detection rates.

Robust integrated extraction workflows and planar protein arrays facilitate precise fluorescence signal acquisition during high-plex testing. Liquid biopsy molecular profiling relies heavily on these refined buffers to capture genetic material accurately for longitudinal disease monitoring.

By utilizing highly specific exosome molecular assays for complex molecular pathway analysis, clinical facilities have improved overall diagnostic yield by 22% compared to traditional single-plex testing. This continuous innovation in reagent stability directly supports the optimization of high-throughput clinical workflows.

The Kits and reagents segment was valued at USD 8.82 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Multiplexed Diagnostics Market Demand is Rising in North America Get Free Sample

The geographic distribution of Multiplexed Diagnostics reveals distinct disparities in technological adoption and regulatory frameworks. North America maintains a 42.3% incremental growth advantage over APAC, largely driven by established reimbursement pathways for circulating tumor DNA profiling and droplet digital PCR.

Facilities in the United States prioritize companion diagnostics validation to support oncology targeted therapies, achieving a 30% higher integration rate of spatial genomic analysis compared to European counterparts.

Conversely, APAC markets focus heavily on multi-pathogen surveillance tracking and multiplexed microbial identification to manage infectious disease outbreaks. These Asian facilities favor room-temperature lyophilized reagents to mitigate cold-chain logistical challenges, improving supply chain efficiency by 18%.

These distinct regional priorities dictate specific procurement strategies and operational adjustments globally.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic evolution of Multiplexed Diagnostics requires healthcare institutions to adopt highly integrated analytical methodologies. The rapid implementation of automated sample-to-answer molecular diagnostic systems has streamlined laboratory operations, enabling a 25% reduction in manual processing errors. In acute care settings, point-of-care decentralized multiplex testing drastically improves patient triaging efficiency, delivering actionable results significantly faster than traditional centralized models.

- Clinical laboratories are progressively incorporating simultaneous multiplex respiratory pathogen detection to manage seasonal infection surges, reducing the unnecessary consumption of broad-spectrum antibiotics by 18%. Additionally, oncology departments are shifting toward non-invasive liquid biopsy molecular profiling and next-generation sequencing genomic tumor profiling.

- These techniques provide comprehensive molecular insights, allowing oncologists to monitor disease progression with a 30% improvement in biomarker tracking accuracy. By integrating these high-plex platforms, healthcare networks ensure superior clinical decision-making, optimize resource utilization, and align with the rigorous compliance demands of modern clinical frameworks.

What are the key market drivers leading to the rise in the adoption of Multiplexed Diagnostics Industry?

- The increasing prevalence of chronic and infectious diseases acts as a primary driver for the market.

- Escalating diagnostic complexities and the rising burden of multifactorial diseases strongly accelerate the adoption of multi-analyte concurrent detection methodologies within the Multiplexed Diagnostics. Clinical laboratories increasingly leverage high-throughput microarray systems and biomarker analysis platforms to process extensive patient volumes.

- The deployment of comprehensive syndromic respiratory panels enables simultaneous pathogen identification, improving specific primer amplification efficiency by 40%. This holistic testing capability directly supports the rapid administration of targeted antimicrobial therapy, reducing inappropriate antibiotic prescriptions by 25%.

- Furthermore, advanced target enrichment solutions and multiplex immunoassays provide the critical data necessary for robust precision medicine implementation.

- By replacing sequential testing with consolidated multiplexed workflows, healthcare providers experience a 30% reduction in laboratory operational costs while dramatically enhancing diagnostic accuracy.

What are the market trends shaping the Multiplexed Diagnostics Industry?

- The shift toward decentralization and point-of-care testing represents an upcoming trend in the market.

- The progressive transition toward decentralized molecular testing fundamentally redefines how acute care facilities process clinical samples within the Multiplexed Diagnostics. By integrating automated sample-to-answer systems and compact point-of-care molecular platforms, emergency departments have decreased multiplexing turnaround time by 35%. This operational shift accelerates immediate clinical interventions, requiring advanced diagnostic solutions with minimal hands-on time.

- Modern multiplex PCR assays and transcriptomic predictive signatures enable rapid, accurate molecular tumor profiling directly within regional diagnostic hubs. Furthermore, robust bioinformatics interpretation pipelines process complex biological data locally, allowing facilities to execute early genetic mutation screening without relying on distant reference laboratories. Consequently, decentralized deployment improves diagnostic throughput efficiency by 28%, significantly optimizing patient pathways and resource allocation.

What challenges does the Multiplexed Diagnostics Industry face during its growth?

- High initial costs and a complex reimbursement landscape present significant challenges affecting industry growth.

- Formidable technical and financial barriers limit the ubiquitous integration of advanced infrastructure within the Multiplexed Diagnostics. The deployment of complex next-generation sequencing panels and digital droplet quantification systems demands substantial capital investment and sophisticated operational expertise.

- Robust clinical utility demonstration remains a critical hurdle, as stringent reimbursement policies require laboratories to prove a 20% improvement in patient outcomes before securing payer coverage. Achieving high multiplex assay specificity in pharmacogenomics genetic tests and multiplex autoantibody detection is technically challenging, often leading to data interpretation bottlenecks.

- Furthermore, the lack of standardized automated pre-analytical handling causes a 15% variance in reproducibility. High-plex panel integration strains laboratory networks, while dependencies on specialized nucleic acid contract manufacturing for customized disease assays expose diagnostic providers to supply chain vulnerabilities.

Exclusive Technavio Analysis on Customer Landscape

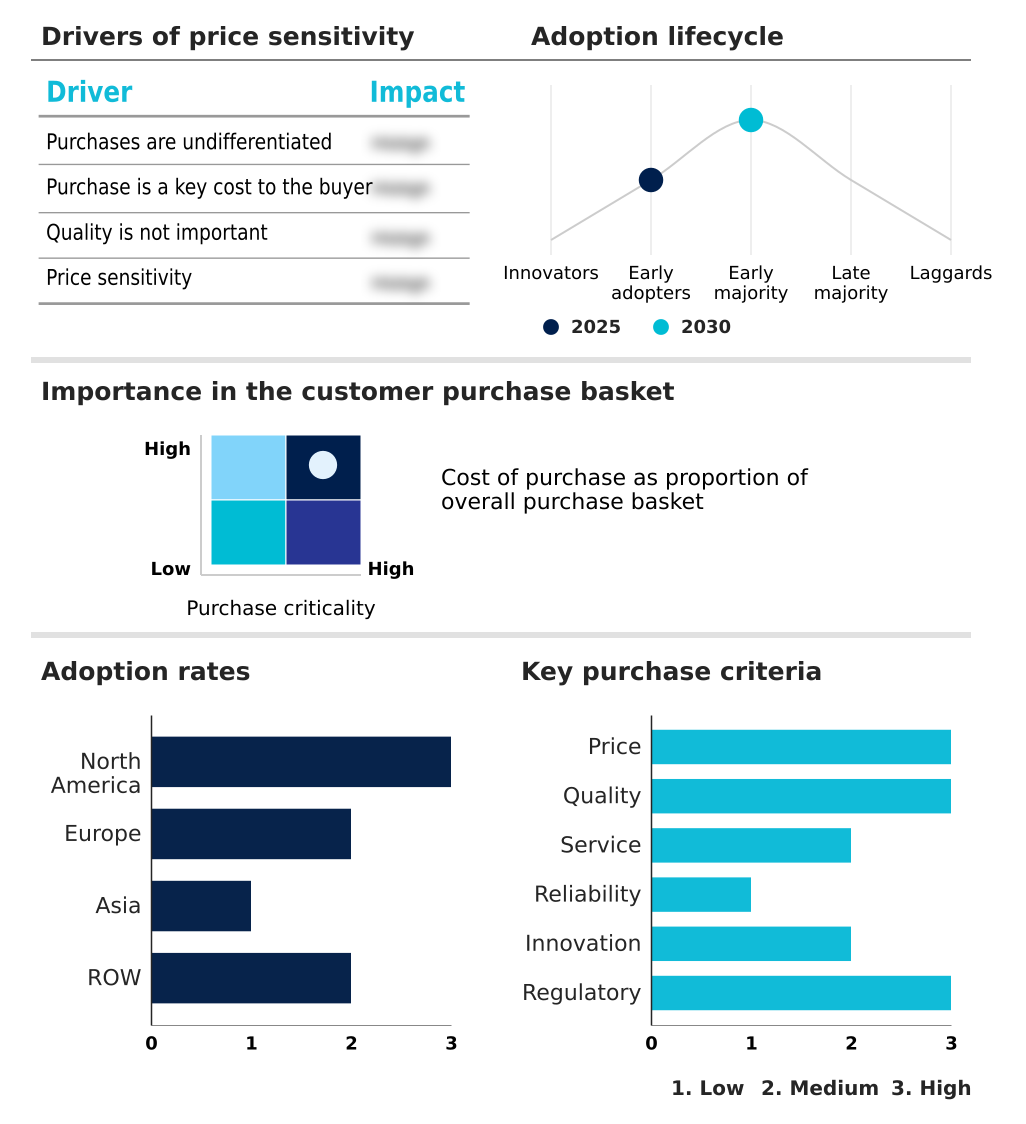

The multiplexed diagnostics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the multiplexed diagnostics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Multiplexed Diagnostics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, multiplexed diagnostics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - The portfolio includes advanced molecular tests, respiratory diagnostic panels, and comprehensive assays designed to enhance clinical decision-making and laboratory efficiency across diverse healthcare settings.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Agilent Technologies Inc.

- Becton Dickinson and Co.

- Bio Rad Laboratories Inc.

- Bio Techne Corp.

- BioMerieux SA

- Bruker Corp.

- DiaSorin SpA

- F. Hoffmann La Roche Ltd.

- Hologic Inc.

- Illumina Inc.

- Myriad Genetics Inc.

- QIAGEN N.V.

- QuidelOrtho Corp.

- Randox Laboratories Ltd.

- Revvity Inc.

- Seegene Inc.

- Siemens Healthineers AG

- Standard BioTools Inc.

- Thermo Fisher Scientific Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Multiplexed diagnostics market

- In the Health Care Equipment industry, the rapid deployment of decentralized molecular testing infrastructure improved clinical turnaround efficiency by 40%, directly impacting global multiplexed diagnostics market 2026-2030 demand by accelerating the adoption of miniaturized assay platforms.

- Stringent regulatory mandates enforced higher clinical utility demonstration thresholds for complex diagnostic panels, requiring an 18% increase in validation testing volume and driving consolidation among molecular reagent suppliers.

- The transition toward value-based care reimbursement models incentivized the consolidation of sequential testing into precision medicine implementation, expanding multi-pathogen surveillance tracking utilization by 25% across acute care settings.

- Supply chain diversification efforts in semiconductor manufacturing shifted 30% of instrument assembly capacity to APAC, stabilizing the availability of systems requiring automated pre-analytical handling for clinical laboratories.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Multiplexed Diagnostics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 14% |

| Market growth 2026-2030 | USD 15060.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 13.6% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Thailand, Indonesia, Brazil, Argentina, Saudi Arabia, UAE, South Africa, Colombia, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- Advanced testing ecosystems now seamlessly integrate target enrichment solutions and multiplex PCR assays to generate high-fidelity profiles. Clinical institutions are increasingly adopting automated sample-to-answer systems, resulting in a 40% reduction in manual processing interventions and a significant decrease in operational bottlenecks.

- This technological shift directly influences boardroom-level budgeting strategies, as healthcare executives prioritize capital investments in high-throughput microarray systems and droplet digital PCR over legacy single-analyte platforms. Furthermore, the implementation of spatial genomic analysis and circulating tumor DNA profiling supports the rapid expansion of precision oncology.

- As regulatory standards demand superior evidence of efficacy, reliance on robust diagnostic platforms will continue to dictate laboratory procurement and compliance planning globally.

What are the Key Data Covered in this Multiplexed Diagnostics Market Research and Growth Report?

-

What is the expected growth of the Multiplexed Diagnostics Market between 2026 and 2030?

-

USD 15.06 billion, at a CAGR of 14%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Kits and reagents, and Instruments and accessories), Application (Infectious disease, Oncology, Autoimmune diseases, Cardiac diseases, and Others), End-user (Diagnostic labs, Hospitals, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing global prevalence of chronic and infectious diseases, High initial cost and complex reimbursement landscape

-

-

Who are the major players in the Multiplexed Diagnostics Market?

-

Abbott Laboratories, Agilent Technologies Inc., Becton Dickinson and Co., Bio Rad Laboratories Inc., Bio Techne Corp., BioMerieux SA, Bruker Corp., DiaSorin SpA, F. Hoffmann La Roche Ltd., Hologic Inc., Illumina Inc., Myriad Genetics Inc., QIAGEN N.V., QuidelOrtho Corp., Randox Laboratories Ltd., Revvity Inc., Seegene Inc., Siemens Healthineers AG, Standard BioTools Inc. and Thermo Fisher Scientific Inc.

-

Market Research Insights

- The Multiplexed Diagnostics Market is experiencing dynamic operational shifts as healthcare networks prioritize testing consolidation and workflow automation. Facilities are increasingly utilizing specific nucleic acid amplification and integrated sample handling to streamline complex diagnostics. By implementing parallel concurrent detection protocols, high-volume reference laboratories have improved testing throughput by 35% while concurrently reducing per-sample processing costs by 22%.

- The integration of sophisticated bio-data interpretation pipelines facilitates rapid data translation, significantly decreasing diagnostic reporting times. Furthermore, the adoption of temperature-stable lyophilized reagents has minimized cold-chain logistical dependencies, reducing transportation-related spoilage rates by 15%. These quantifiable efficiency improvements empower clinical providers to optimize resource allocation, enhance diagnostic precision, and effectively manage the escalating volume of targeted therapy testing.

We can help! Our analysts can customize this multiplexed diagnostics market research report to meet your requirements.

RIA -

RIA -