Personal Identity Management Market Size 2024-2028

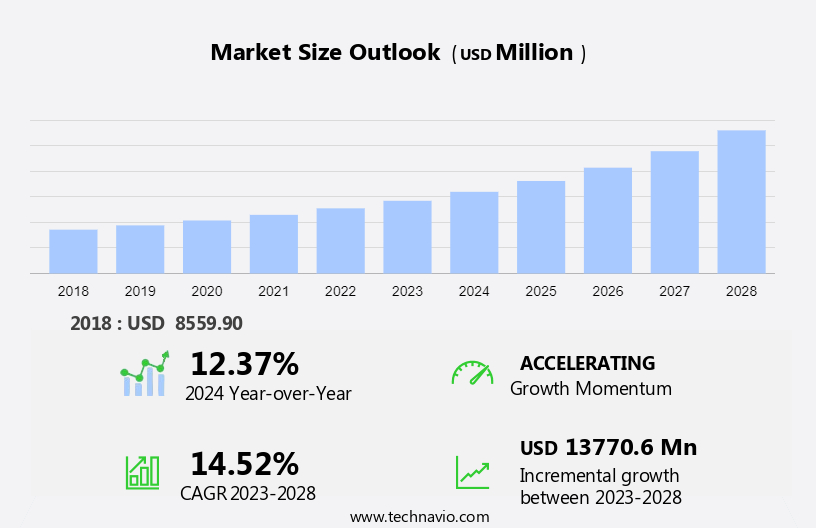

The personal identity management market size is forecast to increase by USD 13.77 billion at a CAGR of 14.52% between 2023 and 2028. The Personal Identity Management (PIM) market is experiencing significant growth due to the integration of technology in various sectors such as media and entertainment, healthcare, and economic development. Technological advancements, including automated meter infrastructure and cloud computing, are driving the real-time data collection and processing requirements for modern electric meters. This trend is expected to continue as the economy develops and reliance on digital platforms increases. Moreover, the media and entertainment industry's shift towards biometric authentication for content access is fueling the demand for PIM solutions. Healthcare providers are also adopting PIM to secure patient data and ensure privacy compliance. However, the emergence of open-source personal identity management solutions poses a threat to market players. CA Technologies and other key players must focus on offering advanced features and services to maintain their competitive edge. In summary, the PIM market is witnessing growth due to the expansion of IoT networks, increasing adoption of face biometrics, and the need for secure data processing in various industries. However, open-source solutions pose a challenge to market players, necessitating continuous innovation and improvement. Key players must focus on offering advanced features and services to maintain their market position.

Organizations manage vast amounts of customer profile data and employee information, which is essential for delivering products and services. Effective identity management is crucial in safeguarding this data and enhancing the customer experience. Personal identity management (PIM) plays a pivotal role in this process. PIM encompasses the processes and technologies that enable organizations to manage and protect the digital and non-digital identities of customers and employees. This includes managing customer profile databases, authentication, and security procedures across various touchpoints such as mobile devices, laptops, and tablets. The increasing use of IoT devices and cloud computing in various industry verticals, including education, public sector, media, entertainment, healthcare, and technological advancements like automated meter infrastructure, necessitates identity management solutions.

Furthermore, data security initiatives have become a top priority for organizations due to the escalating cyber threats. PIM helps mitigate these risks by implementing secure authentication methods and protecting customer profile databases. The integration of PIM with mobile devices, laptops, and tablets enables seamless and secure access to data. PIM is not limited to digital data. It also covers managing non-digital identities, ensuring that physical access to premises and assets is controlled and secure. Technological advancements in PIM include automated meter infrastructure and cloud computing, which offer scalability, flexibility, and cost savings. These advancements enable organizations to manage and secure their identity data more effectively and efficiently.

In conclusion, personal identity management is a critical component of an organization's data security strategy. It ensures the protection of customer profile data and employee information across various touchpoints, including mobile devices, laptops, tablets, and physical access points. By implementing PIM solutions, organizations can enhance the customer experience, protect against cyber threats, and safeguard their digital and non-digital identities.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

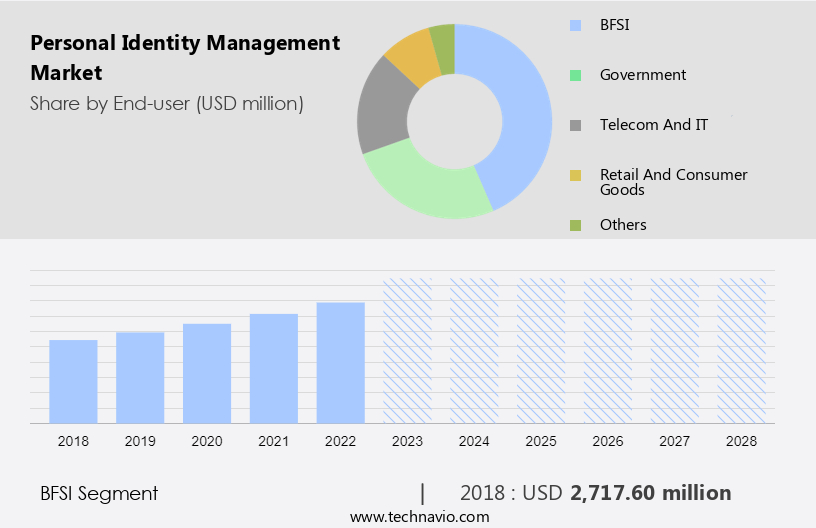

- End-user

- BFSI

- Government

- Telecom and IT

- Retail and consumer goods

- Others

- Deployment

- On-premise

- Cloud-based

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Middle East and Africa

- South America

- North America

By End-user Insights

The BFSI segment is estimated to witness significant growth during the forecast period. The Personal Identity Management (PIM) market witnessed significant growth in 2023, with the BFSI industry vertical leading in terms of value. This sector's dominance is attributed to the increasing digital transformation and regulatory compliance, resulting in the adoption of PIM solutions by banks and financial institutions. With the rising sophistication of cyber threats, it is essential for BFSI organizations to manage their identity data effectively. However, the fragmented implementation of various technologies and architectures results in information silos. To mitigate this, BFSI firms are turning to comprehensive strategies that consolidate information, thereby enhancing security. This trend has led to a growth in demand for PIM solutions in the sector.

Furthermore, PIM solutions offer various functionalities, including content management, access control, professional services, implementation, training, and support. These solutions enable organizations to securely manage and protect sensitive data, ensuring regulatory compliance and data privacy. The market is expected to continue its growth trajectory during the forecast period, driven by the increasing need for secure identity management across industries. Geographically, North America is a significant market for PIM solutions due to the presence of major players and stringent regulatory requirements. Europe and Asia Pacific are also expected to show substantial growth due to the increasing adoption of digital technologies and the need for data security.

In conclusion, the market is witnessing significant growth, driven by the increasing need for secure identity management in various industry verticals. The BFSI sector is leading the market due to the growing adoption of digital transformation and regulatory compliance. PIM solutions offer various functionalities, including content management, access control, professional services, implementation, training, and support, making them essential for organizations to secure their sensitive data. The market is expected to continue its growth trajectory, driven by the increasing need for secure identity management across industries and geographies.

Get a glance at the market share of various segments Request Free Sample

The BFSI segment was valued at USD 2.72 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

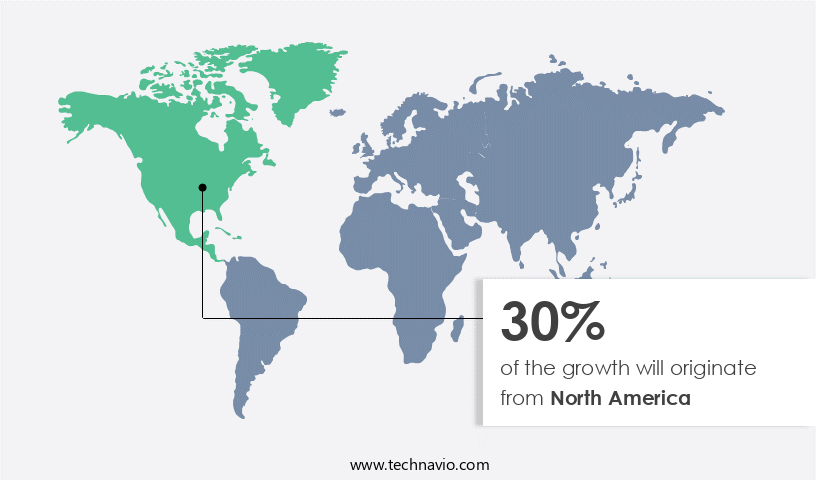

North America is estimated to contribute 30% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In North America, the increasing need for IT and telecom businesses to ensure data security against cyber threats has led to a significant rise in the adoption of personal identity management (PIM) solutions. Malicious actors continue to target enterprises with cyberattacks, resulting in data theft cases that can negatively impact economies. To mitigate these risks, governments in North America are implementing regulations to enforce IT security compliance and governance.

Additionally, the BFSI and industrial sectors, which handle sensitive data, are increasingly adopting PIM solutions to improve their delivery systems' quality. These factors are driving the growth of the PIM market in North America. The complex process of implementing PIM solutions can be time-consuming but is essential for businesses to protect their mobile apps and confidential data from cyber threats.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The rapid growth of IoT networks is the key driver of the market. In today's digital world, organizations are generating vast amounts of both digital and non-digital data from various sources, including customers and employees. Effective management of this data is crucial for delivering personalized products and services, enhancing customer experience, and ensuring data security. However, with the increasing adoption of Internet of Things (IoT) technology, IoT service providers are facing challenges in implementing identity management systems. Neglecting backend systems for IoT security can lead to vulnerabilities, such as privacy violations, security attacks, and poor customer experiences. Furthermore, enterprises are concerned about unauthorized access to devices, external hackers, and denial of service (DoS) attacks.

Furthermore, Personal Identity Management (PIM) plays a vital role in addressing these concerns. PIM solutions enable organizations to manage and secure customer profile data, ensuring access governance, security, and privacy management. By implementing PIM, businesses can provide a seamless customer experience, build trust, and enhance brand reputation. Investing in PIM solutions can help organizations mitigate risks, comply with regulations, and improve overall operational efficiency. With the growing importance of data security and privacy, PIM is no longer an optional feature but a necessity for businesses looking to succeed in today's digital landscape.

Market Trends

The growing adoption of face biometrics is the upcoming trend in the market. Biometric technologies, such as face and gait scanners, are gaining significance in various sectors, including media and entertainment, healthcare, and technological advancements. Data privacy and cybersecurity concerns are driving the growth of the Personal Identity Management (PIM) market. In February 2020, Mastercard Inc. Revealed plans to collaborate with transport operators to create biometric ticketing solutions, enabling automatic passenger identification as they board services. Mastercard is also exploring the integration of advanced behavioral biometrics, including gait, face, heartbeat, and veins, for future payment systems, ensuring secure transactions. Market companies are continually launching innovative products, such as automated meter infrastructure, cloud computing, real-time data, and economic development initiatives, to cater to the evolving needs of businesses and consumers.

Additionally, CA Technologies, for instance, offers Identity and Access Management solutions that ensure secure access to applications and systems. These solutions enable organizations to manage digital identities, protect against cyber threats, and maintain regulatory compliance. In summary, the PIM market is witnessing significant growth due to the increasing adoption of biometric technologies and the need for secure data management and identity protection.

Market Challenge

The threat from open-source personal identity management solutions is a key challenge affecting the market growth. Open-source personal identity management solutions pose a significant challenge to the established market for on-premises and cloud-based personal identity management systems. These open-source solutions can be freely downloaded and implemented across various platforms, including mobile devices, laptops, and tablets. They have gained popularity in economies such as India and China, where many small and medium-sized enterprises (SMEs) cannot afford expensive on-premises or cloud-based alternatives.

However, by opting for open-source solutions, these enterprises can reduce upfront costs and enjoy greater flexibility. In the face of increasing data security initiatives and cyber threats, the need for security procedures is more critical than ever. The Internet of Things (IoT) is expanding the attack surface, making it essential for industry verticals such as education and the public sector to prioritize personal identity management. Open-source solutions offer a cost-effective and adaptable alternative for businesses seeking to enhance their security while minimizing expenses.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Dell Technologies Inc. - The company offers Dell One Identity as a service which helps to achieve identity and access management objectives of administration, governance, and compliance quickly.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AO Kaspersky Lab

- Avatier Corp.

- Broadcom Inc.

- Constellation Software Inc.

- CyberArk Software Ltd.

- Delinea Inc.

- Experian Plc

- International Business Machines Corp.

- Microsoft Corp.

- Okta Inc.

- Open Text Corporation

- Oracle Corp.

- Ping Identity Corp.

- Quest Software Inc.

- SailPoint Technologies Inc.

- Salesforce Inc.

- Thales Group

- VMware Inc.

- Zoho Corp. Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Personal identity management has become a critical area of focus for organizations as they seek to manage both digital and non-digital data related to their customers and employees. With the increasing use of products and services that require authentication, such as mobile devices, laptops, tablets, and IoT devices, the need to secure personal identity data has become paramount. Data security initiatives have taken center stage due to the growing threats of cyberattacks and data theft cases. The market caters to various industry verticals, including education, public sector, media, entertainment, healthcare, and IT & telecom. These industries generate vast amounts of personal identity data, including customer profile data, behavioral data, identity data, derived data, and self-identified data.

Moreover, technological advancements, such as cloud computing, automated meter infrastructure, and real-time data, have further complicated the management of personal identity data. Organizations require professional services, including implementation, training, support, consulting, and managed services, to deploy and manage personal identity management solutions. The process of implementing and managing personal identity management solutions can be complex and time-consuming, requiring expertise in access control, content management, and IT infrastructure. Personal identity management is essential for ensuring a positive customer experience, as it enables secure access to products and services while protecting sensitive data. It is also crucial for organizations to comply with government regulations and industry standards related to data security and privacy.

In conclusion, the market is expected to grow significantly due to the increasing use of biometrics for unique identification and the growing threats of cyber frauds in retail, banking, energy, utility, consumer goods, manufacturing, and other sectors. Organizations must stay up-to-date with the latest technological advancements and security procedures to protect their customers' and employees' personal identity data from cyber threats.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

172 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 14.52% |

|

Market growth 2024-2028 |

USD 13.77 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

12.37 |

|

Regional analysis |

North America, Europe, APAC, Middle East and Africa, and South America |

|

Performing market contribution |

North America at 30% |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

AO Kaspersky Lab, Avatier Corp., Broadcom Inc., Constellation Software Inc., CyberArk Software Ltd., Delinea Inc., Dell Technologies Inc., Experian Plc, International Business Machines Corp., Microsoft Corp., Okta Inc., Open Text Corporation, Oracle Corp., Ping Identity Corp., Quest Software Inc., SailPoint Technologies Inc., Salesforce Inc., Thales Group, VMware Inc., and Zoho Corp. Pvt. Ltd. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -