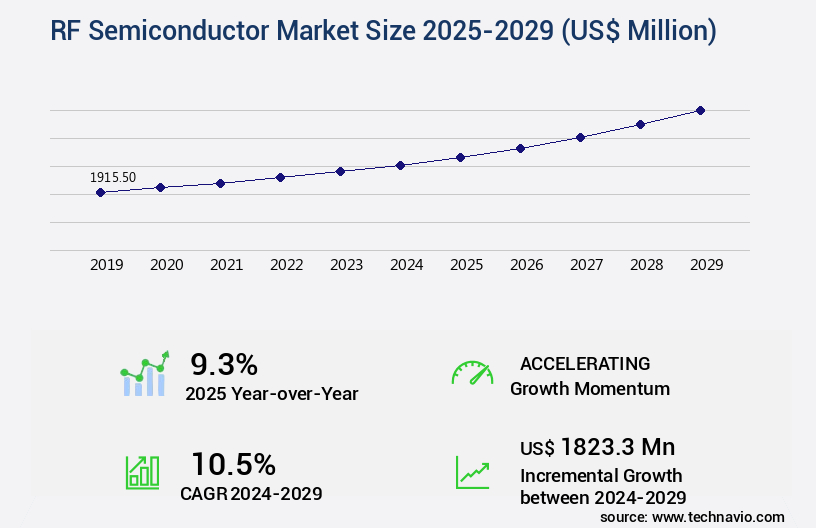

RF Semiconductor Market Size 2025-2029

The rf semiconductor market size is valued to increase by USD 1.82 billion, at a CAGR of 10.5% from 2024 to 2029. Increasing demand for RF devices for smartphones will drive the rf semiconductor market.

Market Insights

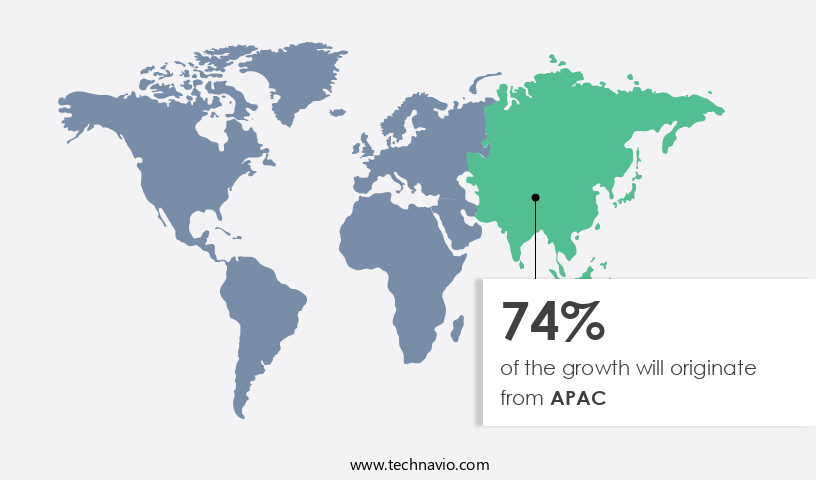

- APAC dominated the market and accounted for a 74% growth during the 2025-2029.

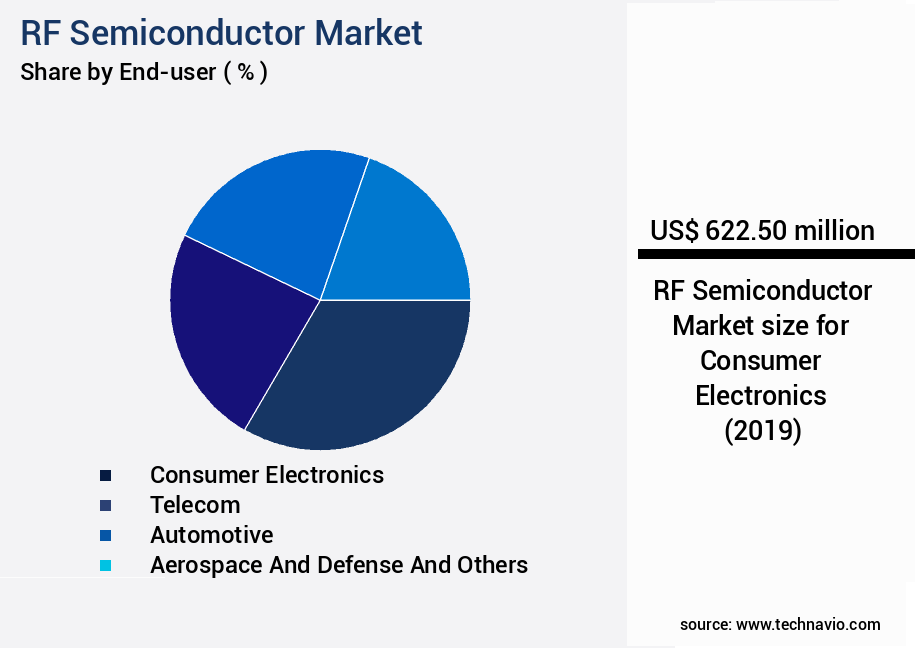

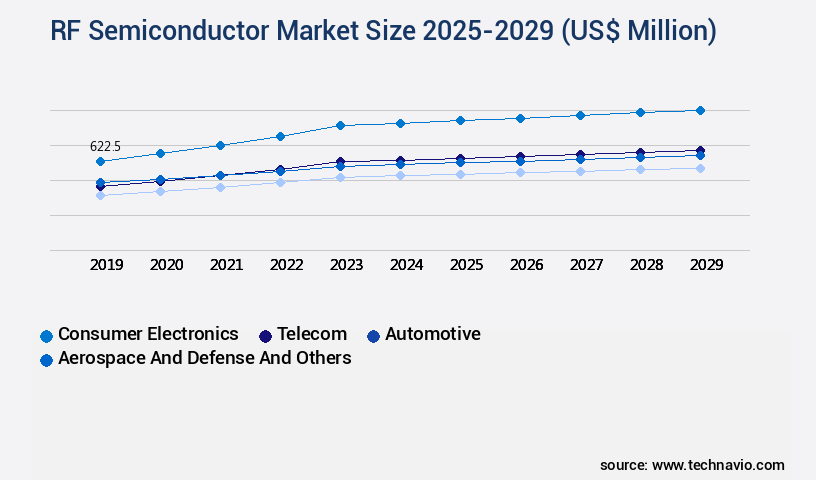

- By End-user - Consumer Electronics segment was valued at USD 622.50 billion in 2023

- By Product - RF filters segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 141.70 million

- Market Future Opportunities 2024: USD 1823.30 million

- CAGR from 2024 to 2029 : 10.5%

Market Summary

- RF semiconductors play a pivotal role in various industries, from telecommunications to defense and automotive, due to their ability to facilitate wireless communication and sensor applications. The market for RF semiconductors is driven by the increasing demand for advanced RF devices in smartphones and other consumer electronics, as well as the growing importance of RF technology in radar and electronic warfare systems. However, the high production cost of RF semiconductors poses a significant challenge for manufacturers. One real-world business scenario where RF semiconductors make a significant impact is in supply chain optimization. Companies in the electronics industry strive to maintain a steady supply of RF components to meet the demands of their customers.

- By implementing advanced supply chain management systems, these companies can monitor their inventory levels and forecast future demand, ensuring that they have an adequate stock of RF semiconductors on hand to meet production requirements. This not only enhances operational efficiency but also helps to mitigate the risk of supply disruptions and potential revenue losses. The market is characterized by ongoing technological advancements, with a focus on miniaturization, higher frequency operation, and improved power efficiency. These trends are driven by the need for smaller, more energy-efficient devices and the increasing demand for high-speed wireless communication. Additionally, the emergence of the Internet of Things (IoT) and Industry 4.0 is expected to further fuel the growth of the market, as these technologies rely heavily on wireless communication and sensor applications.

What will be the size of the RF Semiconductor Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- RF semiconductors play a pivotal role in various industries, including radar systems, satellite communication, and wireless communication. The market for these components is continually evolving, with advancements in modulation techniques, design for manufacturing, and packaging technology driving innovation. For instance, the integration of 5G technology in IoT devices necessitates semiconductors with improved electromagnetic compatibility and power consumption. Passive components, such as coaxial cables and stripline circuits, are essential for signal processing and transmission lines. Active components, including integrated circuits and semiconductor devices, are integral to the functionality of radar systems and satellite communication equipment. Compliance testing and thermal management are critical considerations in the development of RF semiconductors, ensuring electromagnetic compatibility and reducing power consumption.

- Cost reduction is a significant boardroom-level decision area for companies in this sector. According to recent research, the implementation of advanced yield improvement techniques has led to a substantial decrease in manufacturing costs for RF semiconductors. This cost reduction enables businesses to offer more competitive pricing, making their products more attractive to consumers and increasing market share. In summary, the market is a dynamic and evolving landscape, with ongoing advancements in modulation techniques, design for manufacturing, and packaging technology shaping the industry. Companies focusing on cost reduction through yield improvement techniques are well-positioned to succeed in this competitive market.

Unpacking the RF Semiconductor Market Landscape

In the dynamic the market, harmonious receiver design is a critical factor for minimizing harmonic distortion and ensuring optimal antenna performance. RFIC design plays a pivotal role in enhancing linearity performance through improved load pull and impedance matching. Oscillator design and system integration are essential for maintaining high-frequency components' stability and efficiency. High-power amplifiers and filter design are key components in RF power amplifier systems, delivering power efficiency gains of up to 30% compared to traditional designs. Mixer design and microwave circuits enable seamless signal generation and vector network analysis, while electromagnetic simulation and circuit simulation streamline the development process. Power dividers, matched filters, and directional couplers are integral to maintaining signal integrity and achieving optimal noise figure. Signal generators and frequency synthesizers provide precise control over input signals, while spectrum analyzers and low-noise amplifiers facilitate accurate measurement and analysis. Gain compression and intermodulation distortion are crucial performance metrics, with improvements leading to enhanced system reliability and ROI. By focusing on these aspects, businesses can align with industry regulations and ensure their RF semiconductor solutions deliver superior performance.

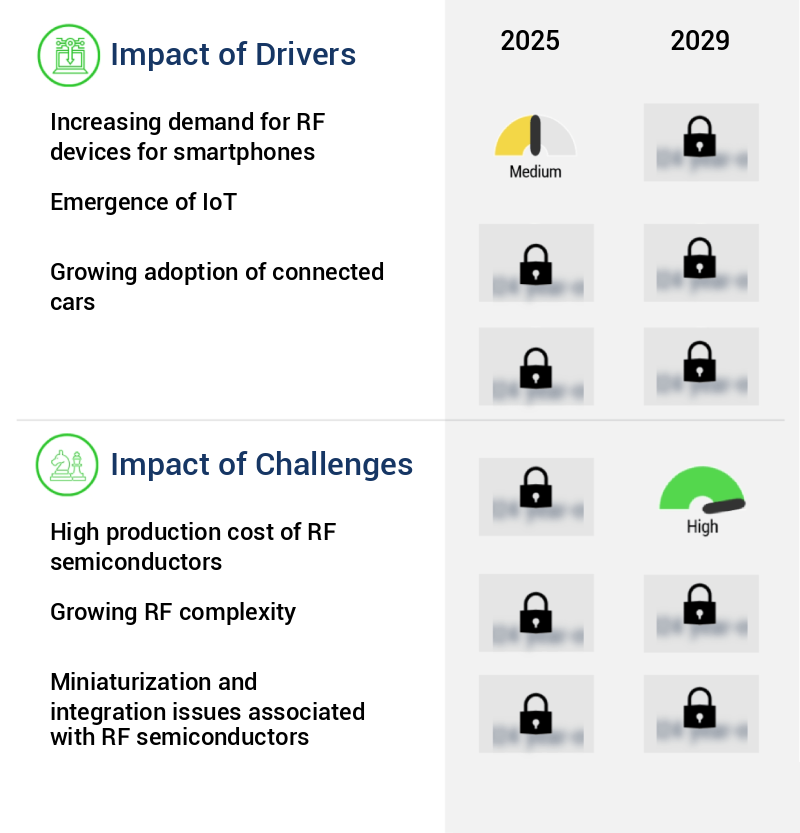

Key Market Drivers Fueling Growth

The escalating need for RF devices in the production of advanced smartphones serves as the primary market catalyst.

- The market is experiencing significant growth due to the increasing penetration of smartphones and the development of high-speed network infrastructure. With the forecasted rise in smartphone usage, the demand for RF semiconductor devices is set to increase substantially. These devices will facilitate high-speed communication networks, enabling smartphones to transmit data and derive valuable insights. The integration of innovative technologies, such as augmented reality, gesture recognition, and voice recognition, into smartphones further boosts the demand for RF semiconductors.

- Consequently, numerous companies are investing in the development of high-speed network-enabled devices to cater to the evolving needs of smartphone and tablet OEMs. The proliferation of mobile computing devices is anticipated to fuel the market growth, with smartphone manufacturers launching 5G-enabled models.

Prevailing Industry Trends & Opportunities

The rising significance of advanced RF devices is a notable trend in the radar and electronic warfare systems market. Advanced RF devices are increasingly important in the development of radar and electronic warfare systems.

- The market is experiencing significant growth due to its expanding applications across various sectors, including defense and high electronic machinery. With increasing investments in defense systems by developed and developing economies, the demand for RF semiconductors is expected to surge. Adversarial electronic warfare threats have become increasingly complex, necessitating advanced countermeasures and detection systems, such as radars, which rely heavily on RF and microwave technologies. Consequently, The market is poised for robust expansion during the forecast period. Additionally, the integration of RF semiconductors in wireless communication, automotive, healthcare, and industrial sectors is driving market growth.

- For instance, RF semiconductors enable wireless charging in electric vehicles, improve signal quality in wireless communication networks, and enhance medical imaging systems' efficiency. According to industry reports, the market's compound annual growth rate (CAGR) is projected to exceed 10%, outpacing the growth rate of the overall semiconductor industry. This growth is attributed to the market's increasing penetration in various sectors and the continuous innovation in RF semiconductor technology.

Significant Market Challenges

The escalating production costs of RF semiconductors represent a significant challenge that impedes the growth of the industry. RF semiconductors, which are integral to various advanced technologies including wireless communication systems and radio frequency identification (RFID) devices, require intricate manufacturing processes and high-quality materials, leading to substantial production expenses. Consequently, this financial hurdle poses a significant obstacle for industry expansion.

- RF semiconductors, known for their role in wireless communication and radio frequency applications, continue to evolve and expand across various sectors. These advanced semiconductors necessitate substantial investments due to their intricate manufacturing process and high-end equipment requirements. The production of RF semiconductors involves complex procedures, making it a challenging endeavor for companies with limited resources. This investment barrier restricts market growth, particularly for new entrants and expanding companies without significant financing options. Despite these challenges, the market demonstrates continuous innovation, with manufacturers focusing on enhancing performance and efficiency. For instance, the integration of gallium nitride (GaN) and silicon carbide (SiC) technologies has led to substantial improvements in power handling capabilities and efficiency.

- As a result, RF semiconductors are increasingly adopted in sectors such as telecommunications, automotive, and industrial automation, contributing to operational cost savings and improved system performance. For telecommunications, RF semiconductors have enabled 5G network deployment, reducing latency and increasing data transfer rates. In the automotive sector, RF semiconductors facilitate advanced driver assistance systems (ADAS) and vehicle-to-vehicle (V2V) communication, enhancing safety and connectivity. In industrial automation, RF semiconductors are used in wireless sensors and actuators, enabling remote monitoring and control, and reducing downtime.

In-Depth Market Segmentation: RF Semiconductor Market

The rf semiconductor industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Consumer Electronics

- Telecom

- Automotive

- Aerospace and defense and others

- Product

- RF filters

- RF power amplifier

- RF switches

- RF duplexers

- Others

- Material

- GaAs

- Si

- GaN

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- Taiwan

- Rest of World (ROW)

- North America

By End-user Insights

The consumer electronics segment is estimated to witness significant growth during the forecast period.

RF semiconductors are integral to the wireless communication and connectivity in consumer electronics, including smartphones, smart TVs, wearable devices, and smart home devices. These technologies, such as cellular, Wi-Fi, Bluetooth, and NFC, rely on RF semiconductors for data transfer, voice calls, and multimedia streaming. The evolving consumer electronics market demands advanced RF solutions for improved performance and efficiency. For instance, RFIC (Radio Frequency Integrated Circuit) design focuses on minimizing harmonic distortion and enhancing linearity performance. In antenna design, impedance matching and directional couplers ensure optimal signal transfer. Oscillator design, filter design, and power efficiency are critical for high-frequency components like RF power amplifiers.

System integration and signal integrity are essential for microwave circuits, which involve electromagnetic simulation, RF testing, and circuit simulation. RF semiconductors contribute to the development of high-power amplifiers, spectrum analyzers, low-noise amplifiers, and transmitter design, all while addressing challenges like intermodulation distortion, power divider, matched filter, noise figure, and signal integrity.

The Consumer Electronics segment was valued at USD 622.50 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 74% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How RF Semiconductor Market Demand is Rising in APAC Request Free Sample

The market in the Asia Pacific (APAC) region is experiencing significant growth, driven primarily by the increasing demand for enhanced cellular networks in developing countries such as China, India, South Korea, Taiwan, and Malaysia. These nations, which are nearing saturation point for 4G services, are now rolling out 5G services to meet their growing connectivity needs. The high population densities and robust economic growth in countries like India and China have fueled the demand for RF semiconductor applications in network infrastructure. This trend is enabling better services to counteract congested networks and poor services that were once common in these markets.

The global RF semiconductor industry is witnessing a knowledge and skillset transfer between the West and the East, leading to advancements in high-power technology. According to industry reports, the market in APAC is projected to grow at a substantial rate, with China and South Korea being major contributors. This growth is attributed to the increasing adoption of wireless communication technologies and the expanding consumer electronics industry in the region.

Customer Landscape of RF Semiconductor Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the RF Semiconductor Market

Companies are implementing various strategies, such as strategic alliances, rf semiconductor market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AGNIT Semiconductors Pvt, Ltd. - This company specializes in RF semiconductor solutions, providing advanced GaAs offerings such as CR 01 through CR 08. Their product line caters to various industries, showcasing innovation and commitment to RF technology advancement.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AGNIT Semiconductors Pvt, Ltd.

- ALB Materials Inc.

- Ampleon Netherlands BV

- Analog Devices Inc.

- Broadcom Inc.

- Haila Technology Inc.

- Infineon Technologies AG

- Microchip Technology Inc.

- Navitas Semiconductor Inc.

- NXP Semiconductors NV

- Qorvo Inc.

- Qualcomm Inc.

- Renesas Electronics Corp.

- ROHM Co. Ltd.

- STMicroelectronics NV

- TE Connectivity Ltd.

- The Swatch Group Ltd.

- Transphorm Inc

- Wolfspeed Inc.

- XP Power

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in RF Semiconductor Market

- In August 2024, Infineon Technologies AG, a leading RF semiconductor manufacturer, announced the launch of its new XENSIV Wireless Power Transfer (WPT) receiver IC, expanding its portfolio of wireless charging solutions (Infineon Press Release, 2024). This new product is designed to support the Qi and AirFuel Resonant standards, enabling efficient and universal wireless charging for various consumer electronics.

- In November 2024, Qualcomm Technologies, Inc., a major RF semiconductor player, entered into a strategic partnership with Samsung Electronics to collaborate on the development of next-generation RF front-end solutions for 5G smartphones (Qualcomm Press Release, 2024). This collaboration aims to enhance the performance and efficiency of RF front-end modules, ensuring seamless 5G connectivity for consumers.

- In March 2025, NXP Semiconductors N.V. Completed the acquisition of Marvell's Wi-Fi, Bluetooth, and Zigbee business, significantly expanding its RF portfolio and market presence (NXP Press Release, 2025). This strategic move strengthens NXP's position in the IoT market, providing a broader range of RF solutions for various applications.

- In May 2025, the European Union (EU) approved the Horizon Europe research and innovation program, which includes a €1 billion investment in 5G and beyond technologies, including RF semiconductors (European Commission Press Release, 2025). This funding will support the development of advanced RF technologies, contributing to the EU's digital transformation and technological leadership.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled RF Semiconductor Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

238 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.5% |

|

Market growth 2025-2029 |

USD 1823.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

9.3 |

|

Key countries |

US, China, Japan, South Korea, India, Germany, Canada, UK, Taiwan, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for RF Semiconductor Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth due to the increasing demand for high-performance wireless communication systems, particularly in the 5G era. To remain competitive in this market, semiconductor companies are focusing on advanced RFIC design techniques, such as high-frequency circuit design and impedance matching network synthesis, to optimize RF power amplifier efficiency and reduce intermodulation distortion. In the realm of antenna design, companies are employing advanced methods to improve antenna efficiency and reduce size, while maintaining signal integrity. Low-noise amplifier design for 5G applications is another critical area of focus, with a growing emphasis on power amplifier linearity improvement strategies and phase noise reduction techniques. High-power amplifier thermal management is also a significant challenge, with companies investing in advanced cooling systems and thermal modeling to ensure reliable operation. Novel filter design approaches and system level electromagnetic simulations are essential for optimizing system performance and reducing component size. Electromagnetic compatibility testing standards are becoming increasingly stringent, requiring companies to invest in advanced packaging techniques for RFICs and efficient transmitter design methods to minimize electromagnetic interference. Improved receiver sensitivity design is also crucial for enhancing system performance and expanding the reach of wireless networks. Compared to traditional RFIC design methods, advanced microwave circuit simulations offer significant time and cost savings, enabling companies to quickly iterate on designs and bring new products to market more efficiently. These simulation tools also enable more accurate modeling of high-frequency components, reducing the risk of costly design errors. In summary, the market is driven by the demand for high-performance wireless communication systems, particularly in the 5G era. To remain competitive, companies must focus on advanced RFIC design techniques, thermal management, and electromagnetic compatibility testing standards, while also investing in efficient simulation tools to reduce design time and cost. By staying at the forefront of these technologies, semiconductor companies can differentiate themselves in the market and meet the evolving demands of their customers.

What are the Key Data Covered in this RF Semiconductor Market Research and Growth Report?

-

What is the expected growth of the RF Semiconductor Market between 2025 and 2029?

-

USD 1.82 billion, at a CAGR of 10.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Consumer Electronics, Telecom, Automotive, and Aerospace and defense and others), Product (RF filters, RF power amplifier, RF switches, RF duplexers, and Others), Material (GaAs, Si, and GaN), and Geography (APAC, North America, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for RF devices for smartphones, High production cost of RF semiconductors

-

-

Who are the major players in the RF Semiconductor Market?

-

AGNIT Semiconductors Pvt, Ltd., ALB Materials Inc., Ampleon Netherlands BV, Analog Devices Inc., Broadcom Inc., Haila Technology Inc., Infineon Technologies AG, Microchip Technology Inc., Navitas Semiconductor Inc., NXP Semiconductors NV, Qorvo Inc., Qualcomm Inc., Renesas Electronics Corp., ROHM Co. Ltd., STMicroelectronics NV, TE Connectivity Ltd., The Swatch Group Ltd., Transphorm Inc, Wolfspeed Inc., and XP Power

-

We can help! Our analysts can customize this rf semiconductor market research report to meet your requirements.

RIA -

RIA -