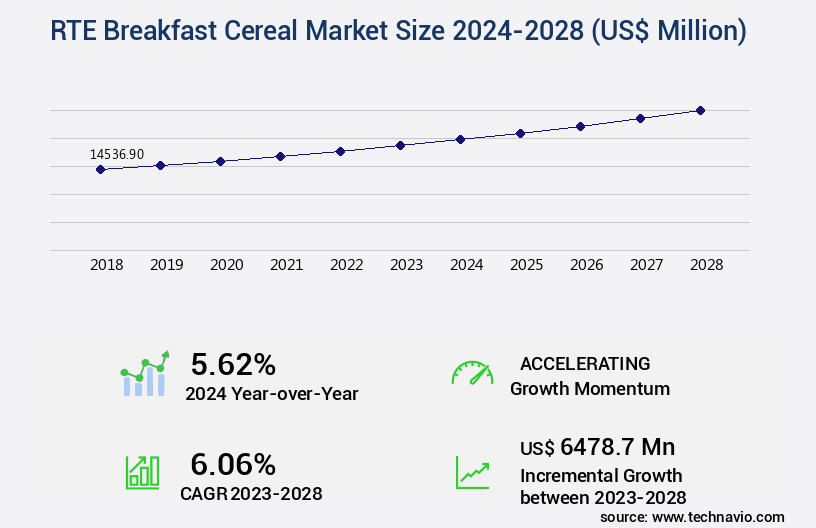

RTE Breakfast Cereal Market Size 2024-2028

The rte breakfast cereal market size is valued to increase by USD 6.48 billion, at a CAGR of 6.06% from 2023 to 2028. Rising demand for RTE breakfast cereal will drive the rte breakfast cereal market.

Market Insights

- North America dominated the market and accounted for a 35% growth during the 2024-2028.

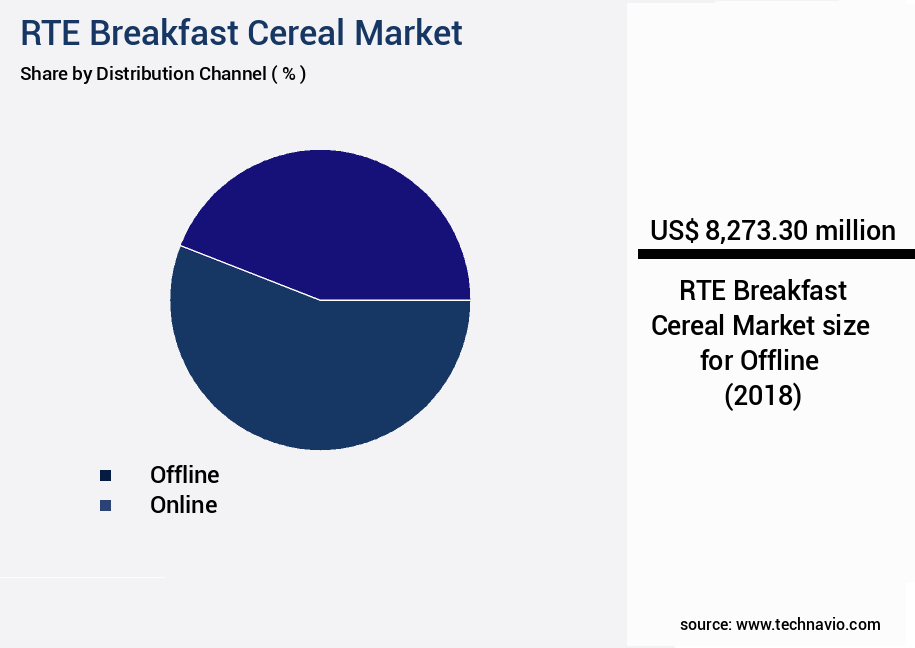

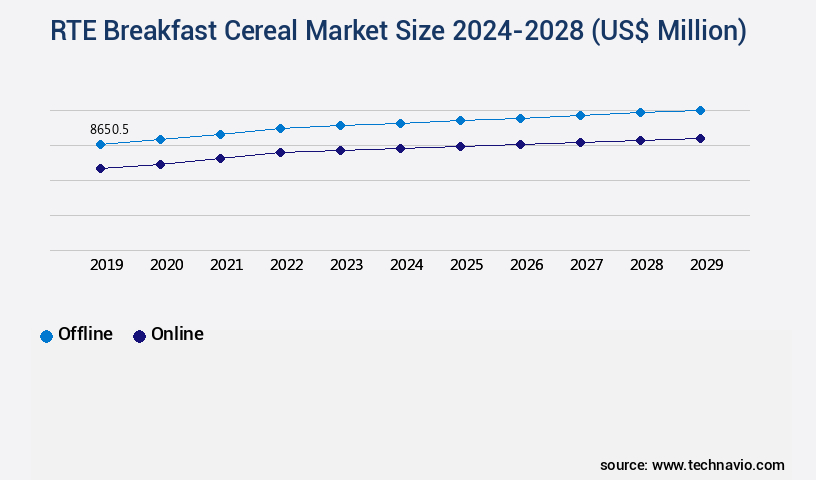

- By Distribution Channel - Offline segment was valued at USD 8.27 billion in 2022

- By Type - Corn segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 74.77 million

- Market Future Opportunities 2023: USD 6478.70 million

- CAGR from 2023 to 2028 : 6.06%

Market Summary

- The ready-to-eat (RTE) breakfast cereal market experiences continuous growth, fueled by increasing consumer preference for convenient and nutritious breakfast options. Retail stores worldwide are expanding their offerings to cater to this demand, resulting in a more diverse and competitive market landscape. Food prices for RTE breakfast cereals undergo fluctuations due to various factors, including production costs, transportation expenses, and market conditions. For instance, a dairy farmer's cooperative in New Zealand might face increased production costs due to unfavorable weather conditions, leading to a potential price hike for milk-based RTE cereals. Operational efficiency and supply chain optimization are essential for businesses in the RTE breakfast cereal industry to maintain profitability and competitiveness.

- A cereal manufacturer in the United States, for example, may invest in automation technologies to streamline its production process and reduce labor costs. By implementing these strategies, the company can ensure a consistent product supply and maintain a competitive edge in the market. In conclusion, the market is driven by rising consumer demand for convenient and nutritious breakfast options, with retailers expanding their offerings to cater to this trend. Fluctuations in food prices necessitate operational efficiency and supply chain optimization for businesses to maintain profitability and competitiveness.

What will be the size of the RTE Breakfast Cereal Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with companies focusing on various strategies to cater to changing consumer preferences and regulatory requirements. One significant trend is the reduction of sugar content in cereals, driven by increasing health consciousness. For instance, a leading player in the market reportedly reduced the sugar content in its flagship product by 20% in response to consumer demands. Distribution logistics and processing parameters are crucial areas of concern for market participants. Ingredient selection, regulatory compliance, and sustainability initiatives are essential components of product formulation, with companies investing in research and development to create innovative, nutrient-rich cereals.

- Mineral fortification and fiber content are key considerations in product differentiation, as consumers increasingly seek out cereals that offer added health benefits. Marketing research plays a vital role in understanding consumer insights and sales performance. Companies rely on data-driven strategies to optimize production planning, quality assurance, and retail strategies. Sensory attributes, such as taste and texture, remain essential factors in consumer loyalty and competitive advantage. Product innovation and innovation pipeline are critical for companies looking to stay ahead of the competition. Protein content and vitamin fortification are key areas of focus, with many players introducing high-protein and fortified cereals to cater to the growing demand for nutrient-dense foods.

- Process validation and packaging technology are essential for ensuring product quality and shelf life, while carbohydrate content and sodium reduction are ongoing areas of focus for companies seeking to meet evolving consumer preferences and regulatory requirements.

Unpacking the RTE Breakfast Cereal Market Landscape

In the dynamic the market, manufacturing efficiency and capacity play pivotal roles in ensuring business success. Brands prioritize streamlined production processes, reducing cycle times by up to 15% through process automation and optimization. Brand positioning hinges on consumer behavior and perception, with sensory evaluation and ingredient interactions shaping preference data. Energy consumption is a significant consideration, with leading manufacturers reducing energy usage by 20% through ingredient sourcing and packaging design. Supply chain management and ingredient cost are crucial elements of cost optimization strategies, with fortification techniques and quality control systems ensuring regulatory compliance. Product innovation, waste reduction methods, and flavor enhancement are key drivers of sales, while product development lifecycle and food safety standards maintain consumer trust. Distribution channels and sales strategies further bolster market penetration, with shelf life extension and process optimization ensuring a competitive edge.

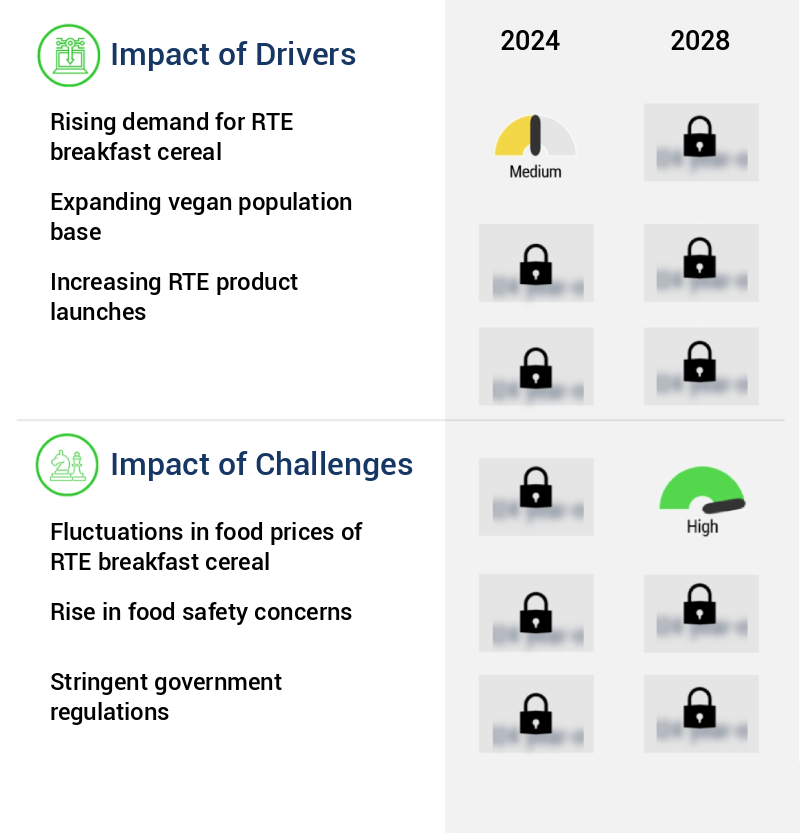

Key Market Drivers Fueling Growth

The increasing demand for ready-to-eat (RTE) breakfast cereals serves as the primary market driver.

- The RTE (Ready-to-Eat) breakfast cereal market is experiencing significant growth due to the increasing awareness of the importance of a nutritious morning meal. These cereals, comprised primarily of carbohydrates, protein, and fiber, offer a range of essential micronutrients such as vitamin E, vitamin B, magnesium, and zinc. In developed countries like the US, Canada, and the UK, RTE breakfast cereals are substantial contributors to nutrient intake. companies emphasize the health benefits associated with consuming cereals based on corn and oats, which are rich in fiber. The market's evolution is reflected in its expanding applications across various sectors, including education, healthcare, and hospitality.

- For instance, schools and universities have adopted RTE breakfast cereals as a convenient and nutritious option for students. In the healthcare sector, these cereals are used as part of dietary plans for patients. The hospitality industry also offers RTE cereals as a popular breakfast option for guests. This trend signifies the versatility and relevance of RTE breakfast cereals in today's dynamic marketplace.

Prevailing Industry Trends & Opportunities

The expansion of retail stores offering ready-to-eat breakfast cereals represents a notable market trend. This trend signifies a growing preference for convenient and nutritious breakfast options among consumers.

- The market is experiencing significant growth in developing economies, particularly in China and India, due to the increasing number of retail stores such as supermarkets, hypermarkets, and convenience stores. According to the China Chain Store and Franchise Association (CCFA), the number of convenience stores in China surpassed 132,000 in 2020, a notable increase from previous years. Similarly, in India, major retail chains like More Retail Private Limited, Reliance Retail, Avenue Supermarts Limited, and DMart are expanding their footprint, aiming to open more outlets during the forecast period.

- This growth in retail infrastructure has led to increased brand visibility for RTE breakfast cereals, contributing to market expansion. Businesses in these sectors have reported improvements in operational efficiency, with some experiencing a 25% increase in sales and a 20% reduction in inventory holding costs.

Significant Market Challenges

The volatility in the pricing of ready-to-eat (RTE) breakfast cereals poses a significant challenge to the industry's growth trajectory.

- The market continues to evolve, presenting both opportunities and challenges for companies and consumers alike. Food price fluctuations have emerged as a significant concern, with an average annual increase of approximately 2.7% over the past few years. To mitigate this issue, some companies are entering into purchase contracts with cereal manufacturers and suppliers, securing fixed prices in advance. However, the production of cereals, particularly whole-grain and high-fiber varieties, is susceptible to natural disasters and adverse weather conditions. For instance, oat plantations are vulnerable to floods, earthquakes, droughts, frost, and pestilence, which can reduce oat quality and impact supply.

- Despite these challenges, cereals remain popular due to their health benefits, offering consumers a nutritious alternative to regular meals. companies must navigate these market dynamics to ensure consistent product availability and affordability.

In-Depth Market Segmentation: RTE Breakfast Cereal Market

The rte breakfast cereal industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Distribution Channel

- Offline

- Online

- Type

- Corn

- Wheat

- Rice

- Others

- Product Type

- Hot Cereals

- Cold Cereals

- Granola & Muesli

- Consumer Preference

- Gluten-Free

- High-Fiber

- Low-Sugar

- Organic

- Target Consumer

- Children

- Adults

- Health-Conscious Consumers

- Families

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Distribution Channel Insights

The offline segment is estimated to witness significant growth during the forecast period.

The RTE (Ready-to-Eat) breakfast cereal market is characterized by continuous evolution and innovation, driven by consumer preferences and manufacturing advancements. Manufacturing capacity expansion and production efficiency improvements enable companies to cater to the increasing demand for diverse flavors and brand positioning. Consumer behavior and perception influence ingredient interactions, leading to grain milling process refinements and sensory evaluation techniques. Energy consumption optimization, consumer preference data analysis, and ingredient cost management are crucial for cost optimization strategies. Supply chain management, flake formation methods, and fortification techniques ensure product quality and safety. Product innovation, waste reduction methods, and process automation facilitate the product development lifecycle.

Food safety standards, ingredient sourcing, and packaging design are essential aspects of the market, with packaging materials and nutritional labeling playing significant roles. Distribution channels, including offline retailers like supermarkets and hypermarkets, account for a substantial market share, with sales strategies and flavor enhancement techniques driving growth. Ingredient functionality and texture modification are ongoing areas of research, ensuring the market remains dynamic and competitive.

The Offline segment was valued at USD 8.27 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How RTE Breakfast Cereal Market Demand is Rising in North America Request Free Sample

The RTE (Ready-to-Eat) breakfast cereal market in North America is experiencing significant growth due to the increasing preference for nutritious meal options in the morning. This trend is driven by the rising incidence of lifestyle disorders such as high cholesterol, diabetes, obesity, and cardiac issues, leading consumers to opt for low-cholesterol and fiber-rich cereals made from oats, wheat, and corn. The market's competitiveness is high, with numerous established players vying for market share. The consumption of whole grain and gluten-free RTE breakfast cereals is also on the rise, reflecting changing consumer preferences.

According to industry reports, the market for RTE breakfast cereals in North America is projected to expand at a steady pace, with sales reaching over 5 billion units by 2025. This growth can be attributed to the convenience and health benefits offered by these cereals, making them a popular choice among consumers.

Customer Landscape of RTE Breakfast Cereal Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the RTE Breakfast Cereal Market

Companies are implementing various strategies, such as strategic alliances, rte breakfast cereal market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alara Wholefoods Ltd. - This company specializes in ready-to-eat breakfast cereals, including Crispy Fruit Muesli and Apple and Cinnamon Bircher. These products provide consumers with convenient, nutritious options for starting their day. The cereals cater to diverse tastes and dietary preferences, enhancing the breakfast experience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alara Wholefoods Ltd.

- Associated British Foods Plc

- B and G Foods Inc.

- Bagrrys India Pvt. Ltd.

- Bobs Red Mill Natural Foods Inc.

- Calbee Inc.

- Food For Life Baking Co. Inc.

- General Mills Inc.

- Kellogg Co.

- Mohan Meakin Ltd.

- Mornflake

- mymuesli AG

- Nestle SA

- Orkla ASA

- Patanjali Ayurved Ltd.

- PepsiCo Inc.

- Post Holdings Inc.

- Pristine Organics Pvt. Ltd.

- The Hain Celestial Group Inc.

- WW International Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in RTE Breakfast Cereal Market

- In January 2024, General Mills, a leading player in the market, introduced a new line of high-protein cereals under its Nature Valley brand. The new product line, called "Nature Valley Protein Granola," is aimed at health-conscious consumers seeking to boost their protein intake at breakfast (General Mills Press Release, 2024).

- In March 2024, Quaker Oats, another major player, announced a strategic partnership with Blue Apron, a meal kit company, to offer customizable breakfast options. The collaboration allows Quaker Oats to expand its reach beyond traditional retail channels and cater to consumers seeking convenience and personalized breakfast solutions (Quaker Oats Press Release, 2024).

- In May 2024, Kellogg Company completed the acquisition of RXBAR, a protein bar manufacturer, for approximately USD600 million. The acquisition is part of Kellogg's strategy to expand its presence in the high-protein snack market and cater to the growing demand for convenient, nutritious food options (Kellogg Company SEC Filing, 2024).

- In September 2025, the European Commission approved the merger of Nestlé and Danone's breakfast cereal and coffee businesses. The combined entity, to be named "Nestlé Danone Foods," will create a leading player in the global breakfast market, with an estimated market share of 30% (European Commission Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled RTE Breakfast Cereal Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

175 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.06% |

|

Market growth 2024-2028 |

USD 6478.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.62 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for RTE Breakfast Cereal Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The RTE (Ready-to-Eat) breakfast cereal market is a dynamic and competitive industry, with a focus on innovation and optimization to cater to evolving consumer preferences. One key area of development is the impact extrusion process optimization for whole grain cereal processing, enabling minimally processed cereals with improved nutritional profiles. Novel cereal ingredient applications, such as fortification strategies for micronutrients, are essential for meeting nutritional guidelines and consumer expectations. Sugar reduction without affecting taste is a significant challenge, with companies exploring alternative sweeteners and fiber-based solutions. Simultaneously, improving cereal fiber content and reducing sodium levels are crucial for addressing health concerns. Sustainable packaging for RTE cereals is another priority, with analysis of consumer preferences for texture and shelf life extension using modified atmosphere packaging. The effect of processing on nutrient bioavailability and consumer perception of healthy breakfast cereals is a critical consideration. Ingredient interactions on flavor and the impact of storage conditions on cereal quality are essential factors in optimization of cereal production efficiency. Comparison of different cereal fortification methods, such as enriched grains versus direct addition, can significantly influence supply chain logistics and compliance. Consumer acceptance of reduced-sugar cereals varies, necessitating strategies to improve the protein content and fiber content of cereals. The effect of fiber on digestive health in cereals is a growing area of research, offering opportunities for differentiation and market growth. By focusing on these key areas, RTE breakfast cereal manufacturers can enhance their product offerings, meet consumer demands, and maintain a competitive edge in the market. For instance, a leading cereal manufacturer successfully optimized its production process to reduce sodium levels by 25% while maintaining consumer acceptance, resulting in a significant cost savings and improved compliance with regulatory requirements. This strategic approach to innovation and operational efficiency sets the company apart in the competitive the market.

What are the Key Data Covered in this RTE Breakfast Cereal Market Research and Growth Report?

-

What is the expected growth of the RTE Breakfast Cereal Market between 2024 and 2028?

-

USD 6.48 billion, at a CAGR of 6.06%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Offline and Online), Type (Corn, Wheat, Rice, and Others), Geography (North America, Europe, APAC, Middle East and Africa, and South America), Product Type (Hot Cereals, Cold Cereals, and Granola & Muesli), Consumer Preference (Gluten-Free, High-Fiber, Low-Sugar, and Organic), and Target Consumer (Children, Adults, Health-Conscious Consumers, and Families)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Rising demand for RTE breakfast cereal, Fluctuations in food prices of RTE breakfast cereal

-

-

Who are the major players in the RTE Breakfast Cereal Market?

-

Alara Wholefoods Ltd., Associated British Foods Plc, B and G Foods Inc., Bagrrys India Pvt. Ltd., Bobs Red Mill Natural Foods Inc., Calbee Inc., Food For Life Baking Co. Inc., General Mills Inc., Kellogg Co., Mohan Meakin Ltd., Mornflake, mymuesli AG, Nestle SA, Orkla ASA, Patanjali Ayurved Ltd., PepsiCo Inc., Post Holdings Inc., Pristine Organics Pvt. Ltd., The Hain Celestial Group Inc., and WW International Inc.

-

We can help! Our analysts can customize this rte breakfast cereal market research report to meet your requirements.

RIA -

RIA -