Semiconductor Market In Healthcare Sector Size 2025-2029

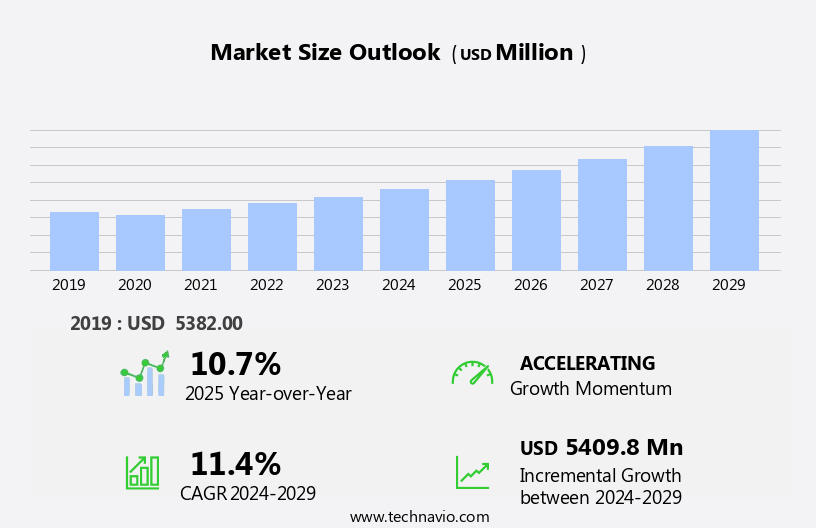

The semiconductor market in healthcare sector size is forecast to increase by USD 5.41 billion, at a CAGR of 11.4% between 2024 and 2029.

- The Semiconductor Market in the Healthcare Sector is experiencing significant growth, driven by the escalating demand for advanced medical devices. These devices, including wearable health monitors, imaging systems, and portable diagnostic tools, rely on semiconductors for their functionality and miniaturization. The integration of artificial intelligence and machine learning algorithms in these devices further accentuates the need for high-performance semiconductors. Another critical trend in this market is the emphasis on sustainable semiconductor manufacturing. As the healthcare industry strives for greener practices, semiconductor manufacturers are responding by adopting more eco-friendly production methods. This shift not only appeals to environmentally-conscious consumers but also positions companies as industry leaders in sustainability.

- However, regulatory compliance poses a significant challenge for semiconductor manufacturers in the healthcare sector. Strict regulations governing medical device manufacturing and usage necessitate stringent quality control measures and rigorous testing procedures for semiconductors. Ensuring compliance with these regulations can add complexity and cost to the manufacturing process, necessitating strategic planning and partnerships to navigate these challenges effectively.

What will be the Size of the Semiconductor Market In Healthcare Sector during the forecast period?

The semiconductor market in the healthcare sector continues to evolve, driven by advancements in chip architecture, healthcare IT, semiconductor fabrication, and various applications. Integrated circuits (ICS) are at the heart of these innovations, with heterogeneous integration enabling the merging of different technologies on a single chip. Reliability testing, wafer bonding, and yield enhancement are crucial elements in the semiconductor fabrication process, ensuring the production of high-quality chips. In healthcare, semiconductors play a pivotal role in remote patient monitoring, computer vision, and memory chips, enhancing the capabilities of diagnostic devices and medical imaging systems. Artificial intelligence (AI) and machine learning are revolutionizing precision medicine, while advanced node technologies such as EUV lithography push the boundaries of transistor density and miniaturization.

Biometric authentication, failure analysis, and verification and testing are essential components of chip security, ensuring data privacy and protection. Semiconductors also find applications in drug delivery systems, data analytics, and hardware security, contributing to the overall growth of the healthcare sector. The semiconductor industry is not without challenges, including the global semiconductor shortage and the need for supply chain management and design automation. Packaging technologies and cleanroom environments are critical to addressing these challenges, ensuring the efficient production and delivery of semiconductor solutions. Prosthetics and implants, wearable health monitoring, and robotics and automation are among the emerging applications of semiconductors in healthcare, underscoring the continuous dynamism of this market.

Memory chips, digital-to-analog converters (DACs), and analog-to-digital converters (ADCs) are integral to these applications, enabling the collection, processing, and analysis of health data. The semiconductor market in healthcare is a complex and ever-evolving landscape, shaped by continuous innovation and the integration of various technologies. From chip architecture to healthcare IT, semiconductor fabrication, and applications, the potential for growth and transformation is vast.

How is this Semiconductor In Healthcare Sector Industry segmented?

The semiconductor in healthcare sector industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- ICs

- Sensors

- Optoelectronic

- Discrete components

- Application

- Medical imaging

- Patient monitoring

- Diagnostic equipment

- Wearable

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Component Insights

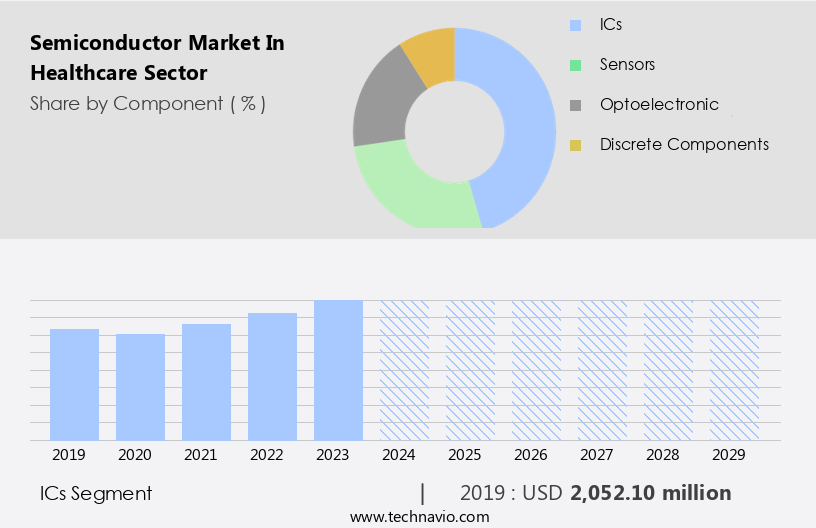

The ics segment is estimated to witness significant growth during the forecast period.

Integrated circuits (ICs) are a cornerstone of semiconductor technology in the healthcare sector, powering the intricate operations of various medical devices. From wearable health monitors to diagnostic equipment, imaging systems, and telemedicine devices, ICs deliver processing power, connectivity, and functionality that are indispensable for effective medical treatment. In medical imaging, ICs process and analyze data from MRI machines, X-rays, CT scanners, and ultrasound devices, ensuring precise imaging and accurate diagnostics. Advancements in IC technology, such as Moore's Law, have led to increased transistor density, enabling the production of smaller, more efficient chips. This trend is reflected in the development of advanced node technologies like 7nm, 5nm, and 3nm.

Heterogeneous integration, wafer bonding, and yield enhancement are essential techniques used in semiconductor fabrication to improve IC performance and reliability. Biometric authentication and failure analysis are critical aspects of IC design, ensuring security and maintaining optimal functionality. Deep learning and machine learning algorithms are increasingly being integrated into ICs to enhance data analytics capabilities in healthcare applications, from precision medicine to drug delivery systems. In the realm of wearable devices, ICs facilitate continuous monitoring of vital health parameters. Wearable health monitoring systems, such as those for heart rate, glucose levels, and blood oxygen saturation, rely on ICs for data processing and transmission.

ICs also play a crucial role in computer vision applications, enabling remote patient monitoring and enabling the development of robotics and automation systems in healthcare. Semiconductor fabrication in cleanroom environments is essential for maintaining the high level of precision required in healthcare applications. Design automation and verification and testing processes are critical to ensuring the reliability and functionality of ICs in medical devices. Packaging technologies and silicon wafers are also essential components of IC manufacturing, ensuring the protection and connectivity of the final product. The global semiconductor shortage has highlighted the importance of supply chain management and process optimization in the semiconductor industry.

ICs are integral to a wide range of healthcare applications, from diagnostic devices and medical imaging systems to prosthetics and implants, digital-to-analog and analog-to-digital converters, and chip security. The integration of ICs into healthcare technology continues to drive innovation and improve patient care.

The ICs segment was valued at USD 2.05 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

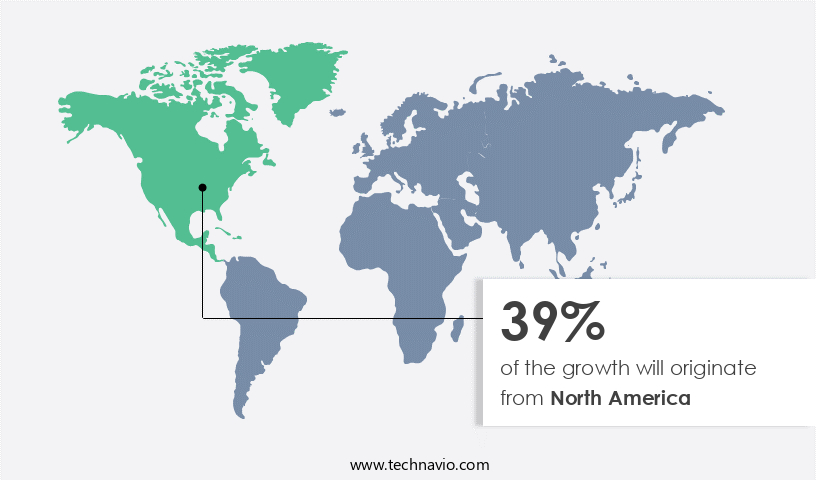

North America is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The semiconductor market in North America's healthcare sector experiences significant growth due to substantial healthcare expenditures and a high prevalence of chronic diseases. In 2023, the United States allocated approximately USD5 trillion to healthcare, representing a 7.5% increase from the previous year, with an average spending of USD14,550 per person. Canada's healthcare spending reached about USD340 billion, equivalent to USD8,750 per Canadian, accounting for around 12% of the country's GDP. This substantial investment in healthcare fuels the demand for advanced technologies, including Moore's Law-driven integrated circuits (ICS) and heterogeneous integration. Reliability testing, wafer bonding, and yield enhancement are crucial for producing high-quality semiconductors in this sector.

Biometric authentication and failure analysis ensure security and accuracy in healthcare applications. Deep learning, analog-to-digital converters (ADCs), and digital-to-analog converters (DACs) play essential roles in various medical devices, such as diagnostic devices, medical imaging, and drug delivery systems. Precision medicine, supply chain management, design automation, and process optimization are transforming healthcare IT. Advanced node technologies, such as 7nm, 5nm, and 3nm, enable the development of smaller, more efficient chips for wearable health monitoring, prosthetics and implants, and remote patient monitoring. EUV lithography and machine learning are critical for creating chip architectures that cater to the unique demands of healthcare applications.

Semiconductor fabrication, computer vision, memory chips, and artificial intelligence (AI) are revolutionizing healthcare, from diagnostics and treatment to drug discovery and development. Chip security and data analytics are vital components of this transformation, ensuring patient privacy and data integrity. The global semiconductor shortage poses a challenge to the healthcare sector, necessitating the exploration of packaging technologies and alternative solutions. Silicon wafers remain the foundation of semiconductor manufacturing, while cleanroom environments ensure the production of high-quality chips. In summary, the semiconductor market in North America's healthcare sector is characterized by significant investment, a high prevalence of chronic diseases, and a growing demand for advanced technologies.

Moore's Law, ICS, heterogeneous integration, reliability testing, wafer bonding, yield enhancement, biometric authentication, failure analysis, deep learning, ADCs, DACs, precision medicine, supply chain management, design automation, process optimization, advanced node technologies, semiconductor fabrication, computer vision, memory chips, AI, chip security, data analytics, packaging technologies, silicon wafers, and wearable health monitoring are all integral components of this dynamic and evolving market.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Semiconductor In Healthcare Sector Industry?

- The surge in demand for sophisticated medical devices serves as the primary catalyst for market growth.

- The semiconductor market in the healthcare sector experiences significant growth due to the increasing demand for advanced medical devices. These devices, including diagnostic imaging systems and wearable health monitoring devices, heavily rely on semiconductor technologies for their functionality, precision, and efficiency. Diagnostic imaging systems, such as MRI, CT, and PET scanners, require high-performance processors and sensors to capture and process detailed images, ensuring accurate diagnosis of complex conditions. For instance, GE Healthcare's Revolution CT scanner utilizes advanced semiconductor technology to achieve high-resolution imaging with lower radiation doses, enhancing diagnostic accuracy and patient safety. Moreover, semiconductor technologies play a crucial role in robotics and automation, medical imaging, and hardware security in the healthcare sector.

- Additionally, packaging technologies and silicon wafers are essential components in the production of semiconductor devices for medical applications. The global semiconductor shortage poses a challenge to the healthcare sector, as the demand for these devices continues to surge. Despite this, the market's future remains promising, with ongoing advancements in semiconductor technologies, such as advanced node technologies, contributing to the sector's growth.

What are the market trends shaping the Semiconductor In Healthcare Sector Industry?

- The focus on sustainable semiconductor manufacturing is an emerging market trend. It is essential to prioritize this area to ensure environmentally friendly and efficient production processes in the semiconductor industry.

- The semiconductor market in the healthcare sector is witnessing significant advancements, driven by the integration of chip architecture in Healthcare IT. Semiconductor fabrication plays a pivotal role in powering various healthcare applications, such as remote patient monitoring, computer vision, and drug delivery systems. The adoption of memory chips and artificial intelligence (AI) in healthcare is increasing, enabling data analytics and improved patient care. Moreover, chip security is becoming increasingly important to protect sensitive patient data. Merck and Intel's recent collaboration is a prime example of industry innovation.

- Launched on November 7, 2024, this academic research program focuses on enhancing sustainability in semiconductor manufacturing through AI and machine learning. Six projects, supported by eleven scientific institutions across Europe, aim to optimize semiconductor manufacturing processes, reduce waste, and improve material discovery. This initiative underscores the industry's commitment to making semiconductor fabrication more environmentally friendly and resource-efficient.

What challenges does the Semiconductor In Healthcare Sector Industry face during its growth?

- Compliance with regulatory requirements poses a significant challenge to the industry's growth trajectory. It is essential for businesses to adhere to these regulations to avoid penalties and maintain their reputation. Failure to do so can result in legal consequences and potential damage to brand image. Therefore, ensuring regulatory compliance is a critical aspect of business strategy and growth in the industry.

- The semiconductor market in the healthcare sector faces regulatory and compliance challenges due to the stringent requirements for patient safety, data privacy, and effectiveness. Adhering to these regulations is complex and time-consuming, as they vary across regions and product categories. In the US, the Food and Drug Administration (FDA) regulates medical devices that utilize semiconductors, necessitating FDA 510(k) clearance or premarket approval (PMA) processes. These rigorous evaluations ensure the safety and efficacy of devices before they reach the market. Moore's Law continues to drive advancements in semiconductor technology, leading to the integration of increasingly complex functionalities into healthcare devices.

- Heterogeneous integration, wafer bonding, yield enhancement, and reliability testing are essential for the production of high-performance semiconductors. Biometric authentication, deep learning, and analog-to-digital converters (ADCs) are among the technologies that have gained significant attention in the healthcare sector. Verification and testing are crucial to ensure the functionality and reliability of these advanced semiconductor solutions. Failure analysis plays a vital role in identifying and addressing any issues that arise during production or usage.

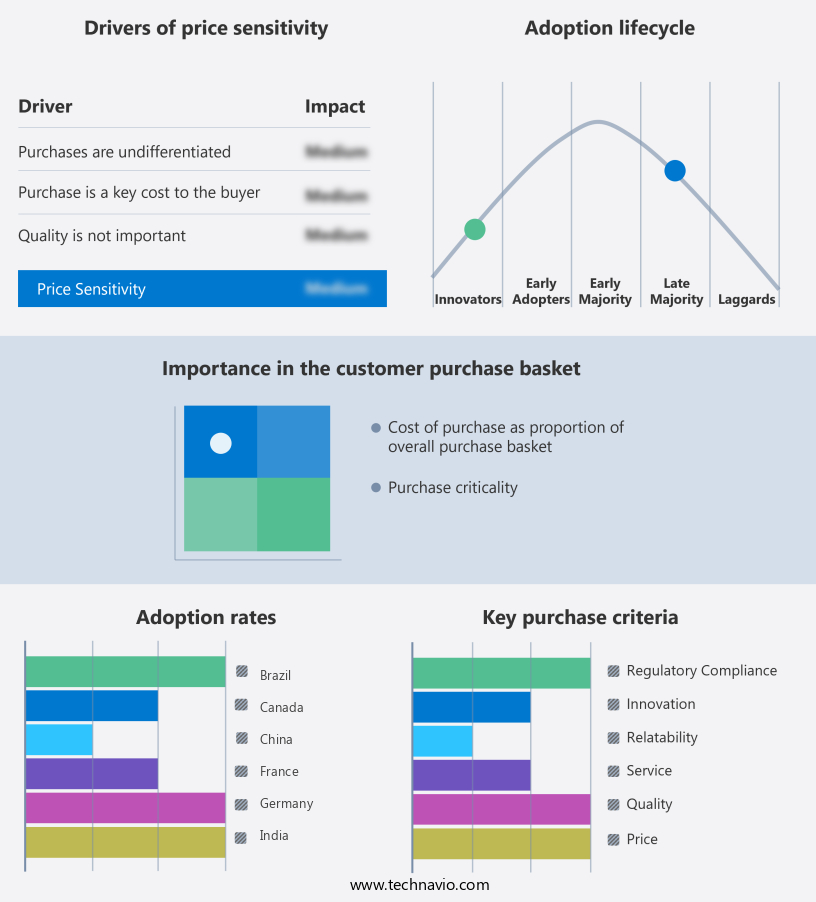

Exclusive Customer Landscape

The semiconductor market in healthcare sector forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the semiconductor market in healthcare sector report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, semiconductor market in healthcare sector forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ams OSRAM AG - The company specializes in semiconductor innovations for the healthcare sector. One such solution is the AS5912, a 512-channel, ultra-low noise converter. This technology, renowned for its power efficiency, facilitates the highest sensitivity readout of CT detector photodiodes. By minimizing noise levels, it significantly enhances diagnostic accuracy and reliability. This converter is a testament to our commitment to delivering advanced semiconductor solutions that cater to the evolving needs of the healthcare industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ams OSRAM AG

- Analog Devices Inc.

- Broadcom Inc.

- Infineon Technologies AG

- Intel Corp.

- Micron Technology Inc.

- NXP Semiconductors NV

- ON Semiconductor Corp.

- Renesas Electronics Corp.

- Samsung Electronics Co. Ltd.

- SK hynix Co. Ltd.

- STMicroelectronics NV

- Taiwan Semiconductor Manufacturing Co. Ltd.

- Texas Instruments Inc.

- Toshiba Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Semiconductor Market In Healthcare Sector

- In February 2023, Medtronic, a leading medical technology, services, and solutions company, announced the launch of its new MiniMed⢠MQ Infuse System, a hybrid closed-loop insulin pump system with integrated continuous glucose monitoring. This innovative semiconductor-based technology is designed to improve diabetes management by automatically adjusting insulin delivery based on real-time glucose data (Medtronic Press Release, 2023).

- In April 2024, Intel and IBM, two tech giants, formed a strategic partnership to collaborate on the development of advanced semiconductor technology for the healthcare sector. This collaboration aims to deliver more efficient, secure, and scalable solutions, including AI-powered medical devices and systems (Intel Newsroom, 2024).

- In January 2025, Qualcomm Life, a subsidiary of Qualcomm, secured a significant investment of USD100 million from several investors, including Singapore's sovereign wealth fund, GIC. This funding will be used to expand their wireless health and fitness platform, which includes semiconductor-based wearable devices and remote patient monitoring systems (Reuters, 2025).

- In July 2025, the U.S. Food and Drug Administration (FDA) approved the use of Google's TensorFlow Processing Unit (TPU) in medical imaging applications. This approval marks a significant technological advancement in the healthcare sector, as TPUs can process medical images faster and more accurately than traditional methods (Google Blog, 2025).

Research Analyst Overview

- In the healthcare sector, semiconductor technology plays a pivotal role in driving innovation and improving patient outcomes. The drug discovery process benefits significantly from yield management and advanced semiconductor manufacturing equipment, such as deposition systems and wafer steamers, enabling the production of high-quality CMOS technology chips. Wireless communication and system-in-package (SIP) solutions facilitate the seamless transfer of healthcare data, ensuring data privacy and security. The integration of silicon photonics and quantum computing in healthcare analytics platforms revolutionizes precision diagnostics and clinical trials, leading to cost optimization and design for manufacturability. Neuromorphic computing and NEMs (nano-electro-mechanical systems) enhance medical imaging algorithms, while MEMS (micro-electro-mechanical systems) and chip interconnect technologies improve implantable devices' functionality and biocompatibility.

- Cleanroom technology and etching machines are essential in producing semiconductors for healthcare applications, ensuring the highest standards of quality and reliability. Healthcare data security is bolstered by advanced packaging materials and technologies, such as advanced packaging and healthcare analytics platforms, which protect sensitive patient information. Semiconductor manufacturing equipment, including deposition systems and cleanroom technology, are integral to the development of healthcare solutions. The integration of CMOS technology, silicon photonics, and quantum computing propels the healthcare sector forward, improving patient care and outcomes.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Semiconductor Market In Healthcare Sector insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

227 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11.4% |

|

Market growth 2025-2029 |

USD 5409.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

10.7 |

|

Key countries |

US, China, Germany, Japan, UK, France, Canada, South Korea, India, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Semiconductor Market In Healthcare Sector Research and Growth Report?

- CAGR of the Semiconductor In Healthcare Sector industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the semiconductor market in healthcare sector growth of industry companies

We can help! Our analysts can customize this semiconductor market in healthcare sector research report to meet your requirements.

RIA -

RIA -