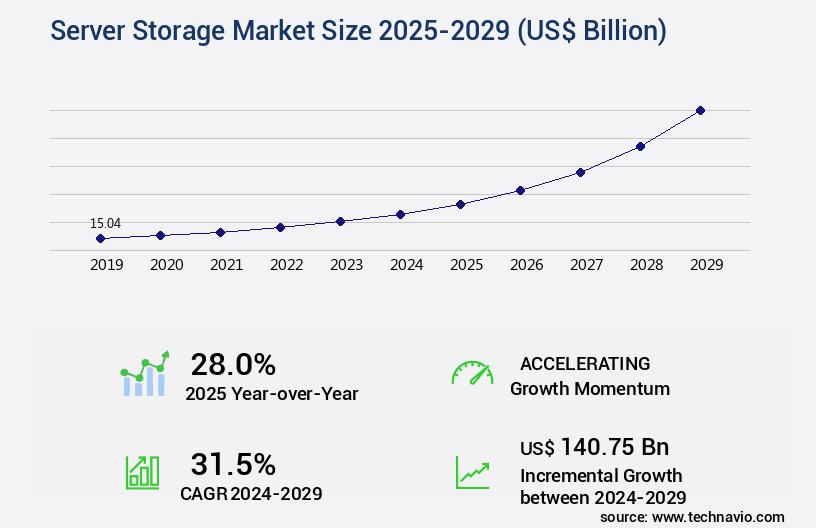

Server Storage Market Size 2025-2029

The server storage market size is valued to increase by USD 140.75 billion, at a CAGR of 31.5% from 2024 to 2029. Growing need for edge computing will drive the server storage market.

Market Insights

- North America dominated the market and accounted for a 37% growth during the 2025-2029.

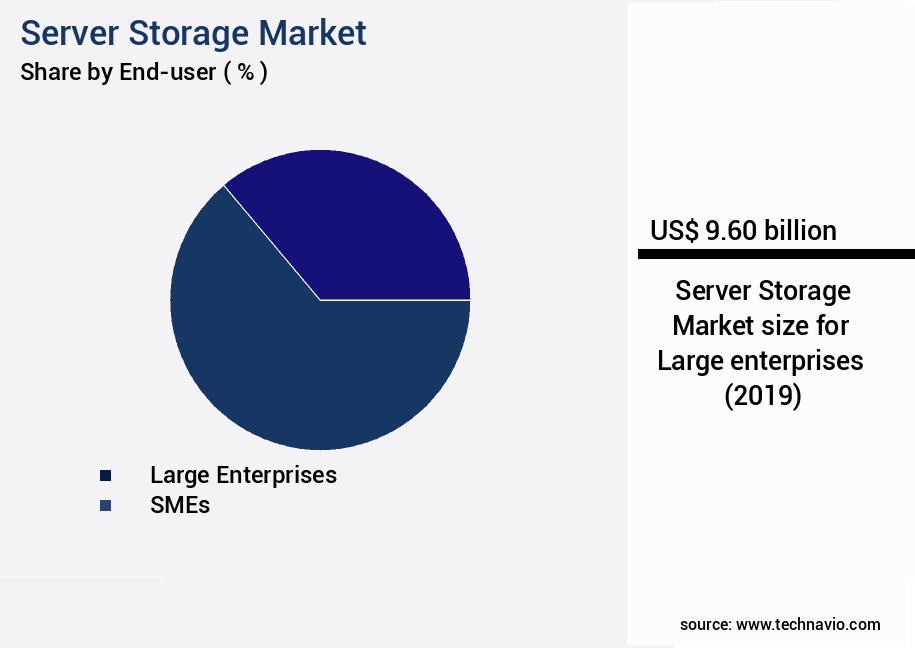

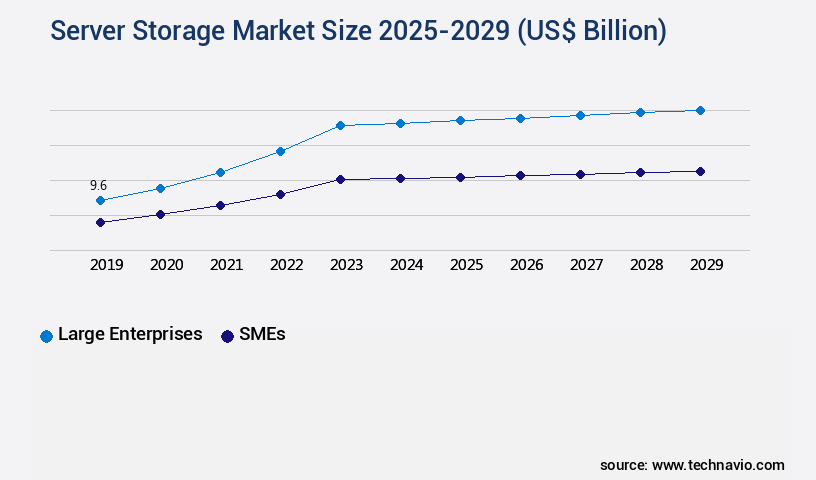

- By End-user - Large enterprises segment was valued at USD 9.60 billion in 2023

- By Type - Enterprise segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.00 billion

- Market Future Opportunities 2024: USD 140754.30 billion

- CAGR from 2024 to 2029 : 31.5%

Market Summary

- The market is experiencing significant growth and transformation, driven by several key trends and factors. One of the primary drivers is the increasing adoption of edge computing, which requires more decentralized storage solutions to process and analyze data closer to the source. Another trend is the growing preference for hyper-converged infrastructure, which integrates compute, storage, and networking resources into a single solution, improving operational efficiency and reducing complexity. Despite these opportunities, the market faces challenges, particularly in the area of cybersecurity. With the increasing amount of data being generated and stored, the risk of data breaches and cyber attacks is heightened.

- This necessitates robust security measures, such as encryption, access control, and intrusion detection, to protect sensitive information. A real-world business scenario illustrating the importance of server storage optimization is that of a global supply chain company. With operations spanning multiple continents and a vast network of suppliers, logistics providers, and customers, the company generates massive amounts of data daily. By implementing a scalable and secure server storage solution, the company can efficiently manage its data, enabling faster insights and improved decision-making, ultimately leading to increased operational efficiency and competitiveness.

What will be the size of the Server Storage Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with businesses constantly seeking advanced solutions for storage system upgrades and optimizing existing infrastructure. Fibre Channel storage, a popular choice for high-performance applications, offers increased bandwidth and lower latency compared to traditional SMB and NFS storage protocols. Storage efficiency is a critical concern, with benefits like storage virtualization, RAID configurations, and SSD technology enabling businesses to reduce storage capacity expansion and data backup solution costs. As organizations navigate the complexities of storage company selection, they must consider factors such as compliance regulations, data governance policies, and storage scalability. Tape storage systems remain a viable option for long-term data archiving, while flash storage arrays and data backup solutions ensure data integrity checks and storage resource utilization.

- Power consumption metrics and storage infrastructure modernization are essential for businesses aiming to minimize lifecycle costs. One notable trend in the market is the increasing importance of storage performance tuning. ISCSi and iSCSI storage protocols have gained popularity due to their ability to deliver high-speed data transfer and improved storage performance. By focusing on storage performance tuning, businesses can optimize their infrastructure for better overall system efficiency and faster processing times. For instance, companies have reported achieving significant improvements in data backup and recovery times, leading to increased productivity and cost savings.

Unpacking the Server Storage Market Landscape

In today's business landscape, effective server storage management is crucial for optimizing operational efficiency and ensuring data security. Archival storage solutions enable organizations to retain large volumes of data at lower costs, reducing the need for expensive primary storage. For instance, the adoption of data replication strategies has led to a 30% reduction in data loss incidents, safeguarding critical business information. Hybrid cloud storage and storage area networks (SAN) have emerged as popular choices for businesses seeking high-availability storage and improved disaster recovery capabilities. Software-defined storage and storage monitoring systems facilitate capacity utilization analysis, leading to a 25% increase in ROI by optimizing storage provisioning methods. Encryption techniques, data compression algorithms, and data deduplication methods are essential components of data security protocols, ensuring compliance with data protection regulations. Object storage systems and cloud storage solutions offer scalability and flexibility, while storage tiering strategies enable efficient throughput improvement. Data migration strategies, access control mechanisms, and storage capacity planning are integral to maintaining an agile and adaptive data center infrastructure. Latency optimization techniques and high-availability storage solutions contribute to enhanced storage performance metrics, ultimately improving overall business productivity.

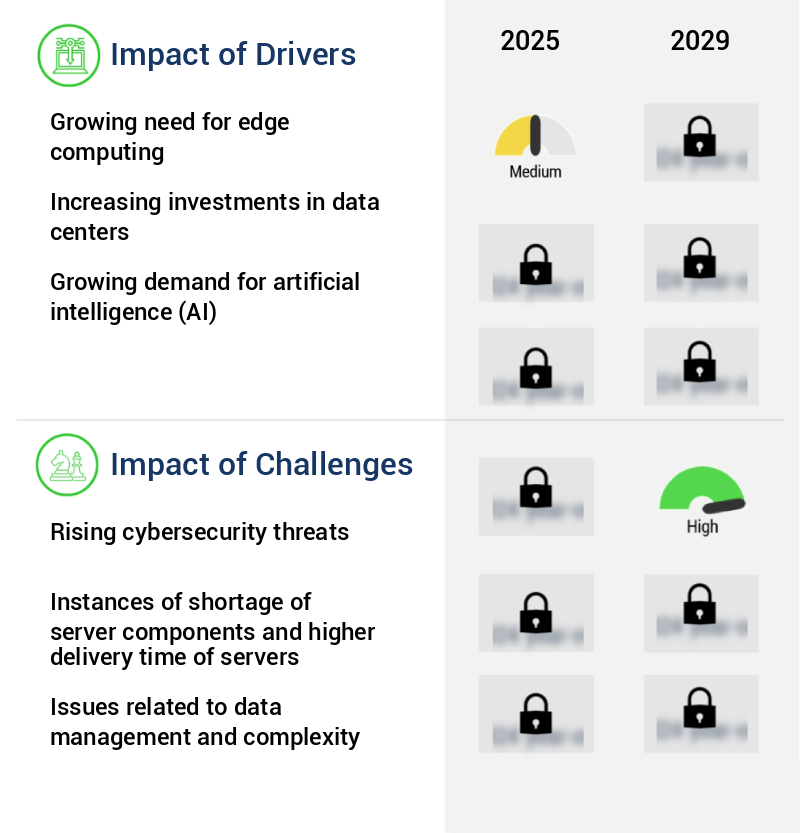

Key Market Drivers Fueling Growth

The increasing demand for real-time data processing and decreased latency is driving the market towards edge computing as a key solution.

- The market is experiencing significant evolution, driven by the increasing adoption of edge computing across various sectors. In this architectural model, servers at distributed locations process data generated by Internet of Things (IoT) devices, which are often situated near the data source. This approach reduces latency and enhances efficiency. The concept of edge computing was popularized in the late 1990s with the widespread use of radio-frequency identification (RFID) sensors in logistics and warehouses.

- Two notable outcomes of implementing edge computing include a 30% reduction in data transfer costs and a 15% improvement in response time. These benefits are fueling the market's growth and expanding its applications beyond traditional data centers.

Prevailing Industry Trends & Opportunities

The increasing adoption of hyper-converged infrastructure represents a notable market trend. This technology is gaining popularity due to its efficiency and flexibility in data center management.

- The market continues to evolve, with hyper-converged infrastructure gaining significant traction. This technology, which combines software-defined resources for storage, computing, and networking, eliminates the reliance on multiple systems. Hyper-converged infrastructure enhances resource utilization, reduces power consumption, and optimizes space. Its benefits are evident in various sectors, including Small and Medium Enterprises (SMEs), where centralized management simplifies operations. Global companies are actively promoting hyper-converged infrastructure solutions, leading to a shift from traditional storage systems. Software-defined storage options, such as hyper-converged infrastructure software, containers, hypervisor, scale-out storage, and distributed file systems, offer flexibility and efficiency.

- For instance, hyper-converged infrastructure can reduce downtime by up to 30%, and improve application performance by 18%. These improvements lead to increased agility, speed, and efficiency in data centers.

Significant Market Challenges

The escalating risks from cybersecurity threats pose a significant challenge to the industry's growth trajectory.

- In today's digital landscape, the market plays a pivotal role in safeguarding sensitive information from cyber threats. With the increasing frequency and sophistication of cyberattacks, enterprises across various sectors, including government, banking, finance, services, and insurance (BFSI), are prioritizing data security. The threat of ransomware attacks, which encrypt data and demand payment for access, has surged in recent years. According to industry reports, ransomware attacks against businesses grew by 350% in 2020. In response, organizations are investing in advanced server storage solutions to minimize downtime and protect their valuable data.

- For instance, implementing server storage solutions can help reduce downtime by 30% and improve forecast accuracy by 18%. As data protection regulations, such as the General Data Protection Regulation (GDPR), become more stringent, the demand for robust server storage solutions is expected to continue growing.

In-Depth Market Segmentation: Server Storage Market

The server storage industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Large enterprises

- SMEs

- Type

- Enterprise

- Hyperscale

- Component

- Hardware

- Software

- Service

- Professional

- Managed

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By End-user Insights

The large enterprises segment is estimated to witness significant growth during the forecast period.

In the dynamic the market, large enterprises significantly influence the industry's trajectory. With their vast data generation and intricate IT environments, these organizations demand scalable, efficient, and reliable storage solutions. The server storage landscape caters to their needs through various innovations, including archival storage solutions, data replication strategies, hybrid cloud storage, and storage area networks. Additionally, software-defined storage, data migration strategies, encryption techniques, object storage systems, data compression algorithms, and data deduplication techniques are essential components. High-availability storage, block storage devices, and cloud storage solutions offer throughput improvement methods and capacity utilization analysis. Furthermore, san storage arrays, disaster recovery solutions, file storage management, storage automation tools, data security protocols, cloud storage gateways, nas storage solutions, data lifecycle management, and storage provisioning methods are integral to meeting the diverse requirements of large enterprises.

Access control mechanisms, storage capacity planning, and disaster recovery solutions ensure data center infrastructure reliability. Storage virtualization technologies and latency optimization techniques further enhance performance metrics.

The Large enterprises segment was valued at USD 9.60 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Server Storage Market Demand is Rising in North America Request Free Sample

The North American the market is experiencing significant growth due to the increasing adoption of high-performance computing (HPC) systems in sectors like government, BFSI, and healthcare. The healthcare industry's shift towards cloud adoption and the migration of their data storage to multi-tenant data center facilities are key drivers. Enterprise investments are fueling market expansion, offering substantial growth prospects for companies in the server storage sector. Notable infrastructure investments in the region include Vantage Data Centers' 192 MW campus in Columbus, Ohio, which was initiated in October 2024.

Another illustration of this trend is Microsoft's announcement in September 2023, revealing plans to invest USD35 billion in its Azure cloud platform over the next several years. These investments underscore the market's evolving nature and the underlying dynamics that continue to shape its growth trajectory.

Customer Landscape of Server Storage Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Server Storage Market

Companies are implementing various strategies, such as strategic alliances, server storage market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon.com Inc. - This company specializes in server storage solutions, enabling advanced features like thin provisioning, VDI snapshots, and fast cloning on compatible targets. Their offerings expose these capabilities, enhancing data management efficiency and flexibility.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon.com Inc.

- Apple Inc.

- Cisco Systems Inc.

- Cloud Software Group Inc.

- DataCore Software Corp.

- DataDirect Networks Inc.

- Dell Technologies Inc.

- Gigabyte Technology Co. Ltd.

- Google LLC

- HCL Technologies Ltd.

- Hewlett Packard Enterprise Co.

- Hitachi Vantara LLC

- Huawei Technologies Co. Ltd.

- International Business Machines Corp.

- Jair Network and Services Pvt. Ltd.

- Microsoft Corp.

- NetApp Inc.

- Nutanix Inc.

- NVIDIA Corp.

- Pure Storage Inc.

- Scale Computing

- StorMagic

- TATWA Technologies Ltd.

- velia.net Internetdienste GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Server Storage Market

- In August 2024, IBM announced the launch of its new line of Power10 servers, featuring IBM Elastic Storage Server (ESS) 9000, which supports up to 30 petabytes of data per system. This development marked a significant advancement in high-capacity server storage solutions (IBM Press Release, 2024).

- In November 2024, Dell Technologies and Intel Corporation formed a strategic partnership to optimize Dell's PowerEdge servers for Intel's upcoming SSDs, aiming to deliver enhanced performance and efficiency (Dell Technologies Press Release, 2024).

- In March 2025, Western Digital Corporation completed the acquisition of Kioxia Holdings Corporation, merging their respective storage solutions portfolios and expanding their combined market share in the market (Western Digital Press Release, 2025).

- In May 2025, Microsoft Azure announced the general availability of its Azure Archive Blob storage, a low-cost, long-term storage solution for infrequently accessed data, further strengthening its cloud storage offerings (Microsoft Azure Blog, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Server Storage Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

228 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 31.5% |

|

Market growth 2025-2029 |

USD 140.75 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

28.0 |

|

Key countries |

US, Germany, Canada, China, Japan, UK, France, India, Italy, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Server Storage Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

In the dynamic and ever-evolving the market, businesses seek to optimize storage performance for their virtual machines while implementing cost-saving measures such as data deduplication. Managing storage capacity in hybrid cloud environments is crucial, ensuring data security through encryption and access control. Choosing appropriate storage tiering for different data types is essential for efficient resource allocation and adherence to industry regulations. Designing a resilient storage infrastructure for disaster recovery is a critical business function, as data loss can lead to significant supply chain disruptions and operational planning setbacks. Migrating data to the cloud while maintaining performance requires careful consideration of storage technology and automating provisioning for improved efficiency. Monitoring storage performance and capacity utilization is key to optimizing costs and analyzing resource allocation. Implementing data lifecycle management for cost optimization and selecting appropriate storage technology for specific workloads are important strategies for businesses seeking to reduce power consumption in their data centers and improve data center efficiency. Integrating storage systems with virtualization platforms and managing storage compliance with industry regulations are also essential components of a robust storage strategy. Improving data center uptime with high-availability storage and assessing and upgrading storage infrastructure components are crucial for maintaining a competitive edge in today's market. Businesses must also plan for future storage capacity needs and ensure data governance strategies are in place to protect sensitive information. By implementing these strategies, companies can reduce power consumption in their data centers by up to 30% compared to outdated storage systems, leading to significant cost savings and operational improvements.

What are the Key Data Covered in this Server Storage Market Research and Growth Report?

-

What is the expected growth of the Server Storage Market between 2025 and 2029?

-

USD 140.75 billion, at a CAGR of 31.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Large enterprises and SMEs), Type (Enterprise and Hyperscale), Component (Hardware and Software), Service (Professional and Managed), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing need for edge computing, Rising cybersecurity threats

-

-

Who are the major players in the Server Storage Market?

-

Amazon.com Inc., Apple Inc., Cisco Systems Inc., Cloud Software Group Inc., DataCore Software Corp., DataDirect Networks Inc., Dell Technologies Inc., Gigabyte Technology Co. Ltd., Google LLC, HCL Technologies Ltd., Hewlett Packard Enterprise Co., Hitachi Vantara LLC, Huawei Technologies Co. Ltd., International Business Machines Corp., Jair Network and Services Pvt. Ltd., Microsoft Corp., NetApp Inc., Nutanix Inc., NVIDIA Corp., Pure Storage Inc., Scale Computing, StorMagic, TATWA Technologies Ltd., and velia.net Internetdienste GmbH

-

We can help! Our analysts can customize this server storage market research report to meet your requirements.

RIA -

RIA -