Silicones Market Size 2024-2028

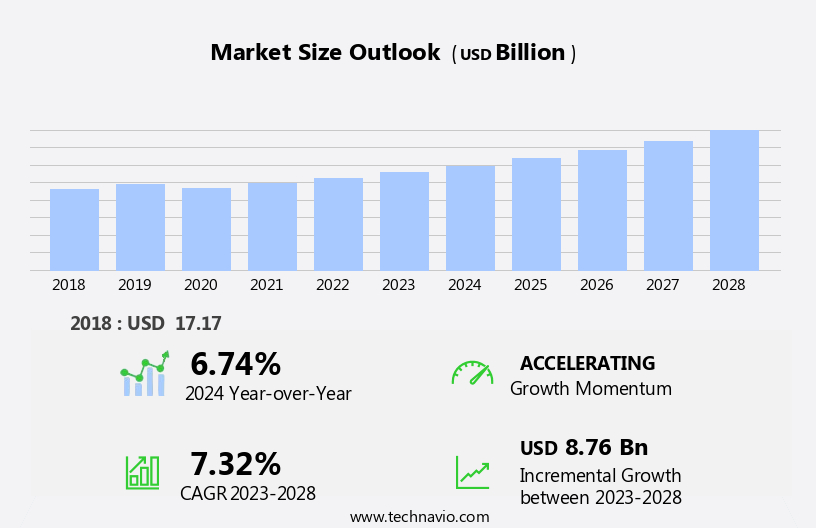

The silicones market size is forecast to increase by USD 8.76 billion, at a CAGR of 7.32% between 2023 and 2028.

- The market is experiencing significant growth, driven by the expanding construction industry and increasing adoption in the electrical and electronics sectors. The construction industry's upward trend is fueling the demand for silicones due to their excellent thermal and electrical insulation properties, making them an essential component in various building applications. Additionally, the electronics industry's growing reliance on silicones for insulation, sealing, and encapsulation applications is further fueling market growth. However, the market faces challenges due to the fluctuating prices of raw materials, primarily silica and methanol, which can impact the profitability of silicones manufacturers.

- These volatile prices can impact the cost structure of silicone manufacturers, potentially leading to price fluctuations in the market and affecting their profitability. Companies operating in this market must closely monitor raw material prices and adapt their strategies accordingly to maintain competitiveness and mitigate risks.

What will be the Size of the Silicones Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market showcases a dynamic and evolving landscape, with ongoing advancements and innovations shaping its various sectors. Silicone fillers play a crucial role in enhancing the properties of silicone resins, while medical applications continue to expand, driven by the biocompatibility and biodegradability of these materials. Silicone extrusion processes enable the production of diverse shapes and sizes, from tubing to profiles, while sealants ensure airtight and watertight bonds. Surface treatment and coatings enhance silicone's durability and resistance to environmental factors, such as heat, weather, and chemicals. Dielectric properties make silicones indispensable in the electronics industry, while anti-fouling and release agents cater to the maritime sector.

Silicone fluids serve as essential lubricants and coolants, and their chemical resistance is a key factor in numerous industrial applications. Adhesives, gels, rubbers, and elastomers expand the versatility of silicones, catering to diverse industries, including automotive, construction, and aerospace. The continuous pursuit of sustainability drives research into biodegradable silicones and eco-friendly production methods. Silicones' adaptability and performance make them a valuable asset in numerous industries, with ongoing advancements ensuring their relevance and growth in the market.

How is this Silicones Industry segmented?

The silicones industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Elastomers

- Fluids

- Resins

- Gels and others

- End-user

- Industrial process

- Construction

- Personal care and consumer products

- Transportation

- Others

- Application

- Industrial Process

- Construction

- Automotive

- Electronics

- Personal Care & Consumer Products

- Healthcare

- Energy

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

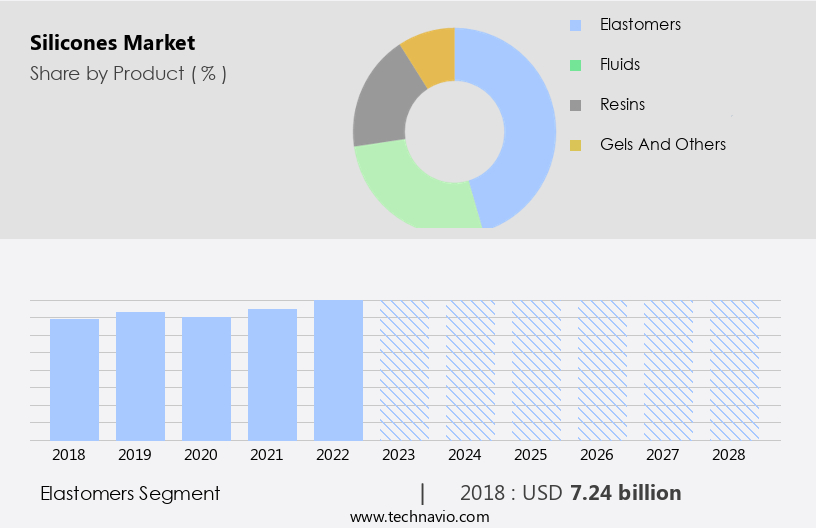

The elastomers segment is estimated to witness significant growth during the forecast period.

Silicone elastomers, a type of high-performance polymer, are manufactured by combining straight-chained, reactive, and linear polymer molecules with crosslinkers, reinforcements, and catalysts. This process results in elastomers with superior absorption, elasticity, and tear strength. Silicone elastomers come in various forms, including room-temperature vulcanized liquid silicone rubber and high-temperature vulcanized or heat-cured rubber. The selection of elastomer type depends on the characteristics of the straight-chain molecules and processing temperature. Silicone elastomers exhibit desirable properties, such as weatherability, thermal conductivity, heat and cold resistance, flame retardancy, electrical conductivity, gas permeability, vibration absorption, radiation resistance, tensile and tear strength, and ozone and UV resistance.

These properties make silicone elastomers suitable for diverse applications, including automotive, construction, electronics, healthcare, and aerospace industries. Crosslinking and vulcanization processes enhance the mechanical properties of silicone elastomers. Crosslinking creates a three-dimensional network within the elastomer, while vulcanization cures the elastomer to improve its durability and resistance to environmental stresses. Additives, such as fillers, pigments, and plasticizers, can be incorporated into silicone elastomers to modify their properties. For instance, silicone fillers enhance the elastomer's mechanical strength, while plasticizers improve its flexibility. Silicone elastomers can be processed using various techniques, including injection molding, calendaring, extrusion, casting, and transfer molding.

These processing methods enable the production of complex shapes and components with consistent dimensions and high precision. Silicone elastomers' biocompatibility, hydrophilicity, and water repellency make them suitable for medical applications. Their biodegradability and sustainability attributes are gaining increasing attention in the industry, driving the development of eco-friendly silicone elastomers. Silicone elastomers' dielectric properties, anti-fouling properties, and release agents make them valuable in the electronics industry. Their excellent chemical resistance and adhesion properties make them suitable for various industrial applications. In summary, silicone elastomers' versatile properties and wide range of applications make them an essential component in various industries.

Their production involves the use of additives, fillers, and various processing techniques, ensuring their high performance and durability. The ongoing research and development efforts in the field of silicone elastomers aim to enhance their properties and expand their applications.

The Elastomers segment was valued at USD 7.24 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

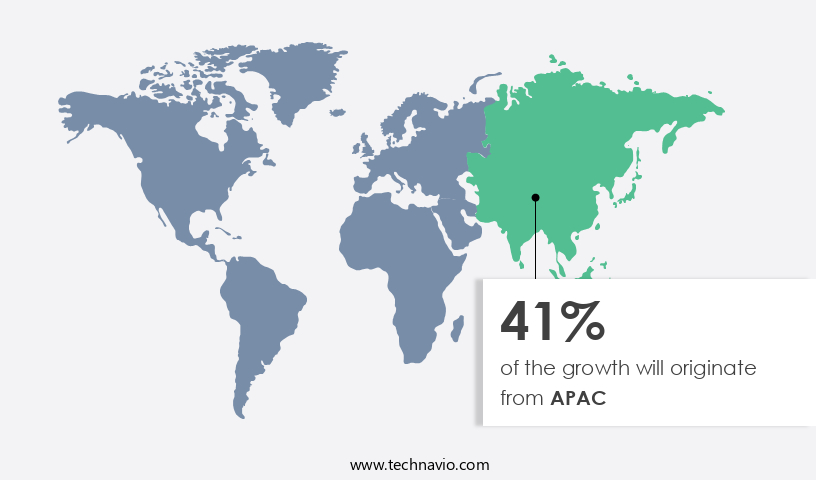

APAC is estimated to contribute 41% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is experiencing significant growth due to the increasing demand from various industries such as industrial processing, construction, automobile, and personal care. The market's expansion is driven by the unique properties of silicones, including hydrophobicity, heat resistance, biocompatibility, and chemical resistance. In the manufacturing sector, particularly in Asia Pacific (APAC), the growing number of companies is fueling the demand for silicone-based industrial lubricants, coatings, and sealants. China, Japan, India, Australia, South Korea, and Indonesia are the major contributors to the APAC market's growth. During the forecast period, APAC is anticipated to register the fastest growth rate due to the increasing demand in rapidly developing economies.

Silicone resins, gels, rubbers, and polymers are used extensively in various applications such as silicone injection molding, crosslinking, calendaring, extrusion, casting, and transfer molding. Additionally, the market is witnessing an increasing focus on sustainability and biodegradability, leading to the development of eco-friendly silicone products. Silicone surface treatment, coatings, and sealants are used to enhance the dielectric properties, anti-fouling properties, anti-static properties, and water repellency of various materials. Silicone adhesives and adhesion promoters are essential in various industries, including medical applications, where biocompatibility is crucial. Overall, the market's growth is driven by its versatile applications, unique properties, and increasing demand from various industries.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses the production, distribution, and application of silicone-based materials, which offer exceptional properties such as durability, heat resistance, and water repellency. These versatile polymers are utilized extensively in various industries, including automotive, construction, electronics, healthcare, and cosmetics. Silicone rubber, sealants, adhesives, coatings, and elastomers are key product categories. Applications range from automotive parts, such as gaskets and hoses, to building insulation, solar panel encapsulants, and semiconductor manufacturing. Silicone's unique properties make it an indispensable component in numerous industries, ensuring its continued growth and demand in the global market.

What are the key market drivers leading to the rise in the adoption of Silicones Industry?

- The construction industry's expansion is the primary catalyst fueling market growth.

- The global construction industry is experiencing notable expansion due to the escalating demand for office spaces, commercial complexes, and residential buildings. This growth trend is propelled by urbanization and substantial investments in infrastructure development, particularly in emerging economies. The increasing global population necessitates the construction of new residences and associated infrastructure, thereby fueling the demand for various construction materials, including silicones. In the realm of construction, silicones play a pivotal role due to their versatility and effectiveness in various applications. Silicone sealants are essential in creating dependable, pliable, and waterproof joints for a multitude of projects, ranging from small-scale domestic renovations to large-scale projects like skyscrapers and bridges.

- Silicone's unique properties, such as biocompatibility, hydrophilicity, and water repellency, make it a preferred choice for numerous applications within the construction sector. The process of silicone production involves techniques like injection molding, crosslinking, calendaring, and reinforcement, which contribute to its durability and sustainability. Silicone additives further enhance its properties, ensuring optimal performance in diverse conditions. As the construction industry continues to evolve, the demand for silicone-based products is poised to increase, driven by the industry's growth and the inherent advantages of silicones.

What are the market trends shaping the Silicones Industry?

- The electrical and electronics industry is experiencing a significant trend toward increased adoption of advanced technologies. This upward trend is a mandatory development, reflecting the industry's commitment to innovation and progress.

- Silicones are a versatile class of materials widely used in the electrical and electronics industry due to their unique properties. Silicone gels, in particular, offer excellent protection to adjoining components by absorbing thermomechanical stress. This makes them an ideal choice for various applications, including printed circuit boards, semiconductors, electronic control units, LED devices, and automotive electronic controllers. The durability and flexibility of silicone gels enable them to encapsulate cable accessories in power transmission and distribution systems, ensuring superior electrical properties and heat stability. Silicone elastomers are another essential category of silicones, extensively used in the electrical and electronics industry.

- They are particularly popular in automotive and general electronic components due to their excellent mechanical strength, electrical insulation properties, and resistance to extreme temperatures. The growing demand for advanced electronics in various industries, including automotive, aerospace, and telecommunications, is expected to fuel the growth of the market. In summary, the electrical and electronics industry relies heavily on silicones for their superior insulation, mechanical strength, and temperature resistance properties. Silicone gels and elastomers are widely used in various applications, from encapsulating electronic components to insulating cables in power transmission systems. The increasing demand for advanced electronics across various industries is expected to drive the growth of the market.

What challenges does the Silicones Industry face during its growth?

- The unpredictable fluctuations in the prices of raw materials pose a significant challenge to the growth of the industry.

- Silicones, derived from silicon metal and methanol, are valued for their exceptional chemical resistance, adhesion, and anti-slip properties. The silicone market's growth is driven by the diverse range of applications for these properties in various industries, including automotive, construction, healthcare, and electronics. Silicone polymers, such as silicone gels, rubbers, and monomers, are produced through silicone casting and curing processes. However, the market faces challenges due to the increasing cost of raw materials. The limited availability of silicon metal has led to a rise in its price, which in turn affects the cost of silicone-based products.

- Additionally, the energy-intensive production process of silicone fluids contributes to the escalating production costs. As a result, silicone companies are forced to increase their product prices, potentially hindering market growth. Despite these challenges, the demand for silicones remains strong due to their unique properties and versatile applications.

Exclusive Customer Landscape

The silicones market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the silicones market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, silicones market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ashland Global Holdings Inc. - The company specializes in providing a variety of silicone materials, formulated through silicone elastomers and emulsions. These offerings are optimized for fully automated industrial applications, including Liquid Injection Molding Systems. The diverse base chemistries cater to the specific demands of automated manufacturing processes, ensuring efficiency and consistency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ashland Global Holdings Inc.

- Avantor Inc.

- Basf SE

- Dow Inc.

- Elkem ASA

- Evonik Industries AG

- Gelest, Inc. (Mitsubishi Chemical Corporation)

- KCC Corporation

- Momentive Performance Materials Inc.

- Shin-Etsu Chemical Co., Ltd.

- Wacker Chemie AG

- Ashland Inc.

- Clariant AG

- Merck KGaA

- Mitsui Chemicals, Inc.

- Nippon Shokubai Co., Ltd.

- PMC Biogenix Inc.

- Silicone Engineering Ltd.

- Specialty Silicone Products, Inc.

- The Chemours Company

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Silicones Market

- In January 2024, Wacker Chemicals AG, a leading silicones manufacturer, announced the expansion of its production capacity for silicone fluids at its site in Nanjing, China. This expansion aimed to meet the growing demand for silicones in the automotive and electronics industries (Wacker Chemicals AG, 2024).

- In March 2024, Dow Inc. And Corning Incorporated entered into a strategic collaboration to develop and commercialize silicon-based materials for the high-growth markets of 5G infrastructure and renewable energy. This partnership combined Dow's silicones expertise with Corning's advanced materials science capabilities (Dow Inc., 2024).

- In May 2024, Momentive Performance Materials Inc. Completed the acquisition of the silicones business of Elkem ASA. This acquisition expanded Momentive's global footprint, particularly in Europe, and strengthened its position as a leading silicones supplier (Momentive Performance Materials Inc., 2024).

- In April 2025, BASF SE received approval from the European Commission for its acquisition of Solvay's European silicones business. This acquisition added significant capacity and capabilities to BASF's portfolio, making it one of the largest silicones producers globally (BASF SE, 2025).

Research Analyst Overview

- The market encompasses a diverse range of applications, from industrial to consumer goods. Quality control is paramount in ensuring the consistency and reliability of silicone-coated fabrics and silicone-reinforced plastics used in various industries. Silicone pricing remains a critical factor, influenced by supply chain dynamics and technological advancements in manufacturing processes, such as those used in producing polydimethylsiloxane (PDMS) and polyvinyl siloxane (PVS). Innovation continues to drive the market, with silicone biotechnology and nanotechnology leading the charge. PDMS and PVS are increasingly used in biomedical applications, while silicone nanoparticles are finding use in microfluidics and sensors. Silicone-based composites are gaining traction in aerospace applications, and silicone actuators are transforming automotive components.

- Safety regulations and testing standards are essential in ensuring the safety and efficacy of silicone-impregnated materials used in food packaging, cosmetics, and pharmaceuticals. The electronics sector is another significant market, with silicone playing a crucial role in semiconductor manufacturing and electronic components. Silicone sensors are also gaining popularity in various industries, from automotive to healthcare. The market is dynamic, with trends shifting towards sustainable manufacturing processes and the development of new applications. Silicone-coated fabrics are being used in building materials to improve insulation and durability, while PDMS and PVS are being explored for use in renewable energy applications.

- The future of the market is bright, with endless possibilities for innovation and growth.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Silicones Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

183 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.32% |

|

Market growth 2024-2028 |

USD 8.76 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.74 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Silicones Market Research and Growth Report?

- CAGR of the Silicones industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the silicones market growth of industry companies

We can help! Our analysts can customize this silicones market research report to meet your requirements.

RIA -

RIA -