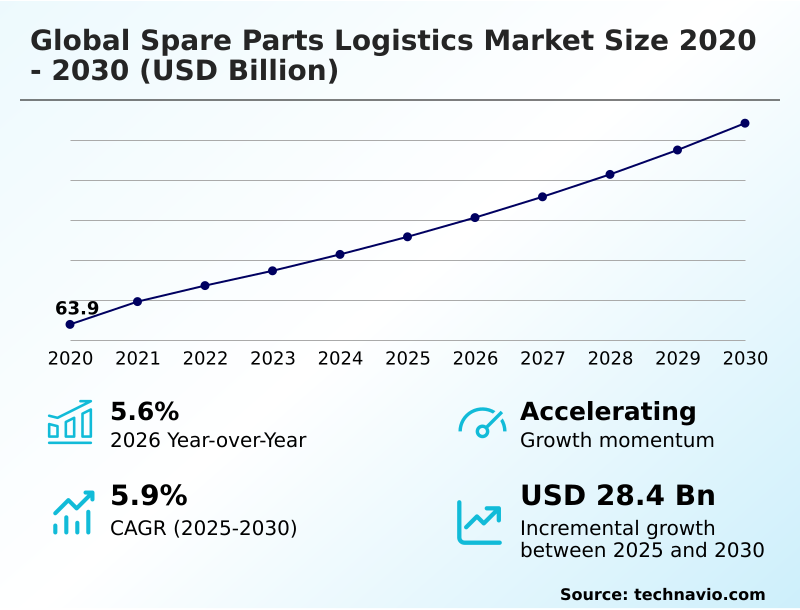

Spare Parts Logistics Market Size 2026-2030

The spare parts logistics market size is valued to increase by USD 28.4 billion, at a CAGR of 5.9% from 2025 to 2030. Increase in electronic components trade between India and China will drive the spare parts logistics market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 41.5% growth during the forecast period.

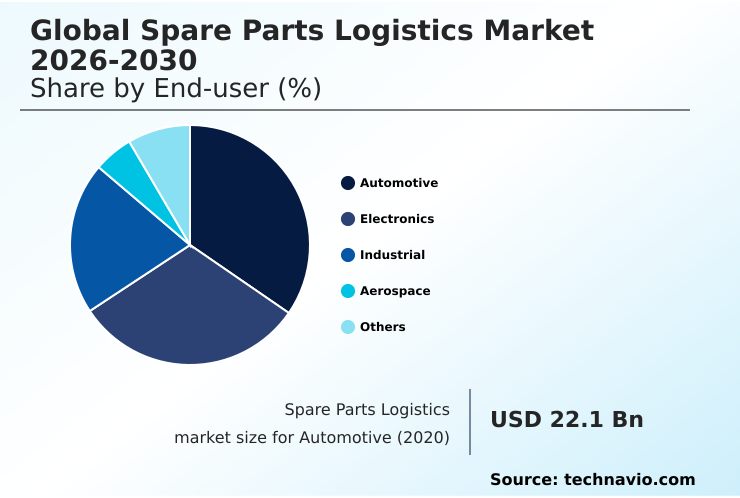

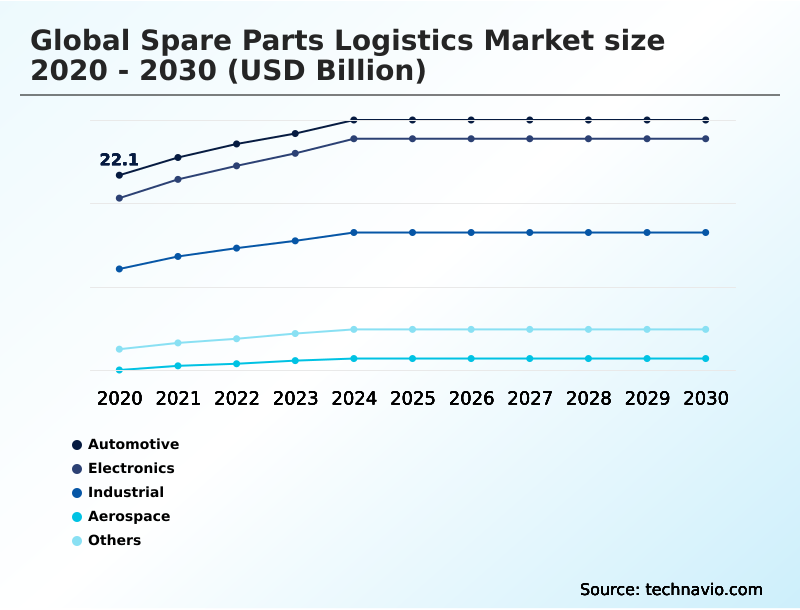

- By End-user - Automotive segment was valued at USD 27.4 billion in 2024

- By Type - Forward segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 50.3 billion

- Market Future Opportunities: USD 28.4 billion

- CAGR from 2025 to 2030 : 5.9%

Market Summary

- The spare parts logistics market is defined by its critical role in ensuring operational continuity across industries like automotive, aerospace, and electronics. Key drivers include the increasing average age of vehicles, which fuels demand for aftermarket parts, and rising hardware spending in APAC, which expands the installed base of equipment requiring maintenance.

- A central trend is the digitalization of the supply chain, where technologies such as real-time tracking with iot sensors and blockchain provide unprecedented visibility and security.

- For instance, a global manufacturer can use a predictive logistics network to anticipate component failure in its machinery, automatically dispatching a replacement part from a decentralized warehousing location before a breakdown occurs, thus minimizing costly downtime.

- However, the industry faces challenges from the rise of additive manufacturing, which alters traditional stocking strategies, and the complexities of executing time-bound deliveries across customized, multi-speed supply chains. The ongoing shortage of skilled labor further complicates network reliability and cost structures, pushing firms toward greater automation and logistics network resilience.

What will be the Size of the Spare Parts Logistics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Spare Parts Logistics Market Segmented?

The spare parts logistics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Automotive

- Electronics

- Industrial

- Aerospace

- Others

- Type

- Forward

- Reverse

- Source

- OEM channel

- Independent aftermarket

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By End-user Insights

The automotive segment is estimated to witness significant growth during the forecast period.

The automotive aftermarket segment is adapting to a dual-inventory reality, managing both traditional and electric vehicle components. This necessitates a resilient supply chain design focused on inventory optimization and forward logistics.

Advanced warehouse automation is becoming standard for handling the growing complexity of aftermarket spare parts. To ensure service continuity, strategies such as parts pooling and kitting are employed for time-critical delivery.

Some operators are exploring 3d printing for non-critical components to achieve lead time reduction, while IoT sensors enhance tracking, reducing errors in just-in-time delivery models by over 15%.

This strategic pivot ensures the automotive aftermarket remains responsive to evolving vehicle technologies and maintenance requirements.

The Automotive segment was valued at USD 27.4 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 41.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Spare Parts Logistics Market Demand is Rising in APAC Get Free Sample

The APAC region, contributing 41.5% of incremental growth, leads the spare parts logistics market, driven by its expansive manufacturing base. In countries like China and India, effective demand forecasting and real-time tracking are critical for managing complex cross-border logistics.

Europe emphasizes circular economy logistics, using advanced reverse logistics and robotics to process returns, while North America leverages a mature transportation management system for logistics network resilience.

Innovations such as a predictive logistics network enable firms to meet service level agreements, while digital twin technology aids in network optimization. For example, some firms have improved delivery precision by 25% by integrating these technologies.

Specialized services, like a cold-chain solution for medical parts, are expanding globally.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the global spare parts logistics market is evident in how different sectors approach supply chain challenges. For the spare parts logistics for automotive industry, the focus is on managing a vast network for aftermarket distribution.

- The impact of 3d printing on spare parts supply is a transformative factor, enabling on-demand production that challenges traditional freight forwarding for heavy machinery spare parts. Concurrently, the use of iot in spare parts warehouse management is becoming standard, enhancing supply chain visibility for service parts and enabling real-time tracking solutions for high-value parts.

- This technology is crucial for optimizing last-mile delivery for industrial parts. In specialized sectors, blockchain for aerospace spare parts traceability ensures authenticity, while cold chain logistics for medical equipment parts guarantees integrity. The complexities of reverse logistics for electronic components highlight the growing importance of circular economy models in automotive spare parts.

- To manage these diverse needs, firms employ ai-powered demand forecasting for aftermarket parts and sophisticated cost-to-serve models for aftermarket distribution. Strategies like decentralized warehousing strategies for spare parts and contract logistics for medical device spare parts are tailored to specific industry requirements.

- Automating inventory for aircraft on ground support demonstrates a high level of sophistication, directly tied to service level agreement management in logistics, where response times are twice as fast as manual systems.

- The role of digital twins in spare parts logistics is expanding, offering simulation capabilities to overcome the challenges of cross-border spare parts logistics and managing obsolescence in high-tech spare parts.

What are the key market drivers leading to the rise in the adoption of Spare Parts Logistics Industry?

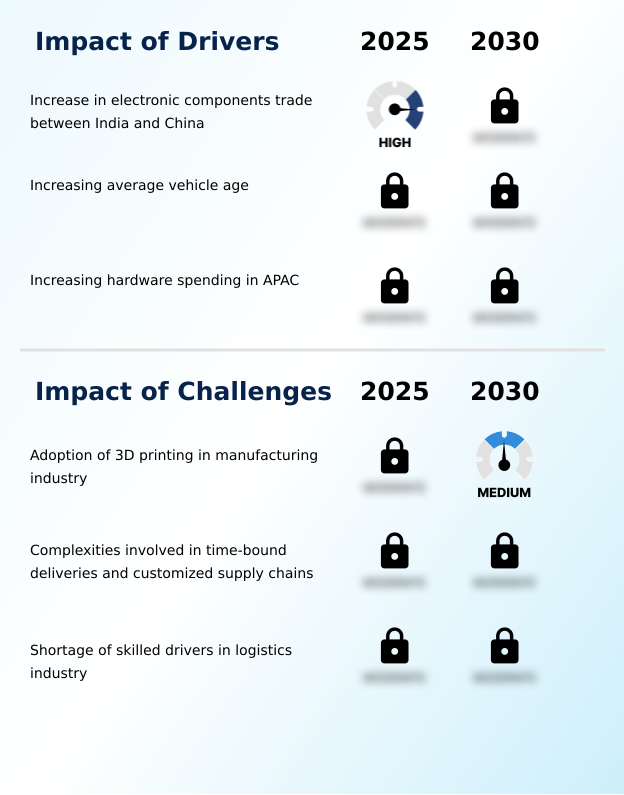

- The increasing trade of electronic components between India and China serves as a key driver for the spare parts logistics market by expanding the volume and complexity of cross-border component movements.

- Increasing hardware spending, particularly in APAC, is a major driver, expanding the installed base of equipment requiring industrial machinery maintenance and aftermarket spare parts. This fuels demand for effective aftermarket distribution and procurement logistics to ensure operational uptime.

- The rising average age of vehicles globally, with older models needing 20% more repairs, also boosts demand. Furthermore, growing trade between nations necessitates sophisticated cross-border logistics and improved customs clearance efficiency.

- This has led to investment in decentralized warehousing and field stocking locations to support predictive maintenance strategies and time-definite routing. These localized hubs are crucial for complex sectors like medical device logistics and for optimizing last-mile delivery.

What are the market trends shaping the Spare Parts Logistics Industry?

- The adoption of real-time tracking, enabled by the Internet of Things (IoT), is an influential trend. This technology is reshaping supply chain visibility and operational efficiency across logistics networks.

- The adoption of digital technologies is a primary trend reshaping the market. A supply chain control tower provides enhanced supply chain visibility, critical for managing high-tech service parts and providing aircraft on ground (aog) support. The use of blockchain traceability and smart contracts ensures end-to-end traceability, reducing disputes by up to 40%.

- Concurrently, mergers are enabling consolidation, allowing for integrated freight forwarding and advanced supply chain orchestration. Technology is also pivotal, with ai-driven inventory management optimizing multi-echelon inventory across global networks. Firms are increasingly using automated storage and retrieval systems and digital freight matching platforms, leading to a 25% improvement in warehouse throughput and logistics efficiency.

What challenges does the Spare Parts Logistics Industry face during its growth?

- The adoption of 3D printing in the manufacturing industry is a primary challenge, disrupting established inventory models and supply chain dynamics for spare parts.

- The rise of additive manufacturing and on-demand production presents a significant challenge, disrupting the traditional service supply chain and necessitating new approaches to component lifecycle management and obsolescence management. A detailed cost-to-serve analysis becomes critical as firms weigh printing versus shipping. The complexities of time-critical delivery and customized supply chains require dynamic inventory substitution and robust contract logistics.

- A shortage of skilled drivers further strains the system, with spot market rates increasing by over 30% in some regions. An integrated logistics provider must now manage intricate returns management and asset recovery processes, often requiring specialized value-added warehousing capabilities to handle unpredictable flows.

Exclusive Technavio Analysis on Customer Landscape

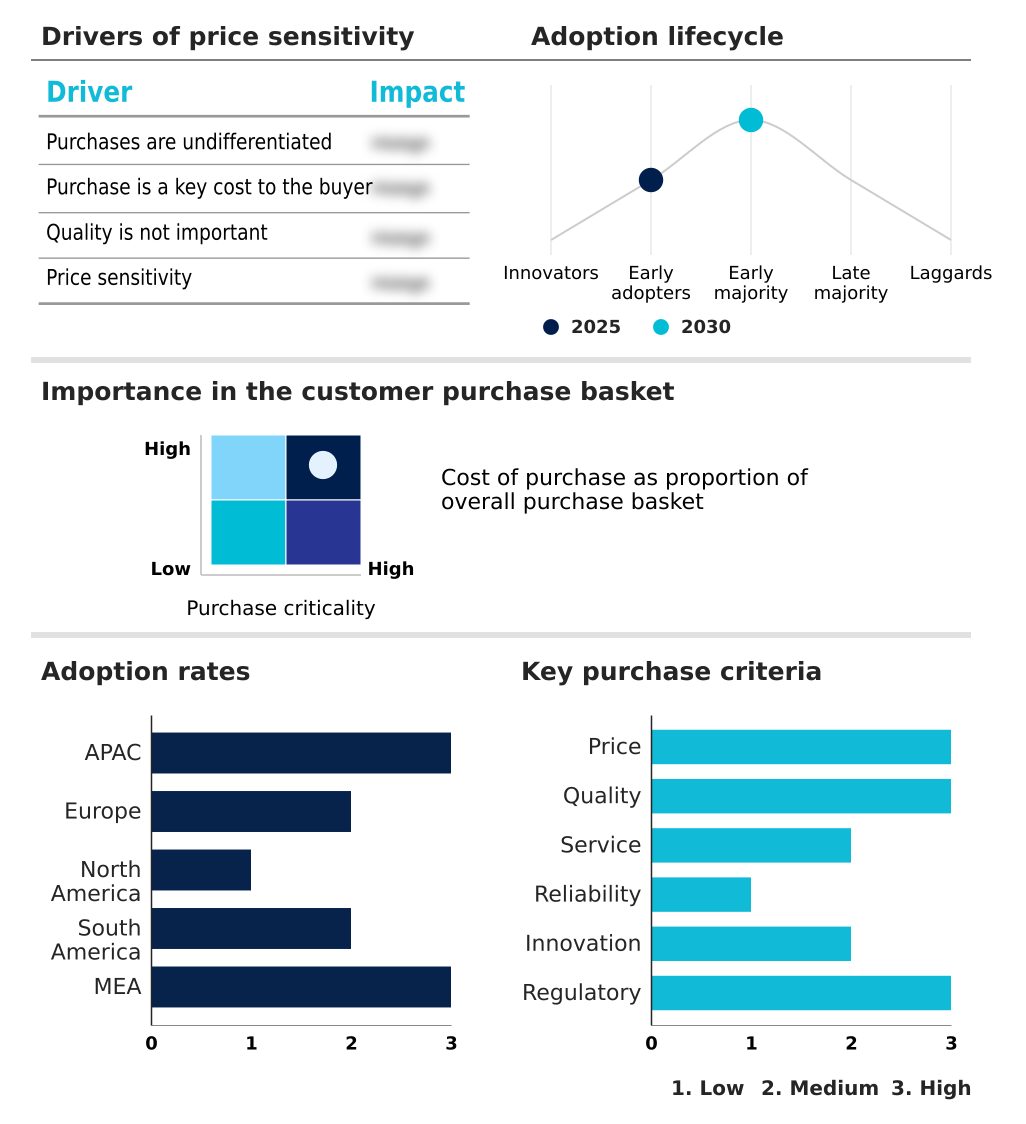

The spare parts logistics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the spare parts logistics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Spare Parts Logistics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, spare parts logistics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

CEVA Logistics SA - Specialized solutions integrate technology and regulatory compliance with time-critical order management, ensuring operational uptime and supply chain resilience for essential components.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- CEVA Logistics SA

- Dachser SE

- DB Cargo AG

- DHL International GmbH

- DSV AS

- Expeditors International Inc.

- FedEx Corp.

- GEODIS

- KLN Logistics Group Ltd.

- Kuehne Nagel Management AG

- Lufthansa Cargo AG

- Nippon Express Holdings Inc.

- Ryder System Inc.

- Scan Global Logistics

- SEKO Logistics

- Toyota Motor Corp.

- TVS Supply Chain Solutions

- United Parcel Service Inc.

- XPO Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Spare parts logistics market

- In August 2025, Caterpillar Incorporated finalized a strategic partnership with a software provider to integrate blockchain technology into its global parts tracking system, aiming to verify component authenticity and mitigate counterfeit risks.

- In May 2025, FedEx Express launched an enhanced cold-chain solution in Europe, tailored for the high-speed transit of sensitive spare parts for medical diagnostic imaging equipment.

- In March 2025, FedEx Corp. advanced its digital transformation by integrating artificial intelligence to predict customer demand and optimize delivery routes for its spare parts services.

- In February 2025, the logistics division of BMW Group operationalized a new regional distribution center in Hungary, featuring hydrogen-powered material handling equipment to support the growing demand for electric vehicle components.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Spare Parts Logistics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.9% |

| Market growth 2026-2030 | USD 28.4 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.6% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Chile, Argentina, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The spare parts logistics market is undergoing a significant transformation driven by the need for enhanced supply chain visibility and efficiency. Core operations like forward logistics and reverse logistics are being redefined by technologies such as iot sensors and blockchain traceability, enabling real-time tracking from origin to end-use.

- Companies are leveraging predictive maintenance and sophisticated demand forecasting to optimize multi-echelon inventory and reduce holding costs. The integration of warehouse automation, including robotics and automated storage and retrieval systems, is crucial for managing complex kitting and in-night delivery services, with some firms reporting a 30% reduction in order processing times.

- This pivot towards technology directly influences boardroom decisions on capital expenditure for digital twin and smart contracts implementation. The market's evolution also addresses challenges in last-mile delivery and cross-border logistics through decentralized warehousing and field stocking locations.

- As firms manage component lifecycle management and asset recovery, on-demand production via 3d printing and additive manufacturing offers a new paradigm for parts pooling and aftermarket distribution. This service supply chain requires robust freight forwarding and contract logistics to maintain service levels.

What are the Key Data Covered in this Spare Parts Logistics Market Research and Growth Report?

-

What is the expected growth of the Spare Parts Logistics Market between 2026 and 2030?

-

USD 28.4 billion, at a CAGR of 5.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Automotive, Electronics, Industrial, Aerospace, and Others), Type (Forward, and Reverse), Source (OEM channel, and Independent aftermarket) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increase in electronic components trade between India and China, Adoption of 3D printing in manufacturing industry

-

-

Who are the major players in the Spare Parts Logistics Market?

-

CEVA Logistics SA, Dachser SE, DB Cargo AG, DHL International GmbH, DSV AS, Expeditors International Inc., FedEx Corp., GEODIS, KLN Logistics Group Ltd., Kuehne Nagel Management AG, Lufthansa Cargo AG, Nippon Express Holdings Inc., Ryder System Inc., Scan Global Logistics, SEKO Logistics, Toyota Motor Corp., TVS Supply Chain Solutions, United Parcel Service Inc. and XPO Inc.

-

Market Research Insights

- The spare parts logistics market is shaped by the imperative for operational uptime and resilient supply chain design. The shift toward a predictive logistics network allows companies to meet stringent service level agreements, reducing equipment downtime by up to 30%. Through advanced network optimization and cost-to-serve analysis, firms achieve greater efficiency, with some improving forecast accuracy by over 20%.

- The management of aftermarket spare parts is increasingly complex, demanding localized inventory management and end-to-end traceability to ensure component authenticity and timely delivery. This strategic focus on integrated logistics providers and supply chain orchestration is essential for maintaining a competitive edge in a demanding global environment.

We can help! Our analysts can customize this spare parts logistics market research report to meet your requirements.

RIA -

RIA -