Steel Rebars Market Size 2026-2030

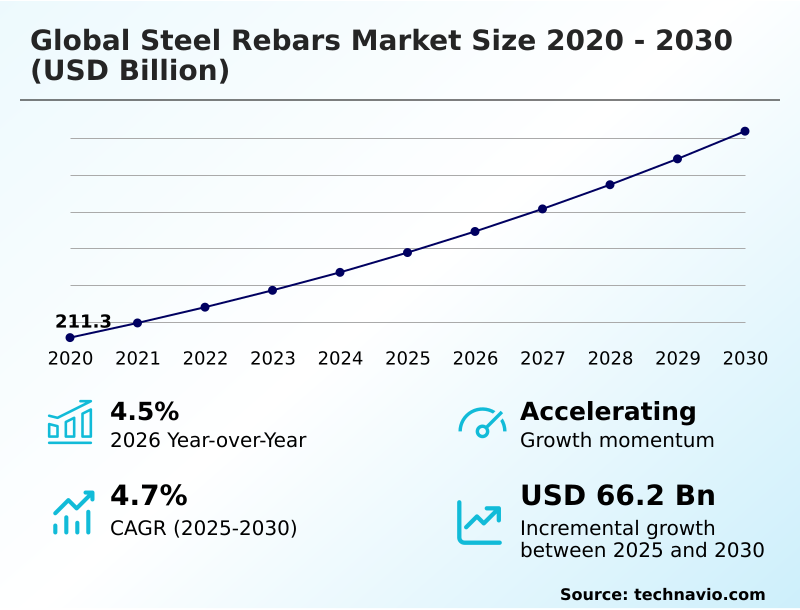

The Steel Rebars Market size was valued at USD 257.7 billion in 2025, growing at a CAGR of 4.7% during the forecast period 2026-2030.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 53% growth during the forecast period.

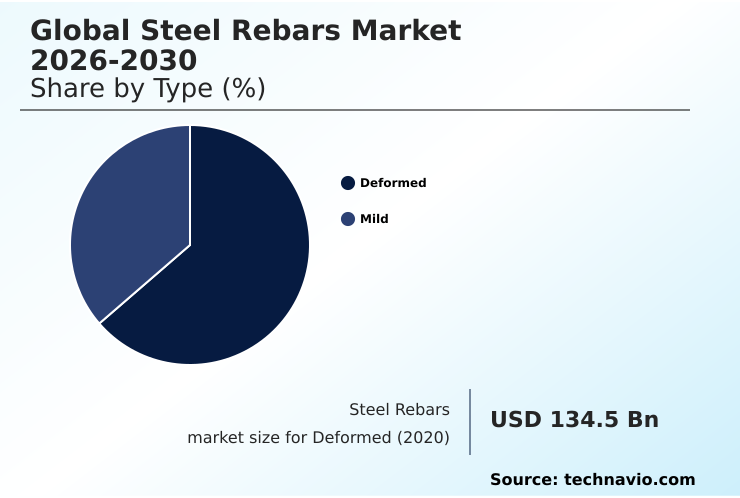

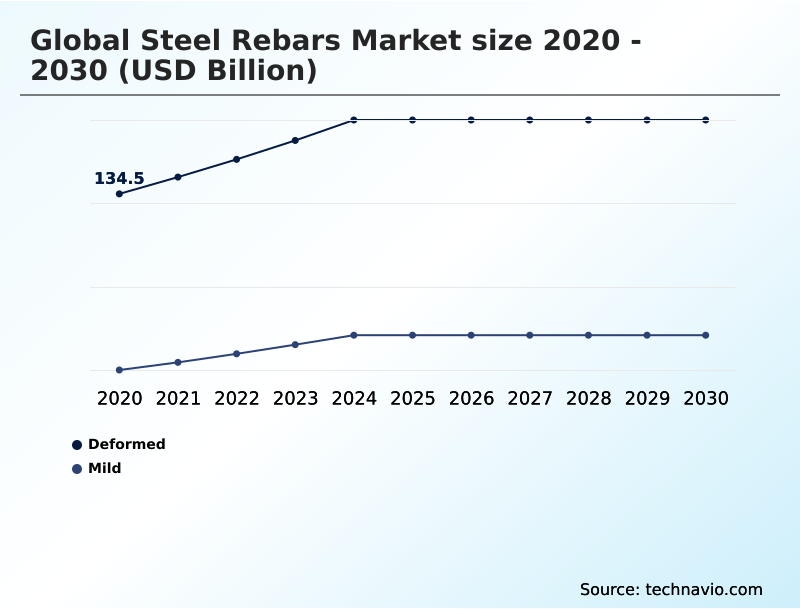

- By Type - Deformed segment was valued at USD 158.7 billion in 2024

- By Application - Residential segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 112.6 billion

- Market Future Opportunities 2025-2030: USD 66.2 billion

- CAGR from 2025 to 2030 : 4.7%

Market Summary

- The steel rebars market is characterized by steady demand, with an approximate 4.5% year-over-year growth driven by global construction. APAC continues to dominate the landscape, accounting for over 50% of the market's incremental growth, fueled by massive public infrastructure investment in the region.

- A key driver is the emphasis on infrastructure development, as nations invest heavily in transportation and utility projects that require vast quantities of reinforced concrete. Conversely, a primary challenge is raw material price volatility, which can increase production costs by over 20% in a single quarter, disrupting supply chain stability.

- For instance, a manufacturer must balance long-term supply contracts for iron ore against spot market price swings, directly impacting project bidding and profitability. This dynamic requires sophisticated risk management to maintain competitiveness in a market fundamentally linked to global economic health.

What will be the Size of the Steel Rebars Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Steel Rebars Market Segmented?

The steel rebars industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Deformed

- Mild

- Application

- Residential

- Commercial

- Public infrastructure

- Grade type

- Grade 60

- Grade 40

- Grade 75

- Grade 80

- Others

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- Middle East and Africa

- Saudi Arabia

- UAE

- Turkey

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

How is the Steel Rebars Market Segmented by Type?

The deformed segment is estimated to witness significant growth during the forecast period.

The deformed segment, which accounts for over 65% of market volume, is defined by its surface protrusions that enhance concrete bonding properties.

These high-strength deformed bars are essential for modern civil engineering, with demand driven by building code standards requiring superior seismic performance.

In practice, the use of advanced deformed rebar can reduce reinforcement congestion by up to 15% compared to lower-grade alternatives, enabling more efficient concrete placement.

The segment's reliance on thermo-mechanically treated (TMT) processes improves ductility, a critical factor for structural integrity in high-rise construction. This focus on performance ensures the segment's dominance in applications where tensile strength testing and load-bearing capacity are non-negotiable.

The Deformed segment was valued at USD 158.7 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Steel Rebars market is rising in the leading region?

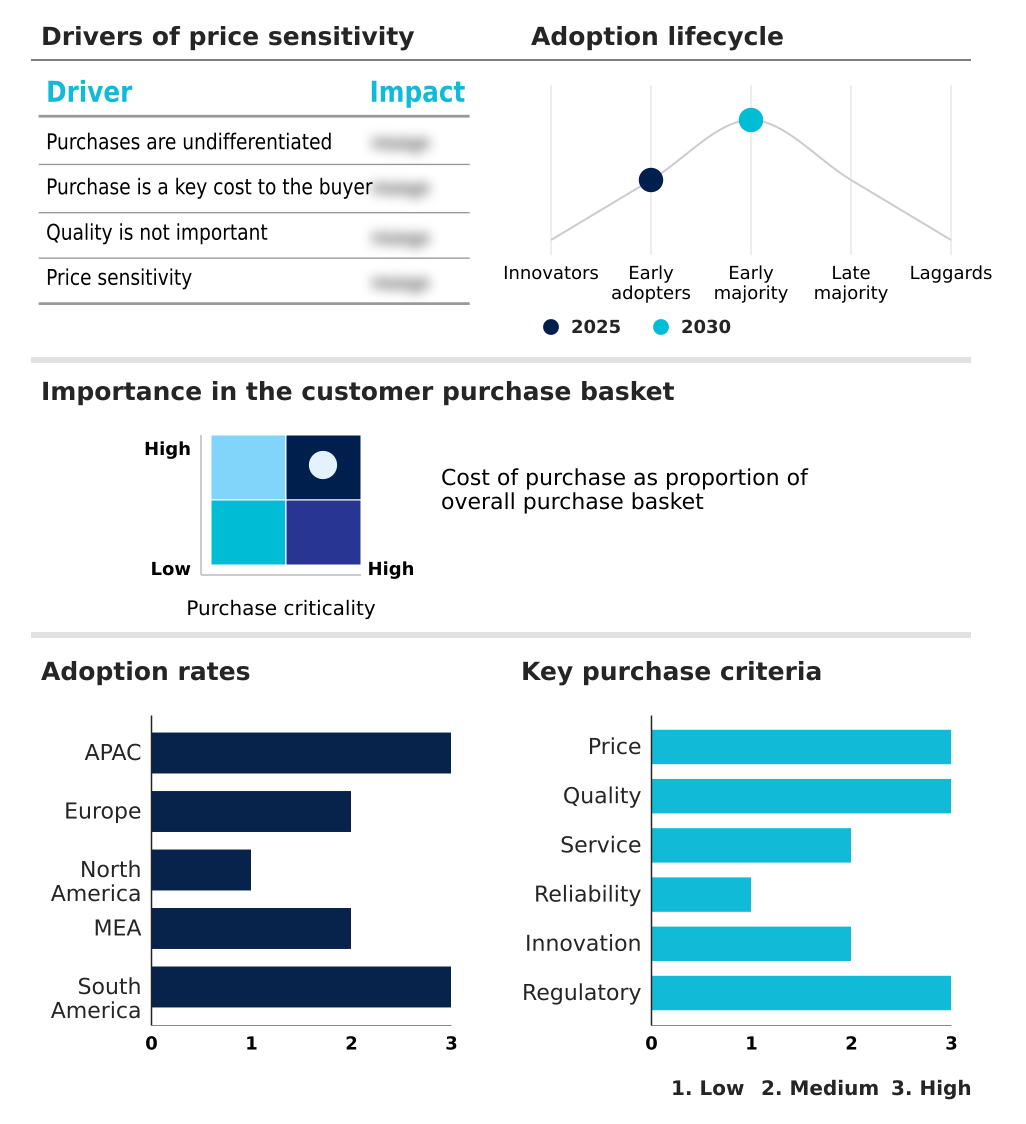

APAC is estimated to contribute 53% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Steel Rebars Market demand is rising in APAC Request Free Sample

The geographic landscape of the steel rebars market is dominated by APAC, which accounts for approximately 53% of the incremental growth, a figure more than double that of Europe at 19%.

This disparity is driven by massive public infrastructure investment and urban development projects in countries like China and India, with China alone representing nearly 45% of APAC's market value.

In contrast, the European market is characterized by a focus on sustainable building materials and retrofitting existing structures, leading to a higher demand for green steel production.

North America is experiencing a resurgence fueled by federal infrastructure spending, prioritizing durable infrastructure and domestic supply chains.

This regional divergence in demand drivers—new builds in APAC versus modernization and low-carbon steelmaking in Europe—necessitates distinct supply chain logistics and product strategies for global manufacturers.

What are the key Drivers, Trends, and Challenges in the Steel Rebars Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic procurement in the construction industry increasingly involves a detailed analysis of steel rebar price per ton vs quality, moving beyond simple cost metrics. For projects in aggressive environments, the specification of corrosion resistant rebar for coastal construction is now standard practice, extending the structural lifespan by over 30% compared to unprotected steel.

- The decision-making process is further complicated by the debate over using fiber reinforced polymer rebar, which, while having a higher initial cost, offers lifecycle savings in maintenance. Engineers must also consider the benefits of thermo-mechanically treated tmt bars benefits, such as superior weldability and ductility, which are critical in seismically active regions.

- The selection between high strength steel rebar grades is a crucial design choice, as using a higher grade can reduce steel tonnage by up to 15%, easing rebar congestion and improving concrete consolidation.

- This choice directly impacts the fundamental production method, influencing the electric arc furnace vs blast furnace steel debate, where sustainability goals and scrap availability play a pivotal role. As regulations tighten, understanding these trade-offs is essential for delivering resilient and cost-effective infrastructure, shaping both project execution and long-term asset performance.

What are the key market drivers leading to the rise in the adoption of Steel Rebars Industry?

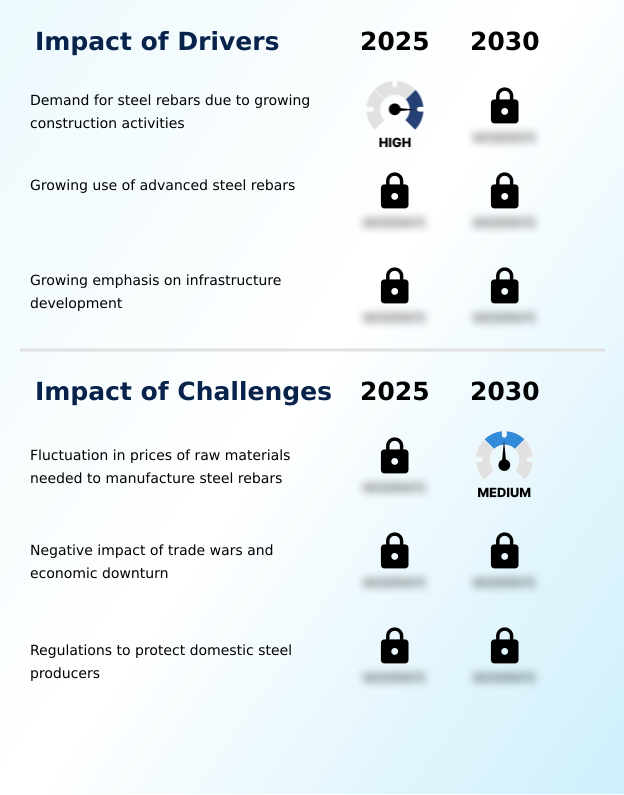

- The key market driver is the escalating demand for steel rebars, fueled by a global surge in construction and infrastructure development activities.

- Massive government spending on durable infrastructure is the foremost driver for the steel rebars market, with public infrastructure investment in some emerging economies increasing by over 20% in the last fiscal period.

- This surge in funding for projects like high-speed railways, bridges, and energy grids creates a direct and sustained demand for high-yield strength steel.

- Furthermore, the growing adoption of advanced rebar, such as thermo-mechanically treated bars, is driven by stricter structural engineering specifications. These advanced products offer a 15% improvement in seismic performance compared to conventional rebars, enabling the construction of more resilient structures.

- The use of advanced metallurgical control during production ensures consistent quality, which is critical for meeting these stringent new standards.

What are the market trends shaping the Steel Rebars Industry?

- An upcoming market trend is the continuous development of product innovations in steel rebars. This is driven by the industry's need for enhanced structural performance and material efficiency.

- A primary trend reshaping the steel rebars market is the accelerated shift toward sustainable manufacturing, specifically the adoption of electric arc furnace (EAF) steelmaking. This method, which uses over 90% recycled scrap as a feedstock, reduces carbon emissions by up to 75% compared to traditional blast furnace routes, aligning with global carbon neutrality goals and circular economy principles.

- This transition enables greater production flexibility and is a key factor in lifecycle cost analysis. Concurrently, the increasing use of alternatives like fiber-reinforced polymer (FRP) rebars for specialized applications is gaining momentum. Although a niche segment, FRP offers superior corrosion resistance and is 25% lighter than steel, making it ideal for durable infrastructure in harsh environments.

What challenges does the Steel Rebars Industry face during its growth?

- A key challenge affecting industry growth is the significant fluctuation in prices for essential raw materials required in the manufacturing of steel rebars.

- The most significant challenge for the steel rebars market is the extreme raw material price volatility, with key inputs like iron ore experiencing price swings of over 40% in a single year. This instability creates substantial uncertainty in production costing and can inflate final project costs for end-users by as much as 15%.

- Such fluctuations are compounded by geopolitical supply risks, which can disrupt established supply chain logistics with little warning. In addition, manufacturers face rising environmental compliance costs associated with emissions reduction mandates, further pressuring profit margins. This forces companies to balance long-term procurement strategies against short-term market dynamics, making financial planning and operational stability difficult to achieve.

Exclusive Technavio Analysis on Customer Landscape

The steel rebars market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the steel rebars market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Steel Rebars Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, steel rebars market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agni Steels Private Ltd. - Offerings include specialized thermo-mechanically treated and high-yield strength steel rebars for demanding construction applications, enhancing structural integrity.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agni Steels Private Ltd.

- ArcelorMittal SA

- Commercial Metals Co.

- Gerdau SA

- Hyundai Motor Co.

- JSW Holdings Ltd.

- Kamdhenu Ltd.

- MMD Steel

- MSP Steel and Power Ltd.

- Nucor Corp.

- Primegold International Ltd.

- Radha Smelters Pvt. Ltd.

- Rashtriya Ispat Nigam Ltd.

- Sage Metals Pvt. Ltd.

- Shagang Group Inc.

- Spark Electrodes Pvt. Ltd.

- Super Shakti Metalics Ltd.

- Tata Steel Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Steel industry, the increasing adoption of high-strength steel alloys, driven by demand for lighter and more durable end-products, directly boosts the market for advanced steel rebars that offer enhanced structural performance.

- A global emphasis on infrastructure and construction activities, with many governments launching stimulus programs, has significantly increased the foundational demand for steel long products, including the steel rebars used in nearly all public works.

- Heightened volatility in the prices of key raw materials like iron ore and coking coal, a persistent issue for steel producers, creates significant cost-management and pricing challenges for steel rebar manufacturers.

- Mounting environmental concerns and regulations are compelling steel producers to shift production methods, accelerating investment in technologies like electric arc furnaces for steel rebar manufacturing to reduce carbon emissions and meet sustainability mandates.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Steel Rebars Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.7% |

| Market growth 2026-2030 | USD 66.2 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.5% |

| Key countries | China, Japan, India, South Korea, Indonesia, Australia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Saudi Arabia, UAE, Turkey, South Africa, Israel, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The steel rebars market ecosystem operates on a value chain starting with suppliers of raw materials, primarily iron ore for blast furnace production and scrap steel for electric arc furnaces (EAFs), which now account for a significant share of production. Manufacturers, including integrated mills and mini-mills, transform these inputs into various grades of rebar.

- Their operations are heavily influenced by high capital expenditure and energy costs, which can represent over 20% of the total production expense. Distribution channels then move the finished products through wholesalers and service centers to end-users in the construction sector, including residential, commercial, and public infrastructure projects.

- Regulatory bodies enforce building code standards and environmental compliance, steering the industry towards high-yield strength steel and sustainable building materials. This intricate network is supported by logistics providers and R&D entities focused on developing advanced metallurgical controls and more efficient manufacturing processes.

What are the Key Data Covered in this Steel Rebars Market Research and Growth Report?

-

What is the expected growth of the Steel Rebars Market between 2026 and 2030?

-

The Steel Rebars Market is expected to grow by USD 66.2 billion during 2026-2030, registering a CAGR of 4.7%. Year-over-year growth in 2026 is estimated at 4.5%%. This acceleration is shaped by demand for steel rebars due to growing construction activities, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Deformed, and Mild), Application (Residential, Commercial, and Public infrastructure), Grade Type (Grade 60, Grade 40, Grade 75, Grade 80, and Others) and Geography (APAC, Europe, North America, Middle East and Africa, South America). Among these, the Deformed segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, Europe, North America, Middle East and Africa and South America. APAC is estimated to contribute 53% to market growth during the forecast period. Country-level analysis includes China, Japan, India, South Korea, Indonesia, Australia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Saudi Arabia, UAE, Turkey, South Africa, Israel, Brazil, Argentina and Chile, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is demand for steel rebars due to growing construction activities, which is accelerating investment and industry demand. The main challenge is fluctuation in prices of raw materials needed to manufacture steel rebars, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Steel Rebars Market?

-

Key vendors include Agni Steels Private Ltd., ArcelorMittal SA, Commercial Metals Co., Gerdau SA, Hyundai Motor Co., JSW Holdings Ltd., Kamdhenu Ltd., MMD Steel, MSP Steel and Power Ltd., Nucor Corp., Primegold International Ltd., Radha Smelters Pvt. Ltd., Rashtriya Ispat Nigam Ltd., Sage Metals Pvt. Ltd., Shagang Group Inc., Spark Electrodes Pvt. Ltd., Super Shakti Metalics Ltd. and Tata Steel Ltd.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The global steel rebars market landscape includes more than 15 major producers, with the top five commanding approximately 35% of the market share. Recent developments show a clear focus on regional production and sustainability. Leading North American manufacturers like Nucor Corp. and Commercial Metals Co.

- are investing in new rebar micro-mills, which are projected to increase regional capacity by over 10%. These mills utilize electric arc furnace technology to serve escalating demand from infrastructure projects. In Asia, players such as Tata Steel Ltd. are expanding capacity for long products to meet domestic needs.

- This strategic shift addresses supply chain vulnerabilities and aligns with the growing adoption of green steel production methods. The primary challenge remains managing the high capital expenditure required for such upgrades while navigating volatile energy and scrap steel prices.

We can help! Our analysts can customize this steel rebars market research report to meet your requirements.

RIA -

RIA -