US Pharmacy Market Size 2024-2028

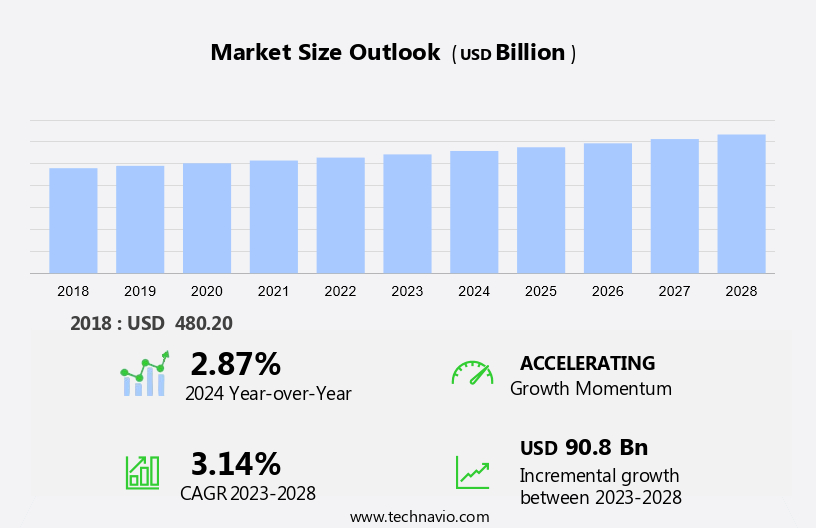

The US pharmacy market size is forecast to increase by USD 90.8 billion at a CAGR of 3.14% between 2023 and 2028. In the dynamic market, several drivers, trends, and challenges shape the industry landscape. The aging population in the United States is a significant growth factor, leading to an increase in pharmaceutical sales. Pharmaceutical exports, biotechnology, biosimilars, biologics, antiretroviral drugs, and vaccines are significant contributors to the sector's growth. This demographic shift also necessitates the adoption of telepharmacy services to cater to the healthcare needs of an expanding elderly population. Another trend in the market is the digitization of electronic health records (EHRs). Additionally, rising pricing in pharmaceuticals and reimbursement pressures are predefined factors influencing market growth. Quality control and licensing are essential aspects of the market, with industry associations playing a crucial role in setting standards and ensuring regulatory compliance. According to recent survey results, retail stores and hospitals remain the key distribution channels for pharmaceuticals.

The market encompasses a wide range of healthcare products, including prescription medications, over-the-counter drugs, and health supplements. Pharmacists play a crucial role in ensuring the safe and effective use of these products by patients. With the increasing adoption of technology in healthcare, digital solutions have become essential components of modern pharmacy services. The growth of retail and hospital pharmacies is significantly influenced by the demand for OTC medications and generic medicines, with projections tied to GDP performance, especially during the April-January period when items like hydroxychloroquine became prominent in the market for medical goods. One significant trend in the market is the integration of technology into various aspects of pharmacy operations.

Furthermore, these digital pharmacies offer convenience and accessibility, allowing patients to order their prescriptions and over-the-counter medications from the comfort of their homes. National health services are increasingly adopting EHRs to improve patient care and streamline operations. EHRs enable pharmacists to access patients' medical histories, allergies, and medication lists, ensuring accurate and safe prescription dispensing. Technology is also transforming the production and distribution of healthcare products. API producers are leveraging digital solutions to improve the efficiency and quality of their manufacturing processes. The use of technology in the market is expected to continue growing, driven by the need for improved patient care, increased convenience, and cost savings.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Prescription

- OTC

- Ownership

- Pharmacy chain

- Independent

- Type

- Retail pharmacy

- Hospital pharmacy

- Others

- Geography

- US

By Product Insights

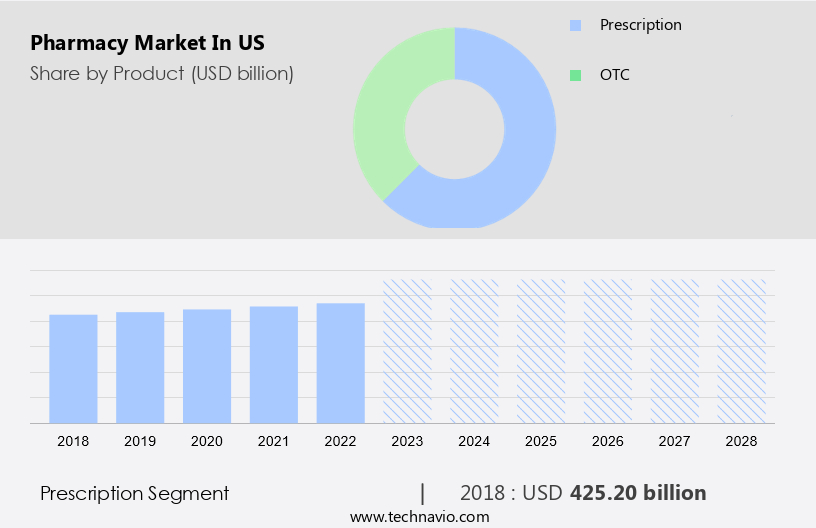

The Prescription segment is estimated to witness significant growth during the forecast period. Pharmaceutical businesses in the United States have leveraged the power of market segmentation to better understand consumer needs and preferences in the prescription sector. This approach allows companies to develop targeted marketing strategies, optimize inventory, and enhance overall customer satisfaction. One crucial aspect of prescription-based market segmentation involves categorizing customers based on their therapeutic requirements. These categories span various health conditions, including cardiovascular health, mental health, respiratory diseases, chronic pain management, and numerous others.

Furthermore, by segmenting the market, pharmacies ensure a comprehensive range of prescription medications for each category, enabling them to offer customized treatment solutions to their clients. The Internet's increasing penetration in the US has significantly influenced market segmentation in the pharmaceutical industry. The S-curve method, a popular analytical tool, helps visualize the growth patterns of various market segments. Exchange rates and representativeness are essential factors to consider when analyzing data from Global GCS data, a valuable resource, that provides insights into consumer behavior and trends within these segments. By staying abreast of market trends and consumer preferences, pharmacies can cater to the unique needs of their clientele, ultimately driving customer loyalty and business success.

Get a glance at the market share of various segments Request Free Sample

The prescription segment was valued at USD 425.20 billion in 2018 and showed a gradual increase during the forecast period.

Our market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The increasing aging population is the key driver of the market. In the United States, the aging population is leading to a significant shift in the pharmacy industry. With the baby boomer generation entering their golden years, there is a rising need for healthcare products, including prescription medications, over-the-counter drugs, and health supplements. Pharmacies have become essential components of the healthcare system, offering medication management and medical advice to a large number of elderly patients dealing with chronic conditions such as diabetes, hypertension, and arthritis. To cater to this demographic change, pharmacists are expanding their services. They now offer medication synchronization, immunizations, and medication treatment management. Technology plays a crucial role in this transformation, with digital solutions like electronic health records and data analytics enabling pharmacists to provide personalized care.

Patients can even access their medications online, making it more convenient for them to manage their health. The market in the US is expected to grow, driven by the increasing demand for healthcare services and the adoption of advanced technology.

Market Trends

The increasing use of telepharmacy services is the upcoming trend in the market. Telepharmacy is transforming the US market by integrating technology and pharmacist expertise to enhance patient care and medication access, particularly in underserved areas. Convenience is a major driver of telepharmacy's growth, as it eliminates the need for lengthy travel to obtain prescriptions and advice. Telepharmacies offer virtual consultations, allowing patients to interact with pharmacists remotely, improving medication administration and adherence. Pharmacists can provide detailed medication information, potential side effects, and usage instructions during these consultations, ensuring patients follow treatment plans effectively.

Furthermore, pharmacists must be licensed to practice in the state where they provide services, ensuring quality control. B2C enterprises and hospitals are increasingly adopting telepharmacy to expand their offerings and improve patient care. This trend is expected to continue, revolutionizing the pharmaceutical sales landscape. Demographic changes, including an aging population and increased urbanization, are predefined factors fueling telepharmacy's expansion. Industry associations and survey results indicate a positive shift towards telepharmacy services.

Market Challenge

Rising pricing in pharmaceuticals and reimbursement pressures is a key challenge affecting the market growth. In the United States, the pharmaceutical sector encounters a multifaceted challenge, marked by escalating drug costs and mounting reimbursement pressures. This predicament poses significant implications for both patients and healthcare providers. The escalating prices of pharmaceutical products have emerged as a topic of controversy in recent years. Patients may struggle to afford essential medications, leading to delayed or inadequate treatment. The financial burden of prescription drugs can negatively impact individuals' financial stability, as well as strain healthcare systems and insurance providers. Furthermore, the pharmaceutical industry grapples with reimbursement demands from diverse sources, including public health programs and private insurance entities.

Furthermore, preventive healthcare measures, such as vitamins, supplements, health monitoring devices, health screenings, and vaccinations, assume growing importance in mitigating the impact of these challenges. Local circumstances, particularly in rural areas and underserved communities, necessitate innovative solutions. Macroeconomic factors, including inflation and regulatory changes, also influence the market dynamics of pharmaceuticals.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Albertsons Companies Inc.: The company offers pharmacy services such as specialty care pharmacy, flu shots, and vaccines.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Cardinal Health Inc.

- CVS Health Corp.

- Humana Inc.

- McKesson Corp.

- Rite Aid Corp.

- The Cigna Group

- The Kroger Co.

- United Health Group Inc.

- Walgreens Boots Alliance Inc.

- Walmart Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a wide range of healthcare products, including prescription medications, over-the-counter drugs, health supplements, vitamins, and minerals. Pharmacists play a crucial role in dispensing these medications and providing advice on their safe and effective use. With the advent of technology, digital solutions such as electronic health records, data analytics, and telemedicine have transformed the industry. Preventive healthcare measures, like health monitoring devices, health screenings, vaccinations, and vitamins and supplements, have gained significant importance in recent years. Local special circumstances, such as rural areas and underserved communities, present unique challenges for the pharmaceutical sector. Macroeconomic factors, changing demographics, licensing, and quality control are predefined factors influencing the industry's growth.

Furthermore, B2C enterprises, including hospitals, retail stores, and e-pharmacies like Medly Pharmacy, Pharmaca, Pharmeasy, and Epharmacy, are major players in the pharmaceutical sales landscape. Pharmaceutical production involves a complex process, from raw material sourcing to manufacturing and distribution. The market is influenced by various factors, including internet penetration, industry associations, survey results, exchange rates, representativeness, GCS data, and national health services

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

138 |

|

Base year |

2023 |

|

Historic period |

2017-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.14% |

|

Market Growth 2024-2028 |

USD 90.8 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

2.87 |

|

Key companies profiled |

Albertsons Companies Inc., Cardinal Health Inc., CVS Health Corp., Humana Inc., McKesson Corp., Rite Aid Corp., The Cigna Group, The Kroger Co., United Health Group Inc., Walgreens Boots Alliance Inc., and Walmart Inc. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast , fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across US

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -