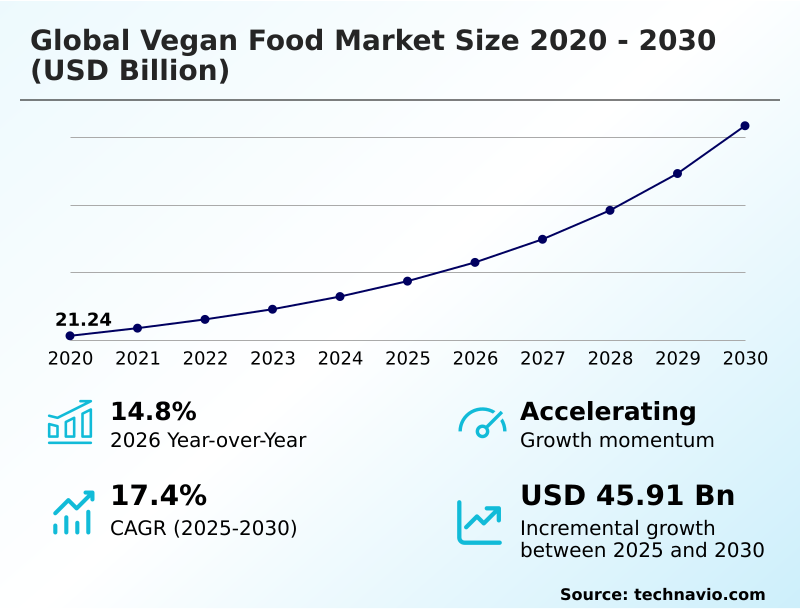

Vegan Food Market Size 2026-2030

The vegan food market size is valued to increase by USD 45.91 billion, at a CAGR of 17.4% from 2025 to 2030. Growing number of vegan consumers will drive the vegan food market.

Major Market Trends & Insights

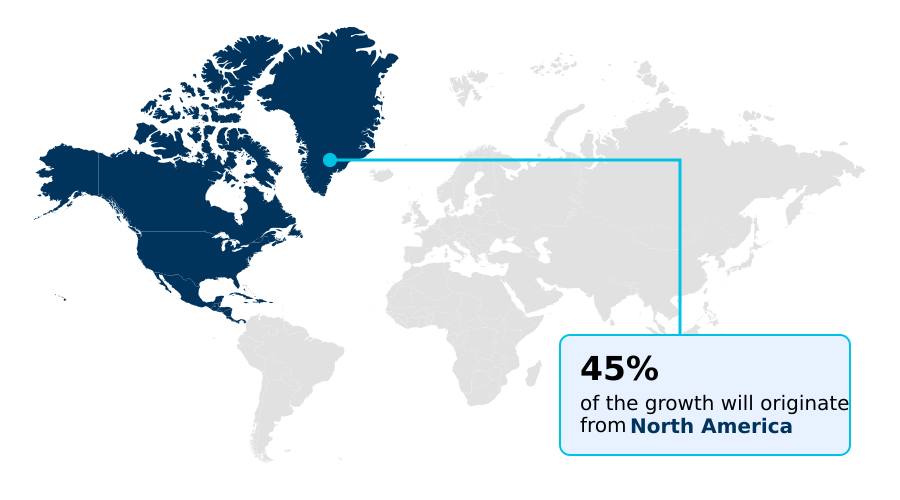

- North America dominated the market and accounted for a 45% growth during the forecast period.

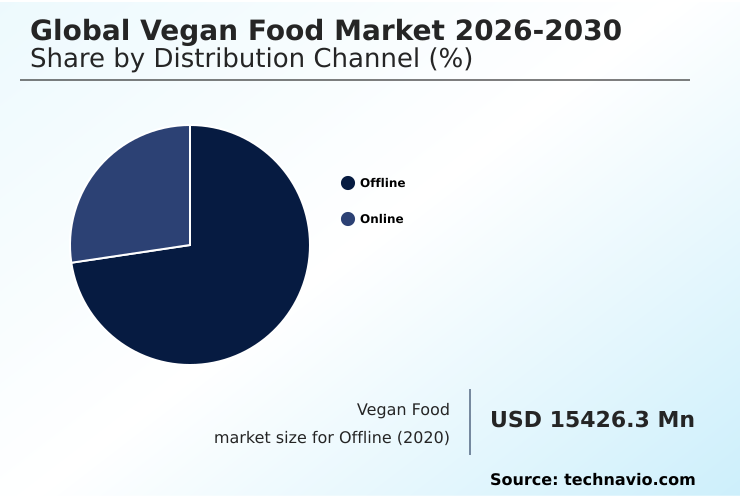

- By Distribution Channel - Offline segment was valued at USD 24.13 billion in 2024

- By Product - Dairy alternative segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 62.06 billion

- Market Future Opportunities: USD 45.91 billion

- CAGR from 2025 to 2030 : 17.4%

Market Summary

- The vegan food market is rapidly evolving, driven by a consumer shift toward healthier, more sustainable eating habits. This transition is moving the industry beyond basic offerings to complex products that replicate the sensory experience of conventional animal-based foods.

- Innovations in high-moisture extrusion are creating more realistic meat analogues, while developments in microbial fermentation are enabling the creation of advanced dairy alternatives with nuanced flavors. The demand for clean-label ingredients and non-GMO verification is a significant factor shaping product development.

- For instance, a food manufacturer aiming to launch a new line of plant-based cheese must navigate a complex supply chain to secure a stable source of plant-based casein.

- This process involves ensuring transparent sourcing, validating allergen-free formulations, and managing the logistics for novel ingredients, which can increase operational overhead but is crucial for meeting the expectations of discerning consumers and building brand loyalty in a competitive landscape. This commitment to food technology innovation and quality is essential for growth.

What will be the Size of the Vegan Food Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Vegan Food Market Segmented?

The vegan food industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

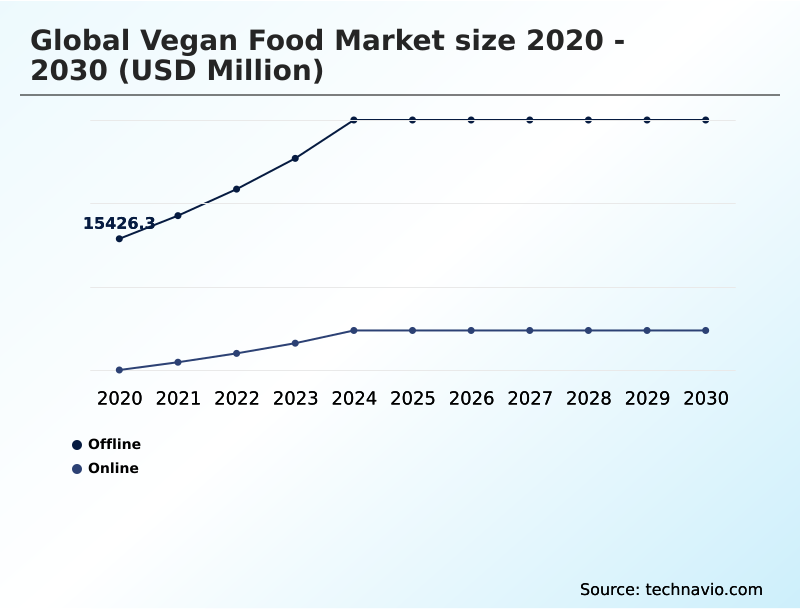

- Distribution channel

- Offline

- Online

- Product

- Dairy alternative

- Meat alternative

- Others

- Source

- Soy based

- Wheat based

- Oats based

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Distribution Channel Insights

The offline segment is estimated to witness significant growth during the forecast period.

The offline channel, encompassing supermarkets and specialty stores, remains the primary point of purchase, driven by established consumer purchasing habits.

The mainstream retail adoption of plant-based proteins has expanded product visibility, moving dairy alternatives and meat analogues from niche sections to prominent aisle placements. This shift is critical for reaching the growing flexitarian consumer base.

Strategic merchandising of private-label vegan products has also been instrumental, with retailers reporting that dedicated plant-based sections improve shopper engagement by over 20%.

The availability of ready-to-eat vegan meals and dairy-free confectionery alongside conventional items normalizes ethical food consumption and supports the omnichannel retail strategy by driving in-store traffic, complementing the growth of direct-to-consumer vegan brands.

The Offline segment was valued at USD 24.13 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 45% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Vegan Food Market Demand is Rising in North America Request Free Sample

The geographic landscape of the global vegan food market is characterized by established dominance in North America, which accounts for nearly 45% of the incremental growth, alongside rapid expansion in the APAC region.

In North America, the mainstream retail adoption of meat analogues and innovations in oat milk processing drive market maturity.

Conversely, APAC's growth is fueled by rising disposable incomes and a high prevalence of lactose intolerance, creating immense demand for lactose intolerance alternatives.

This regional divergence presents supply chain challenges; logistics in North America are optimized for mature cold-chain distribution, whereas scaling in APAC requires a 25% higher investment in developing localized sourcing for ingredients like soy protein concentrate to meet regional tastes and regulatory standards, impacting overall environmental impact reduction goals.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic success in the vegan food market hinges on a deep understanding of nuanced product attributes and consumer preferences. The debate over pea protein vs soy protein efficacy continues to drive formulation science, while the subtle oat milk impact on coffee flavor has become a critical factor in the food service channel.

- A primary focus for R&D teams is achieving desirable plant-based cheese melting properties, a persistent challenge in dairy alternative innovation. Furthermore, consumer perception of meat analogues is shifting, demanding more than just mimicry; it requires improving texture of meat substitutes through advanced technology in plant-based meat production.

- The clean label impact on purchasing decisions cannot be overstated, compelling brands to simplify ingredient lists. This involves a detailed cost analysis of vegan ingredients and a commitment to sustainable sourcing for plant proteins. For businesses, navigating vegan food supply chain logistics is as crucial as product development.

- A key decision involves formulating allergen-free vegan foods without compromising taste, which often requires a greater R&D investment—sometimes 30% higher than for standard formulations. High protein vegan product development remains a lucrative area, especially when marketing plant-based foods to flexitarians. Ensuring the nutritional value of fortified vegan milk and adhering to regulatory compliance for vegan labeling are non-negotiable.

- The industry also faces challenges in vegan seafood replication and must stay ahead of consumer trends in dairy alternatives. The significant investment in alternative protein startups indicates a future defined by continuous innovation in fermented foods in vegan diets and improvements in private label vegan food quality.

What are the key market drivers leading to the rise in the adoption of Vegan Food Industry?

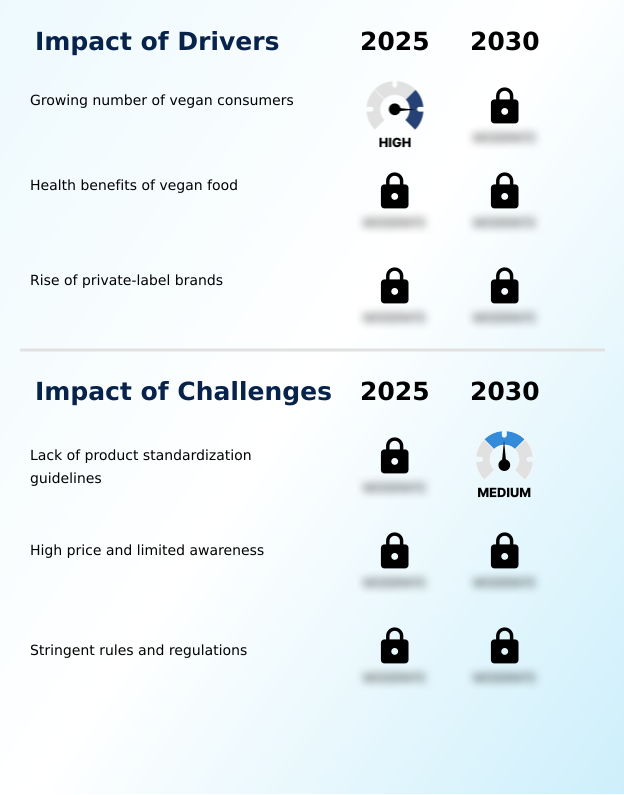

- The expanding global base of vegan consumers, driven by health and ethical considerations, is a primary factor fueling market growth.

- The growing number of consumers adopting vegan lifestyles is a primary market driver, compelling food service menu diversification. The perceived health benefits are encouraging a switch to plant-forward dietary guidelines, aligning with broader health and wellness trends.

- This shift is amplified by the rise of private-label vegan products, which now account for a significant share of sales.

- In some European markets, these store brands are up to 18% cheaper than animal-based equivalents, making ethical food consumption more accessible.

- The popularity of private labels is also linked to improved quality, with retailers launching exclusive lines of fortified vegan foods that cater to the demand for sustainable food systems and transparent sourcing.

What are the market trends shaping the Vegan Food Industry?

- An increase in new product launches to meet the rising demand for vegan food is a significant trend influencing market growth.

- New product launches are accelerating, driven by food technology innovation and a growing inclination toward plant-based proteins. The market is seeing a surge in plant-based seafood alternatives and sophisticated meat analogues, reflecting a broader trend of innovation in taste and nutritional value. Successful launches have been shown to increase a company's revenue stream by over 15% in the first year.

- Brands are focusing on global flavor profiles and clean-label ingredients, appealing to both health-conscious and flavor-driven consumers. The expansion of vegan meal kits and plant-based bakery products in mainstream retail and through direct-to-consumer vegan brands is normalizing plant-based eating, with some online platforms reporting a 40% rise in new customer acquisitions during promotional periods.

What challenges does the Vegan Food Industry face during its growth?

- The absence of uniform, international regulatory policies for product standardization presents a key challenge to market expansion.

- A key challenge is the lack of uniform international regulations, which complicates trade for companies navigating a patchwork of national standards for tempeh fermentation and seitan production. This fragmentation can increase compliance costs by up to 20%, impacting the final price for consumers.

- The high cost of vegan foods, often 1.5 to 2 times that of conventional products, also limits adoption, especially when animal welfare concerns are weighed against budget constraints.

- Addressing these challenges requires not just innovation in lowering production costs for items like texturized vegetable protein, but also efforts toward global regulatory harmonization to build trust and ensure product integrity across borders, especially for products with an allergen-free formulation.

Exclusive Technavio Analysis on Customer Landscape

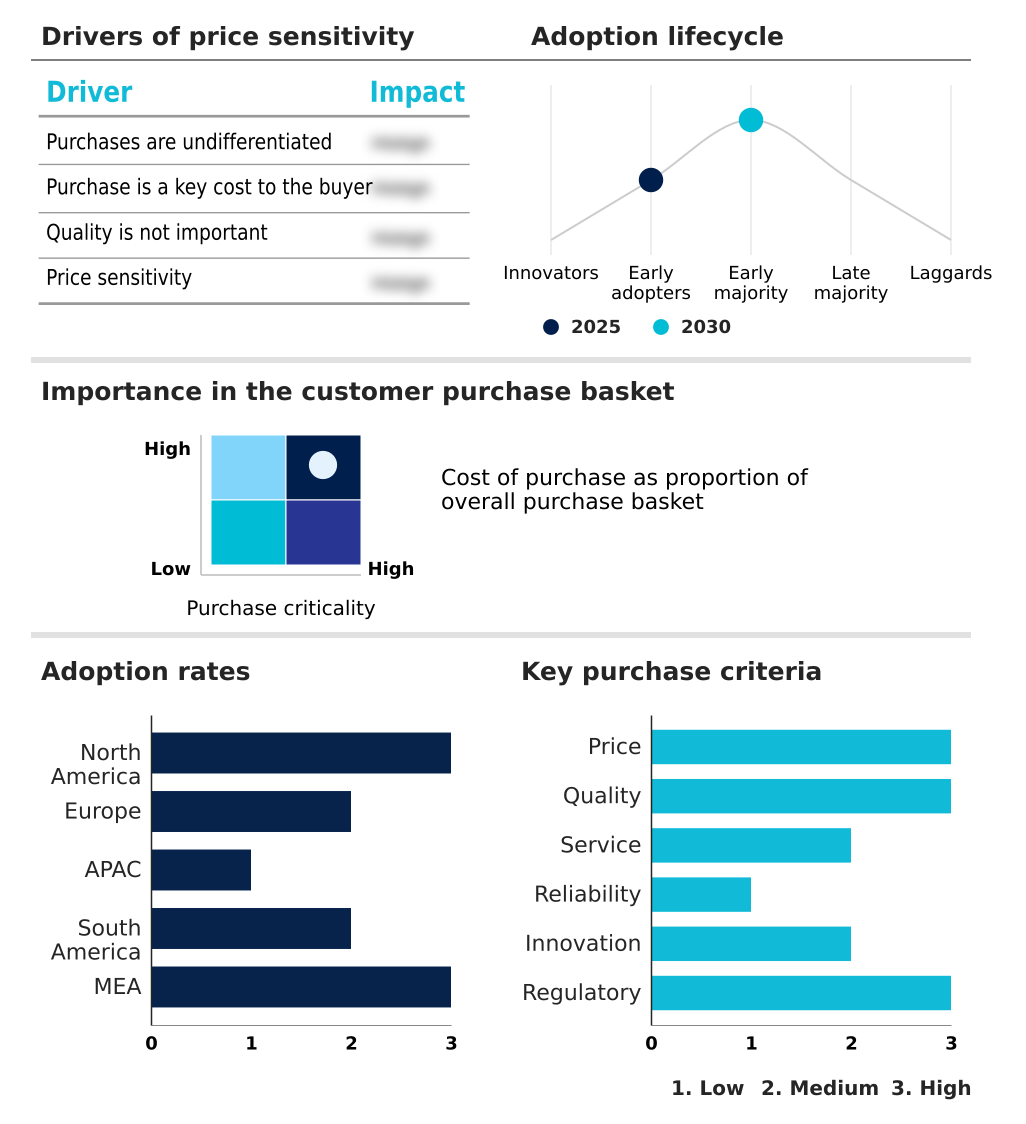

The vegan food market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the vegan food market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Vegan Food Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, vegan food market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amys Kitchen Inc. - Key offerings include a diverse array of plant-based dairy and meat alternatives, catering to evolving consumer health, ethical, and dietary preferences.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amys Kitchen Inc.

- Bega Cheese Ltd.

- Beyond Meat Inc.

- Blue Diamond Growers

- Danone S.A.

- Earths Own Food Co. Inc.

- Eden Foods Inc.

- First Grade International Ltd.

- Maple Leaf Foods Inc.

- Organic Valley

- Otsuka Holdings Co. Ltd.

- Ripple Foods PBC

- Saputo Inc.

- SunOpta Inc.

- The Hain Celestial Group

- Tofutti Brands Inc.

- VBites Foods Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Vegan food market

- In May, 2025, Minor Figures, a UK-based company, launched a new range of functional oat milk beverages called Hyper Oat, featuring ingredients like adaptogens and nootropics to cater to consumer interest in wellness benefits beyond basic nutrition.

- In March, 2025, the Food Safety and Standards Authority of India (FSSAI) published draft amendments to its vegan food regulations, signaling a move towards more stringent compliance and certification for imported vegan products to enhance consumer trust.

- In January, 2025, Vivera, a plant-based meat brand, expanded its Protein Bites range with two new varieties, Tex-Mex and Garden Greens, offering a whole-food-based option that moves beyond direct meat imitation.

- In December, 2024, Marfrig, a major global meat industry player, launched a new gourmet plant-based hamburger in Brazil under its Revolution brand, with plans for international expansion, indicating the mainstreaming of vegan food in South America.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Vegan Food Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 293 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 17.4% |

| Market growth 2026-2030 | USD 45910.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 14.8% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The vegan food market is undergoing a significant transformation, moving beyond simple soy-based products to sophisticated meat analogues and dairy alternatives developed through advanced food technology innovation. Key to this evolution is the use of high-moisture extrusion to create realistic textures and microbial fermentation to develop complex flavors in products like cultured soy and plant-based casein for vegan cheese culturing.

- The demand for clean-label ingredients is driving a focus on non-GMO verification and sustainable ingredient sourcing. Formulators are leveraging vital wheat gluten for seitan production, texturized vegetable protein for structure, and pea protein isolate for allergen-free formulation. This shift has boardroom-level implications, particularly for R&D budgeting.

- For instance, achieving superior sensory profiles in plant-based seafood alternatives or through tempeh fermentation requires specialized expertise, increasing development costs by up to 25% compared to simpler formulations.

- The emphasis on nutritional fortification and the development of fortified vegan foods with natural plant extracts underscores the market’s pivot toward health-centric offerings, while innovations in oat milk processing continue to disrupt the beverage sector.

What are the Key Data Covered in this Vegan Food Market Research and Growth Report?

-

What is the expected growth of the Vegan Food Market between 2026 and 2030?

-

USD 45.91 billion, at a CAGR of 17.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Offline, and Online), Product (Dairy alternative, Meat alternative, and Others), Source (Soy based, Wheat based, Oats based, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing number of vegan consumers, Lack of product standardization guidelines

-

-

Who are the major players in the Vegan Food Market?

-

Amys Kitchen Inc., Bega Cheese Ltd., Beyond Meat Inc., Blue Diamond Growers, Danone S.A., Earths Own Food Co. Inc., Eden Foods Inc., First Grade International Ltd., Maple Leaf Foods Inc., Organic Valley, Otsuka Holdings Co. Ltd., Ripple Foods PBC, Saputo Inc., SunOpta Inc., The Hain Celestial Group, Tofutti Brands Inc. and VBites Foods Ltd.

-

Market Research Insights

- The market's momentum is increasingly shaped by evolving consumer purchasing habits and a pronounced shift toward ethical food consumption. Growth is not just driven by a dedicated vegan base but by a much larger flexitarian consumer base, with reports indicating nearly half of consumers now purchase private-label vegan products, citing improved quality and affordability.

- This has led to a 15% increase in shelf space for store brands in major retail chains. Furthermore, the focus on health and wellness trends is a powerful catalyst; recent surveys show that over 58% of individuals adopting plant-forward dietary guidelines report enhanced well-being.

- This consumer sentiment is compelling food service menu diversification and supporting the expansion of direct-to-consumer vegan brands that leverage eco-friendly packaging.

We can help! Our analysts can customize this vegan food market research report to meet your requirements.