Vetronics Market Size 2024-2028

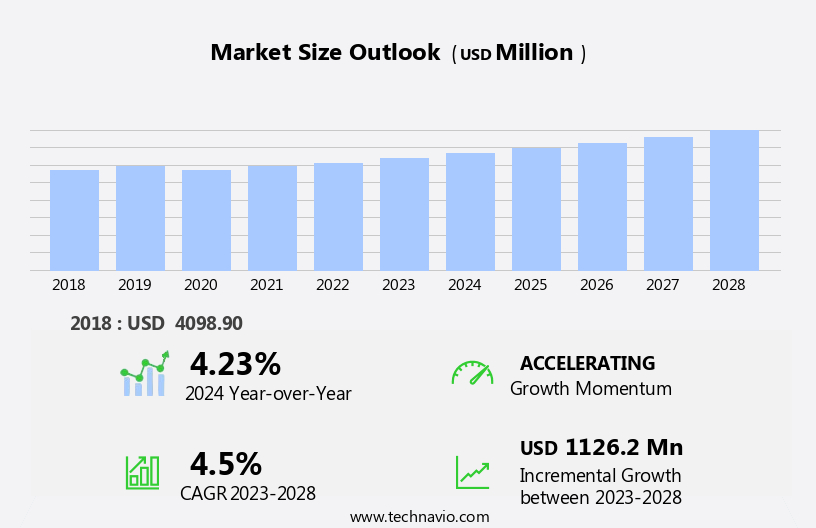

The vetronics market size is forecast to increase by USD 1.13 billion at a CAGR of 4.5% between 2023 and 2028.

What will be the Size of the Vetronics Market During the Forecast Period?

How is this Vetronics Industry segmented and which is the largest segment?

The vetronics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Military

- Homeland security

- Geography

- North America

- US

- Europe

- France

- APAC

- China

- India

- South America

- Middle East and Africa

- North America

By Application Insights

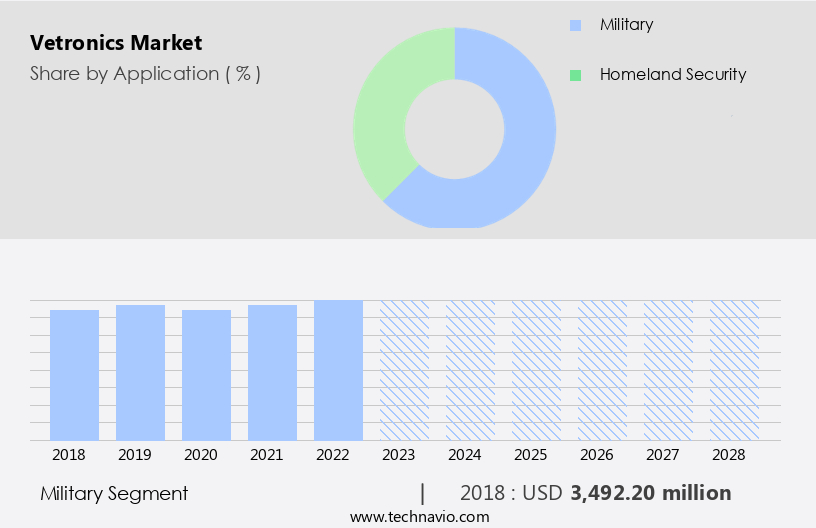

- The military segment is estimated to witness significant growth during the forecast period.

Ground vehicles in military applications are increasingly incorporating advanced technologies for intelligence, surveillance, and reconnaissance (ISR), high-definition video streaming, and threat detection. These innovations necessitate the integration of sophisticated vetronics systems capable of managing complex hardware and software upgrades. The use of open commercial off-the-shelf (COTS) architectures for high data-exchange rates can introduce signal-integrity issues at various levels of the system, including processors. The escalating threats to military vehicles and the evolution of weapons necessitate advanced threat detection and mitigation systems. Modern warfare demands agility, operational capacities, and self-protection. Vetronics systems play a crucial role in enabling joint operations, communication, navigation, power, and vehicle health management.

They include advanced communication systems, modernization programs, and procurement initiatives for next-generation vehicles. Vetronics architecture encompasses a digital hub, mobility system, inter-vehicle communication, and secure communications systems. It also includes vehicle protection systems, weapon control systems, C3 systems, and sensor and optronics. Homeland security applications, such as border security and cross-border security, also benefit from these advanced technologies.

Get a glance at the Vetronics Industry report of share of various segments Request Free Sample

The Military segment was valued at USD 3.49 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

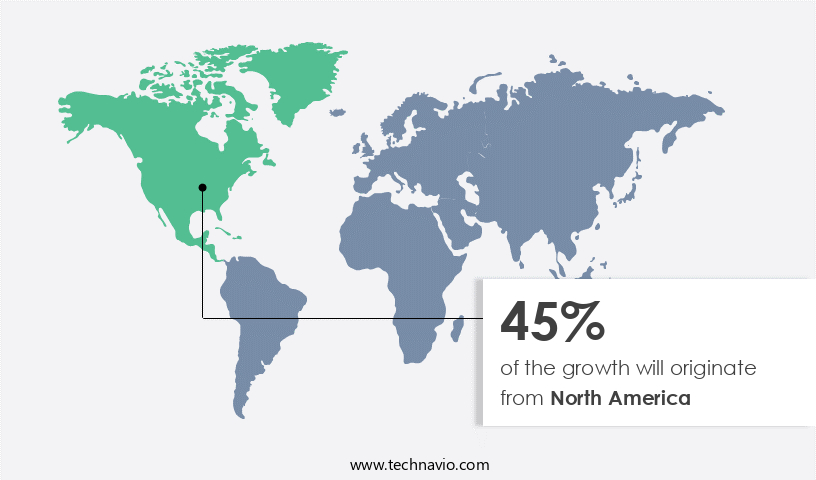

- North America is estimated to contribute 45% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American the market is driven by the significant military presence, particularly In the United States, which is the largest consumer of vetronics systems In the region. Key market participants, such as Curtiss-Wright Corp. And General Dynamics Corp., contribute significantly to the market's expansion in North America and beyond. Military forces In the region recognize the importance of advanced vetronics systems to optimize vehicle performance. Defense agencies are modernizing their fleets by upgrading vetronics systems, including communication, navigation, power, and vehicle protection. These upgrades aim to enhance operational capacities, agility, and self-protection against various threats. The integration of advanced electronic systems, artificial intelligence, and autonomous driving technologies further bolsters the market's growth.

Vetronics systems are essential for joint operations, homeland security, and border security applications. Key technologies include advanced communication systems, modernization programs, and digital hubs for mobility systems. The market encompasses a wide range of ground vehicles, including main battle tanks, light armored vehicles, armored personnel carriers, infantry fighting vehicles, and amphibious armored vehicles. Additionally, the market includes unmanned ground and aerial vehicles, drones, and portable power systems. The market's growth is influenced by the increasing demand for hybrid vehicles, unmanned vehicles, and the integration of cybersecurity measures to counteract cyber attacks.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Vetronics Industry?

Modernization of existing military vehicles is the key driver of the market.

What are the market trends shaping the Vetronics Industry?

Development of advanced vetronics for next-generation military vehicles is the upcoming market trend.

What challenges does the Vetronics Industry face during its growth?

Cybersecurity concerns is a key challenge affecting the industry growth.

Exclusive Customer Landscape

The vetronics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the vetronics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, vetronics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Adecco Group AG - The company specializes in providing advanced vetronics solutions, featuring integrated active protection systems and electro-optical commander sights. These technologies enhance situational awareness and ensure reliable system performance for various military and defense applications. The vetronics offerings cater to the growing demand for sophisticated electronic systems in land, naval, and aerospace sectors. By combining cutting-edge technology and robust design, the company delivers high-performance solutions that meet the stringent requirements of defense organizations worldwide.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adecco Group AG

- AMETEK Inc.

- BAE Systems Plc

- Curtiss Wright Corp

- Elbit Systems Ltd.

- General Dynamics Corp.

- Kongsberg Gruppen ASA

- Krauss Maffei Wegmann GmbH and Co. KG

- L3Harris Technologies Inc.

- Leonardo Spa

- Lockheed Martin Corp.

- Moog Inc.

- Oshkosh Corp.

- Rheinmetall AG

- RTX Corp.

- Saab AB

- TE Connectivity Ltd.

- Thales Group

- Ultra Electronics Holdings Plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Vetronics, or Veterans and Electronics, refers to the integration of advanced electronic systems in military ground vehicles and naval vessels. This market encompasses a wide range of technologies, including communication systems, navigation and display, sensor and optronics, power systems, and vehicle health management. The demand for vetronics systems is driven by the need to enhance the operational capacities of defense forces. With the increasing complexity of modern warfare, there is a growing requirement for advanced communication systems to facilitate joint operations. These systems enable real-time data exchange between military units, improving situational awareness and enabling faster decision-making. The defense sector is also investing in next-generation vehicles, which are equipped with advanced electronic systems.

These systems include artificial intelligence, autonomous driving technologies, and sensors, among others. The integration of these technologies enhances the agility and threat response capabilities of defense forces. Asymmetric warfare approaches and hybrid defense technologies have also led to an increased focus on self-protection systems. Vehicle protection systems, including electronic warfare systems and countermeasure systems, are becoming essential components of vetronics architecture. The market is also witnessing significant investments in procurement and modernization programs. Defense contractors are collaborating with Original Equipment Manufacturers (OEMs) to develop and integrate advanced electronic systems into military vehicles. These systems include line-fit and retro-fit solutions for various types of armored vehicles, such as battle tanks, light protected vehicles, and armored personnel carriers.

The integration of advanced electronic systems in military vehicles is also leading to the development of digital hubs and mobility systems. These systems enable inter-vehicle communication, intra-vehicle communication, and wireless communications technology, enhancing the overall operational efficiency of defense forces. The market is also witnessing the emergence of unmanned vehicles, including unmanned ground vehicles and unmanned aerial vehicles. These vehicles are used for surveillance and reconnaissance, border security, and homeland security applications. The integration of advanced electronic systems In these vehicles enables real-time data collection and transmission, enhancing their operational capabilities. The market is also witnessing the adoption of cloud computing and cybersecurity technologies to enhance the security of communication systems and vehicle health management systems.

The threat of cyber attacks on military vehicles and communication systems is a significant concern, and the integration of secure communications systems and sensors is essential to mitigate these risks. In conclusion, the market is witnessing significant growth due to the increasing demand for advanced electronic systems in military vehicles and naval vessels. The integration of these systems enhances the operational capacities of defense forces, enabling faster decision-making, improved situational awareness, and enhanced threat response capabilities. The market is also witnessing the emergence of new technologies, such as autonomous driving and cloud computing, which are transforming the way defense forces operate.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

143 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 1126.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Key countries |

US, Russia, China, France, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Vetronics Market Research and Growth Report?

- CAGR of the Vetronics industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the vetronics market growth of industry companies

We can help! Our analysts can customize this vetronics market research report to meet your requirements.

RIA -

RIA -