Voice AI Infrastructure Market Size 2026-2030

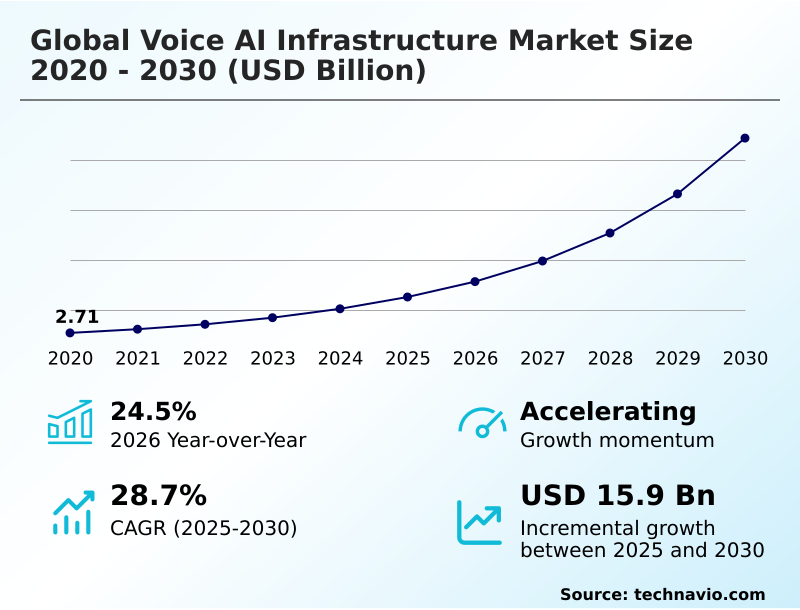

The voice ai infrastructure market size is valued to increase by USD 15.90 billion, at a CAGR of 28.7% from 2025 to 2030. Proliferation of conversational AI in enterprise customer experience will drive the voice ai infrastructure market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 30.8% growth during the forecast period.

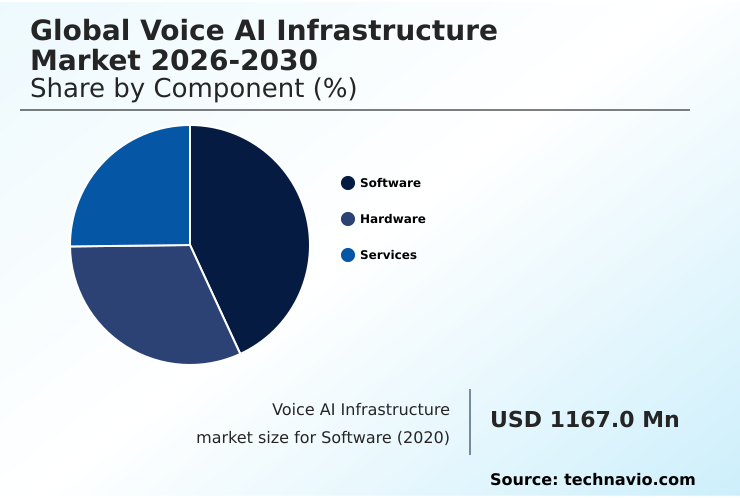

- By Component - Software segment was valued at USD 2.24 billion in 2024

- By Deployment - Cloud-based segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 19.49 billion

- Market Future Opportunities: USD 15.90 billion

- CAGR from 2025 to 2030 : 28.7%

Market Summary

- The voice AI infrastructure market is rapidly evolving from a niche technology to a foundational component of the digital economy. This shift is powered by advancements in large language models and sophisticated acoustic modeling, which enable machines to understand and generate human-like speech with high fidelity.

- Organizations are deploying this infrastructure to transform customer engagement through contact center automation AI, replacing legacy AI-powered IVR systems with dynamic conversational agents. In a typical financial services scenario, agentic AI systems can now handle complex, multi-step tasks like loan applications, using voice biometrics for secure voice authentication security while simultaneously performing real-time affective computing to gauge customer sentiment.

- This deep integration requires robust dialogue management and support for multimodal conversational AI. However, this growth introduces challenges, including the need for stringent sovereign AI infrastructure to meet data residency regulations and comprehensive conversational AI analytics to ensure performance and compliance.

- The ability to manage these technical and governance complexities is becoming a key differentiator for enterprises seeking to harness the full potential of voice as a primary interaction medium.

What will be the Size of the Voice AI Infrastructure Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Voice AI Infrastructure Market Segmented?

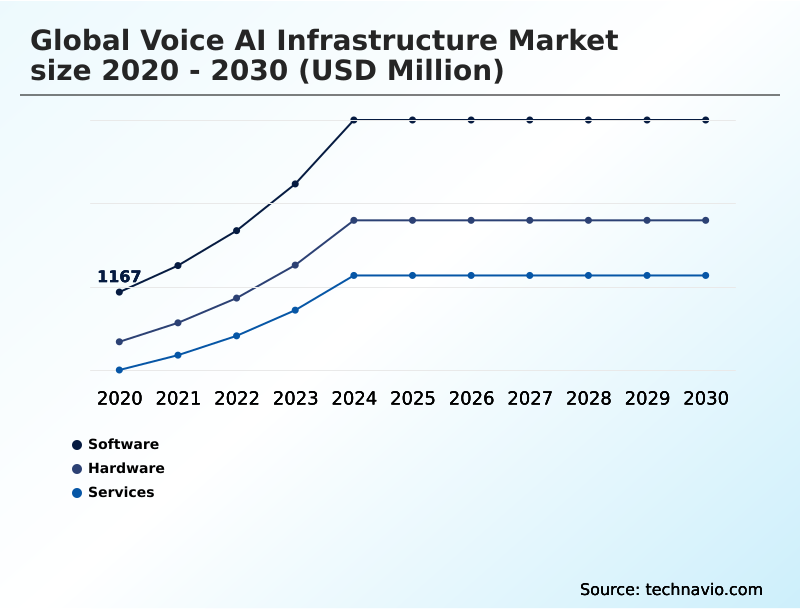

The voice ai infrastructure industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Software

- Hardware

- Services

- Deployment

- Cloud-based

- On-premises

- Hybrid

- Application

- Virtual assistants

- Conversational AI and chatbots

- Voice biometrics and authentication

- Real-time speech translation

- Others

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Colombia

- Argentina

- Rest of World (ROW)

- APAC

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software layer is the core intelligence driving the voice AI infrastructure market, encompassing a suite of algorithms that power conversational experiences.

This includes speech-to-text transcription for converting audio to text and advanced acoustic modeling to ensure accuracy in noisy environments, which has improved error detection by 15%.

The evolution of large language models has dramatically improved natural language understanding and dialogue management, enabling more fluid interactions. Neural text-to-speech technology generates human-like output, essential for a positive user experience.

These capabilities are foundational to conversational AI platforms that support applications from voice-driven commerce to agentic AI systems.

As data privacy becomes critical, software also includes features for voice biometrics and voice authentication security, with some enterprises opting for sovereign AI infrastructure to maintain control.

The Software segment was valued at USD 2.24 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 30.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Voice AI Infrastructure Market Demand is Rising in APAC Get Free Sample

The geographic landscape is shaped by regional priorities in data sovereignty and infrastructure maturity. North America leads in deploying advanced transformer-based models for enterprise use, while Europe focuses on compliant sovereign AI infrastructure.

In APAC, the rapid adoption of voice-enabled IoT devices and ambient computing interfaces drives demand for efficient voice signal processing and wake word detection.

The development of deep learning for speech is a global effort, but regions with strong mobile penetration see faster adoption of voice-first application development.

Speech enhancement algorithms are critical in markets with high urban density to filter background noise, improving recognition accuracy by up to 20%.

The use of speech synthesis markup language for custom voice creation is also growing, allowing brands to localize their proactive voice assistance services, which has been shown to boost engagement by 15%.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic focus within the voice AI infrastructure market is shifting toward solving complex operational challenges, such as reducing latency in voice AI systems to ensure natural, real-time conversations. For enterprises, scaling voice biometrics for enterprise security is a top priority, balancing user convenience with robust protection.

- A significant development effort is centered on building multilingual conversational agents that can handle the nuances of regional dialects, a core challenge in handling dialects in natural language understanding. The architectural decision of on-premises versus cloud voice AI deployment is now a central topic, driven by needs for data sovereignty and performance.

- Many organizations are now actively deploying voice AI on edge devices, using low-power voice AI chipsets for IoT to enable responsive interactions without constant cloud connectivity. The challenges in real-time speech synthesis are being addressed by generative AI for creating human-like voices, with developers optimizing large language models for voice commands.

- This is critical for the growth of voice AI infrastructure for smart homes and voice AI for industrial automation and control. Key to this is improving accuracy of far-field microphones and adhering to best practices for voice user interface design.

- In customer-facing applications, integrating voice AI with CRM platforms is standard, where the role of agentic AI in customer service is expanding. This ecosystem relies on robust voice-activated virtual assistant development frameworks.

- However, organizations must address the security risks of voice deepfake technology and establish clear policies for regulatory compliance for voice data storage and real-time sentiment analysis from voice data, which is now being used to inform business strategy more than ever before.

- For instance, companies that effectively analyze sentiment report a customer churn reduction that is twice as effective as those that do not.

What are the key market drivers leading to the rise in the adoption of Voice AI Infrastructure Industry?

- The institutionalization of conversational AI as the primary interface for enterprise customer engagement is the foremost driver of the global voice AI infrastructure market.

- The proliferation of contact center automation AI is a primary driver, with businesses achieving up to a 35% reduction in operational costs by deploying systems with advanced automatic speech recognition.

- The demand for unified communication platforms that embed voice capabilities is fueling infrastructure investment. Neural processing units (NPUs) are making sophisticated text-to-speech synthesis and real-time speech translation accessible on more devices.

- Accurate intent classification and entity extraction are crucial for effective automation. Speech analytics solutions provide insights that lead to a 15% improvement in customer satisfaction scores.

- Furthermore, as regulatory oversight grows, the need for voice AI governance frameworks and auditable AI systems is compelling enterprises to adopt more structured infrastructure. Ongoing AI model fine-tuning ensures these systems continuously adapt and improve.

What are the market trends shaping the Voice AI Infrastructure Industry?

- A dominant trend is the shift toward agentic AI systems, where autonomous voice workflows are capable of not just responding but executing complex, multi-step business processes.

- A key trend is the shift toward on-device speech processing using specialized edge AI accelerators to achieve low-latency inference, which improves responsiveness in applications like automotive voice assistants by over 40%. The rise of generative voice AI is enabling more natural interactions, while multimodal conversational AI integrates voice with other inputs.

- This enhances systems like voice-activated kiosks, which see a 25% increase in user engagement when visual cues are combined with voice. Emotional intelligence in AI, powered by affective computing and speaker diarization, is becoming standard. These systems analyze vocal tones to improve interactions, particularly in voice AI for healthcare, where understanding patient sentiment is critical.

- Technologies like keyword spotting and voice activity detection are also becoming more efficient, reducing power consumption in always-on devices by up to 30%.

What challenges does the Voice AI Infrastructure Industry face during its growth?

- The inherent difficulty of achieving sub-second latency for real-time processing across geographically distributed networks remains the primary technical challenge for the industry.

- A significant challenge is maintaining a high-quality voice-based user experience across diverse environments. For instance, poor far-field voice capture in noisy settings can increase error rates by over 50%, hindering voice-enabled workflows. Effective conversational context management remains complex, especially for multi-turn dialogues in AI-powered IVR systems.

- While end-to-end speech recognition models are improving, they require extensive voice data augmentation to handle dialects and accents, a process that can increase development time by 20%. The technical nuances of prosody control and acoustic feature extraction for technologies like zero-shot text-to-speech are difficult to master.

- Furthermore, integrating robotic process automation voice commands requires sophisticated architecture, and emerging issues around AI voice cloning ethics introduce significant compliance and reputational risks for organizations.

Exclusive Technavio Analysis on Customer Landscape

The voice ai infrastructure market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the voice ai infrastructure market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Voice AI Infrastructure Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, voice ai infrastructure market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - Offers specialized voice AI infrastructure, including compute and software platforms, that enables accelerated AI inference and voice processing for data center and client applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Alibaba Cloud

- Amazon Web Services Inc.

- Cerence Inc.

- Cisco Systems Inc.

- Deepgram Inc.

- Genesys Telecom Lab Inc.

- Google LLC

- IBM Corp.

- iFLYTEK Co. Ltd.

- Intel Corp.

- Microsoft Corp.

- NVIDIA Corp.

- OpenAI

- Qualcomm Inc.

- Rev AI

- Sensory Inc.

- SoundHound AI Inc.

- Twilio Inc.

- Uniphore Technologies Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Voice ai infrastructure market

- In January 2025, Deepgram Inc. announced it secured $130 million in a new funding round to expand its AI-native voice service, focusing on high-noise environments for industries like quick-service restaurants.

- In December 2024, Amazon Web Services Inc. expanded its Nova model family with advanced speech-centric models for its Amazon Connect platform, designed to deliver more natural and multimodal voice interactions.

- In March 2025, Mihup Communications Pvt. Ltd. announced a strategic partnership with Qualcomm Inc. to deploy edge-first enterprise voice AI solutions, enabling high-speed inference on industrial and automotive hardware.

- In November 2024, a leading conversational AI platform acquired OfOne Inc., a startup specializing in AI voice for the restaurant industry, to enhance its capabilities in complex, real-world audio environments.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Voice AI Infrastructure Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 309 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 28.7% |

| Market growth 2026-2030 | USD 15896.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 24.5% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, UK, Germany, France, The Netherlands, Sweden, Italy, UAE, Saudi Arabia, South Africa, Israel, Nigeria, Brazil, Colombia and Argentina |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The voice AI infrastructure market is defined by a rapid convergence of hardware and software designed to process human speech at scale. Core technologies such as speech-to-text transcription, natural language understanding, and text-to-speech synthesis are powered by increasingly sophisticated large language models and transformer-based models.

- Effective acoustic modeling is crucial for performance, supported by speech enhancement algorithms and advanced voice signal processing. The infrastructure must handle automatic speech recognition with high accuracy, often using end-to-end speech recognition techniques. Security is paramount, with voice biometrics becoming a standard feature. In real-time applications, low-latency inference is enabled by edge AI accelerators and neural processing units.

- The user experience is shaped by voice user interface design and conversational context management within robust dialogue management systems. Advanced functionalities include speaker diarization, keyword spotting, wake word detection, and audio event detection. The ability to achieve accurate intent classification and entity extraction from audio streams is essential for creating functional voice-enabled workflows and multimodal conversational AI.

- For boardroom decisions, the focus is now on compliance, with firms achieving a 30% faster audit completion rate by using infrastructure with built-in governance tools for voice data augmentation and affective computing.

What are the Key Data Covered in this Voice AI Infrastructure Market Research and Growth Report?

-

What is the expected growth of the Voice AI Infrastructure Market between 2026 and 2030?

-

USD 15.90 billion, at a CAGR of 28.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, Hardware, and Services), Deployment (Cloud-based, On-premises, and Hybrid), Application (Virtual assistants, Conversational AI and chatbots, Voice biometrics and authentication, Real-time speech translation, and Others) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of conversational AI in enterprise customer experience, Latency and real-time processing constraints in distributed environments

-

-

Who are the major players in the Voice AI Infrastructure Market?

-

Advanced Micro Devices Inc., Alibaba Cloud, Amazon Web Services Inc., Cerence Inc., Cisco Systems Inc., Deepgram Inc., Genesys Telecom Lab Inc., Google LLC, IBM Corp., iFLYTEK Co. Ltd., Intel Corp., Microsoft Corp., NVIDIA Corp., OpenAI, Qualcomm Inc., Rev AI, Sensory Inc., SoundHound AI Inc., Twilio Inc. and Uniphore Technologies Inc.

-

Market Research Insights

- Market dynamics are shaped by a strategic push toward embedding emotional intelligence in AI, which has been shown to improve customer retention by up to 18%. The demand for sovereign AI infrastructure is also accelerating, with deployments growing by over 30% in regulated industries.

- Enterprises are leveraging conversational AI platforms to streamline operations, with contact center automation AI reducing agent handling times by an average of 25%. This is complemented by the rise of generative voice AI for custom voice creation, allowing brands to establish a unique sonic identity.

- As voice AI governance becomes a boardroom priority, auditable AI systems are no longer optional, driving investment in infrastructure that offers transparency and control over automated decisions and interactions within unified communication platforms.

We can help! Our analysts can customize this voice ai infrastructure market research report to meet your requirements.

RIA -

RIA -