Aerospace Adhesive and Sealants Market Size 2024-2028

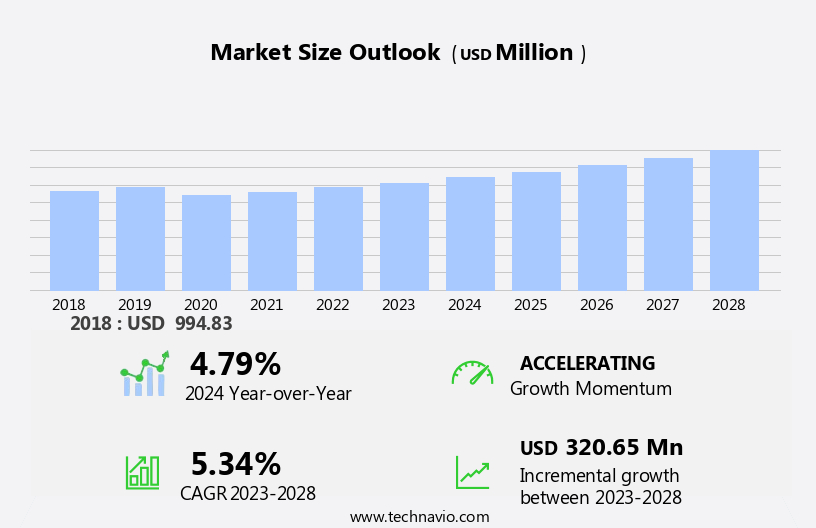

The aerospace adhesive and sealants market size is forecast to increase by USD 320.65 billion at a CAGR of 5.34% between 2023 and 2028.

- The market is experiencing significant growth due to several key factors. The increasing number of air passengers worldwide is driving the demand for new aircraft and the need for maintenance and repairs, thereby boosting the market. Silicones, polyurethanes, polysulfides, acrylics, cyanoacrylates, hot melts, reactive, solvent-borne, UV-cured, and water-borne adhesives are some of the commonly used materials in this industry. Additionally, investments in increasing adhesive production are on the rise to meet the growing demand from the aerospace industry. However, stringent regulatory standards associated with adhesives and sealants pose a challenge to market growth. These regulations ensure the safety and reliability of aircraft components, but they also increase production costs and complexity. To stay competitive, market players are focusing on innovation and technology to meet these regulations while maintaining cost-effectiveness and quality.

What will be the Size of the Market During the Forecast Period?

- The aerospace industry is a critical sector that demands high-performance materials to ensure the safety, reliability, and efficiency of aircraft. Adhesives and sealants play a pivotal role in this industry, providing solutions for bonding various components, sealing gaps, and enhancing the overall performance of aircraft. This article explores the market trends and growth dynamics of aerospace adhesives and sealants, focusing on key industry segments and applications. The aerospace adhesives and sealants market is driven by several factors. The increasing demand for lighter weight aircraft assemblies is one of the primary growth drivers.

- These materials help reduce the overall weight of aircraft, leading to improved fuel efficiency and reduced emissions. Composite materials, which are extensively used in aircraft manufacturing, require specialized adhesives and sealants for bonding and sealing. Another significant trend in the aerospace industry is the use of multifunctional surfacing materials. These materials offer both adhesive and protective coatings, reducing the number of components required and simplifying the manufacturing process. The defense sector is a major consumer of aerospace adhesives and sealants due to the high-performance requirements of military aircraft.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Technology

- Water-based

- Solvent-based

- Others

- End-user

- Commercial

- Military

- General aviation

- Geography

- North America

- US

- APAC

- China

- India

- Europe

- Germany

- UK

- South America

- Middle East and Africa

- North America

By Technology Insights

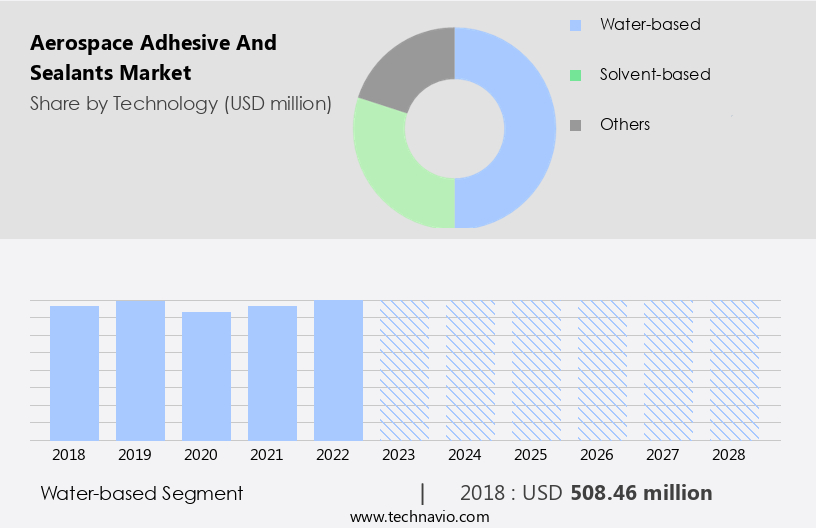

- The water-based segment is estimated to witness significant growth during the forecast period.

Water-based technology in aerospace adhesives and sealants is an eco-friendly solution for addressing bonding and sealing needs in the aviation industry. Unlike traditional solvent-based alternatives, water is used as the primary solvent or carrier for these formulations. This approach is advantageous due to its environmentally conscious nature, making it a preferred choice in applications where emissions need to be minimized. Water-based adhesives and sealants are commonly used in aerospace manufacturing processes, such as bonding and sealing aircraft components, where reducing hazardous air pollutants is essential. These adhesives consist of an organic binder, typically polyvinyl acetate (PVAc), finely dispersed in water.

Furthermore, Two other types of adhesives widely used in the aerospace sector are hot melt adhesives and pressure sensitive adhesives. Hot melt adhesives are applied in a molten state and solidify upon cooling, while pressure sensitive adhesives adhere to surfaces upon application of pressure. Both types have their unique applications in the aerospace industry. Hot melt adhesives are suitable for high-temperature applications, such as bonding engine components and insulation materials. Pressure sensitive adhesives, on the other hand, are ideal for bonding and sealing various aircraft components, such as windows, doors, and interior panels. Manufacturers of aerospace adhesives and sealants include major players such as 3M, Henkel, H.B.

Get a glance at the market report of share of various segments Request Free Sample

The Water-based segment was valued at USD 508.46 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

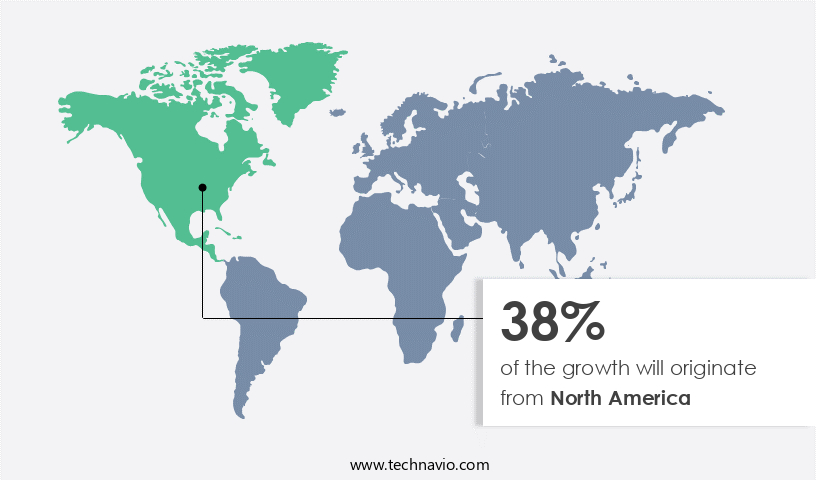

- North America is estimated to contribute 38% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In North America, the market holds significant importance, fueling advancements, production, and demand for superior materials within the aerospace sector. The United States, a key region in this market, is home to prominent aerospace companies such as Boeing and Lockheed Martin. These industry leaders, based in Seattle, Washington, and southern California, are at the forefront of aircraft manufacturing and research and development. The region's thriving aerospace industry is underpinned by the presence of these players and a strong defense sector. Lightweight aircraft assemblies, control systems, nacelle systems, fuselages, and engine parts all rely on high-performance adhesives and sealants for optimal functionality.

The continuous demand for advanced technology and innovation in aerospace applications ensures the market's growth in North America.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Aerospace Adhesive and Sealants Market?

The rise in number of air passengers globally is the key driver of the market.

- The aerospace adhesives and sealants market is witnessing significant growth due to the increasing demand for new aircraft and the expanding MRO business in the US aviation industry. With the rise of low-cost airlines and the growing trend towards decarbonization, there is a heightened focus on producing lightweight aircraft assemblies. This has led to the increased use of advanced materials, such as composite materials in aircraft manufacturing. Aerospace adhesives and sealants play a crucial role in the production and maintenance of various aircraft components, including control systems, nacelle systems, fuselages, engine parts, sandwich panels, and edge bonding. These materials ensure the structural integrity of these components by providing bonding and sealing functions, as well as enhancing their chemical resistance and tensile strength..

- The market for aerospace adhesives and sealants is diverse, with various types of adhesives such as silicone, polyurethane, hot melt adhesives, pressure sensitive adhesives, solvent-borne, and UV cured adhesives, among others, being used. Similarly, sealants come in various forms, including polysulfide, acrylic, cyanoacrylate, epoxy, and reactive sealants. Tier I suppliers and systems integrators are the primary consumers of aerospace adhesives and sealants. The OEM and MRO sectors are the largest markets for these materials, with the MRO business experiencing significant growth due to the increasing demand for aircraft aftermarket services. Fuel costs and the need for fuel efficiency are also driving the demand for lightweight and efficient adhesives and sealants.

What are the market trends shaping the Aerospace Adhesive and Sealants Market?

Increasing investments for boosting adhesive production is the upcoming trend in the market.

- The aerospace adhesives and sealants market is experiencing significant growth due to the increasing demand for lightweight aircraft assemblies in the aviation industry. Aircraft manufacturers and MRO (Maintenance, Repair, and Overhaul) businesses are investing in advanced adhesive technologies to enhance the performance and durability of various aircraft components. This state-of-the-art plant, named Kunpeng, will boost Henkel's production capacity for high-performance adhesive products, including silicone, polyurethane, hot melt adhesives, pressure-sensitive adhesives, and reactive adhesives. The new facility will also optimize Henkel's supply network, enabling the company to efficiently serve both domestic and international markets.

- The growing demand for these adhesive solutions is driven by the need for chemical resistance, lightweight structures, and cost efficiency in aircraft manufacturing. Key applications include control systems, nacelle systems, fuselages, engine parts, sandwich panels, edge bonding, and void filling in honeycomb structures. Moreover, the increasing popularity of low-cost airlines and the rise of leisure tourism have fueled the demand for more fuel-efficient aircraft, further emphasizing the importance of lightweight and strong adhesive solutions. The MRO business in the aircraft aftermarket is also a significant contributor to the growth of the aerospace adhesives and sealants market. Tier I suppliers and systems integrators are increasingly relying on these advanced materials to improve the tensile strength of mechanical fasteners, such as screws and weld joints, and to reduce fuel costs through decarbonization efforts.

What challenges does Aerospace Adhesive and Sealants Market face during the growth?

Stringent regulatory standards associated with adhesives and sealants is a key challenge affecting the market growth.

- In the aerospace industry, adherence to stringent regulatory standards is a critical factor in The market. The FAA, among other international aviation authorities, sets and enforces regulations for materials used in aircraft construction and maintenance, including adhesives and sealants. Compliance with these regulations is essential for manufacturers to secure airworthiness certifications for their products. Adhesives and sealants play a crucial role in the aerospace sector, with applications ranging from control systems and nacelle systems to fuselages, engine parts, and sandwich panels. Materials such as silicone, polyurethane, hot melt adhesives, pressure sensitive adhesives, polysulfide, acrylic, cyanoacrylate, epoxy, hot melt, reactive, sealants, solvent-borne, and UV cured adhesives are commonly used in the industry.

- The aerospace market consists of Original Equipment Manufacturers (OEM) and Maintenance, Repair, and Overhaul (MRO) businesses. Tier I suppliers and systems integrators also play a significant role in the value chain. Lightweight aircraft assemblies, control systems, and fuel costs are driving market growth. Decarbonization and leisure tourism are also contributing factors. Key challenges in the market include the need for chemical resistance, low cost, and high tensile strength. Manufacturers must balance these requirements with the need for lightweight materials to reduce fuel costs and meet decarbonization goals. Mechanical fasteners, such as screws and weld joints, are also used in aircraft assembly but are being replaced by adhesives and sealants to reduce weight and improve performance.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast , partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- Akzo Nobel NV

- Antala S.L.

- Beacon Adhesives Inc.

- Bostik Ltd.

- Dow Chemical Co.

- Dymax Corp.

- Henkel AG and Co. KGaA

- Hernon Manufacturing Inc.

- Hexcel Corp.

- Holcim Ltd.

- Huntsman International LLC

- L and L Products Inc.

- Lanxess AG

- Master Bond Inc.

- Permabond LLC

- PPG Industries Inc.

- Sika AG

- Solvay SA

- Vitrochem Technology

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is experiencing significant growth due to the increasing demand for aircraft production and maintenance, repair, and overhaul (MRO) activities. The market is driven by several factors, including the rise of low-cost airlines, the introduction of newer aircraft models, and the increasing use of composite materials in aircraft manufacturing. Chemical resistance is a crucial factor in the selection of adhesives and sealants for the aerospace industry. Adhesives and sealants used in aircraft applications must be able to withstand extreme temperatures, high pressures, and harsh environmental conditions.

Silicone and polyurethane are popular choices due to their excellent chemical resistance and high performance in extreme conditions. Hot melt adhesives and pressure-sensitive adhesives (PSAs) are widely used in the aerospace industry for various applications, including control systems, nacelle systems, fuselages, engine parts, and sandwich panels. These adhesives offer several advantages, such as high bonding strength, fast curing time, and ease of application. Solvent-borne and water-borne technologies are commonly used in the production of aerospace adhesives and sealants. Solvent-borne adhesives offer high bonding strength and excellent chemical resistance, but they have environmental concerns due to their high volatile organic compound (VOC) content.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

182 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.34% |

|

Market Growth 2024-2028 |

USD 320.65 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.79 |

|

Key countries |

US, China, India, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -