AI In Supercomputer Market Size 2025-2029

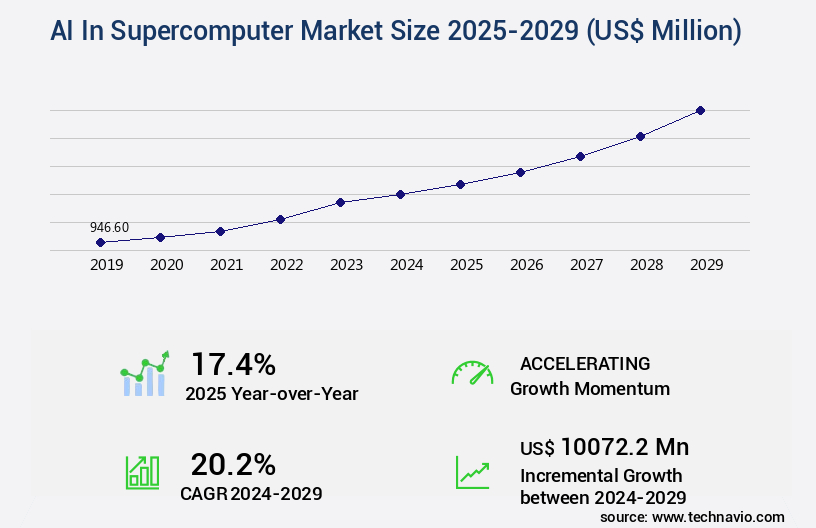

The AI in supercomputer market size is valued to increase by USD 10.07 billion, at a CAGR of 20.2% from 2024 to 2029. Rising demand for high-performance AI workloads will drive the ai in supercomputer market.

Major Market Trends & Insights

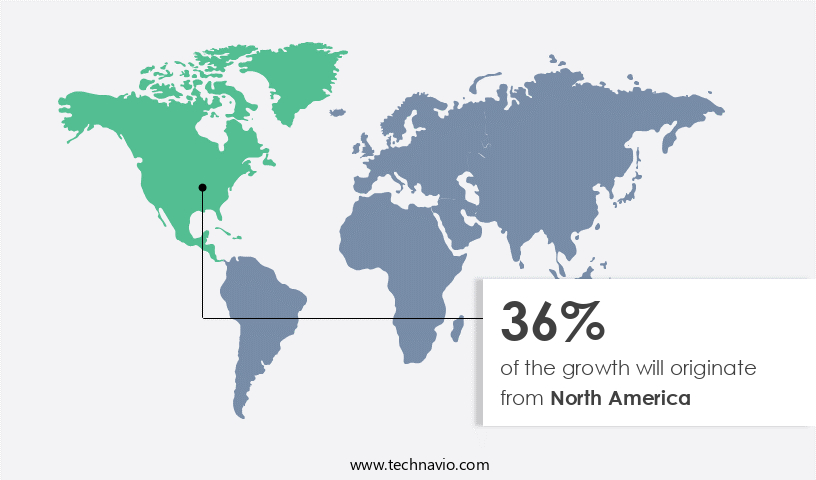

- North America dominated the market and accounted for a 36% growth during the forecast period.

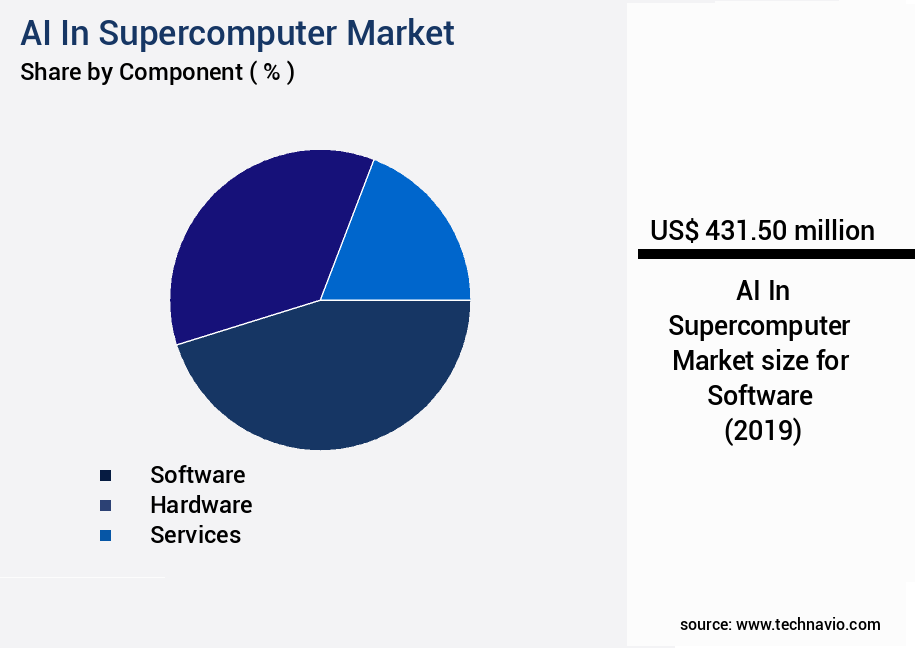

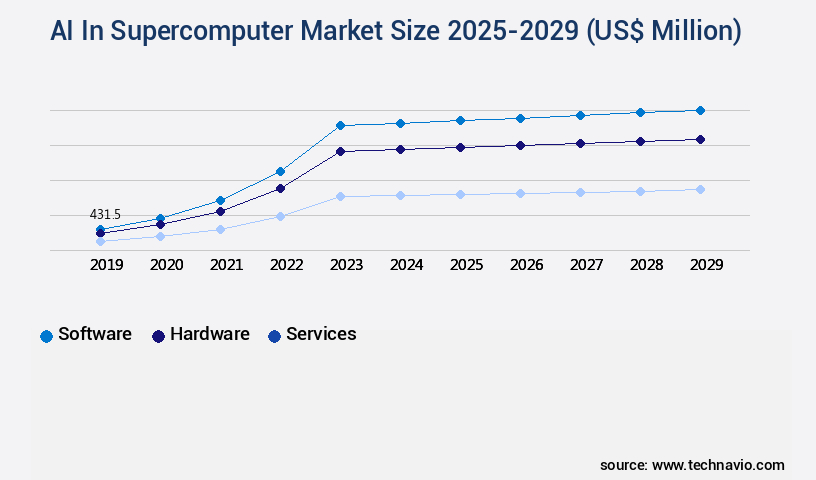

- By Component - Software segment was valued at USD 431.50 billion in 2023

- By Deployment - Cloud-based segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.00 million

- Market Future Opportunities: USD 10072.20 million

- CAGR from 2024 to 2029 : 20.2%

Market Summary

- In the dynamic realm of technology, the market is experiencing significant growth, driven by the escalating demand for high-performance artificial intelligence (AI) workloads. Supercomputers, once relegated to number-crunching tasks, are now being specialized for targeted AI applications, leading to a convergence of these two domains. However, this evolution comes with substantial capital and operational costs, posing challenges for businesses. Quantum computing and algorithm optimization, encryption techniques, natural language processing, data visualization tools, simulation software, and AI algorithms are increasingly integrated into the AI supercomputing landscape. This growth is fueled by the increasing need for advanced AI capabilities in various industries, from scientific research to finance and healthcare.

- By integrating AI into supercomputers, organizations can process vast amounts of data more efficiently and accurately, unlocking new insights and opportunities. Despite these advantages, the high costs associated with AI supercomputers remain a significant barrier to entry for many businesses. These costs include the price of the hardware itself, as well as the ongoing operational expenses, such as cooling and power requirements. Nevertheless, the potential benefits of AI supercomputing are compelling, making it an area of active research and development. In conclusion, the market is poised for continued growth, as businesses seek to harness the power of AI for their most demanding applications.

- While the costs remain a challenge, the potential rewards are significant, making this an exciting and dynamic area of technological innovation.

What will be the Size of the AI In Supercomputer Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI In Supercomputer Market Segmented ?

The AI in supercomputer industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Software

- Hardware

- Services

- Deployment

- Cloud-based

- On-premises

- Hybrid

- End-user

- Healthcare

- Financial services

- Manufacturing

- Retail

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

In the dynamic realm of AI supercomputing, the market is witnessing a significant shift from conventional high-performance computing (HPC) tools to specialized AI frameworks and orchestration platforms. This transformation encompasses deep learning libraries, model training environments, and workload schedulers designed to optimally utilize heterogeneous hardware. The software layer plays a pivotal role in translating raw compute power into valuable intelligence. Modern AI supercomputing software stacks are increasingly containerized and cloud-native, ensuring scalability and portability. Integration with popular frameworks like TensorFlow, PyTorch, and ONNX is now standard practice, while orchestration tools such as Kubernetes and Slurm are being tailored for AI-specific workloads.

The merging of AI and simulation software is fueling growth in sectors like climate science and genomics through hybrid modeling approaches. Moreover, energy efficiency optimization is a key focus area, with neural network architecture, error correction codes, and cooling systems playing essential roles. Model deployment strategies, security protocols, fault tolerance mechanisms, data storage solutions, and data center infrastructure are also undergoing continuous evolution. According to recent studies, the global AI supercomputing market is projected to reach a value of USD150 billion by 2027, growing at a CAGR of 28.1% during the forecast period.

This underscores the immense potential and ongoing innovation in this field.

The Software segment was valued at USD 431.50 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Supercomputer Market Demand is Rising in North America Request Free Sample

North America's AI supercomputing market maintains a leading position, fueled by a robust ecosystem of tech giants, research institutions, and government initiatives. Notable systems, such as IBM Summit and Sierra, based in the region, integrate deep learning and neural networks for AI-driven simulations in healthcare, energy, climate science, and defense. In October 2024, these IBM supercomputers continued to innovate, significantly impacting cancer research and climate modeling.

The US Department of Energy is a key player, funding new AI supercomputing projects, including a flagship system at Lawrence Berkeley National Laboratory, scheduled for deployment in 2026, in collaboration with NVIDIA and Dell. This new system will further advance scientific discovery and data analytics optimization.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to the increasing demand for high-performance computing (HPC) systems to optimize deep learning model training on GPUs and support advanced AI applications. However, node failures in supercomputers can significantly impact performance, necessitating effective strategies for improving fault tolerance. Parallel programming paradigms, such as Message Passing Interface (MPI) and Open Multi-Processing (OpenMP), offer solutions for optimizing computation across multiple processors. Effective data center cooling strategies and reducing power consumption in supercomputing systems are also crucial for managing operational costs. Advanced techniques for data compression in HPC, such as lossless and lossy compression, play a vital role in managing data storage in large-scale supercomputing systems. Implementing security protocols in cloud-based supercomputers is essential for safeguarding sensitive data and ensuring privacy. Benchmarking AI algorithms for supercomputer applications is crucial for evaluating their performance and efficiency. Strategies for model deployment in a high-performance computing environment, such as containerization and virtualization, optimize resource utilization.

Evaluating the energy efficiency of various supercomputer architectures is a critical consideration for reducing carbon footprint and minimizing operational costs. Managing data storage in large-scale supercomputing systems requires advanced techniques for data visualization and analytics. Virtualization plays a significant role in optimizing supercomputer resource utilization, enabling efficient remote management of systems. Performance analysis of different database management systems is necessary for ensuring optimal data access and retrieval. Development and deployment of AI-powered supercomputer simulations offer new opportunities for scientific research and innovation. Network latency and enhancing bandwidth in supercomputer networks are essential for enabling seamless communication between nodes and applications. Techniques for improving the reliability of supercomputer systems, such as redundancy and error correction, are crucial for ensuring uptime and minimizing downtime. Overall, The market offers significant opportunities for innovation and growth, driven by the increasing demand for high-performance computing and AI applications.

What are the key market drivers leading to the rise in the adoption of AI In Supercomputer Industry?

- The surge in demand for advanced artificial intelligence (AI) workloads serves as the primary market catalyst.

- The market is experiencing a significant surge due to the escalating demand for high-performance computing (HPC) capabilities to support increasingly complex AI workloads. Traditional computing systems are no longer sufficient as AI applications evolve from basic automation to advanced generative models and real-time decision-making systems. AI supercomputers, equipped with thousands of parallel processors and optimized memory architectures, are uniquely designed to meet these demands. In sectors such as healthcare, climate science, and materials engineering, AI supercomputers are enabling breakthroughs that were previously unattainable.

- For instance, in drug discovery, these systems can simulate molecular interactions at scale, drastically reducing the time and resources required to identify viable compounds. The computational power of AI supercomputers is revolutionizing industries, making them indispensable tools for innovation and progress.

What are the market trends shaping the AI In Supercomputer Industry?

- The specialization of artificial intelligence supercomputers for targeted applications is an emerging market trend. This focus on specific applications enhances the efficiency and effectiveness of AI technology.

- The AI supercomputer market is experiencing a significant evolution, moving towards specialized systems designed for specific AI workloads and industry applications. In contrast to general-purpose supercomputers, which cater to a broad range of computational tasks, specialized AI supercomputers are optimized for particular domains such as natural language processing (NLP), computer vision, autonomous systems, or scientific simulations. This shift is fueled by the understanding that various AI models possess unique computational requirements.

- For instance, NLP models, including large language models (LLMs), demand high memory bandwidth and efficient handling of sparse data structures. The benefits of this trend include enhanced performance and efficiency gains, making it a crucial development in the AI landscape.

What challenges does the AI In Supercomputer Industry face during its growth?

- The high capital and operational costs represent a significant challenge to the growth of the industry. In order to mitigate this issue, companies must carefully manage expenses, seek cost-effective solutions, and potentially explore opportunities for external funding or partnerships.

- The market is characterized by its resource-intensive nature, necessitating substantial investments in specialized hardware and infrastructure. AI supercomputers demand high-end GPUs, TPUs, or custom AI accelerators, along with advanced cooling systems, high-speed networking components, and substantial energy supplies. These requirements result in significant capital expenditures, often reaching hundreds of millions of dollars for a single installation. Operational costs are equally substantial due to the enormous electricity consumption required to power the processors and maintain optimal thermal conditions. Despite these challenges, the adoption of AI supercomputers is expanding across various sectors, including finance, healthcare, and research, driven by their ability to process complex data and deliver advanced insights.

- The integration of AI in supercomputing is revolutionizing industries by enabling more accurate predictions, faster simulations, and improved decision-making capabilities.

Exclusive Technavio Analysis on Customer Landscape

The ai in supercomputer market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in supercomputer market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Supercomputer Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in supercomputer market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - This company specializes in providing advanced GPUs optimized for artificial intelligence applications, posing a formidable challenge to NVIDIA in data centers and high-performance computing environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Alibaba Cloud

- Amazon Web Services Inc.

- Apple Inc.

- Axelera AI B.V.

- Cerebras

- Google LLC

- Graphcore Ltd.

- Groq Inc.

- Hewlett Packard Enterprise Co.

- Huawei Technologies Co. Ltd.

- Intel Corp.

- International Business Machines Corp.

- Meta Platforms Inc.

- Microsoft Corp.

- NVIDIA Corp.

- SambaNova Systems Inc.

- Tenstorrent Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI In Supercomputer Market

- In January 2024, IBM announced the launch of its new AI-powered supercomputer, "Odyssey," designed to accelerate scientific research and discovery. Odyssey, which ranks among the world's top 10 supercomputers, integrates IBM's AI technology, Power10 processors, and NVIDIA GPUs (IBM Press Release, 2024).

- In March 2024, Fujitsu and Microsoft signed a strategic partnership to develop AI solutions for supercomputing applications. The collaboration aims to integrate Microsoft Azure AI services with Fujitsu's PRIMEHPC supercomputers, targeting industries such as finance, manufacturing, and life sciences (Microsoft News Center, 2024).

- In May 2024, Google announced a USD1 billion investment in its supercomputing division, Google AI, to expand its capabilities in AI research and development. The investment will focus on improving machine learning algorithms, enhancing hardware infrastructure, and expanding partnerships with leading research institutions (Google Blog, 2024).

- In April 2025, the European Union approved the European High-Performance Computing Joint Undertaking (EuroHPC), a €1 billion initiative to build a European supercomputing infrastructure. The initiative will include AI-powered supercomputers, aiming to boost Europe's competitiveness in technology and innovation (European Commission Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Supercomputer Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

245 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 20.2% |

|

Market growth 2025-2029 |

USD 10072.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

17.4 |

|

Key countries |

US, China, Japan, Germany, Canada, UK, India, France, South Korea, and Mexico |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The supercomputer market continues to evolve, driven by advancements in artificial intelligence (AI) technologies. Neural network architecture and deep learning models are at the forefront of this evolution, with energy efficiency optimization becoming a critical factor in their implementation. Error correction codes and cooling systems are essential components in the model training process, ensuring accuracy and reliability. Model deployment strategies and security protocols are also crucial, as AI algorithms and machine learning techniques are increasingly used in various sectors, from computer vision systems in manufacturing to natural language processing in finance. Data storage solutions and data center infrastructure must be able to handle the vast amounts of data generated by these systems, while minimizing network latency and ensuring fault tolerance mechanisms.

- Moreover, the ongoing development of quantum computing and algorithm optimization is poised to revolutionize high-performance computing, with power consumption metrics and cloud computing platforms playing a significant role in making these technologies accessible and cost-effective. Big data analytics and performance benchmarking are essential tools for optimizing AI systems, while GPU acceleration and parallel processing enable faster model training and deployment. According to recent industry reports, the global supercomputer market is expected to grow by over 10% annually, driven by the increasing adoption of AI and machine learning techniques across various industries. For instance, a leading automotive manufacturer recently reported a 25% increase in production efficiency by implementing AI-powered simulation software and machine learning techniques in their manufacturing processes.

- Despite these advancements, system maintenance, hardware upgrades, and data privacy remain significant challenges in the market. Encryption techniques and data visualization tools are essential for addressing these concerns, while performance benchmarking and bandwidth requirements continue to shape the development of new AI technologies. Overall, the supercomputer market remains a dynamic and evolving landscape, with ongoing innovation and development shaping its future.

What are the Key Data Covered in this AI In Supercomputer Market Research and Growth Report?

-

What is the expected growth of the AI In Supercomputer Market between 2025 and 2029?

-

USD 10.07 billion, at a CAGR of 20.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, Hardware, and Services), Deployment (Cloud-based, On-premises, and Hybrid), End-user (Healthcare, Financial services, Manufacturing, Retail, and Others), and Geography (North America, APAC, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Rising demand for high-performance AI workloads, High capital and operational costs

-

-

Who are the major players in the AI In Supercomputer Market?

-

Advanced Micro Devices Inc., Alibaba Cloud, Amazon Web Services Inc., Apple Inc., Axelera AI B.V., Cerebras, Google LLC, Graphcore Ltd., Groq Inc., Hewlett Packard Enterprise Co., Huawei Technologies Co. Ltd., Intel Corp., International Business Machines Corp., Meta Platforms Inc., Microsoft Corp., NVIDIA Corp., SambaNova Systems Inc., and Tenstorrent Inc.

-

Market Research Insights

- The market for AI in supercomputing is a dynamic and ever-evolving landscape. Supercomputers, with their immense processing power, are increasingly integrating AI technologies to enhance their capabilities. For instance, AI algorithms are being employed for system diagnostics, enabling faster identification and resolution of issues. Moreover, remote management tools are being augmented with AI to optimize resource utilization and improve efficiency. According to industry reports, the global supercomputing market is projected to grow by over 15% annually. This growth is driven by the increasing demand for high-performance computing in various sectors, including scientific research, finance, and manufacturing. An example of this trend is the significant sales increase experienced by a leading supercomputer manufacturer due to their AI-powered offerings.

- Furthermore, AI is revolutionizing interconnect technology, enabling faster data transfer and processing. Additionally, it is being used for bias detection, ensuring ethical considerations and model interpretability in AI models. Data compression and memory management are other areas where AI is making a significant impact. Despite these advancements, challenges remain, such as network security and regulatory compliance, which are being addressed through ongoing research and development.

We can help! Our analysts can customize this AI in supercomputer market research report to meet your requirements.

RIA -

RIA -