AI Sensor Integration Market Size 2026-2030

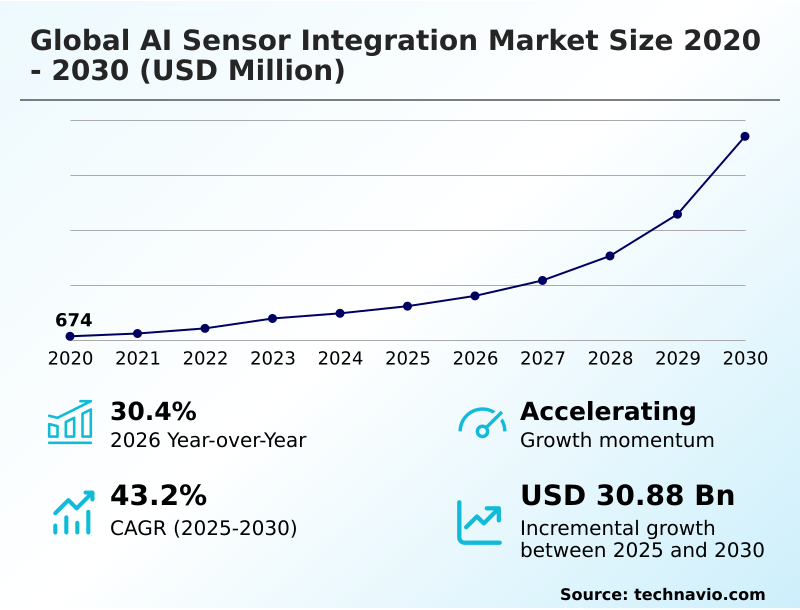

The ai sensor integration market size is valued to increase by USD 30.88 billion, at a CAGR of 43.2% from 2025 to 2030. Rapid advancement in edge computing and local processing capabilities will drive the ai sensor integration market.

Major Market Trends & Insights

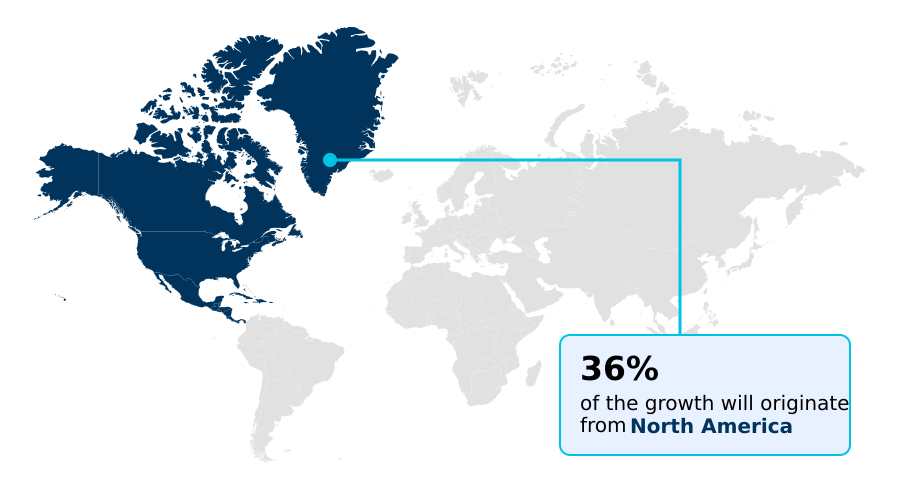

- North America dominated the market and accounted for a 36.1% growth during the forecast period.

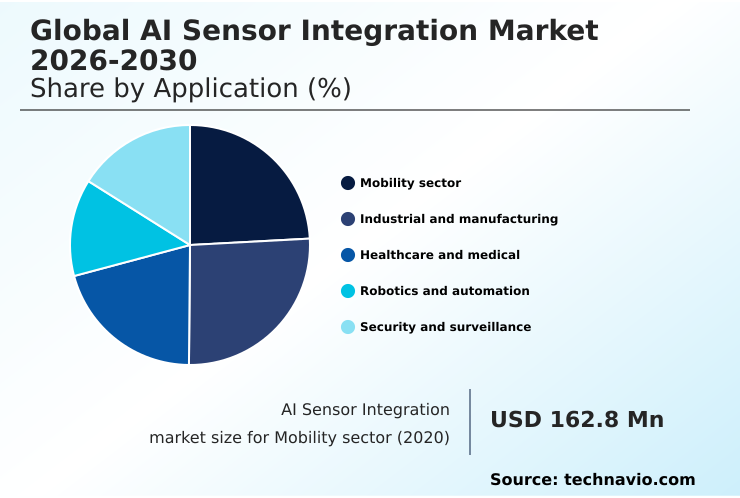

- By Application - Mobility sector segment was valued at USD 1.38 billion in 2024

- By Technology - Machine learning segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 36.36 billion

- Market Future Opportunities: USD 30.88 billion

- CAGR from 2025 to 2030 : 43.2%

Market Summary

- The AI Sensor Integration market is characterized by a rapid shift toward decentralizing intelligence, moving from cloud-based analysis to on-device AI processing. This transition is enabled by developments in system-on-chip architectures and embedded neural networks, which allow for real-time data interpretation directly at the source.

- Key drivers include the push for Industry 4.0 integration, where industrial automation sensors facilitate predictive maintenance systems, and the evolution of autonomous systems perception in mobility. A prominent business scenario involves a smart factory ecosystem where AI-driven thermal sensing and acoustic signature analysis on machinery can preemptively identify potential failures, reducing unplanned downtime by over 30%.

- However, the industry grapples with challenges like hardware-software harmonization and ensuring sensor data security across diverse applications. Trends such as multimodal sensor fusion and autocalibration algorithms are creating more robust and reliable intelligent sensing solutions, paving the way for sophisticated applications in healthcare, robotics, and smart city infrastructure. This convergence of advanced hardware and sophisticated software defines the competitive landscape.

What will be the Size of the AI Sensor Integration Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI Sensor Integration Market Segmented?

The ai sensor integration industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

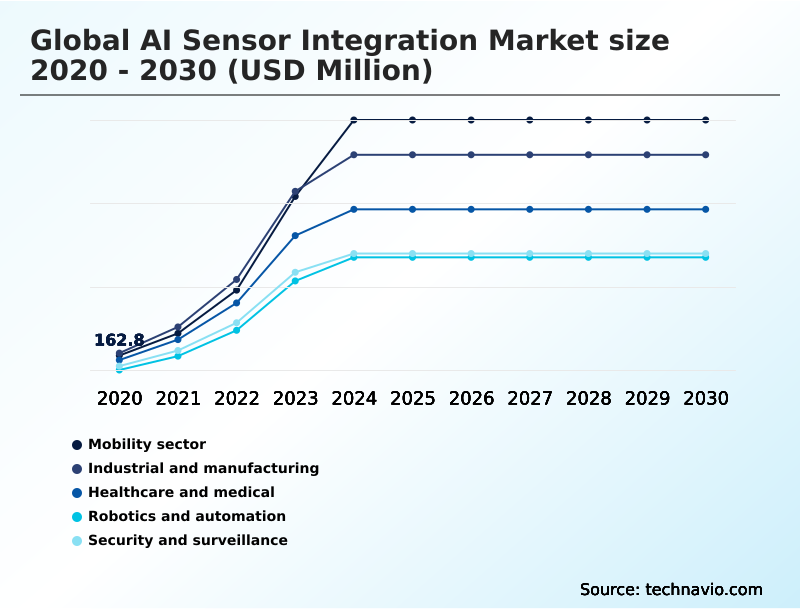

- Mobility sector

- Industrial and manufacturing

- Healthcare and medical

- Robotics and automation

- Security and surveillance

- Technology

- Machine learning

- Computer vision

- Deep learning

- Natural language processing

- Type

- Image sensors

- Radar sensors

- Ultrasonic sensors

- Lidar sensors

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- France

- UK

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Application Insights

The mobility sector segment is estimated to witness significant growth during the forecast period.

The mobility sector is undergoing a profound transformation, driven by the integration of intelligent sensing solutions into software-defined vehicles. This evolution prioritizes autonomous systems perception and advanced safety features, enabled by on-device AI processing and high-resolution sensor fusion.

The deployment of AI-native hardware in advanced driver-assistance systems (ADAS) is critical for achieving real-time path planning and reliable performance. Innovations in AI-driven thermal sensing and specialized AI microprocessors are enabling vehicles to interpret complex environments with high precision.

For instance, the use of deep learning models for sensors has improved object detection accuracy by over 40% in challenging weather conditions, establishing a new benchmark for industrial safety applications and autonomous navigation systems in the global AI sensor integration market 2026-2030.

The Mobility sector segment was valued at USD 1.38 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Sensor Integration Market Demand is Rising in North America Get Free Sample

The geographic landscape of the AI Sensor Integration market reflects distinct regional specializations.

North America leads in R&D and venture capital investment, contributing 36.1% of the market's incremental growth, with a strong focus on autonomous systems perception and AI-enhanced medical imaging.

The region's stringent regulatory compliance frameworks also drive innovation in explainable AI for sensors.

In contrast, APAC dominates global production, leveraging its vast electronics manufacturing base to embed low-power AI inference into consumer devices and industrial automation sensors, supporting a thriving smart factory ecosystem.

Europe distinguishes itself through its focus on Industry 4.0 integration and hardware-software harmonization, with an emphasis on lifecycle AI management and creating self-healing sensor networks that adhere to strict data privacy standards.

This global distribution fosters a competitive environment where regional strengths in technology, manufacturing, and regulation collectively advance the capabilities of intelligent sensing solutions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The AI Sensor Integration market is evolving through highly specific applications that deliver significant operational value. An AI sensor for predictive maintenance is becoming standard in industrial IoT, where real-time processing in AI sensors allows machinery to self-diagnose and prevent failures.

- In mobility, edge AI in autonomous vehicles relies on LiDAR sensor fusion for robotics and other autonomous systems to navigate complex environments safely. This is complemented by on-chip AI for smart cameras, which enhances object detection and classification. For consumers, TinyML for wearable health devices is enabling continuous, low-power health monitoring.

- The use of a digital twin for sensor autocalibration ensures long-term accuracy, while generative AI in sensor data synthesis helps train more robust models. Across industries, computer vision for quality control is achieving near-perfect inspection rates, a significant improvement over manual methods. AI-driven acoustic sensing applications are finding new uses in infrastructure monitoring.

- As deployment scales, AI sensor integration cost analysis becomes crucial, alongside addressing AI sensor integration and data privacy. Key growth areas include AI sensor integration in smart cities and AI sensor integration for supply chains, where hardware acceleration for AI sensors is unlocking new efficiencies.

- Furthermore, natural language processing for robotics and explainable AI in medical sensors are making systems more interactive and trustworthy, showcasing the broad impact of multimodal sensor data analysis.

What are the key market drivers leading to the rise in the adoption of AI Sensor Integration Industry?

- Rapid advancements in edge computing and local processing capabilities are a key driver for the market, enabling real-time data analysis at the sensor level.

- The market's growth is fueled by fundamental shifts in computing and industrial strategy.

- The primary driver is the advancement of edge computing capabilities, which enables local data processing and real-time responsiveness essential for autonomous navigation systems and industrial safety applications, reducing decision latency by over 50% versus cloud-dependent architectures.

- A second major driver is the global adoption of Industry 4.0 integration, where AI-powered predictive maintenance systems are cutting unplanned downtime by as much as 60% in smart factory ecosystems.

- The third driver is the pursuit of higher autonomy in software-defined vehicles, where the integration of advanced safety features has contributed to a 25% decrease in certain accident types, solidifying the importance of intelligent sensing solutions for enhancing safety and efficiency.

What are the market trends shaping the AI Sensor Integration Industry?

- A defining market trend is the emergence of on-chip machine learning and TinyML architectures. This shift facilitates the migration of intelligence from the cloud to the extreme edge of sensor networks.

- Key trends are reshaping the AI Sensor Integration market by embedding intelligence directly at the edge. The rise of TinyML architectures and on-chip machine learning is enabling always-on sensing capabilities in low-power devices, extending battery life in industrial IoT applications by up to 70%.

- Another significant trend is multimodal sensor fusion, where unified software stacks process inputs from various sensors to create a comprehensive environmental understanding, improving fault detection accuracy by over 40% compared to single-sensor systems. Furthermore, the use of digital twin integration for autocalibration algorithms is creating self-healing sensor networks.

- This approach, which facilitates predictive drift correction and lifecycle AI management, reduces manual calibration requirements by 90% and ensures sustained data integrity in critical systems, supporting new pay-per-use data models.

What challenges does the AI Sensor Integration Industry face during its growth?

- Significant technical barriers in achieving hardware and software harmonization present a key challenge to industry growth and integration efficiency.

- Despite strong growth, the AI Sensor Integration market faces significant operational hurdles. A primary challenge is hardware-software harmonization, where the lack of standardized interfaces between system-on-chip architectures and AI models can increase development cycles by up to 30%. This is compounded by the technical demands of creating effective thermal management systems for high-performance, low energy consumption SoCs.

- Another critical challenge is navigating complex regulatory compliance frameworks and ensuring sensor data security, as the need for explainable AI for sensors adds another layer of design complexity.

- Finally, the high capital investment and a shortage of professionals with interdisciplinary engineering skills create a barrier to entry, with the cost of deploying advanced sensor networks being 25% higher than traditional systems, limiting adoption for smaller enterprises.

Exclusive Technavio Analysis on Customer Landscape

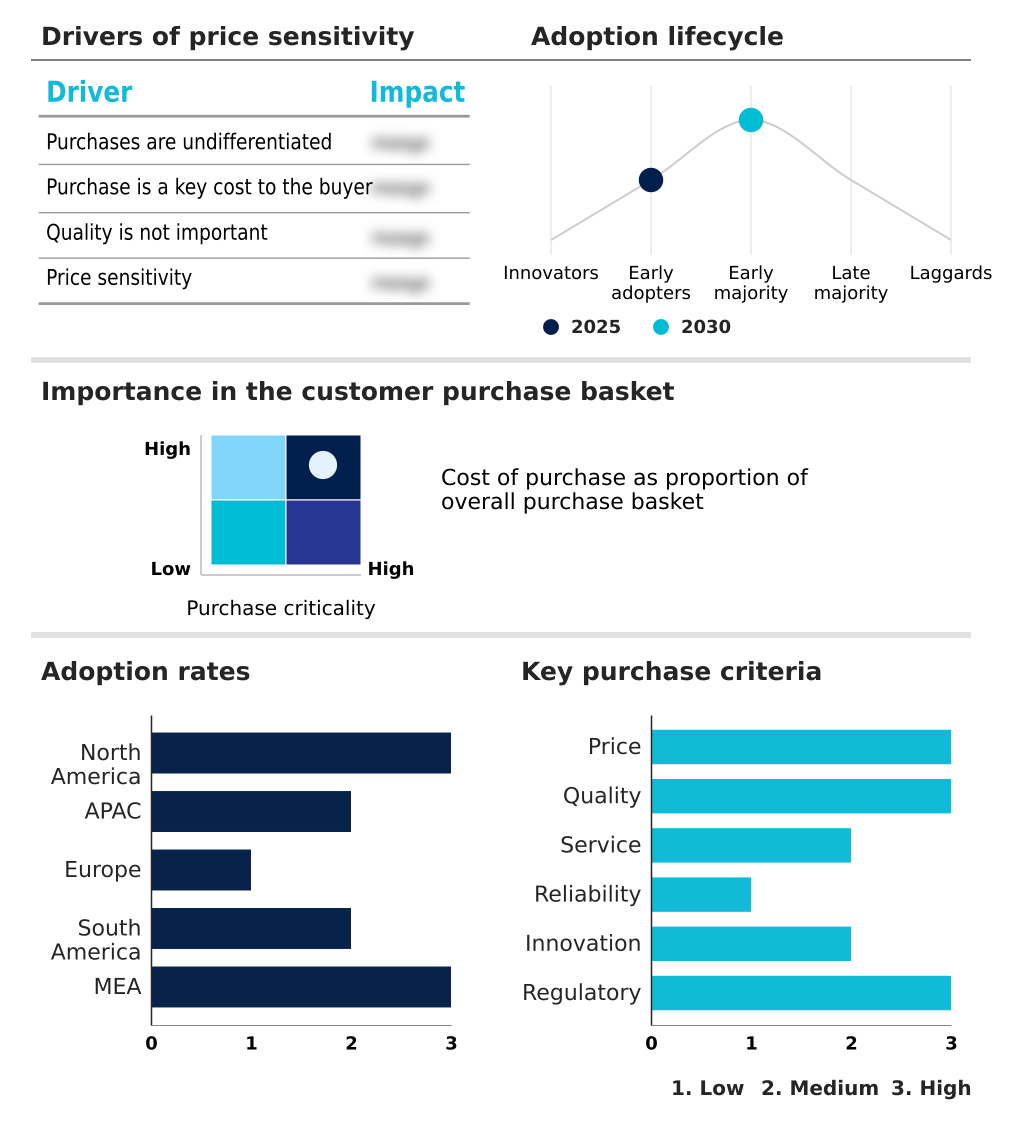

The ai sensor integration market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai sensor integration market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Sensor Integration Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai sensor integration market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Offers intelligent sensing solutions for condition monitoring and AI-driven industrial automation, enhancing operational efficiency and predictive oversight.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- ADLINK Technology Inc.

- Advantech Co. Ltd.

- Analog Devices Inc.

- Basler AG

- Honeywell International Inc.

- Intel Corp.

- Keyence Corp.

- NVIDIA Corp.

- NXP Semiconductors NV

- OMRON Corp.

- Qualcomm Inc.

- Robert Bosch GmbH

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Sony Semiconductor Solutions

- Teledyne FLIR LLC

- Teledyne Technologies Inc.

- Zebra Technologies Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai sensor integration market

- In February, 2025, NXP Semiconductors NV introduced its latest series of high-performance microcontrollers engineered for edge-based AI sensing applications, enabling complex neural networks to run directly on the sensor node.

- In March, 2025, Schneider Electric SE launched an innovative AI-driven thermal and acoustic sensing platform for critical electrical infrastructure, using integrated intelligence to monitor equipment health in real time.

- In April, 2025, NVIDIA Corp. launched an update for its edge computing ecosystem that utilizes a localized large language model to interpret and reason across visual and acoustic sensor data for autonomous mobile robots.

- In May, 2025, Qualcomm Inc. announced the commercial deployment of its next-generation Snapdragon Ride platform, which features highly integrated AI sensor processing units for real-time path planning and hazard detection.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Sensor Integration Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 322 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 43.2% |

| Market growth 2026-2030 | USD 30879.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 30.4% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Singapore, Germany, France, UK, Italy, Spain, Sweden, Brazil, Chile, Argentina, Saudi Arabia, UAE, South Africa, Egypt and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI Sensor Integration market is defined by the convergence of advanced hardware and sophisticated algorithms, creating a new class of intelligent devices. A core technological shift is the adoption of on-chip machine learning and specialized AI microprocessors, which enable real-time data interpretation and local data processing.

- This is critical for applications demanding immediate action, such as autonomous systems perception and haptic feedback integration in robotics. Innovations in multimodal sensor fusion, powered by generative AI models and deep learning models for sensors, allow systems to synthesize data from multiple sources like 3D vision systems and LiDAR point cloud analysis.

- This capability directly impacts boardroom strategy, as companies must decide whether to invest in developing AI-enhanced medical imaging or context-aware surveillance systems to gain a competitive edge. The use of autocalibration algorithms and predictive drift correction improves long-term reliability, while technologies like AI-driven thermal sensing and acoustic signature analysis enhance predictive maintenance systems.

- For instance, firms deploying these technologies report a 35% reduction in false positives. The market is also shaped by the need for hardware-software harmonization, robust sensor data security, and adherence to regulatory compliance frameworks.

What are the Key Data Covered in this AI Sensor Integration Market Research and Growth Report?

-

What is the expected growth of the AI Sensor Integration Market between 2026 and 2030?

-

USD 30.88 billion, at a CAGR of 43.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Mobility sector, Industrial and manufacturing, Healthcare and medical, Robotics and automation, and Security and surveillance), Technology (Machine learning, Computer vision, Deep learning, and Natural language processing), Type (Image sensors, Radar sensors, Ultrasonic sensors, and Lidar sensors) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rapid advancement in edge computing and local processing capabilities, Technical barriers in hardware and software harmonization

-

-

Who are the major players in the AI Sensor Integration Market?

-

ABB Ltd., ADLINK Technology Inc., Advantech Co. Ltd., Analog Devices Inc., Basler AG, Honeywell International Inc., Intel Corp., Keyence Corp., NVIDIA Corp., NXP Semiconductors NV, OMRON Corp., Qualcomm Inc., Robert Bosch GmbH, Rockwell Automation Inc., Schneider Electric SE, Siemens AG, Sony Semiconductor Solutions, Teledyne FLIR LLC, Teledyne Technologies Inc. and Zebra Technologies Corp.

-

Market Research Insights

- The AI Sensor Integration market is defined by rapid advancements that deliver tangible business outcomes. The adoption of intelligent sensing solutions is enabling real-time responsiveness, with edge-based systems processing data up to 20 times faster than centralized models.

- In mobility, the development of software-defined vehicles equipped with advanced driver-assistance systems (ADAS) has led to a 40% reduction in certain types of collisions. In manufacturing, Industry 4.0 integration with cognitive sensing systems facilitates automated quality control, improving defect detection rates by over 60%. These self-contained intelligent units not only enhance performance but also address data privacy at the edge.

- The focus on creating self-healing sensor networks and AI-native hardware underscores a strategic pivot toward more autonomous, efficient, and secure operational frameworks across all major industries.

We can help! Our analysts can customize this ai sensor integration market research report to meet your requirements.

RIA -

RIA -