AI Vehicle Inspection System Market Size 2025-2029

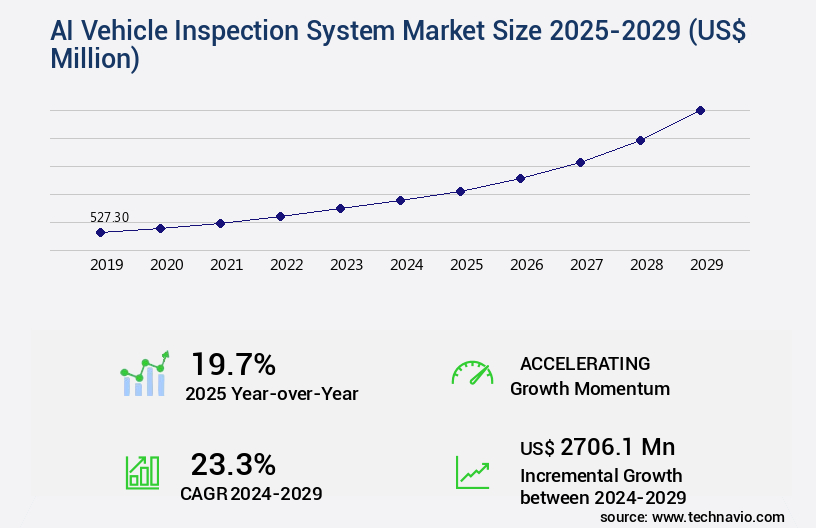

The AI vehicle inspection system market size is valued to increase by USD 2.71 billion, at a CAGR of 23.3% from 2024 to 2029. Increasing demand for operational efficiency and standardization in automotive value chain will drive the ai vehicle inspection system market.

Major Market Trends & Insights

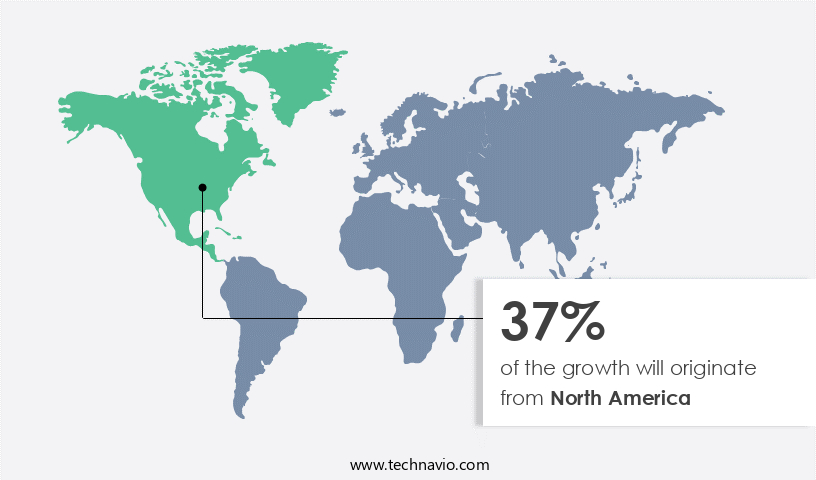

- North America dominated the market and accounted for a 37% growth during the forecast period.

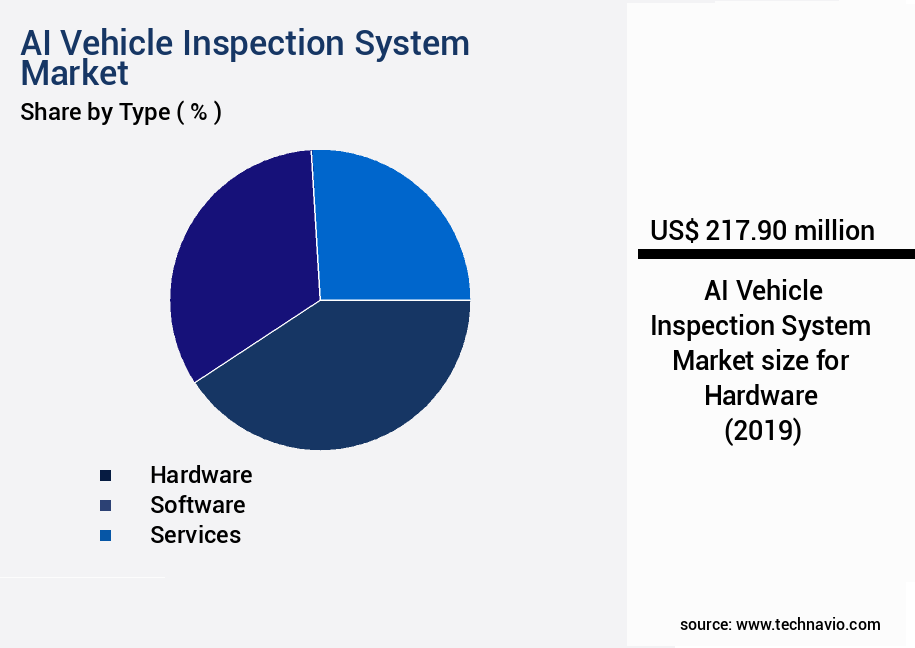

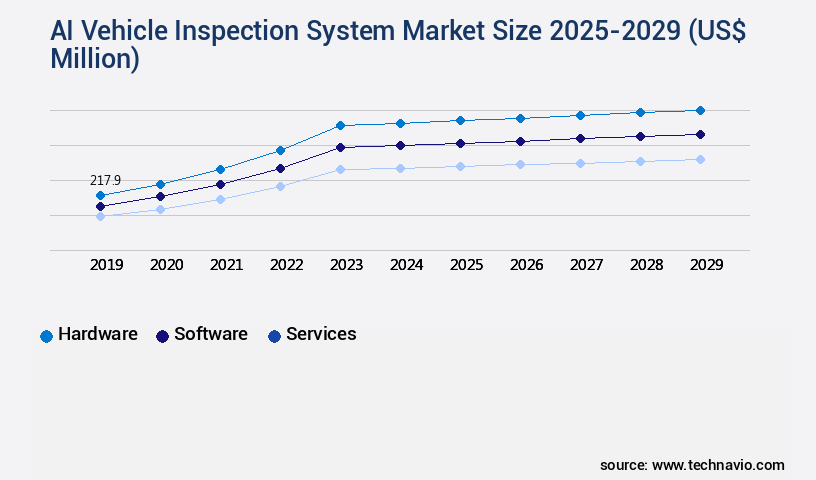

- By Type - Hardware segment was valued at USD 217.90 billion in 2023

- By Technology - Machine learning segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 690.08 million

- Market Future Opportunities: USD 2706.10 million

- CAGR from 2024 to 2029 : 23.3%

Market Summary

- In the global automotive industry, the adoption of AI Vehicle Inspection Systems is gaining traction as a solution to enhance operational efficiency and standardization. These systems leverage advanced technologies like machine learning and computer vision to automate vehicle inspections, reducing human error and increasing throughput. However, the implementation of these systems comes with challenges. The high initial capital outlay and intricate system integration can pose significant barriers to entry for smaller players.

- Furthermore, the shift towards mobile-first solutions and Infrastructure-as-a-Service (IaaS) models is adding to the complexity of the market. Despite these challenges, the benefits of AI Vehicle Inspection Systems, such as improved accuracy, reduced inspection times, and enhanced safety, make them an attractive proposition for businesses seeking to optimize their operations and stay competitive in the evolving automotive landscape.

What will be the Size of the AI Vehicle Inspection System Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI Vehicle Inspection System Market Segmented ?

The AI vehicle inspection system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Hardware

- Software

- Services

- Technology

- Machine learning

- Computer vision

- Deep learning

- Image processing

- Others

- End-user

- Automotive dealerships

- Fleet management companies

- Insurance companies

- Government agencies

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Type Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth as advanced technologies such as deep learning models, predictive maintenance, and computer vision systems revolutionize the automotive industry. These systems employ object detection accuracy, license plate recognition, and image recognition algorithms to assess vehicle condition in real-time, enabling cost reduction strategies through efficient inspection workflow optimization. A key component of these systems is the cloud-based platform, which facilitates API integration capabilities, data analytics dashboards, and remote vehicle inspection. Deep learning models and risk assessment scoring are integral to the AI-powered diagnostics, which enable defect classification and damage assessment with unprecedented accuracy.

Maintenance scheduling and damage assessment are automated, ensuring adherence to vehicle safety standards. The market's ongoing evolution is marked by the integration of sensor fusion methods, thermal imaging analysis, and algorithm performance evaluation, all aimed at improving efficiency and reducing costs. A recent study revealed that AI vehicle inspection systems can achieve a 30% reduction in inspection time compared to traditional methods. This is a testament to the market's potential for enhancing operational efficiency while maintaining the highest data security protocols. The future of the market lies in the continuous development of model training datasets, inspection workflow optimization, and the integration of autonomous inspection capabilities.

The Hardware segment was valued at USD 217.90 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Vehicle Inspection System Market Demand is Rising in North America Request Free Sample

The market is witnessing significant growth, driven by the advanced needs of various industries, particularly in North America, where the United States leads with a mature and high-volume automotive ecosystem. This region's dominance is fueled by the sophisticated requirements of the used vehicle remarketing industry, the strategic push by major insurance sectors for operational efficiency, and the digitization efforts of original equipment manufacturers (OEMs) to enhance customer service experiences. In the remarketing sector, companies like Cox Automotive are pioneering the use of AI to generate trustworthy and transparent digital condition reports, a crucial aspect for high-volume online auction platforms.

The market's growth is further propelled by the increasing demand for streamlined and accurate vehicle inspections, reducing the need for manual labor and minimizing human error.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to the integration of advanced technologies such as computer vision and deep learning in automotive diagnostics. These technologies enable real-time defect classification systems, improving vehicle inspection efficiency and accuracy. AI-based vehicle damage detection using computer vision and deep learning algorithms can identify even the most subtle defects, ensuring comprehensive vehicle condition assessments. Cloud-based vehicle inspection platforms are gaining popularity due to their ability to store and process vast amounts of data, enabling AI-powered predictive maintenance for vehicles. Advanced image processing techniques, including license plate recognition using deep learning and 3D point cloud analysis, enhance the capabilities of AI-driven vehicle safety inspection systems.

Sensor fusion and thermal imaging are also essential components of AI vehicle inspection systems, providing more accurate and reliable results. Data analytics plays a crucial role in risk assessment based on vehicle inspection data, allowing fleet managers to prioritize maintenance and repair activities. AI-powered reporting and visualization tools enable remote vehicle inspection using AI, providing real-time insights into vehicle conditions and maintenance requirements. The integration of these technologies is revolutionizing the automotive industry, enabling more efficient and effective vehicle inspections and maintenance workflows. In conclusion, The market is poised for continued growth as more organizations recognize the benefits of using AI for vehicle damage detection, predictive maintenance, and risk assessment. The integration of computer vision, deep learning, sensor fusion, thermal imaging, and data analytics is transforming the way vehicles are inspected and maintained, leading to improved safety, reliability, and operational efficiency.

What are the key market drivers leading to the rise in the adoption of AI Vehicle Inspection System Industry?

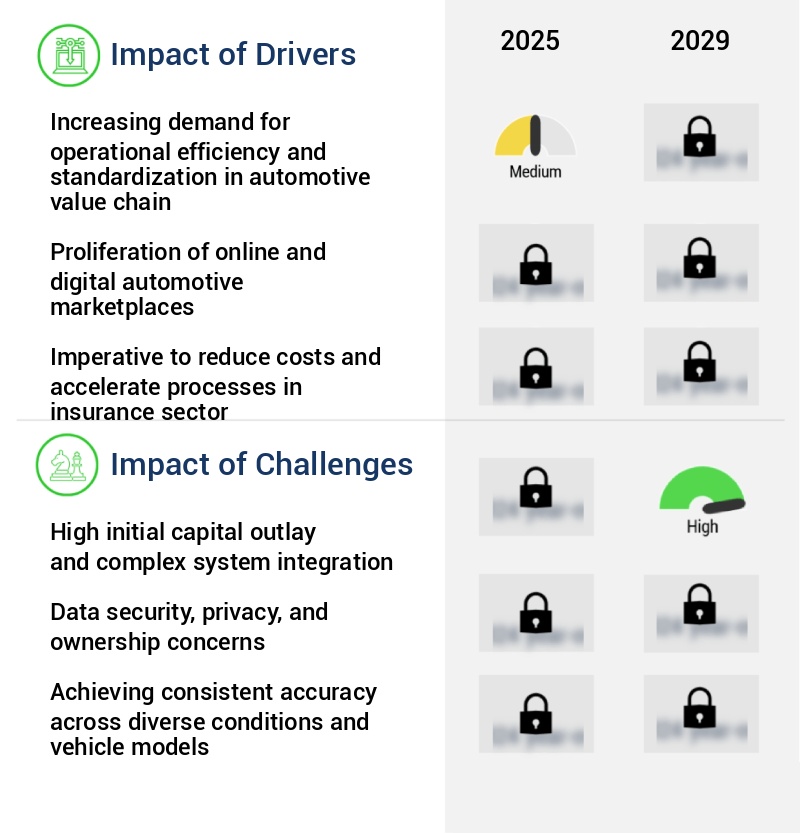

- The escalating need for operational efficiency and standardization in the automotive value chain serves as the primary catalyst for market growth.

- The market is experiencing significant growth due to the increasing demand for operational efficiency, cost reduction, and process standardization in the automotive industry. Traditional manual vehicle inspections, a common practice in manufacturing, logistics, and after-sales service, are known for their inefficiencies. These methods are labor-intensive, time-consuming, and subjective, leading to inconsistent results and disputes. AI vehicle inspection systems offer a solution by introducing automation, objectivity, and speed. For instance, a stationary gantry system can perform a comprehensive exterior and underbody scan in mere seconds, compared to the many minutes or hours required for a manual check.

- The implementation of these systems can significantly reduce reconditioning costs and enhance trust among stakeholders. The integration of AI technology in vehicle inspections is poised to revolutionize the industry, offering substantial benefits to various sectors.

What are the market trends shaping the AI Vehicle Inspection System Industry?

- Shifting towards mobile-first solutions and Infrastructure-as-a-Service (IaaS) models is becoming the industry standard.

- The market is undergoing a significant transformation, moving from traditional, hardware-centric solutions towards more agile, software-driven alternatives. This transition is spurred by the growing demand for accessible and affordable inspection technology among various sectors, beyond the reach of large original equipment manufacturers and auction houses. Advanced software solutions are now being developed, harnessing the processing power and high-definition cameras of standard smartphones and tablets. This mobile-first approach significantly reduces the financial burden for smaller entities such as independent repair shops, used car lots, and insurance adjusters, enabling them to incorporate advanced inspection capabilities without substantial upfront investment.

- The shift towards software-centric AI vehicle inspection systems represents a defining trend in the market, expanding its reach and democratizing the technology.

What challenges does the AI Vehicle Inspection System Industry face during its growth?

- The high initial capital requirements and intricate system integration represent significant challenges that hinder industry growth, necessitating substantial investment and technical expertise.

- The market is experiencing significant evolution, offering advanced solutions for identifying vehicle defects and ensuring safety and efficiency in various sectors. Despite its benefits, the adoption of these systems, particularly for complex gantry and tunnel solutions, is hindered by the substantial initial investment. The procurement of high-resolution cameras, specialized lighting, powerful on-site computing hardware, and physical infrastructure represents a considerable financial commitment. This high upfront cost can deter small and medium-sized enterprises, such as independent auto repair shops, smaller dealerships, and local fleet operators, which collectively comprise a substantial portion of the potential market.

- The complexity of system integration is another challenge. These are not plug-and-play devices; they require deep integration into the existing operational and IT workflows of the end-users. Nevertheless, the market's potential growth is substantial, with an estimated 20% of global vehicle inspection systems expected to transition to AI-driven solutions by 2025.

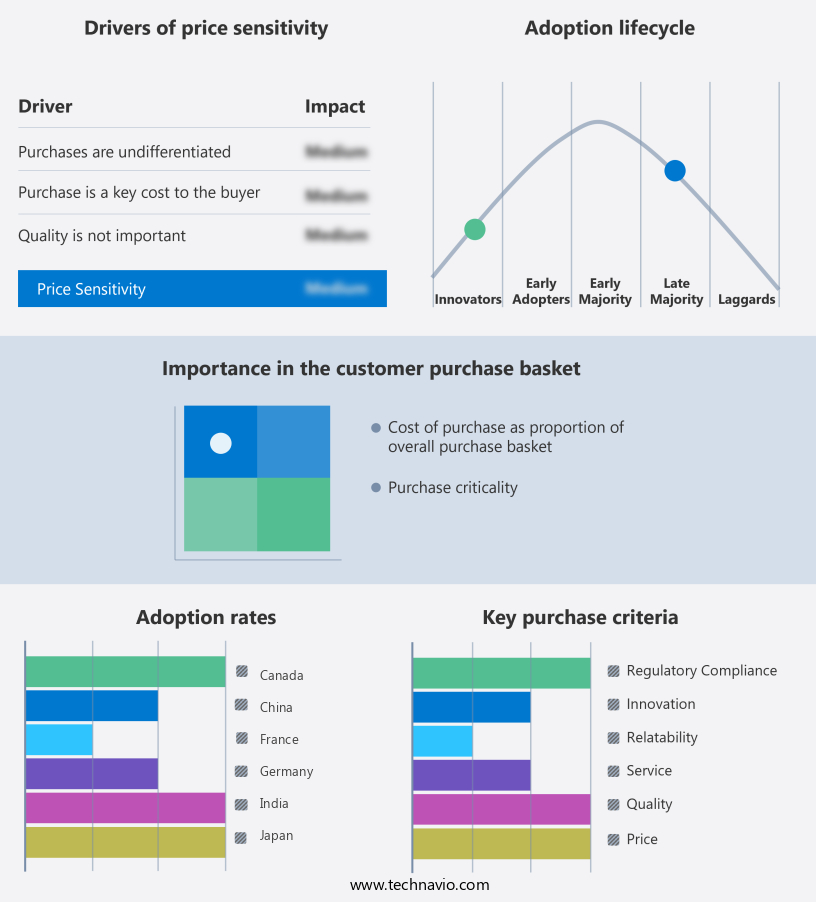

Exclusive Technavio Analysis on Customer Landscape

The ai vehicle inspection system market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai vehicle inspection system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI Vehicle Inspection System Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai vehicle inspection system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bdeo Technologies S.L.

- CamCom Technologies Pvt. Ltd.

- Continental AG

- ControlExpert GmbH

- DeGould Ltd.

- DriveX Technologies OU

- Eventila Technologies Pvt. Ltd.

- Inspektlabs

- Monk AI

- Pave Metrics Inc.

- ProovStation

- Ravin AI Ltd.

- SAWITT FZCO

- Solera Holdings LLC

- Sygma.AI

- Tchek

- Tractable Ltd.

- Trueclaim.ai

- UVeye Inc.

- WeProov

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI Vehicle Inspection System Market

- In January 2024, Tesla, a leading electric vehicle manufacturer, announced the integration of its AI vehicle inspection system into its service centers. This system, named "Tesla Vision," uses artificial intelligence to analyze images and videos from vehicle inspections, reducing the need for manual inspections and improving efficiency (Tesla Press Release).

- In March 2024, Intel and NVIDIA, two technology giants, formed a strategic partnership to develop AI-powered vehicle inspection systems. The collaboration aimed to combine Intel's computing capabilities with NVIDIA's AI expertise, enhancing the performance and accuracy of AI vehicle inspection systems (Intel Press Release).

- In May 2024, Autoliv, a leading automotive safety supplier, completed the acquisition of EyeRis, a computer vision technology company specializing in AI vehicle inspection systems. This acquisition expanded Autoliv's product portfolio and strengthened its position in the growing AI vehicle inspection market (Autoliv Press Release).

- In April 2025, the European Union announced the approval of regulations mandating AI vehicle inspection systems in all member countries by 2028. This policy change is expected to drive significant growth in the European AI vehicle inspection market, as all commercial vehicles will be required to undergo regular AI inspections (European Commission Press Release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Vehicle Inspection System Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

244 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 23.3% |

|

Market growth 2025-2029 |

USD 2706.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

19.7 |

|

Key countries |

US, China, Canada, Mexico, Japan, Germany, South Korea, France, UK, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, revolutionizing the way industries approach vehicle maintenance and safety. Predictive maintenance, enabled by deep learning models and risk assessment scoring, allows for early identification of potential issues, reducing the need for costly repairs. A cloud-based platform facilitates real-time processing, enabling remote vehicle inspections and vehicle condition reporting. For instance, a leading transportation company reported a 25% reduction in maintenance costs after implementing an AI-powered diagnostics system. The industry anticipates a 20% growth in AI adoption for vehicle inspections in the next five years. AI-vehicle inspection systems employ image recognition algorithms, license plate recognition, and object detection accuracy for defect classification.

- API integration capabilities enable seamless data flow between systems, while data analytics dashboards provide valuable insights for maintenance scheduling and damage assessment. Computer vision systems, sensor fusion methods, and thermal imaging analysis contribute to the efficiency improvement metrics of these systems. Data annotation techniques and model training datasets ensure algorithm performance evaluation, maintaining high object detection accuracy. Vehicle safety standards are upheld through AI-vehicle inspection systems, which utilize deep learning models for risk assessment scoring and AI-powered diagnostics. These systems also offer optical character recognition for document verification and compliance checks. Data security protocols are essential in AI-vehicle inspection systems, ensuring the confidentiality and integrity of sensitive vehicle data.

- Inspection workflow optimization and algorithm performance evaluation are ongoing priorities for continuous improvement.

What are the Key Data Covered in this AI Vehicle Inspection System Market Research and Growth Report?

-

What is the expected growth of the AI Vehicle Inspection System Market between 2025 and 2029?

-

USD 2.71 billion, at a CAGR of 23.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Hardware, Software, and Services), Technology (Machine learning, Computer vision, Deep learning, Image processing, and Others), End-user (Automotive dealerships, Fleet management companies, Insurance companies, Government agencies, and Others), and Geography (North America, APAC, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for operational efficiency and standardization in automotive value chain, High initial capital outlay and complex system integration

-

-

Who are the major players in the AI Vehicle Inspection System Market?

-

Bdeo Technologies S.L., CamCom Technologies Pvt. Ltd., Continental AG, ControlExpert GmbH, DeGould Ltd., DriveX Technologies OU, Eventila Technologies Pvt. Ltd., Inspektlabs, Monk AI, Pave Metrics Inc., ProovStation, Ravin AI Ltd., SAWITT FZCO, Solera Holdings LLC, Sygma.AI, Tchek, Tractable Ltd., Trueclaim.ai, UVeye Inc., and WeProov

-

Market Research Insights

- The market for AI vehicle inspection systems is continuously evolving, with advancements in technology driving innovation and growth. According to industry reports, the global market for AI in automotive is projected to grow by 25% annually over the next five years. For instance, a leading automotive manufacturer reported a 15% increase in production efficiency after implementing an AI-powered inspection system. This technology enables faster and more accurate inspections, reducing labor costs and minimizing errors. The integration of AI in vehicle inspection systems is transforming the industry, offering significant benefits such as improved scalability, data preprocessing techniques, and maintenance procedures.

- These advancements contribute to the increasing adoption of AI in the automotive sector, making it an essential component of modern manufacturing processes.

We can help! Our analysts can customize this AI vehicle inspection system market research report to meet your requirements.

RIA -

RIA -