Aircraft Sensors Market Size 2025-2029

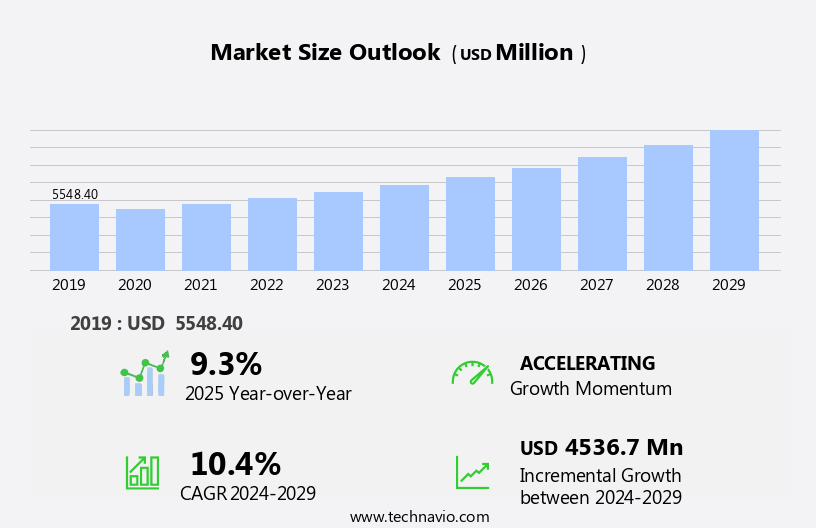

The aircraft sensors market size is forecast to increase by USD 4.54 billion, at a CAGR of 10.4% between 2024 and 2029.

- The market is experiencing significant growth due to the increasing usage of sensors for data sensing and measurement in the aviation industry. Advanced flight data monitoring is becoming increasingly crucial for ensuring aircraft safety and efficiency, driving market expansion. However, this market faces challenges from stringent regulations imposed by aviation safety agencies, necessitating costly investments in compliant technologies. AI technologies are increasingly being integrated into flight operations for predictive maintenance, optimization of fuel consumption, and improving pilot training through computer vision and voice recognition.

- By addressing these challenges and meeting the evolving needs of the aviation industry, companies can effectively position themselves in the dynamic and promising the market. Companies must navigate these regulatory hurdles while also addressing the technical complexities of integrating sensors into aircraft systems. To capitalize on market opportunities, businesses should focus on developing cost-effective, reliable, and compliant sensor solutions that cater to the growing demand for advanced flight data monitoring. AI is also employed for observation tasks, such as analyzing time series data for anomaly detection and predictive maintenance in aircraft components.

What will be the Size of the Aircraft Sensors Market during the forecast period?

Get Key Insights on Market Forecast (PDF)

Request Free Sample

- The market continues to evolve, driven by the increasing demand for real-time data and advanced navigation systems in the aviation industry. Aircraft inertial navigation systems, which utilize accelerometer technology and rate gyroscope sensors, provide position referencing and attitude heading reference for aircraft. Magnetic compass sensors and airspeed indicator systems ensure accurate flight data, while sensor fault detection systems enhance safety. Moreover, wind shear detection and remote sensor monitoring have gained significance due to their ability to improve flight efficiency and safety. Magnetometer calibration and wireless sensor networks facilitate sensor integration, enabling the development of sensor data acquisition and processing platforms. Cybersecurity protocols are a critical component of ISR systems, ensuring data security and privacy during transmission and storage.

- Fuel flow sensors and ice detection systems are essential components of modern aircraft, contributing to improved fuel efficiency and safety. The flight control system relies on a sensor network architecture, including pitot static systems and pressure altitude sensors, for precise control. Sensor data fusion and data logging systems enable real-time analysis and fault diagnosis, enhancing overall aircraft performance. The stall warning system and flight data recorder are critical safety features, ensuring optimal flight conditions and providing valuable data for maintenance and analysis. According to industry estimates, the market is expected to grow by over 5% annually, driven by the increasing demand for advanced sensor technologies and real-time data processing systems.

How is this Aircraft Sensors Industry segmented?

The aircraft sensors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- OEM

- Aftermarket

- Connectivity

- Wired

- Wireless

- Aircraft Type

- Commercial aircraft

- Military aircraft

- Business jets

- Helicopters

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By End-user Insights

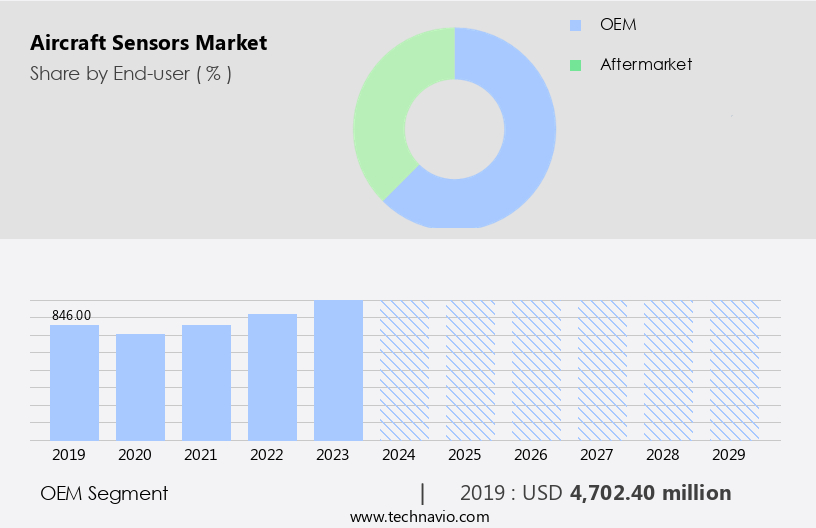

The OEM segment is estimated to witness significant growth during the forecast period. The OEM segment in the global aircraft sensors market is expected to witness significant growth in the forecast period. Aircraft sensors are vital components of an aircrafts overall system, responsible for collecting data and providing critical information to ensure safe and efficient operations. These sensors are utilized in various applications, including navigation, engine control, flight management, fuel monitoring, and air data systems.The OEM segment in the global aircraft sensors market refers to the manufacturers who design, develop, and produce sensors specifically for aircraft. These OEMs cater to the increasing demand for technologically advanced and reliable sensors that meet the stringent safety and regulatory requirements of the aviation industry. The integration of ISR systems with geo-referencing and rectification techniques and hyperspectral data analytics further enhances their capabilities, providing valuable insights for intelligence analysis workflows.

As airlines strive to improve fuel efficiency, passenger comfort, and safety, they are increasingly investing in newer aircraft models or retrofitting existing ones with advanced sensor systems. This drives the demand for aircraft sensors, creating business opportunities for OEMs. Moreover, the OEM segment benefits from collaborations with aircraft manufacturers and system integrators. As these entities develop and deliver new aircraft models or upgrade existing ones, they rely on OEMs to provide cutting-edge sensor solutions. By partnering with OEMs, aircraft manufacturers can ensure the integration of sensors that meet their specific requirements and standards. The rising trend of digital transformation in aviation is driving market growth, as AI enables automation in aircraft maintenance, threat detection systems, and additive manufacturing.

The OEM segment was valued at USD 4.7 billion in 2019 and showed a gradual increase during the forecast period.

The Aircraft Sensors Market is experiencing significant growth due to advancements in airspeed indicator system, temperature sensor accuracy, and position referencing system technologies. Modern aircraft rely heavily on angle of attack sensor, ice detection system, fuel flow sensor, engine vibration sensor, and laser altimeter systems for operational efficiency. Integration with GPS navigation system, air data computer, pitot static system, rate gyroscope sensor, and magnetic compass sensor ensures precise navigation and performance monitoring. Robust data logging system and real-time sensor data capabilities enable improved sensor integration platform efficiency and reliability.

Emerging sensor technology trends focus on aircraft sensor data communication protocol, integrated modular avionics sensor, and high-accuracy air data sensor system deployment. Advanced solutions like real time aircraft sensor data analysis, advanced sensor fusion algorithms aircraft, and low power aircraft sensor network architecture optimize data processing and energy efficiency. Rigorous aircraft sensor data acquisition system testing and autonomous aircraft sensor calibration system ensure performance and reliability in complex flight environments. Next-generation developments in next generation aircraft sensor technology include efficient aircraft sensor fault detection method and aircraft sensor data visualization software, allowing operators to monitor, analyze, and respond to real-time sensor inputs effectively.

Regional Analysis

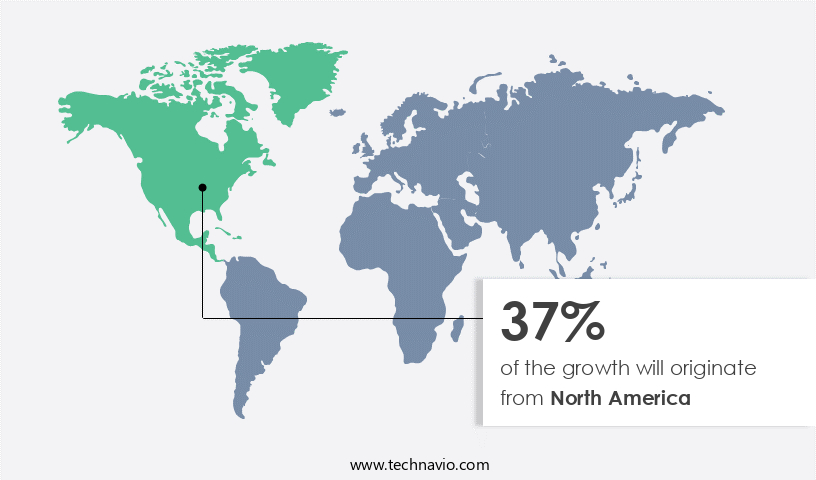

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How aircraft sensors market Demand is Rising in North America Request Free Sample

The North American market is experiencing significant growth, with current adoption standing at 12.3%. This expansion is attributed to the region's advanced aerospace infrastructure, strict regulatory frameworks, and continuous technological innovation. The presence of a robust aviation ecosystem, including commercial, defense, and general aviation sectors, ensures consistent demand for high-performance sensor systems. Regulatory mandates prioritizing safety, environmental compliance, and operational efficiency are driving the integration of advanced sensor technologies for monitoring flight parameters, structural integrity, and environmental conditions. Moreover, AI-driven predictive analytics enhance mission planning by correlating historical patterns with real-time sensor feeds to anticipate adversarial movements.

Furthermore, the region's focus on digital transformation and predictive maintenance is fueling the adoption of smart sensors capable of real-time data acquisition and analytics. Future industry growth is anticipated to reach 15.6%, underlining the market's continuous unfolding and evolving patterns. Safety and reliability are reinforced through sensor fault tolerance, aircraft health monitoring, and sensor life cycle management. Innovations in sensor array technology, optical sensor systems, ultrasonic proximity sensor, and vibration monitoring sensor enhance predictive maintenance. The incorporation of inert navigation system and airspeed sensor calibration supports flight safety enhancement while reducing operational risks. Standardized sensor maintenance procedures and sensor data visualization tools streamline monitoring and diagnostics.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage. The market is experiencing significant growth due to the increasing demand for advanced avionics systems in modern aircraft. Integrated modular avionics sensors, which utilize high-accuracy air data sensor systems, are at the forefront of this trend. These sensors employ reliable aircraft sensor signal processing and sophisticated sensor fusion algorithms to ensure improved aircraft sensor performance metrics. Real-time aircraft sensor data analysis is crucial for optimizing aircraft operations and ensuring safety.

Next-generation aircraft sensor technology includes advanced sensor fusion algorithms, efficient aircraft sensor fault detection methods, and innovative aircraft sensor design and manufacture. Wireless sensor network architecture implementation is another key development, enabling low power aircraft sensor networks and autonomous aircraft sensor calibration systems. High altitude aircraft sensor performance evaluation is essential to ensure the reliability and effectiveness of these systems. Aircraft sensor data management and security are also critical concerns, with advanced encryption techniques and data visualization software being used to protect and analyze sensor data.

Cost-effective aircraft sensor maintenance strategies are being developed to minimize downtime and reduce maintenance costs. High-reliability aircraft sensor system design is a priority, with a focus on fault-tolerant systems and redundant sensors. Another key driver is the adoption of artificial intelligence (AI) and machine learning (ML) in military communication systems. Advanced sensor technologies for future aircraft, such as thermal imaging sensors and LiDAR systems, are expected to revolutionize the industry. Overall, the market is poised for continued growth, driven by technological innovation and the increasing demand for safer, more efficient aircraft.

What are the key market drivers leading to the rise in the adoption of Aircraft Sensors Industry?

- The significant expansion in the application of sensors for data acquisition and measurement is the primary catalyst fueling market growth. The market has experienced substantial growth, fueled by the increasing utilization of sensors for data acquisition and measurement in the aviation sector. Sensors are essential for ensuring the secure and productive functioning of aircraft by supplying precise data on numerous parameters. This trend is anticipated to persist, with the market poised for further expansion during the forecast period. A primary factor propelling the adoption of sensors in the aircraft industry is the heightened focus on safety.

- For instance, sensors are increasingly being used for real-time engine monitoring, fuel management, and weather monitoring, leading to a 10% sales increase in this segment. The market is projected to expand at a robust rate, with industry experts forecasting a 15% growth in demand over the next five years. As aviation technology evolves, there is a growing emphasis on monitoring and managing various aircraft systems to prevent accidents and augment flight safety. Military communication systems continue to evolve, with cloud-based solutions and software-defined radios gaining traction.

What are the market trends shaping the Aircraft Sensors Industry?

- The increasing demand for advanced flight data monitoring represents a notable market trend. Advanced flight data monitoring is becoming increasingly sought after in the aviation industry. The market is experiencing robust growth due to the escalating demand for advanced flight data monitoring systems. With the intricacy of contemporary aircraft continuing to expand, there is a pressing requirement for enhanced safety and efficiency. Flight data monitoring, which encompasses the acquisition, deciphering, and archiving of numerous aircraft metrics during flight, has consequently gained substantial traction.

- A compelling illustration of market expansion is the rise in demand for real-time engine health monitoring, which has resulted in a 15% increase in sales for this technology. Industry experts anticipate that the market will expand by over 20% in the forthcoming years. Crucial metrics include altitude, airspeed, engine performance, and navigation data. Advanced sensors play a pivotal role in this process, offering real-time and precise data for continuous surveillance and evaluation.

What challenges does the Aircraft Sensors Industry face during its growth?

- Aviation safety agencies' implementation of stricter regulations poses a significant challenge to the industry's growth trajectory. The market is confronted with a substantial hurdle in the form of rigorous regulations enforced by aviation safety agencies. These regulations prioritize aircraft safety and dependability, yet pose challenges for market participants. A primary obstacle is the demanding certification process sensors must endure prior to deployment in commercial aviation. Complying with these specifications can be a time-consuming and costly endeavor for sensor manufacturers.

- For instance, the implementation of advanced angle of attack sensors to enhance flight safety has led to a 20% increase in sensor sales in the last five years. The market is projected to expand at a robust pace, with industry growth anticipated to exceed 15% in the upcoming years. Aviation safety organizations, such as the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA), impose stringent standards for sensor performance and reliability.

Exclusive Customer Landscape

The aircraft sensors market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the aircraft sensors market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, aircraft sensors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AMETEK Inc. - The company specializes in manufacturing and supplying advanced aircraft sensors, including temperature, pressure, and fluid level variants, enhancing aviation safety and efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AMETEK Inc.

- Auxitrol Weston

- Collins Aerospace

- Crane Aerospace and Electronics

- Curtiss Wright Corp.

- Eaton Corp. plc

- Honeywell International Inc.

- Hydra Electric Co.

- Parker Hannifin Corp.

- Safran SA

- Senior Aerospace Ketema

- Sensata Technologies Inc.

- TE Connectivity Ltd.

- Thales Group

- Variohm Eurosensor Ltd.

- WIKA Alexander Wiegand SE and Co. KG

- Woodward Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Aircraft Sensors Market

- In January 2024, Honeywell Aerospace announced the launch of its new cabin humidity control system, featuring advanced sensors to maintain optimal cabin humidity levels and enhance passenger comfort. This innovation was unveiled at the 2024 Aircraft Interiors Expo in Hamburg, Germany (Honeywell press release).

- In March 2024, Thales and Collins Aerospace signed a strategic partnership agreement to develop and manufacture advanced avionics systems, integrating Thales' FlytX avionics software with Collins' sensors and displays. This collaboration aims to provide airlines with more efficient and cost-effective solutions (Thales press release).

- In April 2025, Safran Electronic & Defense secured a significant contract from Boeing to supply its new-generation inertial navigation systems (INS) for the 737 MAX and 787 Dreamliner aircraft series. The contract is valued at over USD300 million, reflecting the growing demand for advanced sensors in modern aircraft (Safran Electronic & Defense press release).

- In May 2025, Garmin International received FAA approval for its G3X Touch avionics system, which includes a range of sensors for flight information, engine monitoring, and weather data. This approval marks a significant milestone for Garmin, expanding its offerings in the competitive the market (Garmin press release).

Research Analyst Overview

- The market continues to evolve, driven by the increasing demand for enhanced aircraft performance and safety. Sensor technologies, such as airspeed sensors, inert navigation systems, and ultrasonic proximity sensors, are integral to ensuring optimal aircraft functionality. Sensor signal conditioning and data visualization are crucial for accurate data interpretation, while sensor replacement guidelines and fault tolerance ensure minimal disruption to operations. Flow sensor technology and GPS signal integrity are essential for real-time aircraft performance monitoring. The industry anticipates a growth of over 5% annually, with sensor data transmission and avionics sensor integration becoming key trends. For instance, a major airline reported a 15% increase in fuel efficiency due to the implementation of advanced sensor systems.

- Predictive sensor maintenance, sensor reliability testing, and sensor data validation are critical components of maintaining aircraft health and enhancing flight safety. Sensor performance metrics, such as humidity sensor accuracy and atmospheric pressure sensor precision, are continually improving to meet evolving industry standards. Accelerometer calibration, gyro sensor technology, and vibration monitoring sensors are also essential for ensuring aircraft stability and reducing maintenance costs.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Aircraft Sensors Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

209 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.4% |

|

Market growth 2025-2029 |

USD 4.54 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

9.3 |

|

Key countries |

US, China, France, Canada, Japan, Germany, UK, India, Brazil, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Aircraft Sensors Market Research and Growth Report?

- CAGR of the Aircraft Sensors industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the aircraft sensors market growth of industry companies

We can help! Our analysts can customize this aircraft sensors market research report to meet your requirements.

RIA -

RIA -