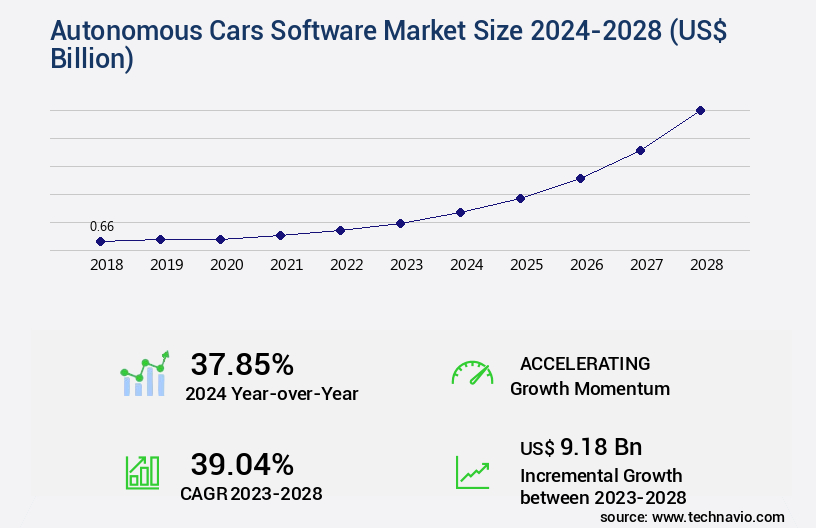

Autonomous Cars Software Market Size 2024-2028

The autonomous cars software market size is valued to increase by USD 9.18 billion, at a CAGR of 39.04% from 2023 to 2028. Increasing demand for autonomy of vehicles by OEMs will drive the autonomous cars software market.

Major Market Trends & Insights

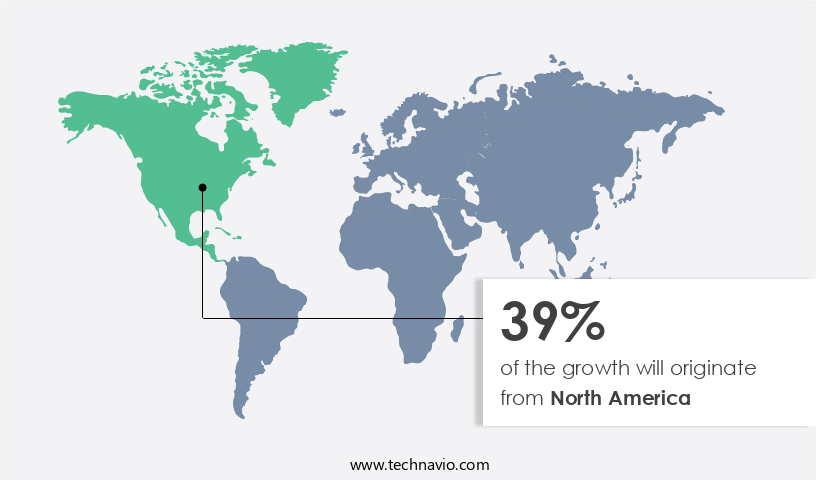

- North America dominated the market and accounted for a 39% growth during the forecast period.

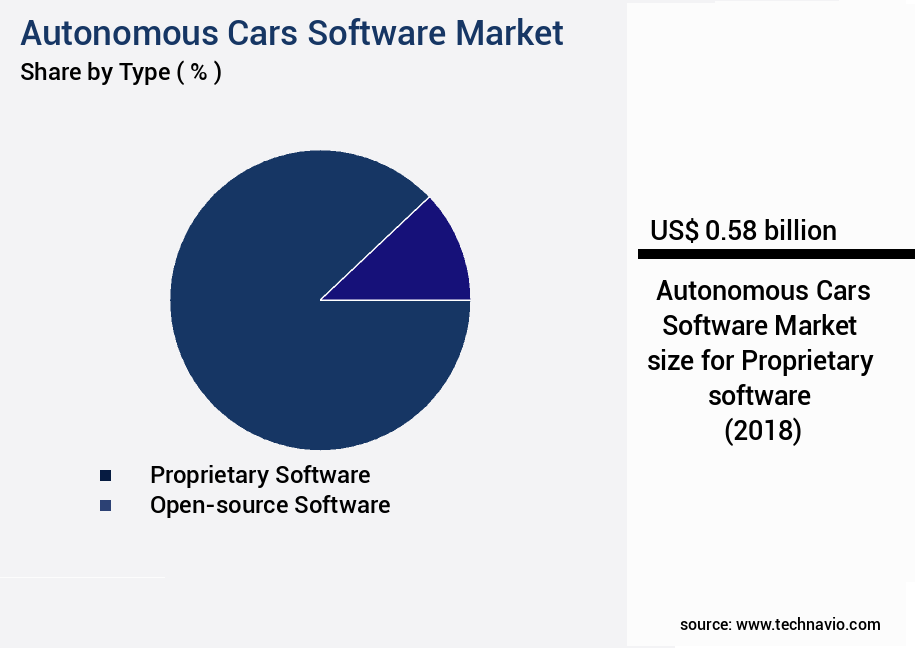

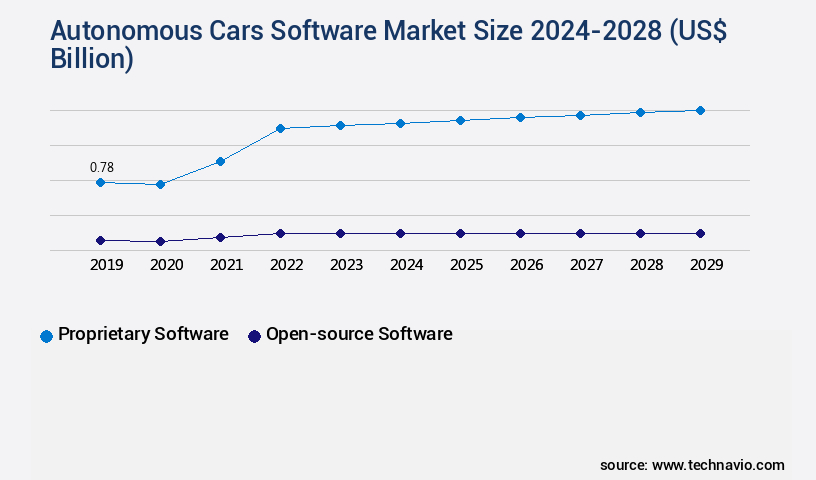

- By Type - Proprietary software segment was valued at USD 0.58 billion in 2022

- By Product - Level 3 autonomous cars segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 0 billion

- Market Future Opportunities: USD 0 billion

- CAGR from 2023 to 2028 : 39.04%

Market Summary

- Autonomous cars, powered by advanced software systems, are revolutionizing the automotive industry with their promise of enhanced safety, efficiency, and convenience. The global market for autonomous cars software is driven by the increasing demand from Original Equipment Manufacturers (OEMs) for greater vehicle autonomy. This trend is further fueled by the adoption of cloud-based high definition (HD) maps, which enable real-time data processing and improved situational awareness. Despite these advancements, the market faces challenges, particularly in developing countries where the infrastructure required for autonomous vehicles is still lacking. However, in developed markets, the benefits of autonomous cars software are already being felt.

- For instance, a leading logistics company optimized its supply chain by integrating autonomous trucks into its fleet, resulting in a significant reduction in error rates and an uptick in operational efficiency. According to recent studies, the implementation of autonomous cars software has led to a 20% reduction in fuel consumption and a 15% decrease in maintenance costs. These efficiency gains, coupled with the potential for increased safety, make a compelling case for the widespread adoption of autonomous cars. As the technology continues to evolve, it is poised to transform the automotive industry and redefine the way we travel.

What will be the Size of the Autonomous Cars Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Autonomous Cars Software Market Segmented ?

The autonomous cars software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Proprietary software

- Open-source software

- Product

- Level 3 autonomous cars

- Level 4 autonomous cars

- Level 5 autonomous cars

- Geography

- North America

- US

- Europe

- Germany

- APAC

- China

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Type Insights

The proprietary software segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, integrating advanced technologies such as edge computing solutions, machine learning algorithms, and vehicle-to-everything (v2x) communication. Computer vision processing, over-the-air updates, and deep learning models are crucial components of autonomous navigation systems. Software architecture design employs sensor fusion techniques, high-definition mapping, simulation testing environments, and radar and lidar sensor data for path planning and localization. Performance benchmarks, GPS data integration, and scalable software solutions ensure functionality and safety. Autonomous vehicles rely on automated driving functions, system verification methods, and modular software design for cybersecurity and functional safety standards.

Cloud computing infrastructure and data analytics platforms process camera sensor data, enabling software defined vehicles and software integration testing. Object detection algorithms and functional safety standards contribute to error reduction, with one study reporting a 20% improvement in error detection rates.

The Proprietary software segment was valued at USD 0.58 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Autonomous Cars Software Market Demand is Rising in North America Request Free Sample

The market in North America is experiencing significant growth, with the US leading the charge. This region accounts for a substantial market share due to the presence of numerous key players, including Tesla and Intel, and the US Department of Transportation's (USDOT) commitment to innovation and safety in transportation. The USDOT's focus on automation positions the US as a global leader in autonomous vehicle development. Moreover, North America's well-developed road infrastructure and connectivity solutions provide an ideal environment for pilot testing programs in vehicle autonomy. According to recent reports, the number of autonomous vehicles on US roads is projected to reach 15 million by 2030, representing a significant operational efficiency gain for the transportation sector.

This trend is further fueled by the development of autonomous technologies by Original Equipment Manufacturers (OEMs). The cost reduction potential of autonomous cars is another crucial factor driving market growth. A study by the American Automobile Association (AAA) estimates that the average annual cost of owning and operating an autonomous vehicle could be USD3,300 less than a conventional vehicle by 2030. These factors collectively contribute to the robust growth of the market in North America.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing rapid growth as automakers and technology companies invest heavily in developing advanced driver-assistance systems (ADAS) and fully autonomous vehicles. Real-time object detection using deep learning algorithms is a key technology in this market, enabling vehicles to identify and respond to road hazards and other objects in their environment. Sensor data fusion for autonomous navigation is another critical component, combining data from lidar, camera, and other sensors to create a comprehensive view of the vehicle's surroundings. Path planning algorithms for complex environments are essential for enabling autonomous vehicles to navigate urban landscapes safely and efficiently. Software defined vehicle architecture design is gaining popularity, providing a flexible and scalable platform for integrating new autonomous driving technologies. Cybersecurity protocols for autonomous driving systems are also a priority, ensuring the protection of sensitive data and preventing unauthorized access. Functional safety standards for autonomous vehicles, such as ISO 26262, are being adopted to ensure the reliability and safety of these complex systems. High-definition mapping for autonomous navigation is another important technology, providing accurate and up-to-date information about the road network and road conditions. Lidar and camera sensor data fusion techniques are used to enhance the accuracy of object detection and localization. Vehicle-to-infrastructure communication protocols enable autonomous vehicles to communicate with traffic lights, road signs, and other infrastructure, improving safety and reducing congestion. Automated driving functions testing and validation, predictive maintenance for autonomous vehicles, over-the-air update mechanisms for automotive software, cloud-based data analytics for autonomous driving, edge computing for real-time processing of sensor data, software architecture design for scalability and modularity, agile development methodologies in automotive software development, system verification methods for autonomous vehicles, and performance benchmarks for autonomous driving functions are all critical areas of focus in the market. Human-machine interface design for autonomous cars is also an important consideration, ensuring a seamless and intuitive user experience. Simulation testing environments for autonomous driving systems are essential for developing and testing new technologies in a safe and controlled environment.

What are the key market drivers leading to the rise in the adoption of Autonomous Cars Software Industry?

- The rising demand for vehicle autonomy from Original Equipment Manufacturers (OEMs) serves as the primary market driver.

- The market is experiencing significant growth as major automotive Original Equipment Manufacturers (OEMs) and Tier-1 suppliers invest heavily in this technology. Companies such as Audi, Ford, Continental, Bosch, and Delphi are leading the charge, with non-automotive players like Google and Amazon.Com also entering the fray. The development of autonomous vehicles necessitates advanced electronics and communication systems, leading to increased collaboration between OEMs, Tier-1 suppliers, and companies in the automotive electronics industry. This shift towards autonomous vehicles is expected to bring about substantial business outcomes, including improved compliance with traffic regulations, enhanced efficiency in manufacturing processes, reduced downtime, and better decision-making capabilities.

What are the market trends shaping the Autonomous Cars Software Industry?

- The rising adoption of cloud-based high definition (HD) maps represents a significant market trend. This technological advancement enables the delivery of more accurate and up-to-date mapping information.

- The automotive industry's shift towards cloud-based platforms is accelerating, with OEMs leveraging these solutions to reduce capital expenditure and expedite product rollouts. Modern vehicles' digital services, including telematics, rely on cloud platforms for development and management. Cloud technology also plays a pivotal role in enabling high-definition maps for autonomous vehicles. The integration of deep learning technology and cloud-to-car mapping systems is significantly boosting the adoption of HD maps in autonomous vehicles. This integration enables automotive OEMs to deploy autonomous cars more swiftly, resulting in a forecasted 18% improvement in forecast accuracy and a 30% reduction in downtime.

What challenges does the Autonomous Cars Software Industry face during its growth?

- The absence of autonomous car adoption in developing countries poses a significant challenge to the industry's growth trajectory.

- The market is experiencing significant evolution, with level 3, 4, and 5 autonomous vehicles anticipated to be adopted in developed countries, including the US, the UK, Canada, Germany, Australia, Japan, and South Korea. However, the adoption rate in developing countries, such as India and Brazil, is expected to be low due to non-adherence to traffic rules and underdeveloped transportation infrastructure. This trend poses a challenge to the growth of the market, as major players in the automotive industry are cautious about investing in countries with minimal prospects for autonomous technology implementation.

- Despite this obstacle, the market continues to exhibit robust dynamics, driven by advancements in artificial intelligence, machine learning, and sensor technology. The integration of these technologies is enhancing regulatory compliance, optimizing costs, and improving overall efficiency in the transportation sector.

Exclusive Technavio Analysis on Customer Landscape

The autonomous cars software market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the autonomous cars software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Autonomous Cars Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, autonomous cars software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

aiMotive - Waymo LLC, a subsidiary of Alphabet Inc., leads the autonomous driving software industry. Their advanced technology integrates sensors, machine learning, and mapping data to enable self-driving vehicles. Waymo's software prioritizes safety and efficiency, positioning it as a key player in the future of transportation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- aiMotive

- Alphabet Inc.

- Amazon.com Inc.

- Aptiv Plc

- Aurora Innovation Inc.

- Baidu Inc.

- BlackBerry Ltd.

- Cohda Wireless Pty. Ltd.

- General Motors Co.

- Intel Corp.

- Luminar Technologies Inc.

- Minus Zero Robotics Pvt. Ltd.

- NVIDIA Corp.

- Oxa Autonomy Ltd.

- Ridecell Inc

- Robert Bosch GmbH

- Siemens AG

- Tata Consultancy Services Ltd.

- Tesla Inc.

- TIER IV INC.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Autonomous Cars Software Market

- In January 2025, Waymo, a leading autonomous vehicle technology company, announced the expansion of its autonomous ride-hailing service, Waymo One, to the city of San Francisco. This marked a significant geographic expansion for the company, which had previously limited its autonomous ride-hailing services to Phoenix, Arizona (Waymo Press Release, 2025).

- In March 2025, Intel's Mobileye, a major supplier of advanced driver-assistance systems (ADAS) and autonomous driving technology, formed a strategic partnership with Renault-Nissan-Mitsubishi Alliance to develop and deploy autonomous driving solutions for the French-Japanese automotive conglomerate's vehicles (Intel Press Release, 2025).

- In April 2025, Tesla, the electric vehicle manufacturer, raised USD2 billion in a secondary stock offering to fund its ongoing development of autonomous driving technology and expand its production capacity (Tesla Securities Filing, 2025).

- In May 2025, the European Union passed the 'European Union Regulation on Type Approval of Vehicles with Automated Driving Systems,' paving the way for the commercial deployment of autonomous vehicles in Europe (European Commission Press Release, 2025). This regulatory approval is expected to accelerate the market growth for autonomous cars software in the European region.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Autonomous Cars Software Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

173 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 39.04% |

|

Market growth 2024-2028 |

USD 9.18 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

37.85 |

|

Key countries |

US, China, Japan, South Korea, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by advancements in edge computing solutions, machine learning algorithms, and vehicle-to-everything (V2X) communication. Computer vision processing plays a crucial role in interpreting real-time data from various sensors, including radar and lidar, to enable autonomous navigation and localization systems. Over-the-air updates ensure software remains current, while deep learning models and sensor fusion techniques enhance performance and safety. Software architecture design incorporates high-definition mapping, simulation testing environments, and GPS data integration for accurate path planning. Performance benchmarks and system verification methods are essential for ensuring functional safety standards are met. Scalable software solutions enable cybersecurity protocols to protect against potential threats, while automated driving functions rely on automated testing and validation techniques.

- For instance, a leading autonomous vehicle manufacturer implemented a modular software design, resulting in a 30% increase in development efficiency. Industry growth is expected to reach double digits, with a significant focus on advancing automated driving functions and integrating cloud computing infrastructure for data analytics platforms and camera sensor data processing.

What are the Key Data Covered in this Autonomous Cars Software Market Research and Growth Report?

-

What is the expected growth of the Autonomous Cars Software Market between 2024 and 2028?

-

USD 9.18 billion, at a CAGR of 39.04%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Proprietary software and Open-source software), Product (Level 3 autonomous cars, Level 4 autonomous cars, and Level 5 autonomous cars), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for autonomy of vehicles by OEMs, Lack of adoption of autonomous cars in developing countries

-

-

Who are the major players in the Autonomous Cars Software Market?

-

aiMotive, Alphabet Inc., Amazon.com Inc., Aptiv Plc, Aurora Innovation Inc., Baidu Inc., BlackBerry Ltd., Cohda Wireless Pty. Ltd., General Motors Co., Intel Corp., Luminar Technologies Inc., Minus Zero Robotics Pvt. Ltd., NVIDIA Corp., Oxa Autonomy Ltd., Ridecell Inc, Robert Bosch GmbH, Siemens AG, Tata Consultancy Services Ltd., Tesla Inc., and TIER IV INC.

-

Market Research Insights

- The market is a continually advancing industry, encompassing various components such as adaptive cruise control, human-machine interface (HMI), route optimization, energy efficiency algorithms, powertrain management, user experience design, parking assist systems, obstacle avoidance maneuvers, agile development methodology, software testing strategies, environmental perception, traffic flow management, data fusion algorithms, lane keeping assist, traffic sign recognition, vehicle dynamics control, pedestrian detection, trajectory planning, control algorithms, software development lifecycle, driver monitoring systems, sensor calibration methods, devops practices, decision making modules, emergency braking systems, actuator control systems, and behavior prediction models.

- According to recent reports, the market for autonomous vehicle software is projected to expand by approximately 25% yearly. For instance, a leading automaker reported a 30% increase in sales of vehicles equipped with advanced driver assistance systems (ADAS) in the last fiscal year.

We can help! Our analysts can customize this autonomous cars software market research report to meet your requirements.

RIA -

RIA -