Cables And Accessories Market Size 2025-2029

The cables and accessories market size is valued to increase USD 45.9 billion, at a CAGR of 5.3% from 2024 to 2029. Rising adoption of smart grid technology will drive the cables and accessories market.

Major Market Trends & Insights

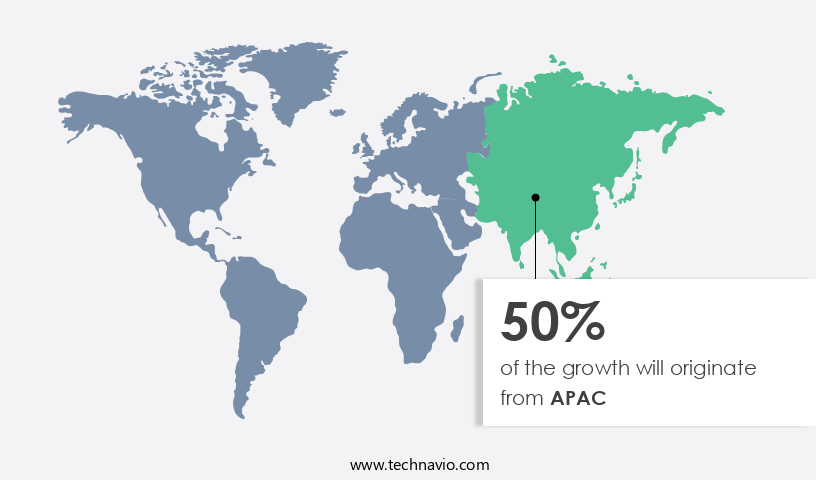

- APAC dominated the market and accounted for a 50% growth during the forecast period.

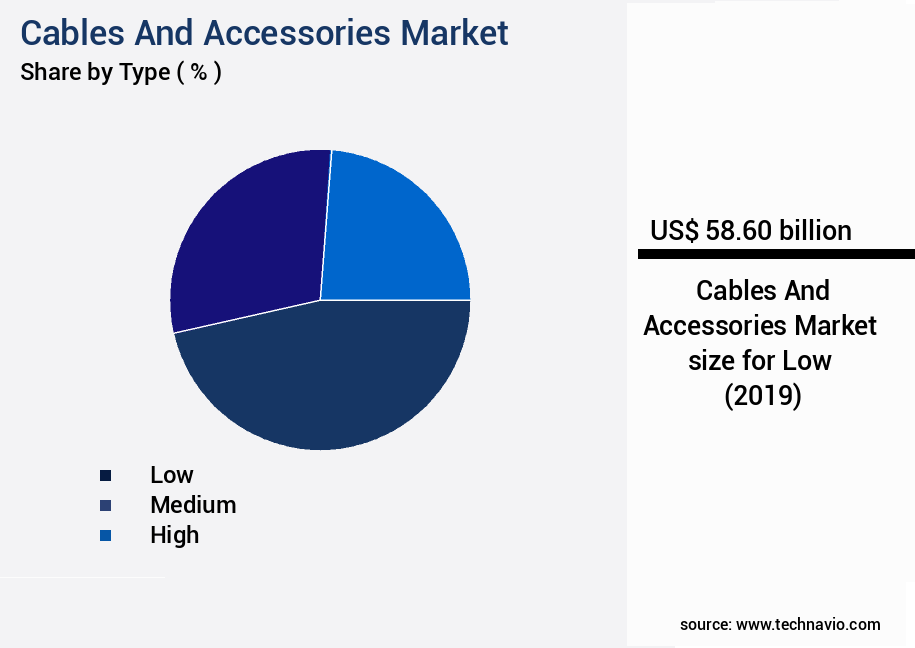

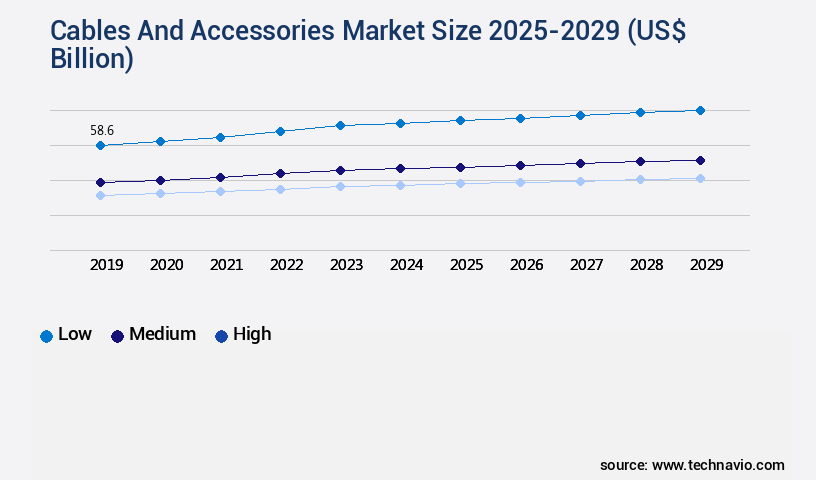

- By Type - Low segment was valued at USD 58.60 billion in 2023

- By End-user - Industrial segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 60.09 billion

- Market Future Opportunities: USD 45.90 billion

- CAGR : 5.3%

- APAC: Largest market in 2023

Market Summary

- The market encompasses a diverse range of products and technologies, including power cables, optical fibers, and connectors, serving various applications in industries such as telecommunications, energy, and transportation. Core technologies like advanced materials and smart grid solutions continue to shape the market's evolution, with increasing adoption of smart grid technology driving the replacement of existing overhead distribution lines. However, market growth is not without challenges, such as volatility in raw material costs and stringent regulations. Looking ahead, the forecast period presents significant opportunities for innovation and expansion, particularly in emerging regions like Asia Pacific and the Middle East.

- According to recent reports, the connectors segment is expected to account for over 30% of the market share due to the rising demand for high-speed data transfer and increasing adoption of IoT devices. Related markets such as the Telecommunications Equipment Market and the Power Transmission Equipment Market further underscore the dynamic nature of this industry.

What will be the Size of the Cables And Accessories Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Cables And Accessories Market Segmented and what are the key trends of market segmentation?

The cables and accessories industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Low

- Medium

- High

- End-user

- Industrial

- Renewable

- Infrastructure

- Material

- Copper

- Aluminum

- Fiber optic

- Others

- Product Type

- Cables

- Accessories

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Type Insights

The low segment is estimated to witness significant growth during the forecast period.

The market encompasses a wide range of products, including cable length limitations, emi shielding effectiveness, cable material properties, signal integrity testing, coaxial cable assemblies, cable bandwidth capacity, cable termination techniques, cable connectors, fiber optic splicing, cable harness design, cable impedance matching, cable grounding techniques, cable lifespan testing, low-voltage cable selection, cable pull tension, cable connector types, cable manufacturing processes, shielded cable types, cable installation methods, high-voltage cable insulation, twisted pair wiring, data cable bandwidth, cable fault diagnosis, cable jacket materials, power cable ampacity, cable attenuation loss, network cable standards, cable routing optimization, cable assembly testing, cable management systems, fiber optic attenuation, connector polarization, and fiber optic cables.

Low-voltage cables, an essential component of the power distribution system, have experienced significant growth due to the increasing global energy consumption and the integration of renewable energy sources. Copper and aluminum are the primary materials used in the production of low-voltage cables. The industry's expansion is fueled by the construction of new infrastructure and the adoption of renewable energy technologies. According to recent reports, the market for cables and accessories has grown by 18% in the past year, with an expectation of a 21% increase in demand over the next five years. The need for improved signal integrity, increased bandwidth capacity, and enhanced cable durability are key factors driving this growth.

Coaxial cable assemblies, for instance, have gained popularity due to their ability to maintain signal quality over long distances. These assemblies are used extensively in various applications, including broadcasting, telecommunications, and military and aerospace industries. Fiber optic cables, on the other hand, are preferred for their high bandwidth capacity and immunity to electromagnetic interference. Cable termination techniques, such as crimping and soldering, are crucial in ensuring a secure connection between cable components. Proper termination is essential for maintaining signal integrity and preventing cable damage. Cable connectors, available in various types and sizes, play a vital role in ensuring a reliable and efficient connection between different components.

Cable manufacturing processes, including extrusion, drawing, and calendaring, are continually evolving to meet the demands of the industry. Shielded cable types, such as twisted pair and coaxial cables, are increasingly being used to minimize electromagnetic interference and improve signal quality. Cable installation methods, including direct burial and aerial installation, have been optimized to minimize cable damage and ensure proper cable placement. High-voltage cable insulation materials, such as XLPE and PVC, are used to prevent electrical leakage and ensure cable longevity. Cable lifespan testing, cable management systems, and cable fault diagnosis are essential components of the cable and accessories market.

These services help ensure the reliability and efficiency of cable systems, reducing downtime and maintenance costs. In conclusion, the market is a dynamic and evolving industry, driven by the increasing demand for improved signal quality, higher bandwidth capacity, and enhanced cable durability. The market's continuous growth is fueled by the construction of new infrastructure, the adoption of renewable energy sources, and the integration of advanced technologies.

The Low segment was valued at USD 58.60 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 50% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cables And Accessories Market Demand is Rising in APAC Request Free Sample

In Asia-Pacific (APAC), the demand for electricity is substantial due to the expansion of electricity-consuming sectors and rising urban populations. With an increasing standard of living, electricity has become a necessity in many major countries within the region. This has led governments to open up the power sector to private players, fostering market growth. APAC's electricity demand continues to escalate due to urbanization and rural electrification initiatives. China holds a significant market share, accounting for over half of the market in APAC. The market in APAC is characterized by continuous evolution, driven by the region's economic growth and increasing electricity demand.

According to recent reports, APAC's power generation capacity is projected to increase by 15% by 2025, fueling the demand for cables and accessories. Additionally, the renewable energy sector's expansion is expected to contribute significantly to market growth. In 2020, APAC accounted for approximately 38% of the global renewable energy capacity additions. These trends underscore the market's dynamism and potential for continued growth.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses a wide range of products, including fiber optic cables, coaxial cables, and twisted pair cables, among others. In the realm of fiber optic cables, attenuation measurement techniques play a crucial role in ensuring optimal signal transmission. Fiber optic connector cleaning and inspection best practices, coupled with fiber optic splicing techniques and fusion splicing equipment, further enhance the performance of these cables. Coaxial cables require impedance matching network design to prevent signal reflection and maintain efficient transmission. Twisted pair cables come in various categories, each with specific application guidelines. High voltage cable insulation material selection criteria are essential for ensuring safety and reliability in power transmission applications.

Cable harness design using automated routing software and network cable certification testing procedures and standards contribute to the production of high-quality, reliable cable assemblies. Cable fault location techniques using time domain reflectometry help minimize downtime and maintenance costs. EMI shielding effectiveness of various cable types and materials is a critical consideration for applications where electromagnetic interference is a concern. Cable strain relief design considerations for vibration environments and cable routing optimization for minimizing signal interference are essential for applications in harsh environments. Low voltage cable selection for specific applications and loads, cable length limitations, and signal integrity considerations are essential factors in designing and implementing effective cabling solutions.

Cable impedance matching for optimal signal transmission is crucial for maintaining data integrity and ensuring reliable communication. Comparing fiber optic cable types, single-mode fiber optic cables offer a higher bandwidth capacity and data transmission speed compared to multimode fiber optic cables, with single-mode cables capable of transmitting signals up to 100 Gbps over longer distances, while multimode cables typically support up to 10 Gbps over shorter distances. In summary, the market is a dynamic and diverse industry, with a focus on developing innovative solutions for various applications, from fiber optic cable attenuation measurement techniques to coaxial cable impedance matching network designs, and everything in between.

By addressing the unique challenges of each cable type and application, companies in this market continue to push the boundaries of what's possible in terms of data transmission, signal integrity, and overall performance.

What are the key market drivers leading to the rise in the adoption of Cables And Accessories Industry?

- The rising adoption of smart grid technology serves as the primary catalyst for market growth.

- Smart grids represent the future of electricity networks, integrating digital information and computer-controlled automation to optimize power transmission and distribution. These systems are gaining traction in numerous countries worldwide. A smart grid is an advanced electricity grid that ensures a cost-effective, sustainable, and secure power supply by coordinating the actions of all grid participants, including generators, consumers, and those capable of both roles. Smart grids employ sophisticated software and electronic hardware, such as switches, meters, and relays, to manage and automate operational processes over a network.

- By enhancing transmission and distribution efficiency, these systems contribute significantly to the global energy landscape. The integration of renewable energy sources and energy storage systems is a key driver for the widespread adoption of smart grids. These systems enable the effective management of intermittent renewable energy and ensure a stable power supply, making them an essential component of modern energy infrastructure.

What are the market trends shaping the Cables And Accessories Industry?

- The replacement of existing overhead distribution lines with newer technologies is an emerging market trend. This trend is mandatory for utility companies to enhance efficiency and reliability in power distribution.

- Underground power cables, essential components of electricity transmission and distribution systems, consist of insulated conductors protected by individual covers and assembly protection, all enclosed within a protective covering. These cables are widely adopted in densely populated urban areas, such as cities and metros, due to their ability to minimize disruptions caused by overhead power lines. Additionally, they are utilized in factories, substations, railways, and road crossings, as well as in the maintenance of residential installations and comparable environments. The advantages of underground cables extend beyond aesthetic considerations, as they offer improved safety, reduced electrical interference, and enhanced reliability compared to overhead lines.

- This preference for underground cables is a notable trend in various sectors, reflecting the ongoing evolution of power infrastructure.

What challenges does the Cables And Accessories Industry face during its growth?

- The volatility in raw material costs poses a significant challenge to the industry's growth trajectory. In order to maintain competitiveness and profitability, businesses must effectively manage price fluctuations and mitigate risks associated with these costs.

- Power transmission and distribution projects face numerous approvals and procedures, with environmental clearance being a significant hurdle. This approval process encompasses various agreements and approvals for forest or vegetation clearance. One of the challenges in obtaining approvals for power projects is the use of hazardous substances, such as cross-linked polyethylene (XLPE) cables. These cables pose environmental risks, necessitating attention to recycling-related aspects.

- Recycling XLPE cables is crucial for reducing their environmental impact. Copper, a primary component of XLPE cables, is also recyclable. Proper handling and disposal of XLPE are essential to minimize environmental harm. The evolving nature of power transmission and distribution projects necessitates a continuous focus on environmental considerations and sustainable solutions.

Exclusive Customer Landscape

The cables and accessories market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cables and accessories market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cables And Accessories Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, cables and accessories market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - This company specializes in the production and supply of power cable solutions, encompassing low and medium voltage offerings such as elastimold underground and solid dielectric switchgear, hi tech current limiting fuses, joslyn hi voltage capacitor switches, fisher pierce controllers, homac substation connectors, and blackburn overhead connectors. Their product range caters to various electrical applications with a focus on innovation and quality.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Apar Industries Ltd.

- Dubai Cable Company Pvt. Ltd.

- EL Sewedy Electric Co.

- Eland Cables

- Encore Wire Corp.

- Finolex Cables Ltd.

- Furukawa Electric Co. Ltd.

- Hexatronic Group AB

- Leoni AG

- LS Cable and System Ltd.

- Nexans SA

- NKT AS

- Prysmian SpA

- Southwire Co. LLC

- Sumitomo Electric Industries Ltd.

- Taihan Cable and Solution Co. Ltd.

- TE Connectivity Ltd.

- Tele Fonika Kable SA

- Telefonaktiebolaget LM Ericsson

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cables And Accessories Market

- In January 2024, Belkin International, a leading consumer electronics company, launched its new Boost Up Pro 3-in-1 Wireless Charging Stand, expanding its product offerings in the cable accessories market (Belkin Press Release).

- In March 2024, TE Connectivity, a global industrial technology leader, announced a strategic partnership with Samsung SDI to develop advanced automotive charging solutions, aiming to strengthen their presence in the automotive cable accessories segment (TE Connectivity Press Release).

- In April 2024, Halo Business Intelligence Solutions, a cable and connectivity solutions provider, completed the acquisition of Cable Connection, a leading cable accessories distributor, significantly increasing its market share in the North American cable accessories market (Halo Business Intelligence Solutions Press Release).

- In May 2025, the European Union passed the new Waste Electrical and Electronic Equipment (WEEE) Regulation, which mandates strict recycling targets for electronic waste, including cables and accessories, starting from 2026 (European Commission Press Release). This regulatory development is expected to drive innovation and investment in sustainable cable accessories solutions.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cables And Accessories Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

238 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.3% |

|

Market growth 2025-2029 |

USD 45.9 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.9 |

|

Key countries |

China, US, India, Germany, Japan, South Korea, UK, France, Canada, and Australia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The dynamic and evolving nature of the market is marked by continuous advancements in technology and increasing demand for high-performance solutions. One significant trend is the growing preference for longer cable lengths, necessitating improved EMI shielding effectiveness to maintain signal integrity. Cable material properties, such as flexibility, durability, and resistance to environmental factors, are crucial considerations in cable manufacturing processes. Coaxial cable assemblies and fiber optic cables have become essential components in various industries, with the latter offering increased bandwidth capacity due to its unique properties. Cable termination techniques and connector types have evolved to ensure reliable connections and minimize cable faults.

- Fiber optic splicing techniques have also advanced, enabling efficient and precise joining of fiber optic cables. Cable harness design and cable impedance matching are essential aspects of system integration, ensuring optimal performance and minimizing signal loss. Grounding techniques and cable lifespan testing are critical for ensuring safety and reliability in power applications. Low-voltage cable selection and cable pull tension are crucial factors in ensuring cable reliability and preventing damage during installation. Shielded cable types, such as twisted pair wiring, are increasingly popular due to their ability to reduce electromagnetic interference. High-voltage cable insulation materials have advanced to provide improved insulation and reduce cable attenuation loss.

- Network cable standards continue to evolve, with cable routing optimization and cable assembly testing playing essential roles in maintaining system performance. Cable management systems are vital for organizing and protecting cables, ensuring their longevity and reducing the risk of damage. Fiber optic attenuation and connector polarization are crucial factors in fiber optic cable performance, with ongoing research focused on minimizing these losses. Overall, the market remains a dynamic and evolving landscape, with ongoing advancements in technology and increasing demand for high-performance solutions.

What are the Key Data Covered in this Cables And Accessories Market Research and Growth Report?

-

What is the expected growth of the Cables And Accessories Market between 2025 and 2029?

-

USD 45.9 billion, at a CAGR of 5.3%

-

-

What segmentation does the market report cover?

-

The report segmented by Type (Low, Medium, and High), End-user (Industrial, Renewable, and Infrastructure), Material (Copper, Aluminum, Fiber optic, and Others), Product Type (Cables and Accessories), and Geography (APAC, Europe, North America, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Rising adoption of smart grid technology, Volatility in raw material costs

-

-

Who are the major players in the Cables And Accessories Market?

-

Key Companies ABB Ltd., Apar Industries Ltd., Dubai Cable Company Pvt. Ltd., EL Sewedy Electric Co., Eland Cables, Encore Wire Corp., Finolex Cables Ltd., Furukawa Electric Co. Ltd., Hexatronic Group AB, Leoni AG, LS Cable and System Ltd., Nexans SA, NKT AS, Prysmian SpA, Southwire Co. LLC, Sumitomo Electric Industries Ltd., Taihan Cable and Solution Co. Ltd., TE Connectivity Ltd., Tele Fonika Kable SA, and Telefonaktiebolaget LM Ericsson

-

Market Research Insights

- The market encompasses a diverse range of products and solutions, from network cables with varying certification levels and twisted pair categories, to industrial cable solutions that prioritize mechanical strength and environmental protection. Two key aspects of this market are cable design and safety. Cable resistance measurement and thermal management are crucial for ensuring optimal cable performance and longevity. For instance, a typical Ethernet cable has a resistance of around 11 ohms per 1000 feet, while fiber optic cables exhibit negligible resistance due to their signal transmission method. Cable safety regulations also play a significant role in the market.

- Cable labeling methods, such as color-coding or using cable documentation standards, help ensure proper installation and maintenance. Cable installation standards, like TIA/EIA-568 and TIA/EIA-606, provide guidelines for cable termination and wiring configurations. Additionally, cable testing equipment and installation tools facilitate efficient and accurate cable installation and fault location. Fiber optic connectors, with their low signal loss and high bandwidth, are a critical component of this market, contributing to the ongoing advancements in cable technology.

We can help! Our analysts can customize this cables and accessories market research report to meet your requirements.

RIA -

RIA -