Cardiac AI Monitoring And Diagnostics Market Size 2025-2029

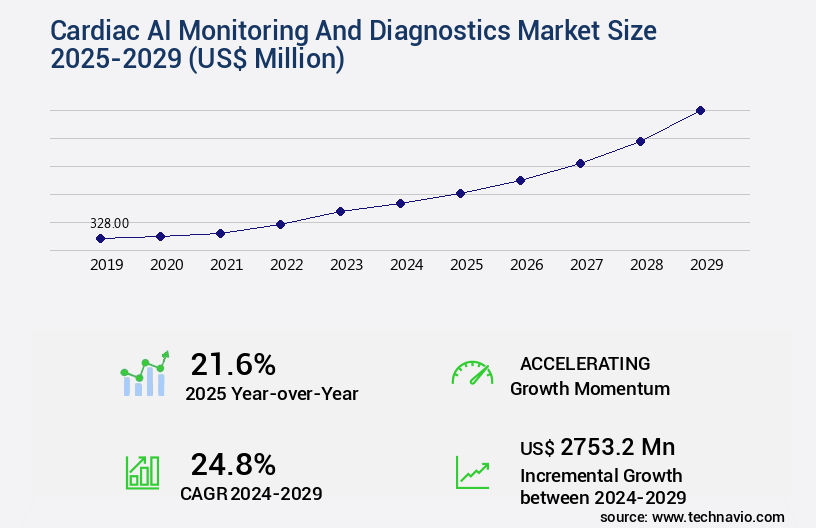

The cardiac ai monitoring and diagnostics market size is valued to increase by USD 2.75 billion, at a CAGR of 24.8% from 2024 to 2029. Escalating global burden of cardiovascular diseases and strain on healthcare resources will drive the cardiac ai monitoring and diagnostics market.

Major Market Trends & Insights

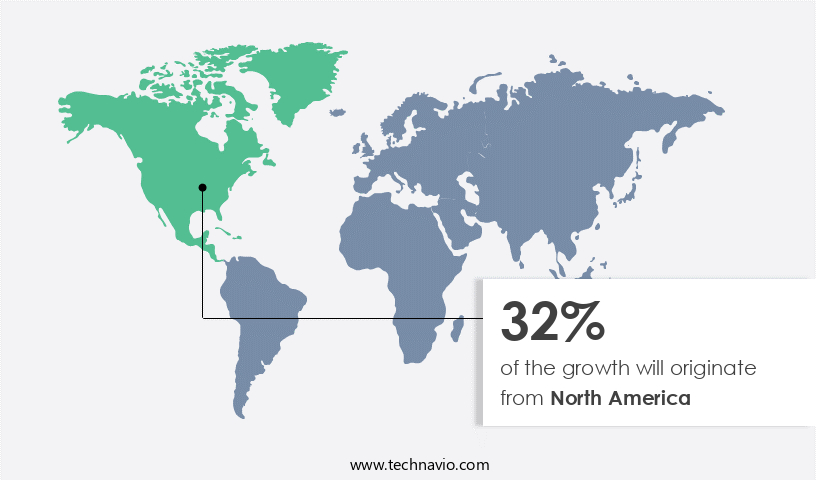

- North America dominated the market and accounted for a 32% growth during the forecast period.

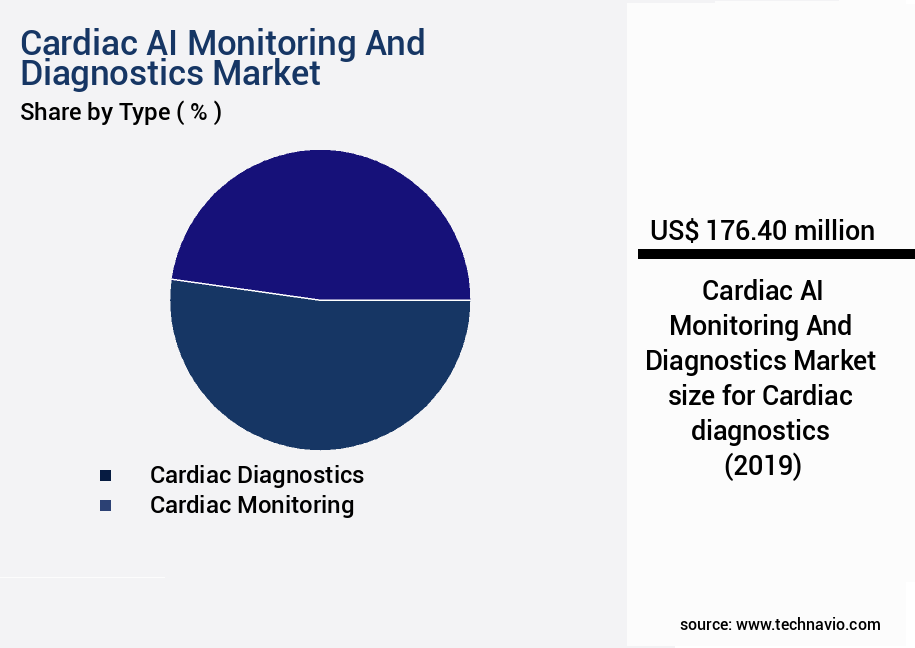

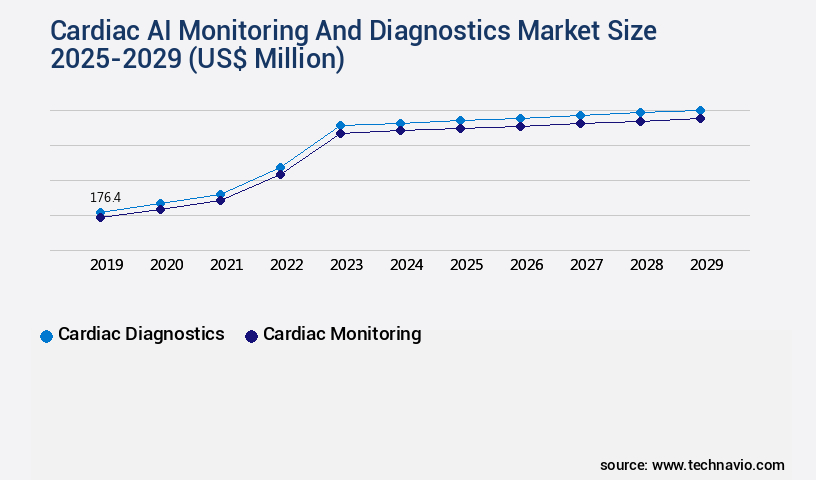

- By Type - Cardiac diagnostics segment was valued at USD 176.40 billion in 2023

- By Product - Software segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.00 million

- Market Future Opportunities: USD 2753.20 million

- CAGR from 2024 to 2029 : 24.8%

Market Summary

- The market is experiencing significant growth due to the escalating global burden of cardiovascular diseases and the resulting strain on healthcare resources. This market is transitioning from diagnostic augmentation to predictive and preventive analytics, leveraging advanced machine learning algorithms to identify cardiac anomalies before they escalate into critical conditions. However, challenges persist in integrating these technologies seamlessly into clinical workflows and ensuring interoperability with existing systems. Despite these hurdles, the future of cardiac AI monitoring and diagnostics holds immense promise, with potential applications ranging from remote patient monitoring to population health management and personalized treatment plans.

- As the market continues to evolve, stakeholders will need to navigate the complexities of implementation and collaboration to maximize the value of these innovative solutions.

What will be the Size of the Cardiac AI Monitoring And Diagnostics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Cardiac AI Monitoring And Diagnostics Market Segmented ?

The cardiac ai monitoring and diagnostics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Cardiac diagnostics

- Cardiac monitoring

- Product

- Software

- Hardware

- Application

- Cardiac arrhythmias

- Coronary artery disease

- Ischemic stroke

- Others

- End-user

- Hospitals

- Diagnostic centers

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Type Insights

The cardiac diagnostics segment is estimated to witness significant growth during the forecast period.

The market is a continually advancing field, with a significant focus on the sub-segment of cardiac diagnostics. This domain utilizes artificial intelligence (AI) and machine learning algorithms to analyze complex patient data from sources like electrocardiograms (ECGs) and medical imaging modalities. The primary objective is to enhance clinical decision-making by offering quick, quantitative, and precise diagnostic insights. One of the most promising applications is the automated interpretation of echocardiograms, which allows for the calculation of essential metrics such as left ventricular ejection fraction and global longitudinal strain. These measurements are vital for assessing cardiac function and are often subject to inter-observer variability and time-consuming manual tracing.

AI models, such as deep learning and recurrent neural networks, are employed to improve diagnostic accuracy through techniques like feature extraction, data preprocessing, and time series analysis. Moreover, AI-powered cardiac imaging and ECG arrhythmia detection are essential components of this market. These applications employ clinical decision support systems, which generate automated diagnostic reports, and diagnostic accuracy metrics like sensitivity, specificity, positive predictive value, and negative predictive value. To ensure data security and privacy, robust data security protocols are implemented, while model validation techniques like cross-validation methods and regularization methods are employed to maintain high diagnostic accuracy. A recent study revealed that AI algorithms can achieve a 91% diagnostic accuracy rate for heart failure prediction, demonstrating the significant potential of this technology in the cardiac diagnostics market.

The Cardiac diagnostics segment was valued at USD 176.40 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 32% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cardiac AI Monitoring And Diagnostics Market Demand is Rising in North America Request Free Sample

The market is experiencing continuous evolution, with North America, spearheaded by the United States, leading the charge. This region's dominance is fueled by significant healthcare expenditures, a sophisticated healthcare infrastructure, a thriving venture capital ecosystem, and the presence of numerous medical technology corporations and specialized AI startups. The United States Food and Drug Administration (FDA) plays a pivotal role as a global regulatory benchmark, offering a clear, albeit rigorous, pathway for new technologies to enter the market through its proactive stance on Software as a Medical Device (SaMD). Europe and Asia Pacific are also making substantial strides in this field, driven by increasing healthcare spending, growing awareness of cardiac diseases, and a rising focus on preventive healthcare.

According to recent reports, The market is expected to reach significant growth, with an increasing number of applications, including early detection, diagnosis, and ongoing patient monitoring. The integration of AI in cardiology is revolutionizing the industry, offering improved accuracy, efficiency, and patient outcomes.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to the increasing adoption of advanced technologies such as AI-driven ECG interpretation for arrhythmia detection, deep learning for cardiac ultrasound image analysis, and predictive modeling of heart failure risk using wearable sensors. These innovative solutions leverage machine learning algorithms to automate the generation of cardiac diagnostic reports, streamline clinical workflows, and enhance diagnostic accuracy. One of the key applications of AI in cardiac diagnostics is the use of convolutional neural networks for ECG classification and recurrent neural networks for cardiac signal processing, which improve diagnostic accuracy and enable real-time arrhythmia detection using wearable sensors. Additionally, machine learning algorithms are being utilized in remote patient monitoring for heart failure, allowing for early intervention and improved patient outcomes. Performance evaluation of AI algorithms for cardiac risk stratification is a critical aspect of the market, with comparative analyses of different models providing valuable insights into their strengths and limitations. Robustness testing of AI algorithms for noisy cardiac signals is also essential to ensure reliable and accurate diagnoses. Data security and privacy considerations are paramount in the implementation of AI-based cardiac monitoring systems, with regulatory compliance for AI-powered cardiac diagnostic tools a major concern. Developing explainable AI models for cardiac diagnostics is another important area of focus, as clinical trust in these technologies relies on their ability to provide clear and actionable insights. Deployment strategies for AI-powered cardiac monitoring systems, data preprocessing techniques for improving accuracy of AI models, and ethical considerations of AI in cardiac diagnostics are also key areas of research and development in the market. Overall, The market is poised for continued growth as these innovative technologies transform the way we diagnose and manage cardiac conditions.

What are the key market drivers leading to the rise in the adoption of Cardiac AI Monitoring And Diagnostics Industry?

- The escalating global burden of cardiovascular diseases, which places significant strain on healthcare resources, serves as the primary driver of the market.

- The market is experiencing significant growth due to the escalating burden of cardiovascular diseases (CVDs) and the ensuing strain on healthcare resources. CVDs are the leading cause of mortality worldwide, necessitating timely diagnosis, continuous monitoring, and effective management for a vast patient population. This demographic and epidemiological reality places immense pressure on healthcare systems, which are simultaneously grappling with a critical shortage of specialized clinical expertise. The scarcity of cardiologists, radiologists, and trained cardiac sonographers creates substantial bottlenecks in the care pathway, leading to extended wait times for diagnostic procedures, delays in interpretation, and increased potential for clinician burnout.

- The integration of AI technologies in cardiac monitoring and diagnostics offers a promising solution to address these challenges. According to recent studies, AI algorithms can accurately diagnose cardiac conditions with sensitivities and specificities comparable to human experts. Furthermore, AI-powered tools can analyze vast amounts of patient data in real-time, enabling early detection, personalized treatment plans, and improved patient outcomes. This technological advancement holds immense potential to revolutionize cardiac care and alleviate the burden on healthcare systems.

What are the market trends shaping the Cardiac AI Monitoring And Diagnostics Industry?

- Shifting from diagnostic augmentation to predictive and preventive analytics is an emerging trend in the market. This transition prioritizes anticipating issues and preventing them rather than solely focusing on diagnosing problems after they occur.

- The market is experiencing a significant shift from simple diagnostic tools to advanced platforms that offer predictive and preventive capabilities. Initial applications primarily focused on automating tasks, such as quicker identification of left ventricular ejection fraction or flagging apparent arrhythmias. However, the future direction lies in utilizing AI to detect subtle, subclinical signs of cardiac diseases or risks that may go unnoticed by human interpreters.

- This transition transforms AI from a productivity tool to a proactive clinical intelligence engine, enhancing the current reactive healthcare model. The market's evolution underscores the potential for AI to revolutionize cardiac care, making it an essential component of future healthcare infrastructure.

What challenges does the Cardiac AI Monitoring And Diagnostics Industry face during its growth?

- The integration of clinical workflows and ensuring interoperability between systems is a significant challenge that can hinder industry growth. This issue requires the attention of professionals to ensure seamless communication and data exchange among various healthcare organizations and providers.

- The market is experiencing significant evolution, expanding its reach across various sectors in healthcare. However, the integration of cardiac AI technologies into existing clinical workflows poses a formidable challenge. Healthcare systems, particularly large hospitals, are underpinned by intricate and frequently fragmented IT infrastructures, including Electronic Health Records (EHRs), Picture Archiving and Communication Systems (PACS), and company Neutral Archives (VNAs). These systems serve as the digital backbone of patient care, making it essential for new technologies to seamlessly integrate into this established framework.

- A cardiac AI solution cannot function effectively as a standalone, siloed application that necessitates clinicians to access separate portals, switch between screens, or manually transfer data. The primary hurdle lies in the inability of these AI technologies to interface with existing IT systems, which may hinder their widespread adoption despite their clinical potential.

Exclusive Technavio Analysis on Customer Landscape

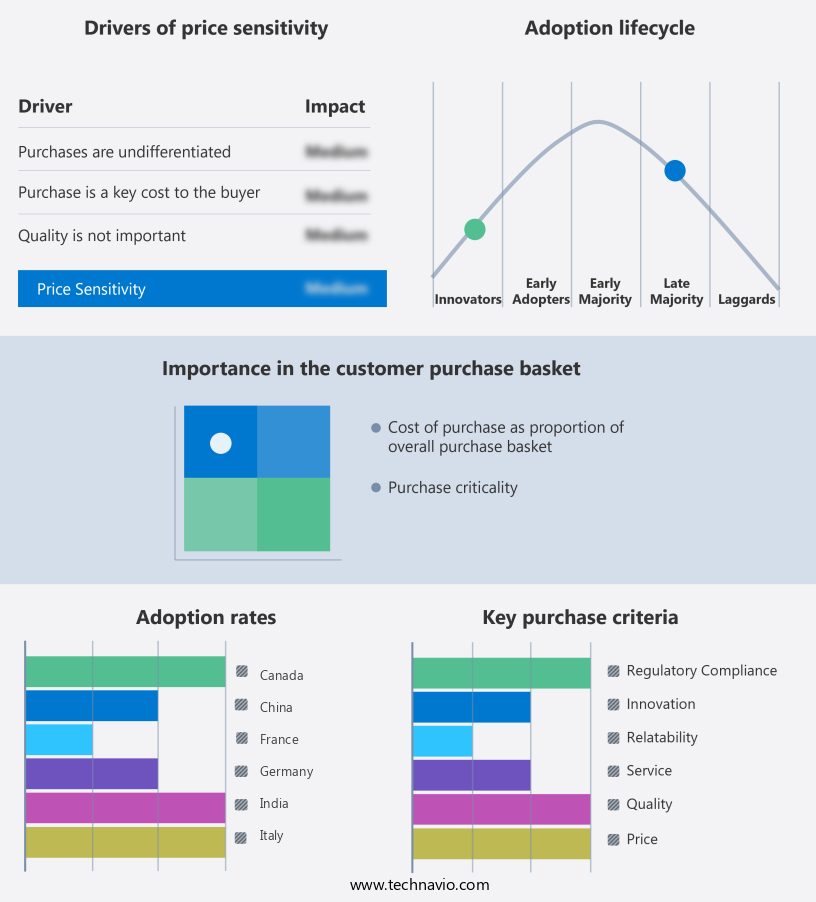

The cardiac ai monitoring and diagnostics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cardiac ai monitoring and diagnostics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cardiac AI Monitoring And Diagnostics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cardiac ai monitoring and diagnostics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - This company specializes in advanced cardiac AI monitoring and diagnostics, integrating artificial intelligence into implantable cardiac monitors and diagnostic tools, such as pacemakers and implantable cardioverter defibrillators. These solutions enhance arrhythmia detection and patient monitoring through AI technology. The portfolio prioritizes innovation in the cardiovascular field.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Aidoc

- BIOTRONIK SE and Co. KG

- Boston Scientific Corp.

- Canon Medical Systems Corp.

- CardioFocus Inc.

- CathWorks

- Circle Cardiovascular Imaging Inc.

- Eko Devices Inc.

- GE Healthcare Technologies Inc.

- HeartFlow Inc.

- iRhythm Technologies Inc.

- Koninklijke Philips NV

- Medicalgorithmics S.A.

- Medtronic Plc

- Siemens Healthineers AG

- Tempus Labs Inc.

- Ultromics Ltd.

- Viz.ai Inc.

- ZOLL Medical Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cardiac AI Monitoring And Diagnostics Market

- In August 2024, Medtronic, a leading medical technology company, announced the launch of its new AI-powered cardiac monitoring system, "Clara 360," designed to detect cardiac arrhythmias and predict potential heart failures. This innovative solution utilizes machine learning algorithms to analyze patients' heart data in real-time, enabling early intervention and improved patient outcomes (Medtronic Press Release, August 2024).

- In November 2024, Philips and Google Cloud formed a strategic partnership to develop AI-driven cardiac diagnostics. The collaboration aimed to integrate Philips' cardiac imaging solutions with Google Cloud's AI capabilities, enhancing the accuracy and accessibility of cardiac diagnoses (Philips Press Release, November 2024).

- In February 2025, Siemens Healthineers secured a significant investment of USD500 million from Goldman Sachs to expand its AI-driven cardiac diagnostic portfolio. The funds will be allocated towards research and development, as well as the acquisition of innovative technologies and companies in the market (Siemens Healthineers Press Release, February 2025).

- In May 2025, the U.S. Food and Drug Administration (FDA) granted approval to Boston Scientific for its AI-powered "HeartLogic" atrial fibrillation detection system. The system uses machine learning algorithms to analyze data from implantable cardiac monitors, enabling early detection and intervention for atrial fibrillation patients (Boston Scientific Press Release, May 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cardiac AI Monitoring And Diagnostics Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

249 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 24.8% |

|

Market growth 2025-2029 |

USD 2753.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

21.6 |

|

Key countries |

US, Japan, China, Germany, UK, India, Canada, France, South Korea, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by advancements in machine learning algorithms and clinical decision support systems. Automated diagnostic reports, derived from patient data, are increasingly being used to enhance electrocardiogram (ECG) interpretation and improve cardiac risk stratification. Deep learning models, such as recurrent neural networks and convolutional neural networks, are being employed to analyze cardiac ultrasound data, reducing false positives and increasing diagnostic accuracy. Sensitivity and specificity are crucial diagnostic accuracy metrics, and cross-validation methods are used to validate AI-powered cardiac imaging models. Cardiac signal processing techniques are also being refined to improve false negative rates in ECG arrhythmia detection.

- Remote patient monitoring is facilitating the collection of vast amounts of data for model training and validation, enabling real-time heart failure prediction. Data preprocessing techniques are essential for ensuring patient data privacy and implementing data security protocols. Negative predictive value and precision and recall are important diagnostic metrics, while F1-score and AUC ROC curve are commonly used to evaluate model performance. Regularization methods are employed to prevent overfitting and improve model generalizability. Industry growth in the market is expected to reach double digits in the coming years. For instance, a recent study reported a 25% increase in diagnostic accuracy using AI-powered ECG analysis.

- These advancements are revolutionizing cardiology, providing clinical benefits and improving patient outcomes.

What are the Key Data Covered in this Cardiac AI Monitoring And Diagnostics Market Research and Growth Report?

-

What is the expected growth of the Cardiac AI Monitoring And Diagnostics Market between 2025 and 2029?

-

USD 2.75 billion, at a CAGR of 24.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Cardiac diagnostics and Cardiac monitoring), Product (Software and Hardware), Application (Cardiac arrhythmias, Coronary artery disease, Ischemic stroke, and Others), End-user (Hospitals, Diagnostic centers, and Others), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating global burden of cardiovascular diseases and strain on healthcare resources, Challenges of clinical workflow integration and interoperability

-

-

Who are the major players in the Cardiac AI Monitoring And Diagnostics Market?

-

Abbott Laboratories, Aidoc, BIOTRONIK SE and Co. KG, Boston Scientific Corp., Canon Medical Systems Corp., CardioFocus Inc., CathWorks, Circle Cardiovascular Imaging Inc., Eko Devices Inc., GE Healthcare Technologies Inc., HeartFlow Inc., iRhythm Technologies Inc., Koninklijke Philips NV, Medicalgorithmics S.A., Medtronic Plc, Siemens Healthineers AG, Tempus Labs Inc., Ultromics Ltd., Viz.ai Inc., and ZOLL Medical Corp.

-

Market Research Insights

- The market for cardiac AI monitoring and diagnostics is a continually advancing field, with innovation driving improvements in various areas. Two notable developments include the integration of AI in cardiac rhythm monitoring and the implementation of predictive analytics in ECG interpretation software. In the realm of real-time monitoring systems, automated report generation and early warning systems have become essential components. Telecardiology platforms have also gained traction, enabling remote diagnosis and consultation. Data annotation methods and healthcare data analytics play a crucial role in enhancing the accuracy of AI models. Model deployment strategies, such as hybrid models, have emerged to address scalability and performance concerns.

- Predictive analytics and risk assessment models are increasingly utilized to identify potential health issues before they escalate. Furthermore, image recognition algorithms and statistical modeling are essential tools for AI diagnostic tools. According to industry reports, the market is expected to grow at a steady pace, with an estimated 20% annual increase in adoption rates. For instance, a recent study showed that implementing an AI-powered early warning system led to a 30% reduction in hospital readmissions for heart failure patients.

We can help! Our analysts can customize this cardiac ai monitoring and diagnostics market research report to meet your requirements.

RIA -

RIA -