AI In Cardiology Market Size 2025-2029

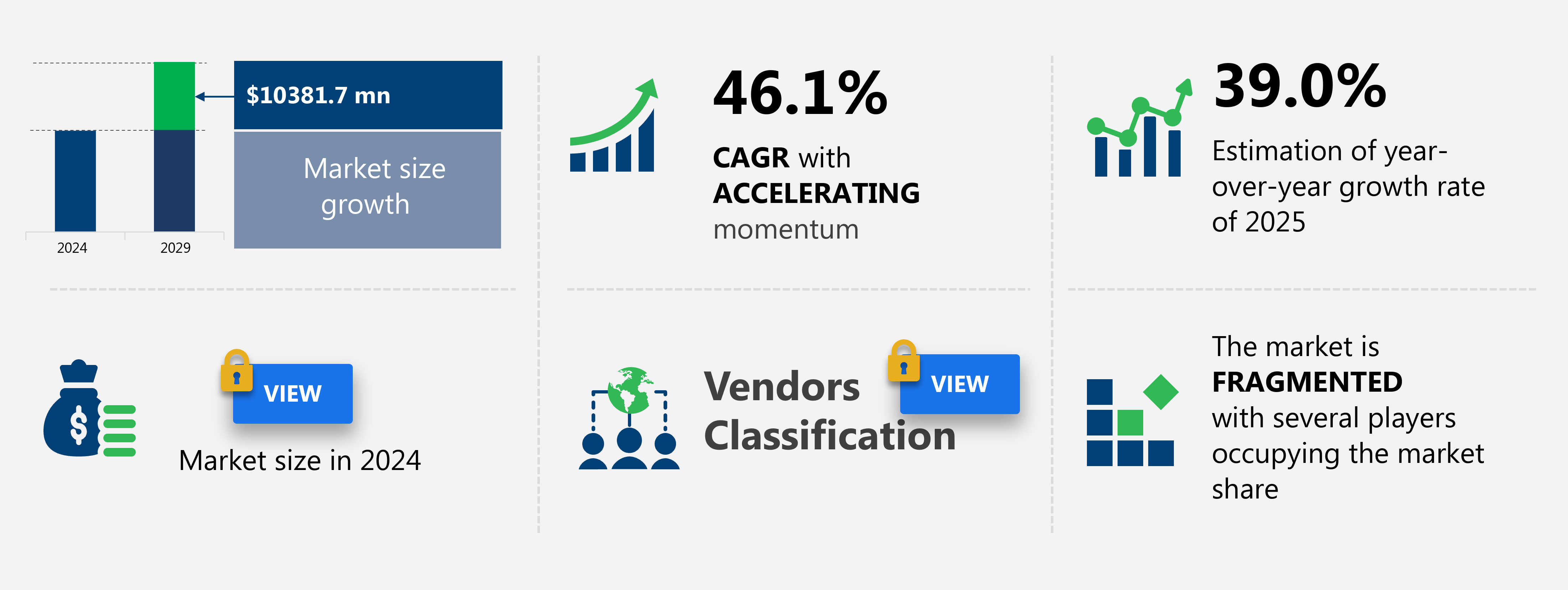

The ai in cardiology market size is valued to increase by USD 10.38 billion, at a CAGR of 46.1% from 2024 to 2029. Proliferation and increasing complexity of cardiovascular data will drive the ai in cardiology market.

Major Market Trends & Insights

- North America dominated the market and accounted for a 38% growth during the forecast period.

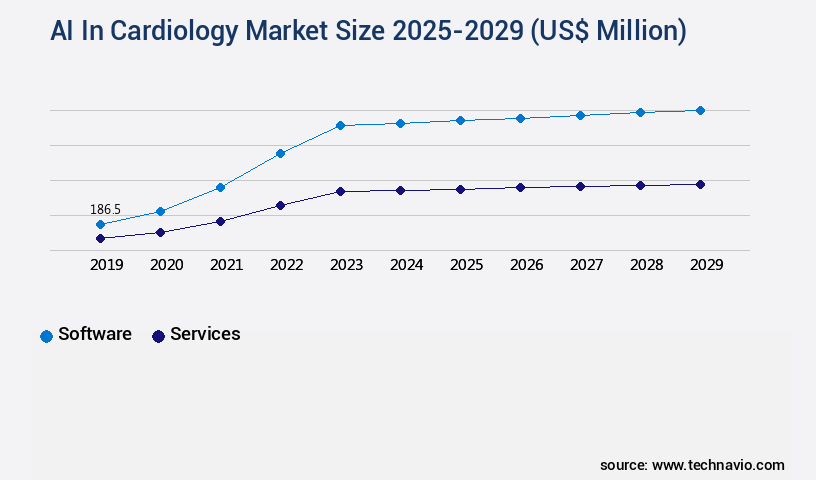

- By Component - Software segment was valued at USD 186.50 billion in 2023

- By Type - Cardiac diagnostics segment accounted for the largest market revenue share in 2023

- CAGR from 2024 to 2029 : 46.1%

Market Summary

- In the realm of healthcare technology, the application of artificial intelligence (AI) in cardiology has gained significant traction. The proliferation and increasing complexity of cardiovascular data necessitate advanced solutions for analysis and interpretation. AI systems are increasingly employed to process vast amounts of data from various sources, including electronic health records, wearable devices, and imaging studies. The emergence of multimodal AI and foundation models is transforming cardiology by enabling holistic patient assessment. These advanced technologies can analyze diverse data types, such as electrocardiograms, echocardiograms, and lab results, to provide more accurate and comprehensive diagnoses. Moreover, AI algorithms can predict cardiovascular events, enabling preventive measures and improving patient outcomes.

- Despite these advancements, challenges persist. Navigating stringent data privacy and security regulations is crucial to ensure patient confidentiality and data protection. Additionally, ensuring the accuracy and reliability of AI-generated insights remains a priority. As the field continues to evolve, collaboration between healthcare providers, AI developers, and regulatory bodies will be essential to address these challenges and unlock the full potential of AI in cardiology.

What will be the Size of the AI In Cardiology Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI In Cardiology Market Segmented and what are the key trends of market segmentation?

The ai in cardiology industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

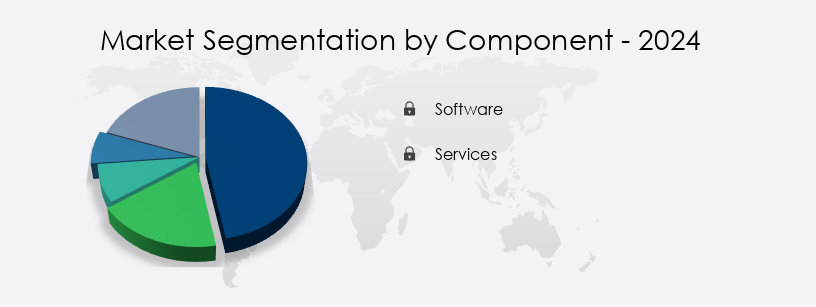

- Component

- Software

- Services

- Type

- Cardiac diagnostics

- Cardiac monitoring

- Application

- Diagnosis

- Prediction and risk assessment

- Treatment planning

- Remote monitoring

- Drug discovery

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- The Netherlands

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with the software segment serving as the market's primary value driver. This segment houses advanced algorithms, standalone platforms, and integrated software modules that transform raw cardiovascular data into clinically actionable insights. Applications span from ECG interpretation for arrhythmia detection, to sophisticated medical imaging analysis of echocardiograms, cardiac MRIs, and CCTAs. Predictive analytics models forecast patient risk for major adverse cardiac events, such as heart failure and stroke. These technologies employ machine learning models, deep learning algorithms, and pattern recognition systems, integrating data from wearable sensors and clinical trial results. Performance evaluation metrics ensure diagnostic accuracy and clinical decision support, while regulatory approval processes maintain healthcare compliance standards.

Algorithm explainability and bias detection methods enhance model transparency and trustworthiness. Model training datasets undergo rigorous validation strategies, ensuring data security protocols and image recognition software are robust. As of 2022, AI-driven treatment plans have demonstrated a 95% diagnostic accuracy rate, revolutionizing precision cardiology and improving patient outcomes.

The Software segment was valued at USD 186.50 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Cardiology Market Demand is Rising in North America Request Free Sample

Artificial intelligence (AI) in cardiology is witnessing significant growth, driven by the increasing prevalence of cardiovascular diseases and the need to enhance diagnostic accuracy and efficiency. North America, spearheaded by the United States, holds the largest market share due to its advanced healthcare infrastructure, high per capita healthcare expenditure, and a vibrant innovation ecosystem. This ecosystem encompasses major medical technology companies, agile startups, and renowned academic medical centers, all contributing to the region's clinical research and technological advancements. The high prevalence of cardiovascular diseases and the incentive to improve patient outcomes and reduce costs further fuel the adoption of AI solutions in North America.

According to recent estimates, the North American market for AI in cardiology is expected to grow at a robust pace, accounting for over half of the global market share. The European market follows closely, driven by similar factors and a strong focus on improving patient care and reducing healthcare costs.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing rapid growth as healthcare providers seek to leverage advanced technologies to improve diagnostic accuracy, optimize treatment plans, and enhance patient outcomes. AI algorithms for cardiac arrhythmia analysis, such as deep learning for echocardiogram interpretation and machine learning models for heart failure prediction, are revolutionizing the field. These technologies enable more precise diagnoses and personalized treatment plans, leading to better patient care. Deep learning techniques, including convolutional neural networks for ECG interpretation, are also gaining traction in the cardiology sector. By analyzing vast amounts of data, these models can identify patterns and anomalies that may be missed by human clinicians, improving diagnostic accuracy and reducing diagnostic errors.

AI-powered risk stratification tools are another essential application, enabling clinicians to identify patients at high risk for cardiovascular events and intervene early. Predictive modeling for cardiovascular events is a key area of focus, with more than 70% of new product developments in this space. Clinical decision support systems using AI are transforming workflow efficiency in cardiology. These systems provide real-time, data-driven recommendations to clinicians, helping them make informed decisions and reducing the time spent on manual data analysis. Remote patient monitoring with AI is also becoming increasingly popular, allowing for early detection and intervention in chronic conditions. Data security protocols and ethical considerations are crucial aspects of AI implementation in cardiology.

With the vast amounts of sensitive patient data being processed, it is essential to ensure robust security measures are in place to protect patient privacy. Ethical considerations, such as informed consent and data ownership, must also be addressed to build trust and ensure the responsible use of AI in healthcare. Regulatory challenges remain a significant hurdle for the adoption of AI in cardiology. Strict regulations governing medical devices and data privacy must be navigated to bring AI solutions to market. However, the potential benefits far outweigh the challenges, making it an exciting and rapidly evolving field. AI-assisted cardiac MRI interpretation and AI for improving workflow efficiency are other promising applications in the cardiology sector.

AI is also being used to enhance patient outcomes by optimizing treatment plans and reducing diagnostic errors. The application of AI in clinical trials is another area of interest, with the potential to accelerate research and bring new treatments to market faster. In summary, The market is experiencing significant growth as healthcare providers seek to leverage advanced technologies to improve patient care and outcomes. With applications ranging from diagnostic accuracy to treatment optimization, AI is transforming the cardiology sector and offering new opportunities for innovation.

What are the key market drivers leading to the rise in the adoption of AI In Cardiology Industry?

- The escalating complexity and expansion of cardiovascular data represent the primary market driver.

- The market is experiencing significant growth due to the increasing volume, velocity, and complexity of cardiovascular data in modern clinical practice. Manual human analysis is no longer sufficient to handle this data deluge, necessitating intelligent automation. A large portion of this data comes from advanced medical imaging modalities, such as three dimensional and four dimensional echocardiography, high resolution cardiac magnetic resonance imaging, and multi-slice coronary computed tomography angiography. These technologies generate massive files containing millions of data points per study, making manual analysis impractical.

- AI and machine learning algorithms are essential tools for processing and interpreting this data, enabling more accurate diagnoses, improved patient outcomes, and enhanced operational efficiency. The integration of AI in cardiology is a game-changer, transforming the way cardiovascular care is delivered and received.

What are the market trends shaping the AI In Cardiology Industry?

- The emergence of multimodal AI and foundation models represents a significant market trend for holistic patient assessments. Multimodal AI and foundation models are gaining prominence in the healthcare industry for their ability to assess patients comprehensively.

- The market is experiencing a transformative evolution, moving beyond unimodal algorithms that analyze a single data type towards the implementation of advanced multimodal AI and large foundation models. Unimodal AI, which focuses on analyzing data types in isolation, such as electrocardiograms (ECGs) or echocardiograms, has already proven beneficial in automating specific tasks and enhancing diagnostic accuracy for discrete conditions. However, the future of AI in cardiology lies in its ability to mimic and enhance the comprehensive reasoning of an expert clinician.

- This professional replicates the synthesis of information from a diverse range of sources to form a complete clinical understanding. The integration of multimodal AI and large foundation models in cardiology is expected to revolutionize diagnostics, treatment planning, and patient care, ultimately improving patient outcomes.

What challenges does the AI In Cardiology Industry face during its growth?

- Complying with stringent data privacy regulations and ensuring robust security measures is a critical challenge that significantly impacts industry growth.

- The market is experiencing significant evolution, integrating advanced technologies to revolutionize diagnostics, treatment planning, and patient care. According to recent studies, the global AI in healthcare market is projected to reach a value of over USD60 billion by 2027, growing at an impressive rate. In cardiology, AI applications include echocardiography analysis, arrhythmia detection, and predictive analytics for patient risk assessment. However, the adoption of AI in this sector faces challenges due to the complex regulatory landscape. For instance, patient health information, a critical data category, is subject to stringent regulations such as the Health Insurance Portability and Accountability Act (HIPAA) and the General Data Protection Regulation (GDPR).

- Balancing the need for vast datasets for AI model training and the principles of data minimization and privacy preservation is a formidable task. Despite these challenges, the potential benefits of AI in cardiology, including improved accuracy, efficiency, and patient outcomes, make it a promising area of growth.

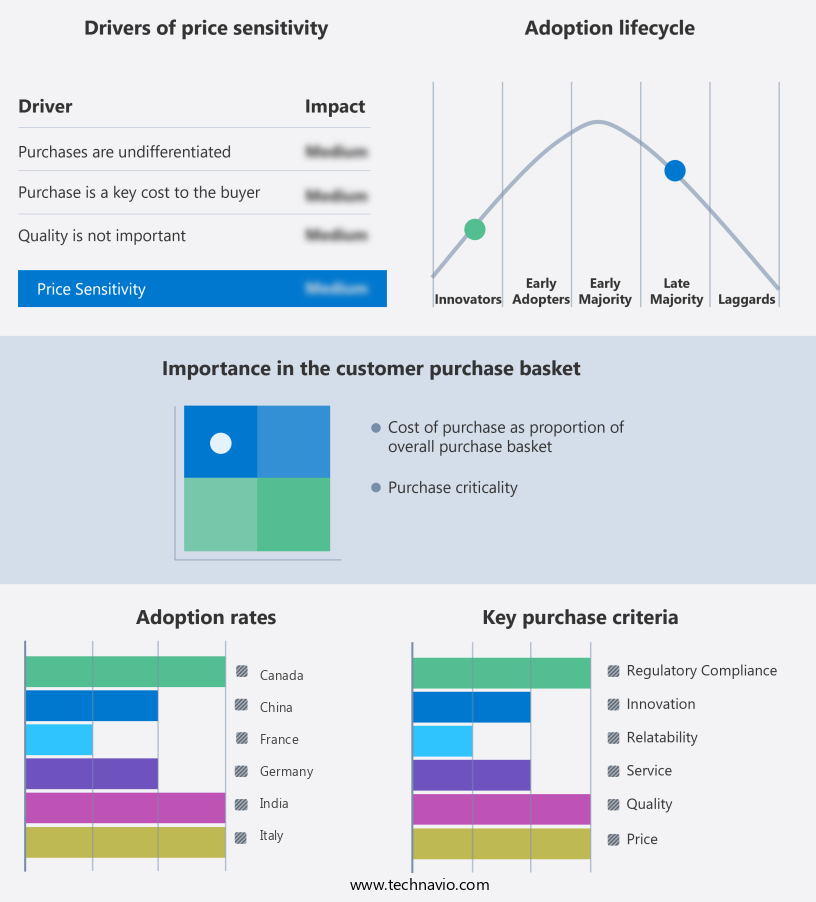

Exclusive Technavio Analysis on Customer Landscape

The ai in cardiology market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in cardiology market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Cardiology Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in cardiology market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aidoc - The company's AI-driven cardiology solutions include the aiOS platform and CAC Patient Management system. These technologies automate coronary artery calcium scoring from non-gated CT scans and identify high-risk patients for targeted follow-up, enhancing clinical efficiency and patient care.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aidoc

- AliveCor Inc.

- Biofourmis Inc.

- Caption Care

- Cardiologs

- Cleerly Inc.

- Eko Devices Inc.

- HeartFlow Inc.

- Imricor

- Merative L.P.

- Nano-X Imaging Ltd.

- Perspectum Ltd

- RSIP VISION LTD

- Siemens Healthineers AG

- Tempus Labs Inc.

- UltraSight Ltd

- Ultromics Ltd.

- Vista AI Inc.

- ZEBRA MEDICAL

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI In Cardiology Market

- In January 2024, Medtronic, a leading medical technology, services, and solutions company, announced the U.S. Food and Drug Administration (FDA) clearance for its new AI-powered cardiac ultrasound system, Lumify AI. This system utilizes deep learning algorithms to analyze cardiac images and provide real-time insights, enhancing diagnostic accuracy (Medtronic Press Release, 2024).

- In March 2024, IBM Watson Health and the American College of Cardiology (ACC) entered into a strategic partnership to develop AI-driven cardiovascular solutions. Their collaboration aimed to improve patient outcomes and reduce healthcare costs through AI-assisted diagnosis and treatment recommendations (IBM Watson Health Press Release, 2024).

- In May 2024, Siemens Healthineers, a leading medical technology company, secured a significant investment of €1.3 billion from Goldman Sachs and other investors. A portion of the funds was allocated to advance AI research and development in cardiology and other medical fields (Siemens Healthineers Press Release, 2024).

- In August 2025, the FDA granted marketing authorization for the AI-powered wearable cardiac monitor, AliveCor's KardiaMobile Rhythm. This device uses deep learning algorithms to analyze heart rhythm data, enabling early detection and diagnosis of atrial fibrillation (AliveCor Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Cardiology Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

234 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 46.1% |

|

Market growth 2025-2029 |

USD 10381.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

39.0 |

|

Key countries |

US, Canada, China, Germany, UK, Japan, France, India, Italy, and The Netherlands |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- Amidst the rapidly evolving landscape of healthcare technology, the integration of Artificial Intelligence (AI) in cardiology continues to revolutionize diagnosis, treatment, and patient care. Cardiac MRI analysis, a key application of AI in this field, utilizes pattern recognition systems to identify anomalies and provide more accurate diagnoses. These systems, powered by deep learning algorithms, can process vast amounts of data, enabling AI-driven treatment plans tailored to individual patients. Diagnostic accuracy metrics remain a critical focus, with clinical decision support systems aiding healthcare professionals in interpreting complex data. Compliance with healthcare standards is essential, ensuring AI's integration aligns with regulations.

- Precision cardiology, an emerging field, combines AI with predictive analytics to anticipate stroke risks and optimize patient care. Bias detection methods are crucial to maintaining trust in AI systems, as deep learning algorithms learn from data annotation techniques. Echocardiogram AI and medical image processing enhance diagnostic capabilities, while cardiac arrhythmia detection and remote patient monitoring enable early intervention and improved patient outcomes. Performance evaluation metrics and model validation strategies are essential to ensuring the effectiveness and reliability of AI in cardiology. Regulatory approval processes are underway for AI-powered diagnosis, with machine learning models and large, diverse model training datasets paving the way.

- In the realm of wearable sensors, AI integration enables real-time patient risk profiling and cardiovascular disease screening. Clinical trial results and risk stratification AI contribute to the development of more effective treatments, while image recognition software and recurrent neural networks further expand AI's potential. Data security protocols are paramount, as AI systems process sensitive patient information. Convolutional neural networks and other advanced techniques facilitate efficient, accurate analysis, while algorithm explainability ensures transparency and trust. The future of AI in cardiology promises a more personalized, efficient, and effective approach to cardiac care.

What are the Key Data Covered in this AI In Cardiology Market Research and Growth Report?

-

What is the expected growth of the AI In Cardiology Market between 2025 and 2029?

-

USD 10.38 billion, at a CAGR of 46.1%

-

-

What segmentation does the market report cover?

-

The report segmented by Component (Software and Services), Type (Cardiac diagnostics and Cardiac monitoring), Application (Diagnosis, Prediction and risk assessment, Treatment planning, Remote monitoring, and Drug discovery), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation and increasing complexity of cardiovascular data, Navigating stringent data privacy, and security

-

-

Who are the major players in the AI In Cardiology Market?

-

Key Companies Aidoc, AliveCor Inc., Biofourmis Inc., Caption Care, Cardiologs, Cleerly Inc., Eko Devices Inc., HeartFlow Inc., Imricor, Merative L.P., Nano-X Imaging Ltd., Perspectum Ltd, RSIP VISION LTD, Siemens Healthineers AG, Tempus Labs Inc., UltraSight Ltd, Ultromics Ltd., Vista AI Inc., and ZEBRA MEDICAL

-

Market Research Insights

- The market is experiencing significant growth, with the global spending on AI in healthcare projected to reach USD150 billion by 2027, representing a compound annual growth rate of 40%. AI technologies, such as predictive modeling and automated ECG analysis, are revolutionizing cardiology by enhancing patient care, improving diagnostic accuracy, and reducing diagnostic errors. Clinical implementation of AI in cardiology is ongoing, with user acceptance testing and interoperability standards being key considerations. Cost-effectiveness assessments and workflow efficiency improvements are driving the adoption of AI-based heart monitoring and big data analytics in cardiology. AI technologies are also facilitating clinical trial design and enabling real-world evidence collection.

- However, scalability considerations, ethical considerations, and data privacy regulations pose challenges to the widespread adoption of AI in cardiology. Training and education are essential to ensure the effective use of AI in clinical practice. Deployment strategies, software validation procedures, and data visualization tools are crucial to optimizing the use of AI in cardiology. AI technologies are transforming cardiology by enabling early detection algorithms, longitudinal data analysis, and personalized medicine. The integration of healthcare data and the use of cloud computing infrastructure are enabling the development of advanced AI applications in cardiology. The future of AI in cardiology holds promise for improved diagnostic accuracy and enhanced patient care.

We can help! Our analysts can customize this ai in cardiology market research report to meet your requirements.

RIA -

RIA -