Champagne Market Size 2026-2030

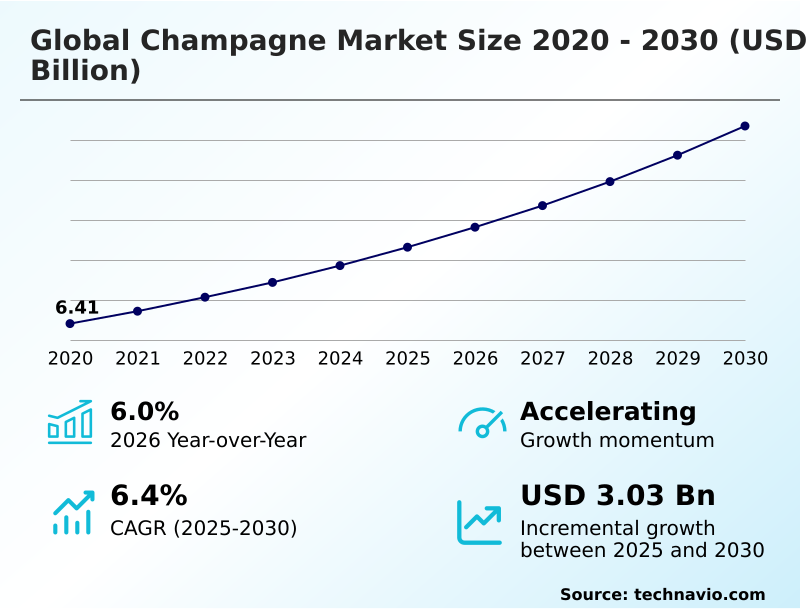

The Champagne Market size was valued at USD 8.32 billion in 2025, growing at a CAGR of 6.4% during the forecast period 2026-2030.

Major Market Trends & Insights

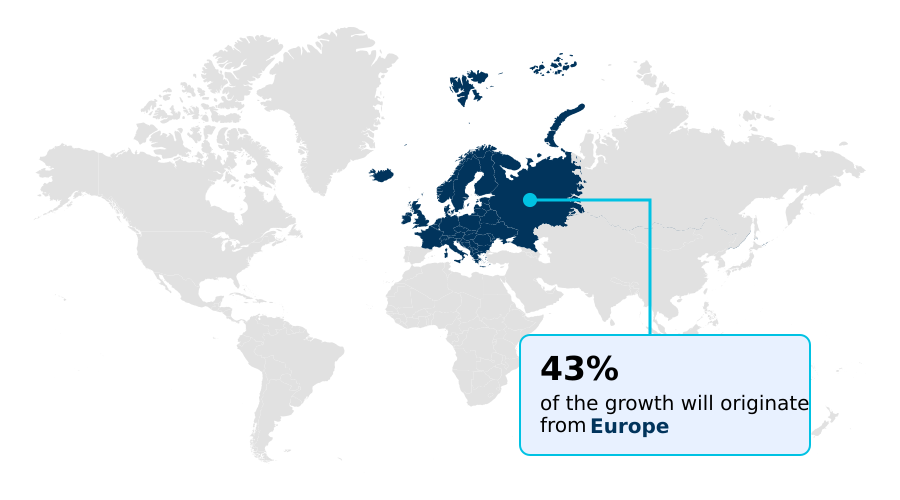

- Europe dominated the market and accounted for a 42.9% growth during the forecast period.

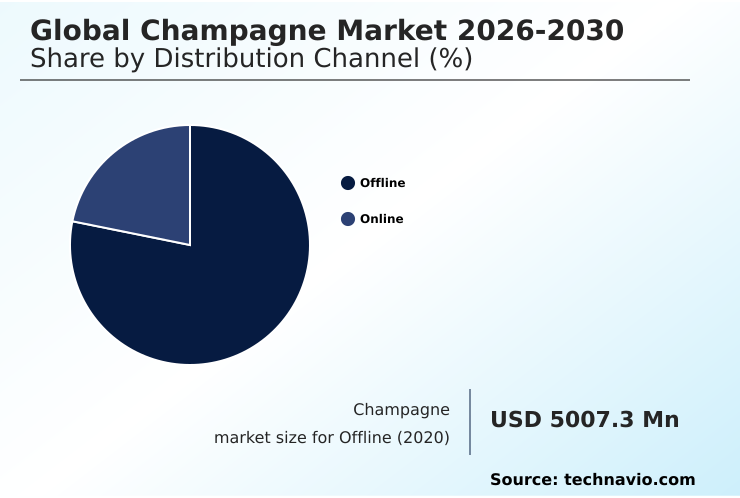

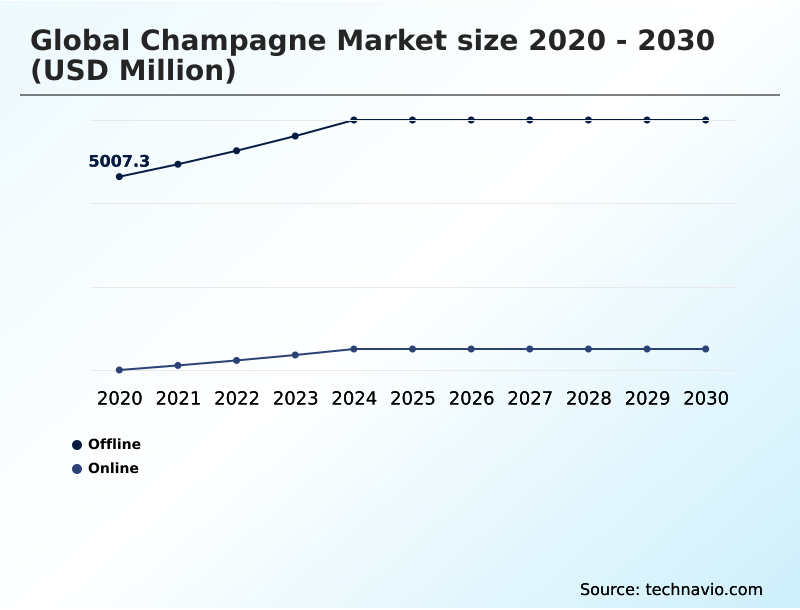

- By Distribution Channel - Offline segment was valued at USD 6.07 billion in 2024

- By Price Range - Economy segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 4.94 billion

- Market Future Opportunities 2025-2030: USD 3.03 billion

- CAGR from 2025 to 2030 : 6.4%

Market Summary

- The champagne market is defined by a structural shift towards premiumization, with consumers prioritizing quality and origin over volume. This is evidenced by the luxury segment growing 15% faster than the economy segment. A key driver is the increasing demand from millennial consumers, who value experiential purchases and share them on social media, expanding brand equity.

- However, the market faces a significant challenge from the rising popularity of lower-priced sparkling alternatives like prosecco and cava, which now capture over 30% of the sparkling wine volume in some regions. In response, a producer might leverage cold-chain technology to ensure grape quality and protect the distinct autolytic notes of its prestige cuvee, reinforcing its premium position against substitutes.

- This focus on provenance and sustainable viticulture is crucial for maintaining market leadership and justifying premium price points amid climate volatility.

What will be the Size of the Champagne Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Champagne Market Segmented?

The champagne industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Offline

- Online

- Price range

- Economy

- Mid-range

- Luxury

- Type

- Non-vintage champagne

- Vintage champagne

- Prestige cuvee

- Geography

- Europe

- France

- UK

- Germany

- North America

- US

- Canada

- Mexico

- APAC

- India

- China

- Australia

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- Europe

How is the Champagne Market Segmented by Distribution Channel?

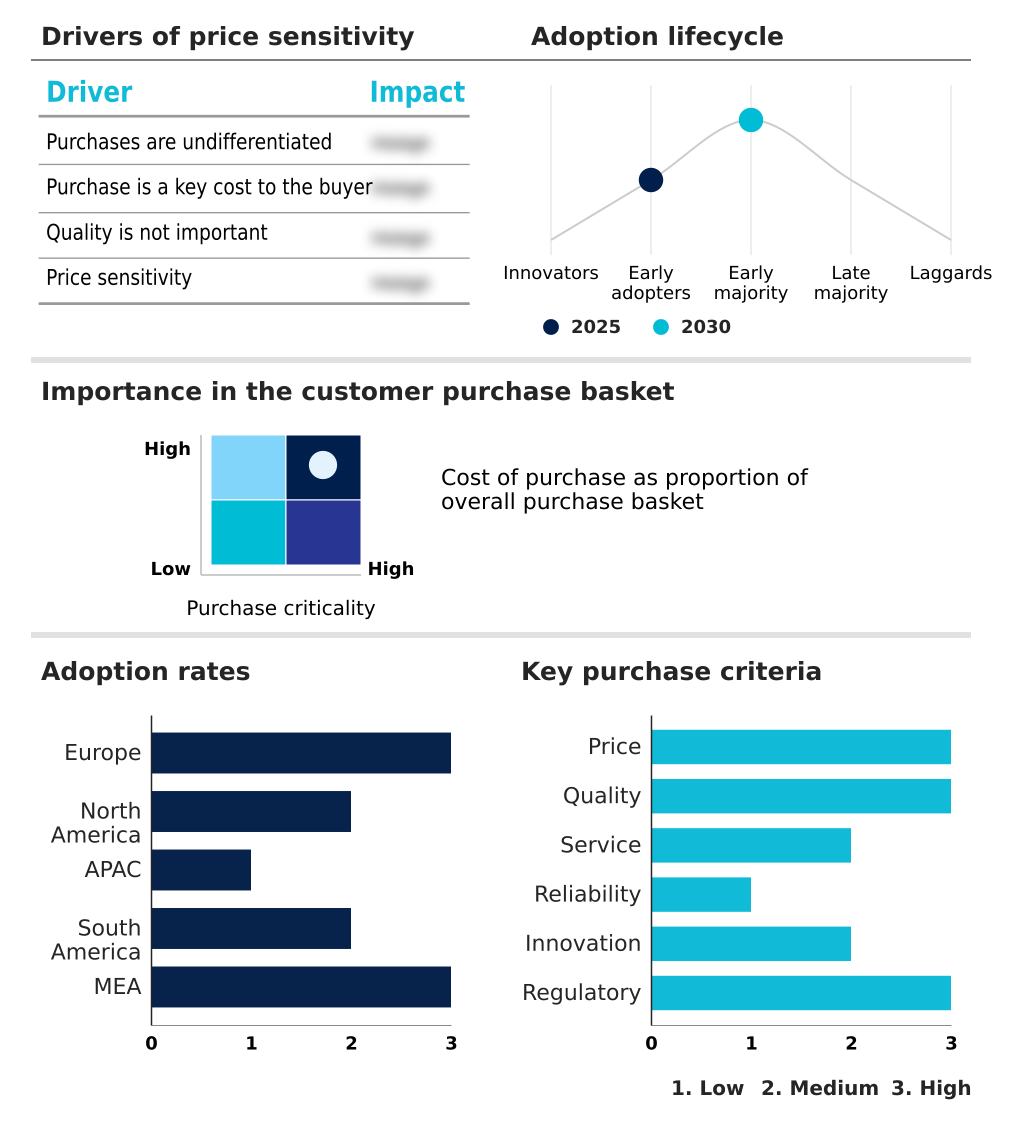

The offline segment is estimated to witness significant growth during the forecast period.

The offline segment, representing 77% of the total market, remains the cornerstone of champagne distribution through off-premise channels like specialty retailers and on-premise consumption in the hospitality sector.

These physical venues offer an immersive experience, allowing consumers to receive expert sommelier services and appreciate the nuances of lees aging or specific disgorgement date information.

The premiumization trend is highly evident here, as fine dining establishments drive sales of bottles showcasing complex autolytic notes from extended aging.

This channel is critical for brands to convey the quality derived from processes like malolactic fermentation and the traditional riddling process, justifying higher price points and building long-term loyalty.

The Offline segment was valued at USD 6.07 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Champagne market is rising in the leading region?

Europe is estimated to contribute 42.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Champagne Market demand is rising in Europe Request Free Sample

Europe remains the dominant region, accounting for 42.9% of incremental growth, driven by deep-rooted brand equity and strong cooperative networks. Countries like France and the UK show high per-capita consumption through established off-premise channels.

In contrast, North America, contributing nearly 25% of growth, exhibits a strong appetite for premium styles like blanc de blancs, supported by sophisticated cold-chain technology in its supply chains.

The APAC market is characterized by rapid growth in wine tourism and a focus on grower champagne, indicating a maturing palate.

Regional trade agreements continue to shape market access, while the strict appellation d'origine controlee rules ensure the unique character derived from the methode champenoise is protected globally.

What are the key Drivers, Trends, and Challenges in the Champagne Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the champagne market requires an understanding of both consumer intent and production nuances. When consumers search for the best champagne for celebrations, they often find themselves evaluating champagne versus prosecco quality differences, a key consideration for marketers positioning premium products.

- The higher price of champagne is justified by its complex production and superior aging potential, leading enthusiasts to consult a champagne aging potential guide for investment and collection purposes. However, the industry's future is closely tied to environmental factors, making the impact of climate on champagne production a critical variable for long-term supply stability.

- A producer's ability to maintain grape quality can mean a 20% difference in yield compared to less resilient vineyards. Addressing these consumer questions and operational challenges is vital for sustained growth, as is highlighting offerings in an organic champagne brands comparison to meet evolving wellness trends. This comprehensive approach ensures relevance in a competitive market.

What are the key market drivers leading to the rise in the adoption of Champagne Industry?

- The growing demand for champagne from millennials is a key market driver, fueled by this generation's preference for experiential luxury and social media visibility.

- The growing demand from millennial consumers, who now represent 40% of the luxury beverage market, is a primary driver. This demographic prioritizes experiential marketing and authenticity, fueling on-premise consumption in the hospitality sector.

- Recent product launches cater to this trend, with a 25% increase in low-sugar options like brut nature and the introduction of single-serve options to broaden accessibility.

- The enduring gifting culture and use of champagne as a celebration drink are amplified by social media, boosting sales of high-margin vintage champagne and prestige cuvee products.

- This ensures sustained growth as younger consumers integrate champagne into a wider array of social occasions.

What are the market trends shaping the Champagne Industry?

- The expansion of the e-commerce sector is a pivotal market trend, fundamentally reshaping how consumers discover and purchase champagne online.

- The expansion of e-commerce is a defining trend, with online sales growing 30% faster than traditional retail, enabling direct-to-consumer sales for many boutique producers. This digital shift facilitates the discovery of niche products like rose champagne and supports the rising demand for private-label brands, which now account for 1 in 10 bottles sold in some key markets.

- Concurrently, sales of products with organic certification are surging, reflecting a consumer pivot towards sustainable viticulture and biodynamic techniques. Producers are responding by highlighting unique cuvee blending methods and transparent sourcing, moving beyond standard non-vintage champagne offerings to capture this conscientious consumer segment.

What challenges does the Champagne Industry face during its growth?

- Rising competition from other alcoholic beverages, including premium sparkling alternatives and craft spirits, presents a significant challenge to the market's growth.

- Significant challenges stem from climate volatility, which directly impacts grape quality and limits production volume, with some premier cru vineyards reporting yield reductions of up to 20% in adverse years. These weather-related disruptions complicate vineyard management and strain supply chain logistics, threatening the consistent terroir expression essential for premium brands.

- This pressure is compounded by competition from other alcoholic beverages and campaigns against alcohol consumption. While the premiumization trend provides some insulation, producers face rising costs from investments in adaptive measures like mechanical harvesting and advanced irrigation, squeezing margins even for grapes from grand cru vineyards.

Exclusive Technavio Analysis on Customer Landscape

The champagne market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the champagne market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Champagne Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, champagne market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Champagne de Castellane - Vendors offer a spectrum of champagnes, from accessible non-vintage blends to exclusive prestige cuvées, catering to diverse consumer segments and occasions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Champagne de Castellane

- Champagne Devaux

- Champagne GH Martel Co.

- Champagne Joseph Perrier

- Champagne Laurent Perrier

- Champagne Louis Roederer

- Champagne Nicolas Feuillatte

- Champagne Piper Heidsieck

- Champagne Taittinger

- Constellation Brands Inc.

- E and J Gallo Winery

- F Korbel and Bros

- GH Mumm

- Groupe Thienot

- Krug

- Lanson BCC

- Remy Cointreau SA

- Veuve Clicquot

- Vranken Pommery Monopole

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Brewers industry, a significant increase in craft production and consumer interest in unique flavor profiles has amplified the appeal of artisanal beverages, directly benefiting grower champagne and boutique producers in the champagne market who emphasize terroir expression.

- Rapid shifts in alcohol consumption patterns, particularly among younger demographics favoring premium and experiential drinks, are expanding the occasions for champagne consumption beyond traditional celebrations, impacting on-premise consumption.

- The rising demand for premium and super-premium offerings, a key trend in the Brewers industry, reinforces the premiumization trend within the champagne market, boosting sales of vintage champagne and prestige cuvee products.

- Increasing online sales and the growth of e-commerce platforms, a major development in the Brewers industry, are creating new direct-to-consumer sales channels for champagne houses, improving supply chain logistics and market access.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Champagne Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 288 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.4% |

| Market growth 2026-2030 | USD 3031.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.0% |

| Key countries | France, UK, Germany, Italy, Spain, The Netherlands, US, Canada, Mexico, India, China, Australia, South Korea, Japan, Indonesia, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The champagne market ecosystem is a complex network where grape growers, cooperative networks, and historic houses interact within a strict regulatory framework set by the Appellation d'Origine Contrôlée. This system governs everything from vineyard management to cuvee blending, ensuring high standards.

- The value chain is dominated by offline channels, which account for over 75% of sales, though direct-to-consumer sales are growing by more than 10% annually. Raw material suppliers (grape growers) hold significant power due to finite land and increasing climate volatility, influencing production costs.

- Distribution is managed through a tiered system of importers, wholesalers, and retailers, including the vital hospitality sector. End-users, ranging from casual celebrants to serious collectors, are influenced by marketing, brand equity, and the premiumization trend.

What are the Key Data Covered in this Champagne Market Research and Growth Report?

-

What is the expected growth of the Champagne Market between 2026 and 2030?

-

The Champagne Market is expected to grow by USD 3.03 billion during 2026-2030, registering a CAGR of 6.4%. Year-over-year growth in 2026 is estimated at 6.0%%. This acceleration is shaped by growing demand for champagne from millennials, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Offline, and Online), Price Range (Economy, Mid-range, and Luxury), Type (Non-vintage champagne, Vintage champagne, and Prestige cuvee) and Geography (Europe, North America, APAC, South America, Middle East and Africa). Among these, the Offline segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers Europe, North America, APAC, South America and Middle East and Africa. Europe is estimated to contribute 42.9% to market growth during the forecast period. Country-level analysis includes France, UK, Germany, Italy, Spain, The Netherlands, US, Canada, Mexico, India, China, Australia, South Korea, Japan, Indonesia, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Israel and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is growing demand for champagne from millennials, which is accelerating investment and industry demand. The main challenge is rising competition from other alcoholic beverages, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Champagne Market?

-

Key vendors include Champagne de Castellane, Champagne Devaux, Champagne GH Martel Co., Champagne Joseph Perrier, Champagne Laurent Perrier, Champagne Louis Roederer, Champagne Nicolas Feuillatte, Champagne Piper Heidsieck, Champagne Taittinger, Constellation Brands Inc., E and J Gallo Winery, F Korbel and Bros, GH Mumm, Groupe Thienot, Krug, Lanson BCC, Remy Cointreau SA, Veuve Clicquot and Vranken Pommery Monopole. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape of the champagne market is marked by intense rivalry, with the top 10 vendors accounting for over 60% of total sales. Major players like Champagne Louis Roederer and Veuve Clicquot are focusing on innovation to maintain their market position.

- For instance, recent industry moves show a 25% increase in investment in sustainable viticulture and regenerative farming practices, aiming to enhance brand equity and appeal to environmentally conscious consumers. These actions are a direct response to the growing demand for authenticity and transparency in production.

- However, the entire industry grapples with supply chain logistics complicated by climate volatility, which can impact grape quality and production volumes. Companies are adapting by investing in advanced vineyard management technologies to mitigate these risks and ensure consistency.

We can help! Our analysts can customize this champagne market research report to meet your requirements.

RIA -

RIA -