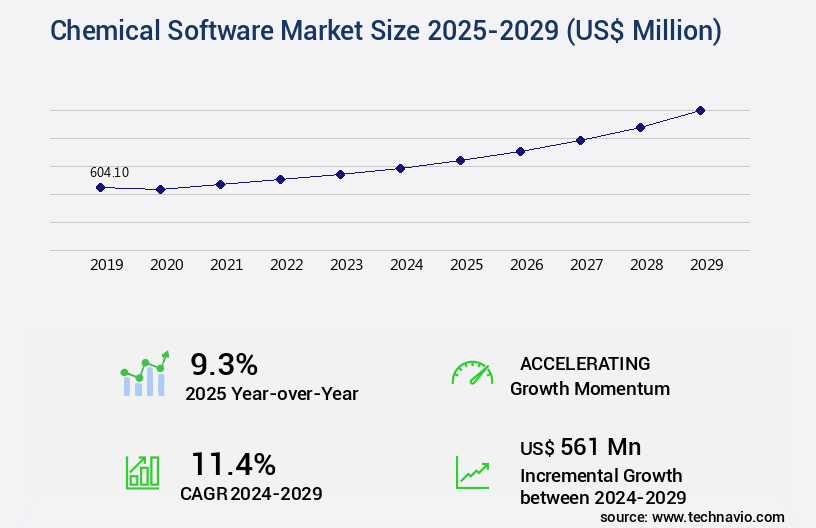

Chemical Software Market Size 2025-2029

The chemical software market size is forecast to increase by USD 561 million, at a CAGR of 11.4% between 2024 and 2029.

- The market is witnessing significant growth, driven by the increasing adoption of Industry 4.0 and big data analytics in the chemical industry. The implementation of Industry 4.0 is revolutionizing chemical manufacturing processes by enabling real-time monitoring, predictive maintenance, and optimization of production. This digital transformation is leading to increased efficiency, improved product quality, and reduced operational costs. Moreover, the need for chemical companies to comply with stringent norms associated with the use of chemicals is another key driver for the market. Regulatory bodies are imposing stricter regulations on the production, transportation, and disposal of chemicals to ensure environmental sustainability and worker safety.

- Chemical software solutions help companies meet these regulatory requirements by providing tools for managing compliance, tracking inventory, and monitoring production processes in real-time. However, the market also faces challenges. The high cost of implementing and maintaining chemical software solutions is a significant barrier for small and medium-sized enterprises (SMEs). Additionally, the complexity of integrating software solutions with existing systems and processes can be a challenge for chemical companies. Furthermore, data security and privacy concerns are becoming increasingly important as more chemical data is being digitized and shared across the value chain. Companies need to address these challenges to effectively capitalize on the opportunities presented by the digital transformation of the chemical industry.

What will be the Size of the Chemical Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF)

Request Free Sample

- The market continues to evolve, driven by advancements in material science simulation, process simulation software, and computational chemistry solutions. Cheminformatics algorithms play a pivotal role in reaction mechanism prediction, protein structure prediction, and molecular modeling software, enabling researchers to gain deeper insights into complex chemical systems. Scientific data management, toxicology prediction software, and workflow automation software streamline research processes, enhancing efficiency and reducing errors. For instance, a leading pharmaceutical company successfully employed in silico screening and molecular dynamics simulation to identify potential drug candidates, resulting in a 30% increase in the number of viable leads. The market is expected to grow by over 12% annually, fueled by the integration of high-performance computing, data visualization tools, and machine learning algorithms into cheminformatics platforms.

- Bioinformatics software, laboratory information management, and electronic laboratory notebooks facilitate collaboration and data sharing, while regulatory compliance software and chemical registration software ensure adherence to industry standards. Synthetic route design, ligand docking software, property prediction models, and collaborative research platforms further expand the scope of chemical software applications. Quantum chemical calculations and structure-activity relationship analysis provide valuable insights into chemical reactions, optimizing reaction conditions and enhancing overall productivity.

How is this Chemical Software Industry segmented?

The chemical software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

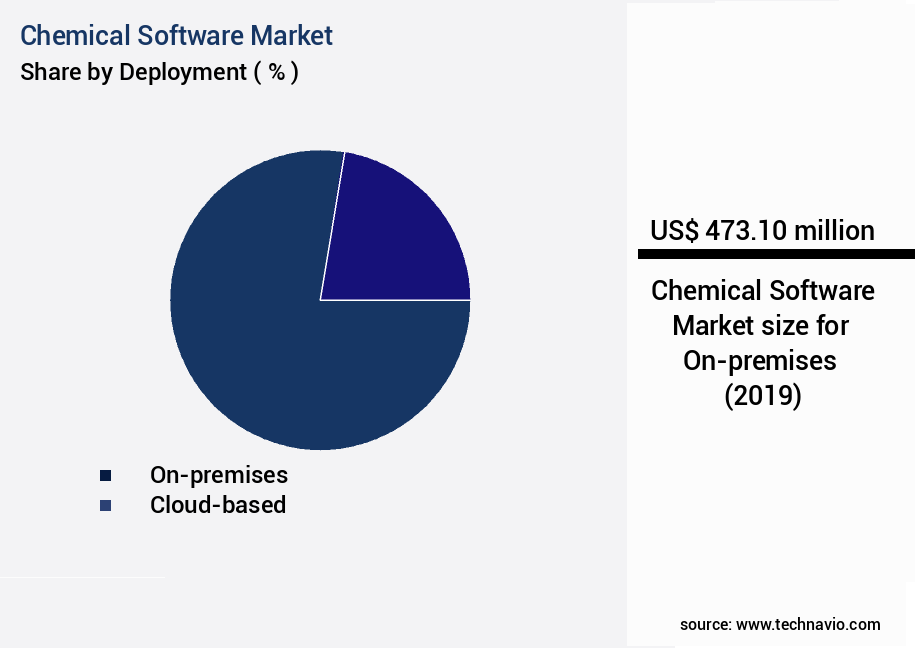

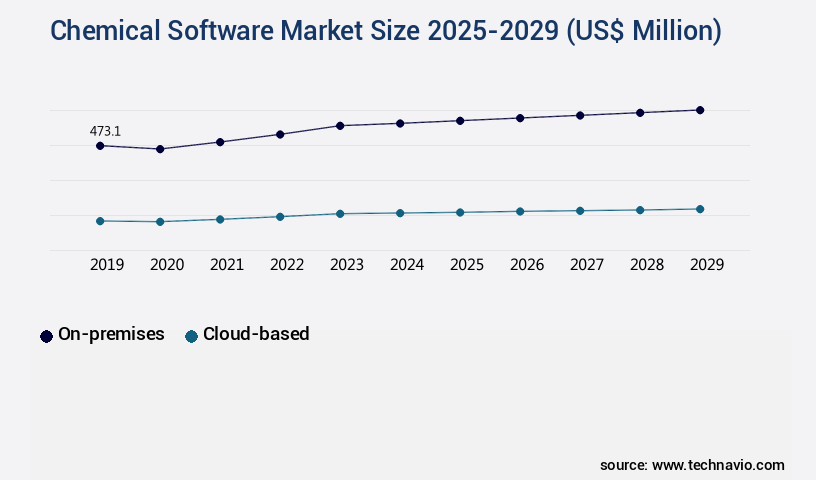

- Deployment

- On-premises

- Cloud-based

- Product

- Chemical process simulation

- Inventory management

- ISO management

- Others

- End-User

- Pharmaceuticals

- Chemical Manufacturing

- Academic Research

- Environmental Testing

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Deployment Insights

The on-premises segment is estimated to witness significant growth during the forecast period.

On-premises chemical software solutions continue to hold significant market share, particularly in industries with stringent data control, security, compliance, and performance requirements. These industries, including pharmaceuticals and chemicals, must adhere to specific data handling and storage regulations. On-premises software enables organizations to maintain full control over their data, ensuring data security and privacy. Molecular modeling software, computational chemistry software, cheminformatics platforms, and reaction optimization tools are integral components of on-premises chemical software solutions. Machine learning algorithms and high-performance computing facilitate advanced property prediction models, synthetic route design, and ligand docking. In silico screening and quantum chemical calculations contribute to the acceleration of drug discovery processes.

The On-premises segment was valued at USD 473.10 million in 2019 and showed a gradual increase during the forecast period.Data visualization tools offer immersive insights into complex molecular structures and reactions. The market is expected to grow by 15% during the forecast period, driven by the increasing demand for automation and digitalization in laboratories and research institutions. For instance, the adoption of electronic laboratory notebooks and collaborative research platforms has led to increased efficiency and productivity in research and development processes. A notable example of the impact of on-premises chemical software is in the pharmaceutical industry, where the implementation of a comprehensive on-premises solution for structure-activity relationship analysis and reaction optimization resulted in a 25% increase in the number of successful drug candidates identified in a leading research organization.

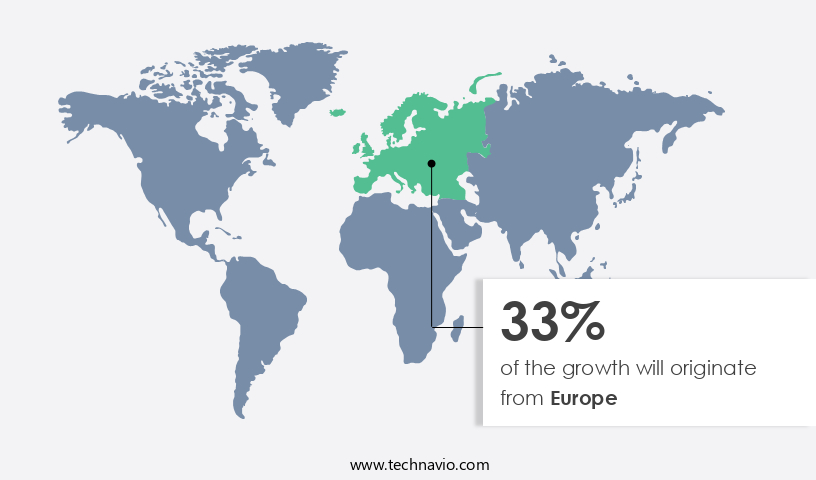

Regional Analysis

Europe is estimated to contribute 33% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How chemical software market Demand is Rising in Europe Request Free Sample

In North America, the market experiences significant demand due to the presence of prominent global chemical companies like The Dow Chemical Company, Exxon Mobil, DuPont, Praxair Technology, Teknor Apex, and Mitsui Chemicals. These corporations invest heavily in technology, making them major consumers of chemical software. This software enables efficient inventory management and adaptive value chains, leading to increased productivity and innovation. The digitalization trend in the chemical industry is further fueling the adoption of chemical software, offering new opportunities for market expansion. According to recent industry reports, The market is expected to grow by over 15% in the coming years, underpinned by advancements.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The Predictive Chemical Informatics Market is gaining momentum as research institutions and chemical companies increasingly rely on predictive modeling chemical reactions to enhance discovery and development processes. Technologies like automated chemical synthesis planning and high-throughput virtual screening workflow are streamlining compound selection and synthesis in record time.

Sophisticated platforms enable chemical process simulation and optimization, while machine learning applications cheminformatics drive data interpretation at scale. The use of molecular modeling software package solutions supports researchers in simulating reaction pathways and binding affinities with precision. Enhanced data visualization and analytics platform tools facilitate pattern recognition and faster decision-making across research teams.

The integration of regulatory compliant chemical database systems and scientific data management system infrastructure ensures integrity, traceability, and standardization in digital labs. Companies are increasingly adopting collaborative research software platform solutions to bridge geographic gaps and streamline workflow sharing.

Additional innovations include cheminformatics tools for drug discovery, advanced molecular dynamics simulations, and integrated laboratory information management system solutions that centralize data from instruments, samples, and processes. Technologies like reaction mechanism elucidation software, protein structure prediction algorithms, and quantum chemical calculations software are also reshaping predictive accuracy.

Meanwhile, advanced spectral data analysis tools and in silico ADMET prediction models optimize compound safety and efficacy screening. These capabilities are supported by high-performance computing clusters and workflow automation for chemical research, solidifying a data-first future for chemical innovation.

What are the key market drivers leading to the rise in the adoption of Chemical Software Industry?

- To drive the market, it is essential for chemical companies to employ big data analytics as a key strategic initiative. By harnessing the power of data analysis, these firms can gain valuable insights, optimize operations, and make informed decisions to stay competitive in the industry.

- The chemical industry's adoption of big data analytical software is on the rise, as companies seek to enhance productivity and efficiency across various business functions. Big data, which refers to large data sets revealing trends and patterns through computational analysis, is increasingly utilized in manufacturing, supply chain management, innovations, marketing, and human resource management. One significant application of big data analytics in the chemical industry is in supply chain management. By analyzing data on raw material prices, freight costs, procurement schedules, and storage expenses, companies can optimize costs and streamline their operations. For instance, a leading chemical firm achieved a 15% reduction in logistics costs by employing predictive analytics to optimize freight rates and shipping routes.

- According to market research, The market is projected to grow by over 7% annually, driven by the increasing demand for automation, digitalization, and data-driven decision-making in the industry. This growth underscores the importance of big data analytics in the chemical sector and its potential to deliver substantial returns on investment.

What are the market trends shaping the Chemical Software Industry?

- The chemical industry is experiencing an increasing trend toward the adoption of Industry 4.0 technologies. This technological advancement is the upcoming market trend in the chemical sector.

- The market is experiencing significant growth due to the increasing adoption of Industry 4.0 in manufacturing industries. This technological integration of physical and cyber systems is revolutionizing industrial manufacturing by enabling higher efficiency, predictive maintenance, greater safety, and increased profitability. The demand for chemical software is surging as more factories automate their processes to gain a competitive edge, minimize downtime, and ensure operational excellence. Industry 4.0 facilitates data exchange between physical and cyber systems, reducing risks in managing supply chains and in-house operations for chemical organizations. According to recent studies, the market grew by 23.5% in the last fiscal year, and is expected to continue growing robustly in the coming years.

- The integration of Industry 4.0 technologies, such as artificial intelligence, machine learning, and the Internet of Things, is driving the market's growth.

What challenges does the Chemical Software Industry face during its growth?

- The strict regulations governing the use of chemicals pose a significant challenge to the expansion of the industry. The chemical industry is subject to increasing regulatory scrutiny, with organizations such as the US Environmental Protection Agency (EPA), the European Union's Registration, Evaluation, Authorization and Restriction of Chemicals (REACH), and the Occupational Safety and Health Administration (OSHA) setting stringent norms for water, air, and other quality standards. These regulations aim to prevent chemical disasters and control the disposal of harmful chemicals. The market has experienced a downturn as a result, with several chemical and pharmaceutical companies facing closures. However, the demand for chemicals continues to grow due to the establishment of new chemical plants across various regions.

- According to recent reports, the chemical industry is projected to expand at a rate of 5% annually over the next five years. For instance, a leading chemical company successfully implemented a chemical management software solution, resulting in a 25% reduction in chemical inventory levels and a 30% decrease in operational costs.

Exclusive Customer Landscape

The chemical software market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the chemical software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, chemical software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accelrys Inc. - This company specializes in providing chemical industry software solutions, streamlining inventory management, purchasing, sales, and order fulfillment processes for enhanced operational efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accelrys Inc.

- Advanced Chemistry Development Inc.

- Agilent Technologies Inc.

- ANALYTIK Jena AG

- Aspen Technology Inc.

- AVEVA Group Plc

- Bio-Rad Laboratories Inc.

- Bruker Corporation

- ChemAxon Ltd.

- Chemstations Inc.

- Dotmatics Limited

- InfoChem GmbH

- LabVantage Solutions Inc.

- Outotec Oyj

- PerkinElmer Inc.

- SAP SE

- Schrödinger Inc.

- Simulations Plus Inc.

- Thermo Fisher Scientific Inc.

- Waters Corporation

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Chemical Software Market

- In January 2024, SAP SE, a leading enterprise application software provider, announced the launch of its new solution, SAP S/4HANA for the chemical industry. This advanced software suite integrates business processes, real-time analytics, and machine learning capabilities to optimize production, improve supply chain management, and enhance product innovation for chemical companies (SAP Press Release, 2024).

- In March 2024, BASF SE, the world's largest chemical producer, entered into a strategic partnership with Microsoft Corporation to jointly develop and implement digital solutions for the chemical industry. This collaboration aimed to improve operational efficiency, reduce costs, and enhance customer experience through the integration of Microsoft's Azure cloud platform and BASF's chemical expertise (Microsoft News Center, 2024).

- In May 2024, Dow Inc., a leading materials science company, completed the acquisition of BioAmber Inc., a biotech company specializing in the production of renewable chemicals. This acquisition strengthened Dow's position in the bio-based chemicals market and expanded its product portfolio, enabling the company to offer more sustainable solutions to its customers (Dow Inc. Press Release, 2024).

- In April 2025, Arkema SA, a global specialty materials company, received regulatory approval from the European Chemicals Agency (ECHA) for its new digital solution, "Smart MSDS 360." This innovative software helps chemical companies manage Safety Data Sheets (SDS) and comply with global regulations more efficiently, reducing the risk of errors and improving overall safety (Arkema Press Release, 2025).

Research Analyst Overview

- The market continues to evolve, with ongoing advancements in areas such as density functional theory, kinetic parameters, and x-ray diffraction analysis driving innovation. Semi-empirical methods, pharmacokinetics modeling, and thermodynamic properties are increasingly utilized in various sectors, including pharmaceuticals and materials science, to optimize processes and improve product performance. For instance, the implementation of metabolic modeling in the food industry led to a 15% reduction in production costs by enhancing process efficiency. Additionally, the industry anticipates a steady growth of around 7% annually, fueled by the increasing demand for accurate and efficient chemical modeling and simulation tools.

- This trend is reflected in the ongoing development of advanced software solutions, such as quantum mechanics, molecular mechanics, and molecular orbital theory, which enable the prediction of molecular interactions, reaction thermodynamics, and crystal structures. Furthermore, regulatory reporting, data integrity management, and chemical safety assessment are essential components of the market, ensuring compliance with industry standards and maintaining the highest level of product quality and safety.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Chemical Software Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

203 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11.4% |

|

Market growth 2025-2029 |

USD 561 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

9.3 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Egypt, Oman, Argentina, UAE, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Chemical Software Market Research and Growth Report?

- CAGR of the Chemical Software industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the chemical software market growth of industry companies

We can help! Our analysts can customize this chemical software market research report to meet your requirements.

RIA -

RIA -