Chile Information Technology (IT) Market Size 2025-2029

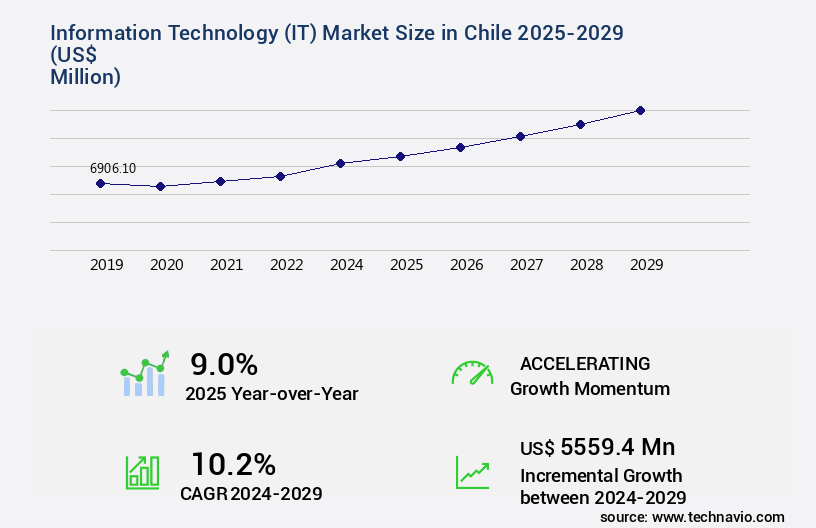

The Chile information technology (it) market size is forecast to increase by USD 5.56 billion, at a CAGR of 10.2% between 2024 and 2029.

The Chile Information Technology (IT) Market is anticipated to exceed USD 17 billion by 2029, up from approximately USD 12 billion in 2024, driven by accelerated digital transformation, the adoption of cloud-based solutions, and an increasing focus on cybersecurity infrastructure. In 2023, over 65% of Chilean enterprises adopted cloud computing and data analytics platforms, supporting the demand for enterprise resource planning (ERP) systems and IT managed services. The market is witnessing significant investments in IoT-enabled solutions, AI-driven automation, and 5G connectivity, reshaping operational frameworks across industries. Internal linking opportunities include topics like Cloud Computing Market, Cybersecurity Services Market, IT Managed Services Market, and Enterprise Software Solutions Market, reflecting the evolving digital ecosystem in Chile.

Major Market Trends & Insights

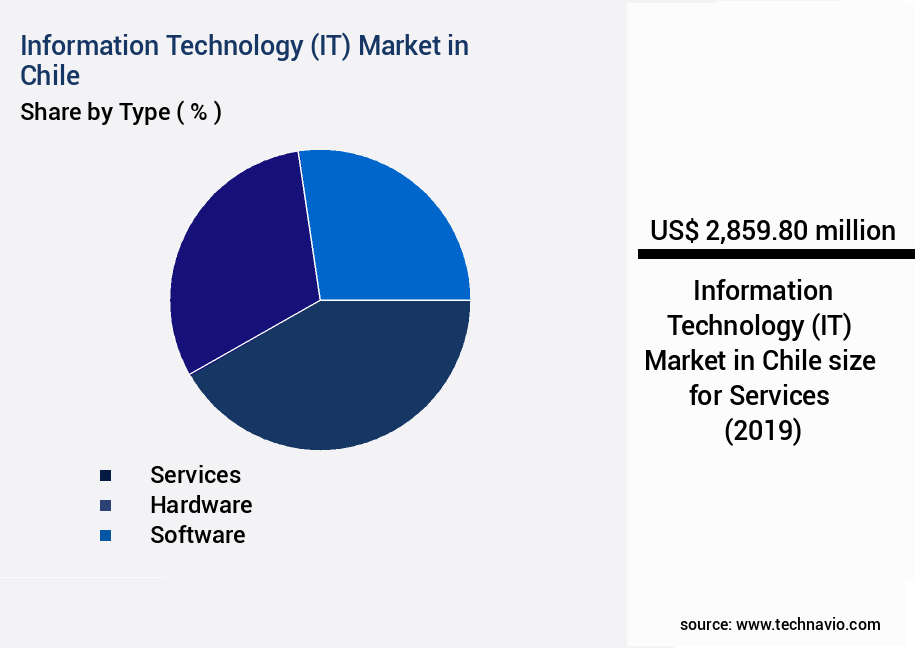

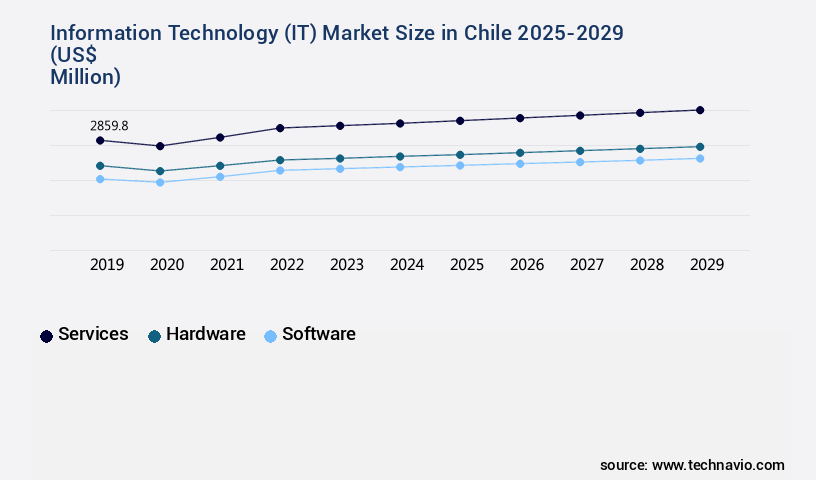

- By the Type, the Services sub-segment was valued at USD 2.86 billion in 2022

- By the End-user, the BFSI sub-segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 109.63 billion

- Future Opportunities: USD USD 5.56 billion

- CAGR : 10.2%

What will be the size of the Chile Information Technology (IT) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

The global digital transformation market continues to evolve as enterprises prioritize cloud migration and data center modernization to enhance operational efficiency. Organizations are integrating AI-powered solutions and IoT sensors to streamline workflows, improve decision-making, and optimize business outcomes. Increasing reliance on mobile platforms has accelerated the need for mobile app security, while cybersecurity awareness and data breach prevention remain central to safeguarding critical information assets across industries.

Adoption trends indicate a measurable shift toward integrated strategies, with enterprises leveraging technology consulting and digital strategy to achieve scalable modernization. Digital transformation initiatives now encompass DevOps automation, software testing, and IT infrastructure optimization to ensure agility and resilience. Furthermore, businesses are investing in innovation roadmaps, digital skills development, and tech incubators to remain competitive in an environment driven by continuous technological advancement.

A notable comparison in market performance highlights the increasing allocation of resources toward security. For example, investment in cloud security accounted for 32% of total digital infrastructure spending, while spending on broader IT infrastructure optimization represented 28%. Additionally, projections suggest that cybersecurity-related investments are expected to grow by 18% in the near term, outpacing overall digital marketing expenditure growth, which stands at 12%. This divergence reflects a market where data protection and operational continuity are prioritized alongside initiatives such as social media management, search engine marketing, and customer experience management.

The focus on secure, data-driven strategies, combined with government subsidies and strong technology partnerships, continues to reinforce a sustainable digital workforce. Organizations are implementing digital marketing strategies, online advertising campaigns, and email marketing within integrated platforms, while predictive analytics tools and security audits ensure long-term scalability and compliance.

How is this Chile Information Technology (IT) Market segmented?

The information technology (it) in Chile industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Services

- Hardware

- Software

- End-user

- BFSI

- IT and telecom

- Government

- Healthcare

- Others

- Deployment Type

- Cloud-Based

- On-Premises

- Organization Type

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- Geography

- South America

- Chile

- South America

By Type Insights

The services segment is estimated to witness significant growth during the forecast period.

IT services encompass consulting, learning and training, development and integration, hardware maintenance and support, IT management, process management, and software support. Consulting and software maintenance and support services are experiencing significant growth within this market segment. Businesses in Chile are seeking to enhance their delivery systems and adopt cost-effective models, leading to increased demand for IT services. Additionally, the transition from on-premises to cloud-based software and IT infrastructure deployment is driving market expansion. This shift also necessitates a growing need for IT education and training services. Software-as-a-Service (SaaS) and Infrastructure-as-a-Service (IaaS) are increasingly popular, with companies opting for these solutions to streamline operations and reduce capital expenditures.

IT asset management is crucial for organizations to maintain control over their technology investments, ensuring compliance with regulations and maximizing the value of their IT resources. Artificial intelligence, machine learning, and data analytics are transforming the IT landscape, enabling businesses to gain insights from their data and make informed decisions. Content marketing, mobile app development, and digital marketing are essential components of a comprehensive IT strategy, helping businesses reach and engage their audience effectively. Security remains a top priority, with network security, endpoint security, and data encryption essential for protecting sensitive information. Compliance regulations, such as the General Data Protection Regulation (GDPR), necessitate robust security measures.

Cloud computing services, including data warehousing, cloud storage, and platform-as-a-service (PaaS), offer businesses flexibility and scalability. Disaster recovery and business continuity planning are essential for ensuring business resilience. The IT talent pool in Chile is rich, with skilled labor available for software development, project management, and technology adoption. Innovation hubs and startup ecosystems are fostering the growth of new technologies and business models. Venture capital and digital inclusion initiatives are driving innovation and digital transformation in Chile's IT sector. Blockchain technology, cybersecurity solutions, and agile methodologies are among the emerging trends shaping the market.

The Services segment was valued at USD 2.86 billion in 2019 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The global IT infrastructure market is evolving rapidly as organizations prioritize effective IT infrastructure scalability and optimized IT infrastructure design to support growing digital demands. Enterprises are increasingly implementing innovative cloud computing solutions and high-performance computing systems to enhance processing power while ensuring secure data center operations. Advanced network monitoring tools and integrated IT security platforms have become essential for maintaining system reliability and enabling efficient IT cost reduction methods without compromising performance or security.

Businesses are adopting agile software development practices and automated software deployment to accelerate product delivery while ensuring reliable IT service delivery. Modern data analytics techniques and enterprise mobility management are also gaining traction as organizations seek greater flexibility and actionable insights from their operations. Comprehensive IT risk assessment and proactive IT risk mitigation are critical to maintaining operational continuity, supported by robust disaster recovery mechanisms and effective cybersecurity strategies.

A recent comparison highlights a strong industry shift toward cloud-based data security measures, which account for a 34% adoption rate, compared to 21% for traditional on-premises security frameworks. Similarly, strategic IT transformation initiatives represent 28% of current enterprise investments, outpacing legacy system upgrades at 17%. This trend underscores the growing demand for scalable and secure infrastructure, emphasizing strategic IT talent management and digital-first approaches. As companies focus on resilience and agility, the integration of enterprise mobility, security automation, and comprehensive disaster recovery systems will remain key to ensuring long-term competitiveness.

What are the Chile Information Technology (IT) Market drivers leading to the rise in adoption of the Industry?

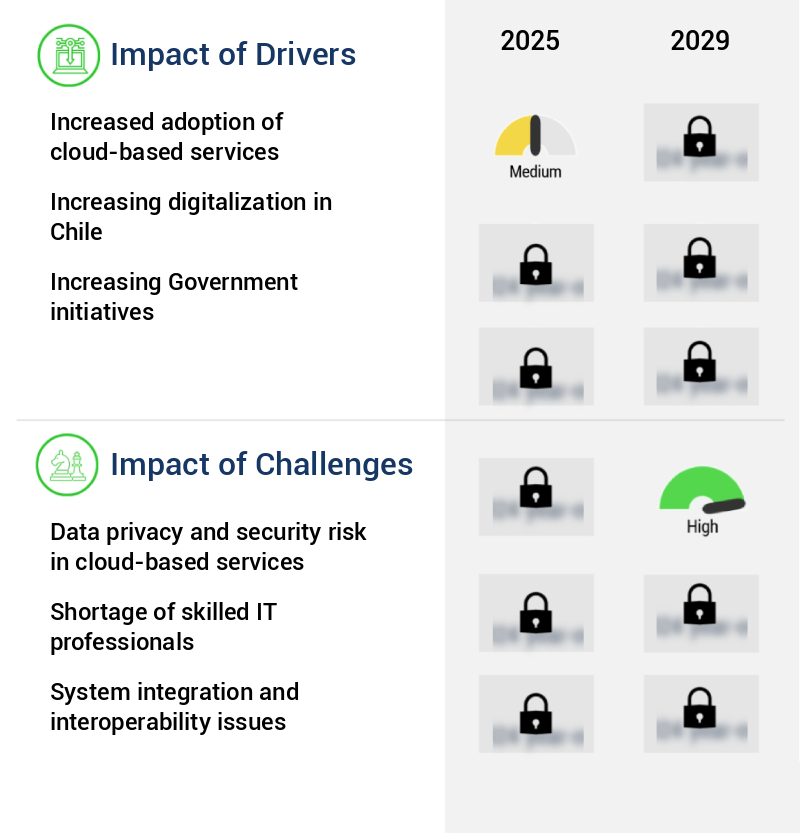

- The significant expansion in the utilization of cloud-based services serves as the primary catalyst for market growth. In Chile, enterprises are embracing digital transformation to remain competitive in today's business landscape.

- A significant shift towards cloud computing is driving this digitization process. Cloud-based solutions offer enterprises cost-effective, flexible, and scalable alternatives to traditional IT infrastructure. These benefits enable businesses to adapt quickly to changing requirements and business dynamics.

- Cloud technologies, such as Business Intelligence, Platform-as-a-Service (PaaS), and Data Center Infrastructure, are gaining popularity among Chilean enterprises.

- Wireless security and data mining are essential components of these solutions. Venture capital investments in Chile's startup ecosystem are fueling the growth of digital innovation, with a focus on agile methodologies and social media marketing. The Chilean market for IT services is witnessing a rise in demand for digital solutions. Data analytics is a key area of investment, with enterprises seeking to gain insights from their data to make informed business decisions.

- The adoption of cloud-based solutions is not limited to large enterprises; Small and Medium Enterprises (SMEs) are also embracing this technology to stay competitive. The Chilean IT market is experiencing significant growth, driven by the adoption of cloud-based solutions and the resulting digital transformation.

What are the Chile Information Technology (IT) Market trends shaping the Industry?

- The emergence of artificial intelligence (AI) represents a significant market trend in the present business landscape. This technological advancement is mandated by the increasing demand for automation, efficiency, and innovation.

- Chilean enterprises are embracing Artificial Intelligence (AI) in their IT services to automate processes and enhance efficiency. AI integration improves process integrity and enables easy categorization and tagging of information for future retrieval. This technology addresses the issue of employees spending a significant amount of time on paperwork, thereby increasing enterprise costs and decreasing overall return on investment.

- The adoption of Software-as-a-Service (SaaS), mobile app development, content marketing, online advertising, and machine learning are also driving the digital transformation in Chilean businesses. By implementing AI in IT services, Chilean businesses can streamline operations, reduce manual effort, and improve data management.

- Furthermore, IT service management and asset management are critical areas where AI is being adopted to ensure compliance with regulations and secure networks through data encryption, anti-virus software, and network security.

How does Chile Information Technology (IT) Market face challenges during its growth?

- The growth of the cloud-based services industry is significantly impacted by the challenges posed by data privacy and security risks. These concerns are mandatory considerations for businesses and organizations when adopting cloud solutions.

- In Chile's IT market, cloud computing services continue to gain traction, with businesses recognizing the benefits of scalability, cost savings, and flexibility. However, data privacy and security concerns remain significant barriers to adoption, particularly for public cloud services.

- Cloud security management is a complex challenge for organizations, requiring robust measures to protect sensitive data from unauthorized access and cyber-attacks.The adoption of blockchain technology is also increasing, driven by its potential to enhance security and transparency.

- Managed services, including network infrastructure and endpoint security, are becoming essential for businesses to maintain their IT operations efficiently. The emergence of edge computing is expected to further transform the market, enabling faster data processing and reducing latency.

- Overall, Chile's IT market is dynamic and evolving, with a focus on innovation, security, and efficiency. Enterprises are leveraging advanced technologies to create new business models and enhance customer experiences.

Exclusive Customer Landscape

The information technology (it) market in Chile forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the information technology (it) market in Chile report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market research and growth strategies.

Customer Landscape of Chile Information Technology (IT) Market Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, information technology (it) market in Chile forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market research report.

Accenture PLC - This company specializes in providing cutting-edge IT solutions, encompassing data and analytics, finance, and metaverse applications. Our offerings are designed to empower businesses with actionable insights, financial optimization, and immersive digital experiences. Through advanced technologies and data-driven strategies, we help organizations enhance operational efficiency, mitigate risks, and drive growth. Our expertise lies in translating complex data into meaningful insights, enabling informed decision-making and strategic planning. By leveraging the latest technologies and trends, we deliver customized solutions tailored to our clients' unique needs.

The market growth and forecasting report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture PLC

- ADEXUS S.A

- Alphabet Inc.

- Amisoft

- Atos SE

- Cisco Systems Inc.

- Dassault Systemes SE

- Deloitte Touche Tohmatsu Ltd.

- HCL Technologies Ltd.

- Hewlett Packard Enterprise Co.

- Infosys Ltd.

- International Business Machines Corp.

- Microsoft Corp.

- NetApp Inc.

- Oracle Corp.

- SAP SE

- Schneider Electric SE

- SONDA S.A.

- Tata Consultancy Services Ltd.

- Verizon Communications Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Information Technology (IT) Market In Chile

- In March 2023, Chilean telecommunications company Entel and technology giant Microsoft announced a strategic partnership to accelerate digital transformation in Chile's small and medium-sized enterprises (SMEs) through cloud services and solutions. This collaboration aims to boost productivity and competitiveness among Chilean businesses (Entel press release).

- In June 2024, Chilean IT company Codelcoic and American tech firm IBM signed a deal to develop an AI-powered predictive maintenance system for Codelcoic's mining operations. This initiative is expected to optimize maintenance processes, reduce downtime, and improve overall efficiency (IBM press release).

- In October 2024, Chilean IT services provider Cognitics raised USD10 million in a Series A funding round led by US-based venture capital firm Sapphire Ventures. This investment will support Cognitics' expansion into new markets and the development of innovative IT solutions (Cognitics press release).

- In February 2025, the Chilean government launched a national digital transformation strategy, "Chile Conecta Digital," aimed at bridging the digital divide and promoting the adoption of technology in various sectors, including education, healthcare, and agriculture (Chilean Ministry of ICT press release). This initiative includes the allocation of USD500 million for digital infrastructure projects and the training of 100,000 Chileans in digital skills.

Research Analyst Overview

- In the dynamic and ever-evolving market, various sectors continue to embrace innovative technologies and solutions to drive growth and efficiency. IT Service Management and Asset Management practices are being optimized through Software-as-a-Service (SaaS) offerings, enabling agility and cost savings. Anti-virus software and Data Encryption solutions remain crucial components in securing digital assets, while Artificial Intelligence and Machine Learning are revolutionizing business processes.

- Mobile App Development and Innovation Hubs foster digital transformation, with Compliance Regulations ensuring data privacy and security. Online Advertising and Digital Marketing strategies are essential for businesses seeking to expand their reach.

- Cloud Computing Services, including Infrastructure-as-a-Service (IaaS) and Platform-as-a-Service (PaaS), offer scalability and flexibility. Talent pools are being cultivated through Education and Training programs, while Technology Investments continue to shape the landscape.

- Firewall Solutions and Disaster Recovery plans ensure business continuity, and IT Consulting Services provide strategic guidance. The IT sector in Chile is characterized by ongoing innovation, with emerging trends such as Blockchain Technology, Cybersecurity Solutions, and Edge Computing gaining traction. Venture Capital and the Startup Ecosystem are fueling digital inclusion and driving technological advancements.

- Data Mining, Digital Innovation, and Agile Methodologies are shaping the future of IT services. Hardware upgrades, Endpoint Security, Network Infrastructure, Managed Services, and IT Outsourcing are all integral parts of the IT market's continuous evolution. Wireless Security, IT Governance, Software Licensing, and Software Development are essential components of any modern IT strategy. Skilled labor, Data Analytics, and Social Media Marketing are in high demand as businesses adapt to the digital age.

- The IT market in Chile remains a vibrant and dynamic landscape, with ongoing technological advancements and evolving market patterns shaping the future of the industry. The focus on cybersecurity and data analytics is essential for businesses to ensure data privacy and security while gaining valuable insights from their data.

- They enable the implementation of advanced technologies like Big Data, Artificial Intelligence, and Internet of Things (IoT), which are essential for digital innovation. Moreover, cybersecurity solutions are a critical concern for enterprises adopting cloud technologies. The open architecture and shared resources of public cloud infrastructure make it more susceptible to security threats. Moreover, the demand for big data management, data warehousing, and infrastructure-as-a-service (IaaS) solutions is on the rise. Chile's talent pool is growing, with a focus on digital literacy, web development, and digital marketing skills.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Information Technology (IT) Market in Chile insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

198 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.2% |

|

Market growth 2025-2029 |

USD 5559.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

9.0 |

|

Key countries |

Chile |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Information Technology (IT) Market in Chile Research and Growth Report?

- CAGR of the Chile Information Technology (IT) Market industry during the forecast period

- Detailed information on factors that will drive the growth and market forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Chile

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the information technology (it) market in Chile growth of industry companies

We can help! Our analysts can customize this information technology (it) market in Chile research report to meet your requirements.

RIA -

RIA -