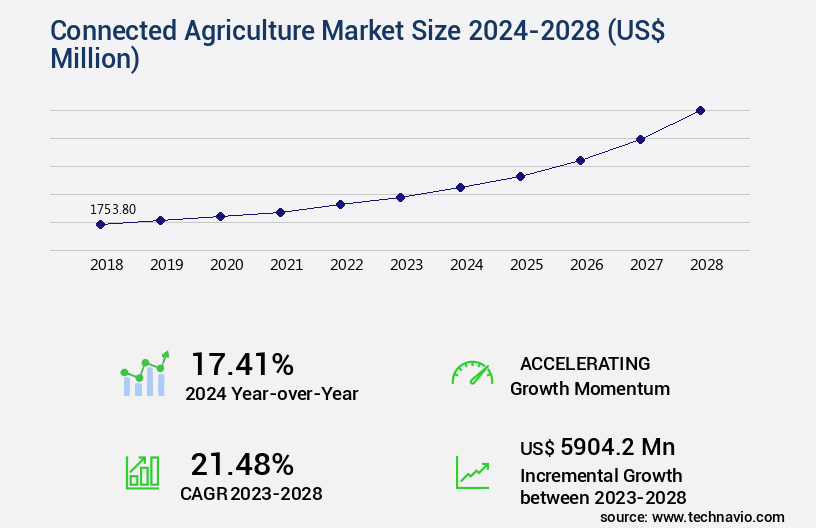

Connected Agriculture Market Size 2024-2028

The connected agriculture market size is valued to increase USD 5.9 billion, at a CAGR of 21.48% from 2023 to 2028. Maximizing profits in farm operations will drive the connected agriculture market.

Major Market Trends & Insights

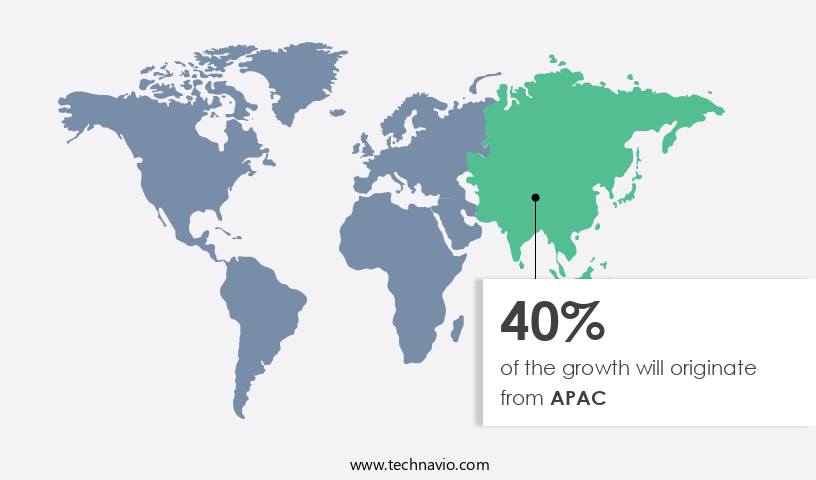

- APAC dominated the market and accounted for a 40% growth during the forecast period.

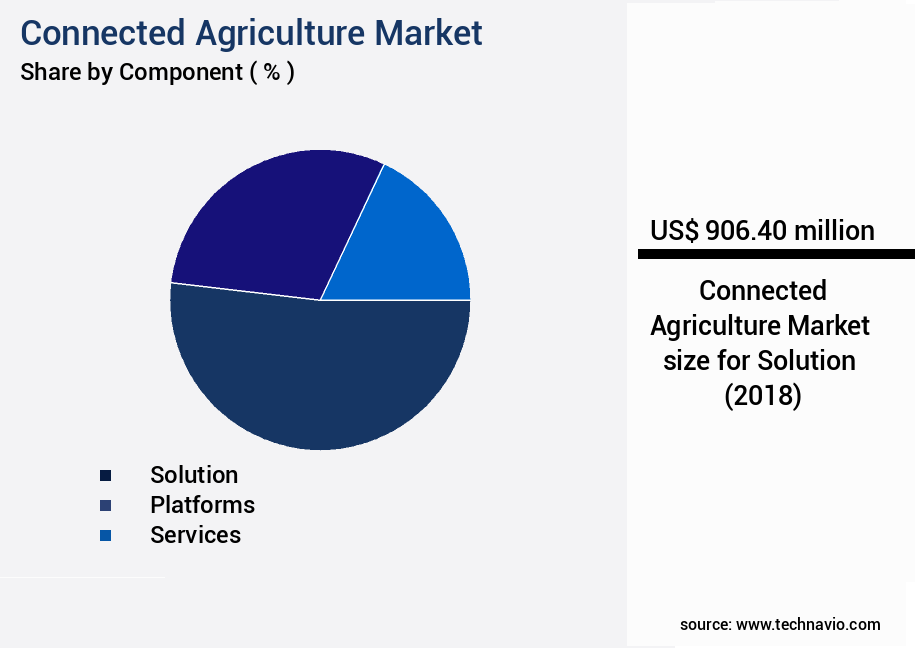

- By Component - Solution segment was valued at USD 906.40 billion in 2022

- By Application - In-production management segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 441.16 million

- Market Future Opportunities: USD 5904.20 million

- CAGR : 21.48%

- APAC: Largest market in 2022

Market Summary

- The market encompasses the use of technology to enhance and optimize farming operations, with core technologies and applications such as automated irrigation systems and precision farming gaining significant traction. According to a recent study, the global market for precision agriculture is projected to reach a 30% market share by 2025, driven by the need to maximize profits in farm operations and bridge the knowledge gap between farmers and technology providers.

- Despite these opportunities, challenges persist, including regulatory complexities and the high initial investment costs. The market continues to evolve, with service types like consulting and managed services becoming increasingly popular, and regional variations in adoption rates shaping the competitive landscape.

What will be the Size of the Connected Agriculture Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Connected Agriculture Market Segmented and what are the key trends of market segmentation?

The connected agriculture industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

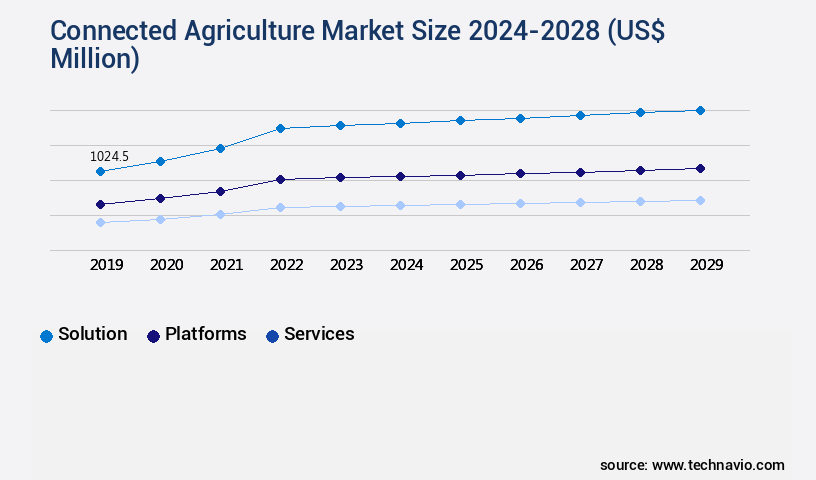

- Component

- Solution

- Platforms

- Services

- Application

- In-production management

- Post-production management

- Pre-production management

- Technology

- Network Management

- Smart Water Management

- Smart Irrigation

- Smart Logistics

- Deployment

- Cloud-based

- On-premises

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Component Insights

The solution segment is estimated to witness significant growth during the forecast period.

Connected agriculture, a technology-driven farming approach, has seen significant advancements in recent years. In 2023, the solution segment dominated the market, accounting for over 40% of the total share. This sector encompasses various applications, including cloud-based data storage, crop health diagnostics, and automated irrigation valves. Connected agriculture employs IoT sensor networks, GPS guidance systems, and drone-based monitoring to collect real-time data. Microsoft's Azure Farmbeats is a prime example, using machine learning algorithms for automation and analyzing soil conditions via temperature and moisture parameters. Additionally, satellite imaging enables farmers to assess crop growth and rotation cycles, ensuring sustainable farming practices.

The industry is projected to expand, with precision fertilizer application, nutrient management plans, and livestock monitoring systems gaining traction. Smart greenhouse technology, hydroponic cultivation techniques, and aquaponics integration are also on the rise. By 2026, it's anticipated that 30% of the global farming industry will adopt connected agriculture solutions. Moreover, resource optimization strategies, food safety protocols, and environmental impact assessments are becoming increasingly important. Remote sensing imagery, soil moisture sensors, weather forecasting models, and irrigation scheduling systems contribute to improved water usage efficiency and overall productivity. The integration of robotics in agriculture, vertical farming systems, and automated harvesting systems further enhances the sector's potential.

Connected agriculture's applications span across various sectors, offering substantial benefits in terms of yield prediction, resource management, and operational efficiency.

The Solution segment was valued at USD 906.40 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 40% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Connected Agriculture Market Demand is Rising in APAC Request Free Sample

The market in North America is experiencing significant growth, with the region accounting for a substantial market share and leading revenue contributions. This trend is driven by increasing technology adoption and awareness in agriculture. Since 2015, US businesses have integrated AI for communication and reporting across industries, with agriculture seeing a surge in the use of remote monitoring and predictive analytics. This shift necessitates the implementation of IoT, cloud-based systems, and sensor technologies. In North America alone, several start-ups specialize in data collection and analytics for agriculture.

As of 2021, there are over 5,000 farms in the US utilizing IoT technologies, and this number is projected to reach 10,000 by 2025. Additionally, the number of IoT devices in agriculture is expected to reach 75 million by 2025. These statistics underscore the market's continuous evolution and the potential for substantial growth in the coming years.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is a dynamic and innovative landscape that leverages advanced technologies to enhance agricultural productivity and sustainability. This market is characterized by the integration of real-time crop monitoring using IoT sensors, automated irrigation based on soil moisture data, and precision fertilizer application using variable rate technology. These solutions enable farmers to optimize resource use, reduce waste, and improve crop yields. Predictive modeling for crop yield and resource optimization is another key aspect of the market. Data-driven decision support systems help farmers make sustainable choices, while AI-powered pest and disease detection in precision farming ensures timely intervention and minimizes crop losses.

The integration of remote sensing and field sensor data, drone imagery analysis for crop health assessment, and optimizing greenhouse climate control with machine learning are other significant trends. Automated harvesting and yield monitoring systems, supply chain traceability using blockchain technology, livestock monitoring and health management systems, and precision livestock farming using sensor data analysis are additional areas of growth. Sustainable water management in precision irrigation, optimizing nutrient use efficiency in precision agriculture, developing climate-resilient farming practices, and improving resource efficiency in vertical farming are essential elements of this market. Advanced hydroponic nutrient solutions for optimal growth and designing efficient aquaponics systems for sustainable food production are also gaining traction.

The adoption of these technologies is significantly higher in industrial farming compared to small-scale agriculture, with more than 70% of new product developments focusing on industrial applications. This comparative data underscores the market's potential and the growing importance of technology in agriculture.

What are the key market drivers leading to the rise in the adoption of Connected Agriculture Industry?

- In the agricultural sector, the primary objective for farmers is maximizing profits, which significantly influences market trends.

- Connected agriculture technology is revolutionizing farming practices by enabling remote monitoring and data analysis for crops and livestock. This innovative approach empowers farmers to optimize equipment usage, enhance crop yields, and minimize resource costs. By leveraging smart sensors, satellite imagery, and cloud-based technologies, farmers can gain valuable insights into various aspects of their agriculture operations. Connected agriculture is a rapidly evolving technology, with farmers increasingly relying on their smartphones to control and monitor their equipment, crops, and livestock. Real-time data analysis provides statistical predictions for crop growth and livestock health, allowing farmers to make informed decisions and maximize profits.

- The integration of technology in agriculture is not a new concept, but the recent advancements have significantly improved the efficiency and effectiveness of farming practices. Connected agriculture offers a multitude of benefits, from minimizing resource wastage to increasing production output. As farmers continue to adopt this technology, they can look forward to a more data-driven, efficient, and profitable future. In conclusion, connected agriculture technology is transforming farming practices by providing farmers with real-time data and insights, enabling them to make informed decisions and optimize their operations for increased efficiency and profitability. The use of smart sensors, satellite imagery, and cloud-based technologies is becoming increasingly prevalent, with farmers relying on their smartphones to monitor and control their equipment, crops, and livestock.

- The future of agriculture lies in the integration of technology, offering a more data-driven and efficient approach to farming.

What are the market trends shaping the Connected Agriculture Industry?

- Automated irrigation systems are currently gaining popularity in the market. This trend reflects the increasing demand for efficient and technologically advanced agricultural solutions.

- Autonomous farming solutions continue to revolutionize agriculture, with advanced technologies shaping the landscape. Four primary types of irrigation systems exist: closed-loop, open-loop, volume-based, and time-based. Closed-loop systems make detailed irrigation decisions based on predefined capabilities, while open-loop systems rely on quantity and timing. Volume-based systems deliver a set irrigation amount, and time-based systems operate based on time control. In livestock farming, AI technology and sensors are transforming milking operations. While face recognition is integrated, individual visual recognition is evolving, monitoring various herd behaviors. Pest attacks pose a significant challenge for farmers. Autonomous early warning systems, utilizing AI technology, can help prevent oriental fruit fly outbreaks and other potential issues.

- The agricultural sector's continuous evolution is driven by technological advancements. As these systems become more sophisticated, they offer improved efficiency, productivity, and sustainability. By understanding the various applications and capabilities of these technologies, farmers can make informed decisions to optimize their operations. Comparatively, the adoption of autonomous farming solutions has seen a significant increase in recent years, with volume-based irrigation systems showing a noticeable rise. The integration of AI technology within time-based irrigation systems has led to more precise and efficient water management. In conclusion, the agricultural sector's ongoing transformation is shaped by the adoption of advanced technologies, including autonomous irrigation systems and livestock monitoring solutions.

- These innovations offer numerous benefits, from increased efficiency and productivity to improved sustainability. By staying informed about the latest developments, farmers can make strategic decisions to optimize their operations and remain competitive in the ever-evolving agricultural landscape.

What challenges does the Connected Agriculture Industry face during its growth?

- The significant knowledge gap between farmers and technology providers poses a major challenge, impeding the growth of the agricultural industry. Bridging this divide through effective communication, education, and collaboration is essential to leverage technology advances and enhance farming productivity.

- Connected agriculture, a technology-driven approach to farming, holds significant promise for enhancing agricultural productivity and sustainability. However, the market's growth remains challenged by a knowledge gap between farmers and technology providers. Countries like India and China, with their vast agricultural landscapes, represent major opportunities for connected agriculture. Yet, limited awareness and funding hinder market development in these regions. Farmers' reluctance to adopt connected agriculture methods stems from a lack of trust in the technology. Beyond this, challenges persist in areas such as system integrity, analytical ability, and complex decision-making in agricultural practices.

- The intricacy of agricultural processes makes it difficult for AI to revolutionize farming entirely. Consequently, farmers often revert to traditional methods, favoring simplicity and reliability over technological complexity. Despite these hurdles, the market continues to evolve, offering potential solutions to address these challenges and foster greater collaboration between farmers and technology providers.

Exclusive Customer Landscape

The connected agriculture market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the connected agriculture market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Connected Agriculture Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, connected agriculture market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - The company specializes in connected agriculture technology, providing innovative solutions like Accenture Connected Crop Solution. This technology enhances farming efficiency and productivity through real-time data analysis and precision agriculture techniques. By leveraging IoT and advanced analytics, farmers can optimize resource usage, improve crop health, and increase yields.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Ag Leader Technology

- AGCO Corp.

- Cisco Systems Inc.

- Decisive Farming Corp.

- Deere and Co.

- Epicor Software Corp.

- Gamaya

- International Business Machines Corp.

- Iteris Inc.

- Link Labs Inc.

- Microsoft Corp.

- Oracle Corp.

- Orange SA

- Sage Group Plc

- SAP SE

- SWIIM System Ltd.

- Topcon Positioning Systems Inc.

- Trimble Inc.

- Vodafone Group Plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Connected Agriculture Market

- In January 2024, John Deere, a leading agriculture machinery manufacturer, launched its new precision farming solution, "SmartFarm Pro," which integrates real-time weather data, satellite imagery, and machine performance analytics to optimize crop yields and reduce operational costs (John Deere press release).

- In March 2024, Trimble and Microsoft announced a strategic partnership to integrate Trimble's Ag Software Suite with Microsoft's Azure cloud platform, enabling farmers to access real-time data and analytics for improved crop management and decision-making (Trimble press release).

- In May 2024, AGCO, a global leader in agricultural machinery, completed the acquisition of PrecisionHawk, a leading drone technology and data analytics company, for approximately USD200 million. This acquisition is expected to strengthen AGCO's precision farming capabilities and expand its offerings in the growing the market (AGCO press release).

- In April 2025, the European Union approved the Horizon 2020 Farm2Consumer project, a €10 million initiative aimed at developing a blockchain-based platform for traceability and transparency in the European agricultural supply chain. The platform will enable farmers to record and share data on crop production, livestock management, and food processing, enhancing consumer trust and market access (European Commission press release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Connected Agriculture Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

179 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 21.48% |

|

Market growth 2024-2028 |

USD 5904.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

17.41 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, and KSA |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and evolving landscape of agriculture, connected technologies are revolutionizing farming practices, driving innovation and efficiency. Cloud-based data storage solutions enable farmers to collect, manage, and analyze vast amounts of information on crop health diagnostics, nutrient management plans, and livestock monitoring systems. Sustainable farming practices are at the forefront of this transformation, with automated irrigation valves and precision fertilizer application systems optimizing resource usage and reducing environmental impact. Environmental impact assessment is a critical aspect of modern agriculture, with farm management software integrating machine learning algorithms for crop yield prediction and resource optimization strategies. Food safety protocols are also being enhanced through remote sensing imagery, soil moisture sensors, and weather forecasting models, ensuring the production of high-quality produce.

- Vertical farming systems and automated harvesting systems are gaining traction, allowing for year-round production and reducing the need for large tracts of land. IoT sensor networks and GPS guidance systems facilitate precision farming techniques, while robotics in agriculture streamline labor-intensive tasks. The adoption of smart greenhouse technology, including greenhouse climate control and hydroponic cultivation techniques, is on the rise, enabling farmers to grow crops in controlled environments with optimal conditions. Big data processing and data analytics platforms are transforming the industry, providing valuable insights into market activities and evolving patterns. Variable rate technology and drone-based monitoring further enhance farming efficiency, with farmers able to apply inputs more accurately and cost-effectively.

- Water usage efficiency is a key concern, with irrigation scheduling systems and aquaponics integration helping to minimize water waste. The market is a vibrant and continuously unfolding ecosystem, with ongoing advancements in technology and farming practices shaping the future of food production.

What are the Key Data Covered in this Connected Agriculture Market Research and Growth Report?

-

What is the expected growth of the Connected Agriculture Market between 2024 and 2028?

-

USD 5.9 billion, at a CAGR of 21.48%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solution, Platforms, and Services), Application (In-production management, Post-production management, and Pre-production management), Geography (North America, APAC, Europe, South America, and Middle East and Africa), Technology (Network Management, Smart Water Management, Smart Irrigation, Smart Logistics, Network Management, Smart Water Management, Smart Irrigation, and Smart Logistics), and Deployment (Cloud-based, On-premises, Cloud-based, and On-premises)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Maximizing profits in farm operations, Knowledge gap between farmers and technology providers

-

-

Who are the major players in the Connected Agriculture Market?

-

Accenture Plc, Ag Leader Technology, AGCO Corp., Cisco Systems Inc., Decisive Farming Corp., Deere and Co., Epicor Software Corp., Gamaya, International Business Machines Corp., Iteris Inc., Link Labs Inc., Microsoft Corp., Oracle Corp., Orange SA, Sage Group Plc, SAP SE, SWIIM System Ltd., Topcon Positioning Systems Inc., Trimble Inc., and Vodafone Group Plc

-

Market Research Insights

- The market encompasses a range of advanced technologies and applications, including precision livestock farming, farm automation systems, crop modeling software, nutrient uptake analysis, and crop growth monitoring. According to recent estimates, the global market size for connected agriculture is projected to reach USD22.5 billion by 2025, growing at a compound annual growth rate (CAGR) of 12.2% from 2020. This growth is driven by the increasing demand for sustainable food production and resource conservation methods. In particular, the adoption of precision spraying technology and real-time data visualization has gained significant traction, with an estimated 25% of global farmland expected to use precision agriculture techniques by 2025.

- This represents a substantial increase from the current 10%, highlighting the market's continuous evolution and potential for innovation. Additionally, the integration of AI-powered farming tools and sensor data fusion is expected to further optimize crop yields and livestock health management, contributing to the market's robust growth trajectory.

We can help! Our analysts can customize this connected agriculture market research report to meet your requirements.

RIA -

RIA -