Endometriosis Drugs Market Size 2025-2029

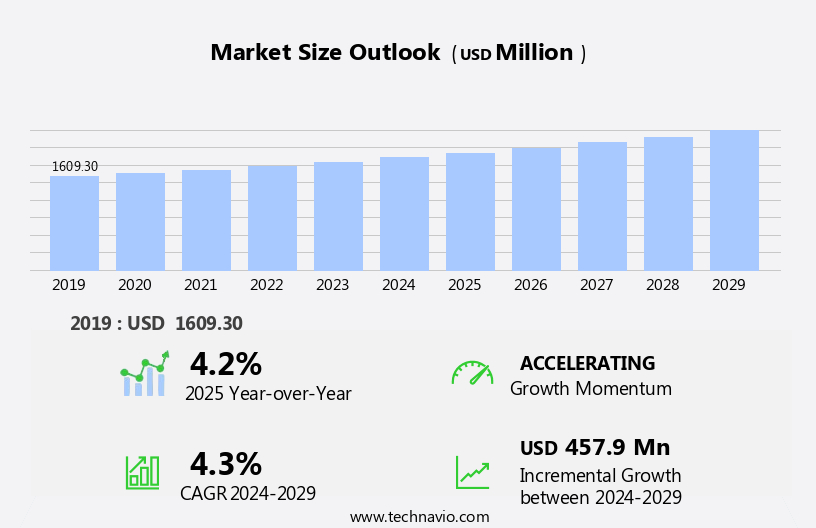

The endometriosis drugs market size is forecast to increase by USD 457.9 million at a CAGR of 4.3% between 2024 and 2029.

- The market is driven by the increasing prevalence of endometriosis and advancements in diagnostic techniques, leading to earlier identification and treatment. A strategic shift towards non-hormonal therapeutic pathways is also a significant trend, as these treatments offer advantages over hormonal therapies in terms of long-term efficacy and fewer side effects. Infertility drugs, such as prescription medications, are widely used to address these issues. However, the market faces challenges, including the high cost of novel therapies and stringent reimbursement hurdles, which may limit patient access and affordability.

- Companies seeking to capitalize on market opportunities must focus on developing cost-effective, non-hormonal therapies and navigating complex regulatory environments to secure reimbursement for their products. Effective collaboration with healthcare providers, patient advocacy groups, and payers can also help address affordability concerns and expand market reach. The pipeline analysis includes gene therapy, digital health, and telemedicine, aiming to improve treatment duration and patient experience.

What will be the Size of the Endometriosis Drugs Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

Endometriosis, a chronic condition characterized by hormonal imbalance and immune system dysfunction, affects an estimated 176 million women worldwide, leading to significant disease burden and economic impact. Mortality rates are low, but the disease can cause debilitating pain, infertility, and other health complications. Access to care remains a challenge for many, particularly those in underserved communities, due to health disparities and limited reimbursement policies. Support groups and academic centers play crucial roles in providing resources and advocacy for patients. Surgical specialists and reproductive endocrinologists are often involved in diagnosis and treatment, while research institutions and pharmaceutical companies invest in developing new drugs and prevention strategies.

Complementary therapies, such as stress management, psychological counseling, and physical therapy, can help manage symptoms and improve long-term outcomes. Prevalence rates of endometriosis are influenced by various factors, including genetic predisposition, environmental factors, and lifestyle choices. Early detection and intervention are key to reducing the disease's impact on patients' lives. Healthcare policy and health insurance coverage are essential in ensuring access to care for all women. Drug pricing and reimbursement policies are ongoing concerns for patients and healthcare professionals. Prevention strategies, such as dietary supplements and lifestyle modifications, can help reduce the risk of developing endometriosis.

Medical device companies and pain specialists offer alternative treatment options for those who do not respond to traditional hormonal therapies. Public health initiatives and patient advocacy groups aim to raise awareness and promote research into the causes and treatments of endometriosis. The women's health therapeutics market encompasses a range of interventions aimed at managing hormonal imbalances, mental health concerns, and chronic diseases.

How is this Endometriosis Drugs Industry segmented?

The endometriosis drugs industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Hormone therapy

- Analgesics

- Route Of Administration

- Oral

- Injectables

- Others

- Distribution Channel

- Retail pharmacy

- Hospital pharmacy

- Online pharmacy

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Product Insights

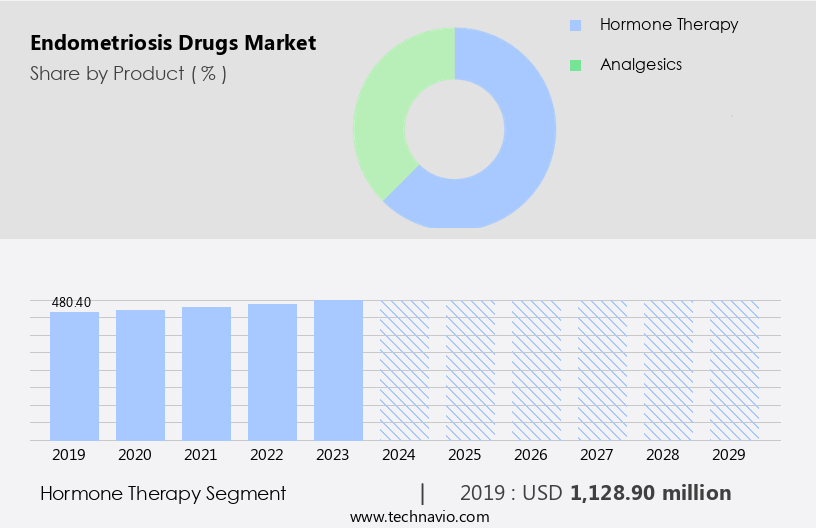

The Hormone therapy segment is estimated to witness significant growth during the forecast period. The market is primarily driven by hormone therapy, which functions as the cornerstone of treatment by managing the disease's progression and alleviating symptoms. Hormone therapy's fundamental principle revolves around modulating the female hormonal cycle, specifically suppressing estrogen, which fuels the growth and inflammation of ectopic endometrial lesions. Inducing a hypoestrogenic state, these therapies starve the lesions of their growth stimulus, leading to regression and symptom relief. This segment includes various drug classes, each with distinct mechanisms, delivery routes, and clinical profiles. Combination hormone therapy, a common approach, combines estrogen and progestin to mimic the natural menstrual cycle, reducing the risk of side effects. Lastly, non-drug alternatives, including herbal remedies and menstrual cups, are gaining popularity as more women seek natural and eco-friendly options.

Gonadotropin-releasing hormone agonists (GnRH agonists) induce a menopausal state, while gonadotropin-releasing hormone antagonists (GnRH antagonists) prevent the release of gonadotropins, inhibiting ovulation and estrogen production. Aromatase inhibitors, another class, prevent the conversion of androgens to estrogen. Adjunctive therapies, such as non-steroidal anti-inflammatory drugs (NSAIDs) and opioids, are often used to manage pain. Oral contraceptives and ovulation induction drugs, while not primary hormone therapies, can also help manage symptoms and improve fertility. Surgical intervention, including laparoscopic surgery and endometrial ablation, can provide long-term relief for some patients. Patient adherence is crucial for treatment success, as hormone therapies require consistent use for optimal results. The increasing prevalence of breast cancer is driving the demand for progesterone drugs as they are used in hormone replacement therapy and cancer treatment.

Each approach offers unique benefits and challenges, necessitating careful consideration and ongoing management to optimize patient outcomes.

The Hormone therapy segment was valued at USD 1128.90 million in 2019 and showed a gradual increase during the forecast period.

The Endometriosis Drugs Market is expanding significantly due to increased awareness, improved diagnostics, and evolving treatment strategies. Shifts in lifestyle factorsâsuch as delayed childbearing, sedentary habits, and diet are believed to influence hormone levels, potentially triggering endometrial tissue growth outside the uterus. This contributes to rising incidence rates, particularly among women of reproductive age. Global epidemiology studies reveal notable regional variations in disease prevalence, with underdiagnosis still common in many areas due to a lack of awareness and medical access. Drug interactions with other medications, such as anticoagulants and antidepressants, can impact treatment efficacy and require careful monitoring.

Disease progression and associated complications, including ovarian cysts, ectopic pregnancy, heavy menstrual bleeding, and chronic pelvic pain, necessitate ongoing care and management. Regulatory approval, healthcare costs, and patient education are critical factors influencing market access and treatment decisions. Clinical trials and diagnostic imaging, including transvaginal ultrasound and genetic testing, are essential tools for diagnosing and monitoring the disease. Intrauterine insemination (IUI) and preterm birth are potential complications for patients undergoing fertility treatments. In summary, the market is characterized by a diverse range of treatment options, from hormone therapies to surgical interventions and adjunctive therapies.

Regional Analysis

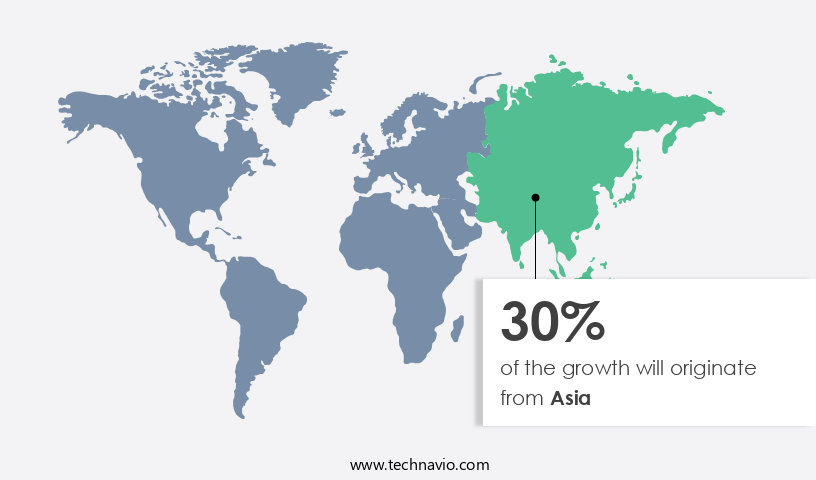

Asia is estimated to contribute 30% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is currently the largest and most valuable segment due to several factors. The high prevalence of diagnosed endometriosis, substantial healthcare expenditure per capita, a well-established pharmaceutical industry, and a robust patient advocacy framework contribute to this dominance. In the United States, the premium pricing environment for novel pharmaceuticals and extensive direct-to-consumer advertising fuel market growth by elevating patient awareness and encouraging consultations. The commercial landscape is marked by the significant influence of private payers and Pharmacy Benefit Managers (PBMs), whose formulary decisions impact treatment accessibility and affordability. Combination hormone therapy and oral contraceptives are commonly used to manage symptoms and slow disease progression. Diagnostic procedures like ultrasound, laparoscopy, and CT scan help in diagnosis.

Gonadotropin-releasing hormone agonists and antagonists are also employed for symptomatic relief and to prevent ovulation. Aromatase inhibitors and ovulation induction drugs are utilized in treating endometriosis-associated infertility. Disease awareness campaigns and patient education initiatives play a crucial role in improving treatment efficacy and patient adherence. Diagnostic imaging, genetic testing, and laparoscopic surgery are essential for accurate diagnosis and surgical intervention. Adjunctive therapies, such as non-opioid analgesics and intrauterine insemination (IUI), are employed to manage pain and support fertility. Market access and regulatory approval are critical factors influencing the adoption of new treatments. Soybeans derivatives and Dioscorea villosa are among the natural sources of progesterone, while synthetic production methods are also utilized. Clinical trials, transvaginal ultrasound, and ectopic pregnancy management are integral components of the drug development process.

Patient reported outcomes and chronic pelvic pain studies contribute to understanding treatment efficacy and quality of life improvements. Healthcare costs, ovarian cysts, heavy menstrual bleeding, and pregnancy complications are significant concerns for patients and payers. Uterine fibroid embolization and endometrial ablation are alternative treatment options for managing symptoms. Drug interactions and adverse effects necessitate careful consideration when prescribing treatments. In summary, the market in North America is driven by a combination of factors, including high prevalence, substantial healthcare expenditure, robust industry, and patient advocacy. The landscape is characterized by the influence of private payers, PBMs, and the significant role of combination hormone therapy, oral contraceptives, and surgical interventions in managing symptoms and improving quality of life.

Ongoing research and clinical trials contribute to the development of novel treatments and a better understanding of disease progression and patient outcomes.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Endometriosis Drugs market drivers leading to the rise in the adoption of Industry?

- The market's growth is primarily attributed to the rising disease prevalence and advancements in diagnostic techniques. The market is driven by the significant prevalence of endometriosis, estimated to affect around 190 million women and girls worldwide, and advancements in diagnostic technology and awareness. Historically, this large patient population has been underserved due to social stigma, lack of public awareness, and healthcare system challenges, leading to lengthy diagnostic delays averaging seven to ten years.

- Endometriosis can also lead to disease progression, endometriosis-associated infertility, and the need for surgical intervention. Adherence to treatment is crucial for managing symptoms and preventing disease progression. Despite the availability of various treatment options, including endometrial ablation, patients may experience adverse effects, necessitating ongoing research and development for more effective and tolerable therapies. The market is driven by the increasing prevalence of hormonal disorders, such as endometriosis, infertility, and menopause. Additionally, the growing awareness of the role of hormones, including progesterone, in breast cancer and other cancers, as well as precursor lesions, is fueling demand for progesterone-based treatments.

What are the Endometriosis Drugs market trends shaping the Industry?

- The strategic shift towards non-hormonal therapeutic pathways is gaining momentum in the healthcare industry. It is essential for professionals to stay informed about this market trend and explore potential treatment options outside of hormonal therapies. The market is witnessing a significant shift in treatment approaches, moving away from the long-standing reliance on hormonal suppression towards the development of non-hormonal therapeutic agents. Traditional treatments, such as gonadotropin-releasing hormone (GnRH) agonists and antagonists, as well as oral contraceptives, have been the mainstay of pharmacologic management for decades. These therapies provide pain relief for many patients but are associated with limitations, including side effects leading to high discontinuation rates.

- Chronic pelvic pain, preterm birth, and uterine fibroid embolization are among the key challenges addressed by the market. Ovulation induction and other fertility-focused treatments are also areas of interest, as endometriosis significantly impacts fertility in many women. The market dynamics are driven by the unmet need for more effective and side effect-friendly treatments, the increasing understanding of the disease's complexities, and the ongoing research and development efforts in this field. Clinical trials are ongoing for various non-hormonal therapies, including aromatase inhibitors, which inhibit the production of estrogen, and agents targeting the endocannabinoid system. Diagnostic imaging and genetic testing are also playing increasingly important roles in the accurate identification and staging of endometriosis, enabling more targeted and effective treatments.

How does Endometriosis Drugs market face challenges during its growth?

- The high cost of novel therapies and stringent reimbursement hurdles pose a significant challenge to the growth of the industry. These factors necessitate careful consideration and strategic planning to ensure the affordability and accessibility of innovative healthcare solutions. The market faces a significant challenge due to the high costs of novel therapeutic agents, which can limit patient access due to stringent reimbursement policies and payer cost-containment strategies. The shift from low-cost, repurposed generic medications to specifically developed, branded specialty drugs, such as oral gonadotropin-releasing hormone (GnRH) antagonists, offers clinical benefits but comes with a premium price tag.

- Patient education plays a crucial role in managing endometriosis, with non-opioid analgesics, intrauterine insemination (IUI), and laparoscopic surgery being common treatment options. Patient-reported outcomes and transvaginal ultrasound are essential tools for diagnosing and monitoring the disease. Despite these advancements, pregnancy complications remain a concern for women with endometriosis, necessitating ongoing research and development. These delays have suppressed the treatable market size. Endometriosis is characterized by the growth of endometrial tissue outside the uterus, resulting in symptoms such as ovarian cysts, pain management, heavy menstrual bleeding, and ectopic pregnancy.

Exclusive Customer Landscape

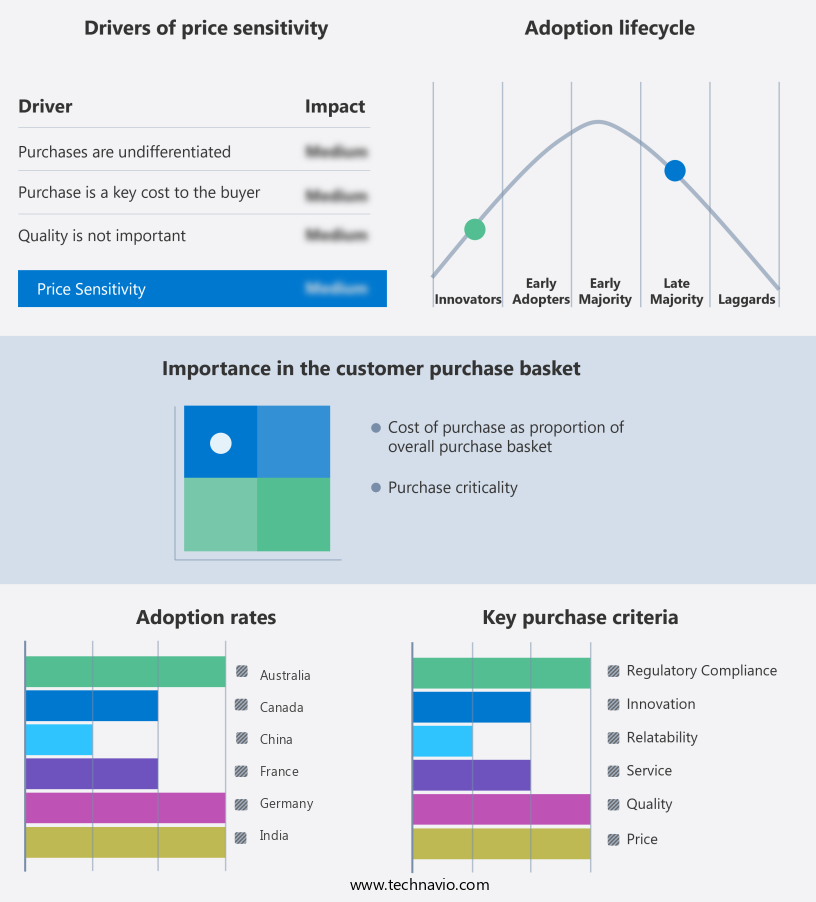

The endometriosis drugs market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the endometriosis drugs market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, endometriosis drugs market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbbVie Inc. - The company specializes in endometriosis drugs and offers two oral dosage strengths of Orilissa for treatment: 150 mg once daily and 200 mg twice daily.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Ananda Pharma

- Bayer AG

- Debiopharm International SA

- Enteris BioPharma Inc.

- Gedeon Richter Plc

- Gesynta Pharma AB

- Hope Medicine

- Johnson and Johnson Services Inc.

- Kissei Pharmaceutical Co. Ltd.

- Neurocrine Biosciences Inc.

- Nippon Shinyaku Co. Ltd.

- Novartis AG

- Organon and Co.

- Pfizer Inc.

- Sanofi SA

- Takeda Pharmaceutical Co. Ltd.

- Teva Pharmaceutical Industries Ltd.

- Viramal Ltd

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Endometriosis Drugs Market

- In January 2024, Pfizer Inc. announced the US Food and Drug Administration (FDA) approval of Lupron Depot for Endometriosis-Associated Pain (Lupron DA), marking a significant advancement in the treatment of endometriosis symptoms (Pfizer Press Release, 2024).

- In March 2024, AbbVie and Endo Pharmaceuticals entered into a collaboration to co-promote Andrographis Panayottis extract, an investigational treatment for endometriosis-related pain, in the US market. This strategic partnership combines AbbVie's marketing expertise with Endo's clinical expertise, potentially accelerating the product's commercialization (AbbVie Press Release, 2024).

- In May 2024, Merck KGaA secured European Commission approval for Orlissa (felbamate), a new treatment for endometriosis-associated pain. This approval expands the product's availability beyond the US market, making it accessible to more patients in Europe (Merck KGaA Press Release, 2024).

- In April 2025, AstraZeneca announced the completion of a USD 1.3 billion investment in its global R&D center in Cambridge, UK, which includes a dedicated research unit for endometriosis. This significant investment underscores the company's commitment to advancing treatments for endometriosis and other women's health conditions (AstraZeneca Press Release, 2025).

Research Analyst Overview

The market continues to evolve, driven by ongoing research and development in various sectors. Combination hormone therapy, including gonadotropin-releasing hormone agonists and antagonists, remains a cornerstone of treatment. Disease awareness campaigns aim to improve symptom recognition and drive earlier intervention. Treatment efficacy and quality of life are key considerations, with adjunctive therapies such as aromatase inhibitors and pain management strategies gaining attention. Drug interactions and adverse effects are ongoing concerns, necessitating careful consideration in clinical trials and regulatory approval processes. Ovarian cysts, heavy menstrual bleeding, and endometriosis-associated infertility are common challenges, leading to a diverse range of therapeutic approaches.

Ovulation induction, diagnostic imaging, genetic testing, and chronic pelvic pain management are among the areas of active research. Market access and patient adherence are critical factors, with healthcare costs and patient education playing important roles. Surgical intervention, such as laparoscopic surgery and endometrial ablation, offer alternatives to drug therapy. Ongoing clinical trials explore new treatments, including non-opioid analgesics and intrauterine insemination (IUI). Preterm birth, ectopic pregnancy, and pregnancy complications are areas of ongoing research, with a focus on improving patient outcomes. Drug development and regulatory approval processes continue to unfold, with a focus on addressing disease progression and improving patient care.

The market remains dynamic, with ongoing research and innovation shaping the landscape. These high prices impose a substantial economic burden on healthcare systems, particularly in regions with single-payer structures and in the US, where Pharmacy Benefit Managers (PBMs) and private insurers have significant market access control.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Endometriosis Drugs Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

229 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.3% |

|

Market growth 2025-2029 |

USD 457.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.2 |

|

Key countries |

US, UK, China, Germany, Canada, Japan, France, India, Australia, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Endometriosis Drugs Market Research and Growth Report?

- CAGR of the Endometriosis Drugs industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the endometriosis drugs market growth of industry companies

We can help! Our analysts can customize this endometriosis drugs market research report to meet your requirements.

RIA -

RIA -