Europe Cyber Security Market Size 2025-2029

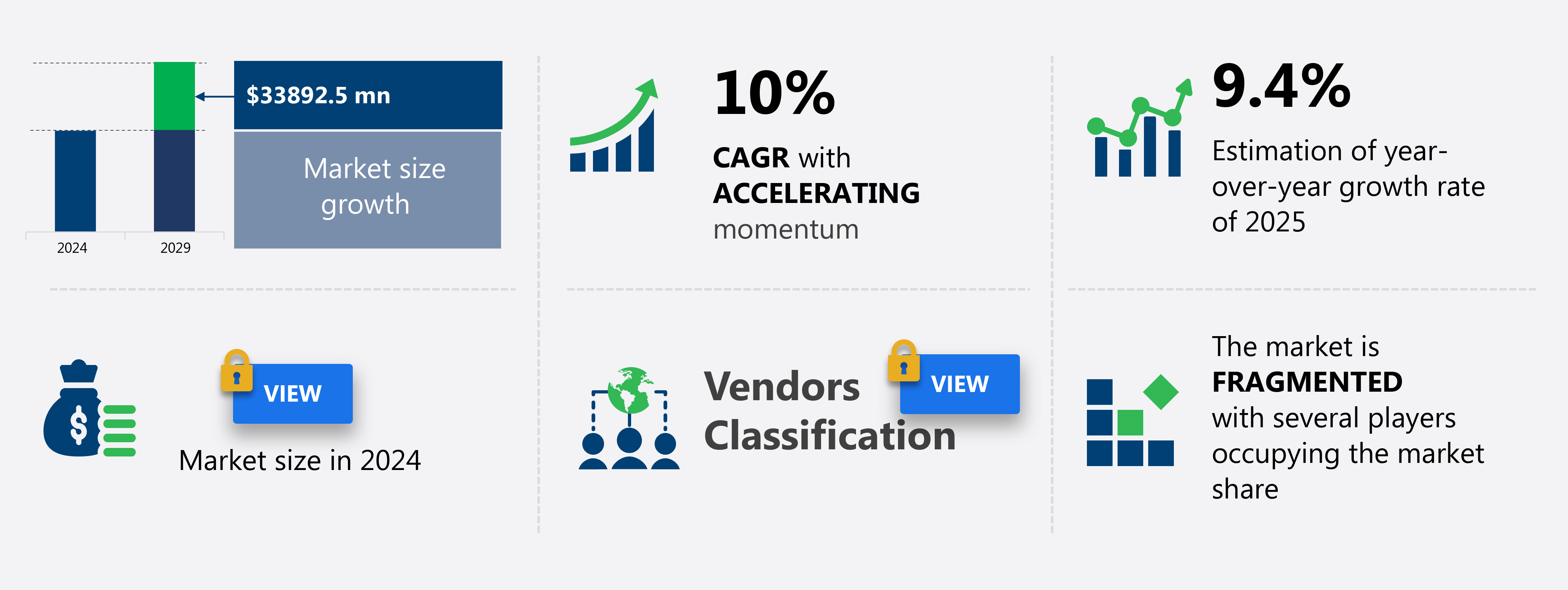

The Europe cyber security market size is forecast to increase by USD 33.89 billion at a CAGR of 10% between 2024 and 2029.

- The Cyber Security Market is experiencing significant shifts as the sophistication and volume of cyber threats continue to escalate. Malicious actors employ advanced techniques, such as AI and machine learning, to bypass traditional security measures, posing a constant challenge for organizations. In response, there is a growing trend toward platform consolidation, with Extended Detection and Response (XDR) and Secure Access Service Edge (SASE) architectures gaining traction. These solutions offer integrated threat detection and response capabilities, enhancing security posture and improving incident response times.

- This skills gap leaves many vulnerable to attacks and underscores the need for innovative recruitment strategies, training programs, and partnerships to address this issue. Companies seeking to capitalize on market opportunities and navigate challenges effectively must stay informed of emerging threats and invest in advanced technologies and talent development initiatives. However, the market's dynamic landscape also presents challenges. The critical shortage of cyber security skills and talent persists, making it difficult for organizations to effectively defend against cyber threats. One such solution is a cloud workload protection platform, which safeguards cloud-based infrastructure from threats.

What will be the size of the Europe Cyber Security Market during the forecast period?

Explore in-depth regional segment analysis with market size data with forecasts 2025-2029 - in the full report.

Request Free Sample

- The market for cyber security solutions continues to evolve, with new threats and vulnerabilities emerging constantly. Email security gateways and endpoint security solutions are essential for safeguarding against phishing emails and malware attacks. Security architecture design incorporates threat modeling techniques, risk assessment methodologies, and authentication protocols to create robust systems. Log management systems and incident management processes enable businesses to respond effectively to security breaches. A recent study revealed a 300% increase in distributed denial service attacks in the past year, highlighting the importance of network traffic analysis and intrusion prevention systems. Encryption algorithms and security orchestration automation are crucial for maintaining data security and ensuring business continuity planning.

- Compliance and regulations, such as GDPR and HIPAA, necessitate the implementation of password management systems, mobile device management, and data governance frameworks. Moreover, the cyber security market is expected to grow by 12% annually, driven by the increasing adoption of security analytics platforms, web application firewalls, and social media security solutions. Vulnerability management programs, authorization policies, and data masking techniques are also gaining popularity as businesses prioritize securing their digital assets.

How is this Europe Cyber Security Market segmented?

The Europe cyber security market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029,for the following segments.

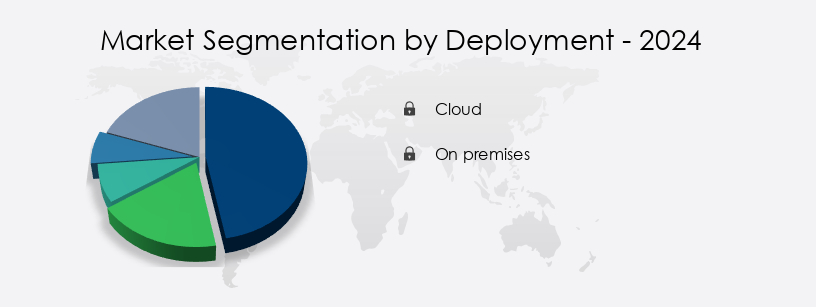

- Deployment

- Cloud

- On premises

- Component

- Solutions

- Services

- Sector

- Large enterprises

- SMEs

- Type

- Network

- Cloud

- End-point and IOT

- Application

- End-user

- Government

- BFSI

- ICT

- Manufacturing

- Others

- Geography

- Europe

- France

- Germany

- Italy

- UK

- Europe

By Deployment Insights

The Cloud segment is estimated to witness significant growth during the forecast period. The European cyber security market is witnessing significant growth, with cloud-based deployment, or Security as a Service (SaaS,) leading the way. In this model, security solutions are delivered over the internet as a subscription-based service, offering numerous advantages aligned with current business and IT trends. One major advantage is the financial benefit of transitioning from capital expenditure (CapEx) to operational expenditure (OpEx), eliminating large upfront investments and providing scalable, predictable costs. This makes advanced security capabilities more accessible to organizations of all sizes, including small and medium-sized enterprises (SMEs), a significant sector in Europe's economy. Zero trust security, ransomware prevention strategies, and security automation tools are integral components of this evolving market.

Enterprises are also applying a thorough risk assessment methodology and streamlined incident management process to ensure operational resilience. A solid data governance framework supports compliance, while a structured vulnerability management program and security awareness training programs empower employees against attacks. Tools like log management system, security analytics platform, and intrusion prevention system help monitor and respond to threats. Solutions like secure remote access, email security gateway, and web application firewall protect endpoints, and phishing email detection strengthens user protection. For internal controls, password management system and data backup and recovery are deployed.

According to recent industry reports, the European cyber security market is expected to grow by over 12% annually, underscoring its importance in safeguarding digital assets and ensuring business continuity. For instance, a large financial institution implemented a cloud-based intrusion detection system, resulting in a 35% reduction in false positives and a 40% decrease in mean time to detect and respond to threats. This success story highlights the potential of cloud-based cyber security solutions to enhance security while optimizing costs.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage. The cyber security market is experiencing robust growth due to the increasing number of advanced persistent threats (APTs) targeting businesses worldwide. These threats often bypass traditional security measures, making it crucial for organizations to invest in advanced solutions. Another essential aspect of cybersecurity is ensuring security throughout the software development lifecycle. Secure software development practices, such as secure coding best practices and application security testing tools, are vital in preventing vulnerabilities.

Data loss prevention (DLP) implementation best practices are essential for protecting sensitive information. Zero trust architecture and behavioral analytics for security are becoming increasingly popular in mitigating risks. Ransomware attacks are a significant concern, and organizations must deploy robust strategies, such as network security monitoring tools and vulnerability management lifecycle, to minimize their impact. Artificial intelligence (AI) and machine learning (ML) are transforming cybersecurity. AI and ML for threat detection enable organizations to proactively identify and respond to threats. Phishing awareness training modules are also essential in preventing social engineering attacks. Lastly, security automation and orchestration are streamlining security operations, making them more efficient and effective.

The Cyber Security Market in Europe is experiencing robust growth, driven by increasing digital transformation and the rising complexity of cyber threats. Organizations are prioritizing vulnerability assessment and implementing security information event management systems to gain real-time visibility into threats. A robust risk management framework is being adopted across enterprises to manage evolving cyber risks. To secure sensitive data, businesses are utilizing advanced data encryption methods and cloud security posture management tools. The use of software defined perimeter enhances secure access, while artificial intelligence security and machine learning security enable automated threat detection and mitigation. In response to breaches, digital forensics incident response and privileged access management have become critical functions.

The cybersecurity market is continuously evolving, with organizations requiring a comprehensive approach to security. From APT detection to incident response and ransomware attack mitigation, investing in advanced solutions and best practices is crucial for businesses to protect their digital assets. However, even with the best precautions, breaches can still occur. In such cases, an effective incident response strategy, including identity and access management solutions and multi-factor authentication deployment, is crucial.

What are the Europe Cyber Security Market drivers leading to the rise in adoption of the Industry?

- The escalating complexity and quantity of cyber threats serve as the primary catalyst for market growth. The European cyber security market experiences persistent growth due to the evolving and complex cyber threat landscape. Malicious actors, including cybercriminals, organized crime syndicates, and state-sponsored groups, employ advanced and persistent attack methodologies. Ransomware attacks have evolved, with attackers not only encrypting data but also exfiltrating sensitive information and threatening to publish it or launch denial of service attacks.

- For instance, a recent ransomware attack on a European organization resulted in a 10% sales loss and significant reputational damage. This underscores the importance of investing in comprehensive cyber security measures to protect against these evolving threats. This new paradigm of targeted and strategic cyber warfare necessitates robust cyber security solutions. The market is expected to grow by 12% in the next year, reflecting the market's dynamic and ever-evolving nature.

What are the Europe Cyber Security Market trends shaping the Industry?

- Platform consolidation is a mandated trend in the market, with XDR and SASE architectures being the primary targets. The European cyber security market is experiencing a significant shift towards integrated platforms, with Extended Detection and Response (XDR) and Secure Access Service Edge (SASE) emerging as dominant trends. Traditional security approaches, characterized by fragmented and complex stacks of disconnected point solutions, have resulted in operational inefficiencies and high costs for organizations. These challenges include alert fatigue, critical visibility gaps, and excessive total cost of ownership.

- According to recent research, the European cyber security market is expected to grow by over 12% in the next year, reflecting the increasing demand for integrated solutions. A notable example of this trend is a large financial institution's successful implementation of an XDR platform, resulting in a 20% reduction in security incidents and a 30% decrease in false positives. The market is now moving away from the best-of-breed, siloed approach, favoring a more unified and platform-centric model instead.

How does Europe Cyber Security Market face challenges during its growth?

- The critical shortage of talent with advanced cyber security skills poses a significant challenge to the growth and development of the industry. The European cyber security market faces a significant hurdle in realizing its full potential due to the persistent and deep-rooted shortage of qualified professionals. This issue is not cyclical but structural, affecting organizations of all sizes and sectors. The demand for cyber security experts, particularly in areas such as cloud security, threat intelligence, incident response, and security engineering, significantly exceeds the available talent pool.

- For instance, a recent survey revealed that over 60% of European organizations reported having a shortage of cyber security skills, with 36% stating that this shortage had increased over the past year. The cyber security workforce shortage is expected to reach 3.5 million by 2021, according to a report by Cybersecurity Ventures. This skills gap not only increases the risk of cyber attacks but also hampers the ability of organizations to respond effectively to threats and maintain an optimal security posture. This talent gap fuels a highly competitive and expensive labor market, making it challenging for many organizations, including small and medium-sized enterprises (SMEs) and public sector bodies, to recruit and retain the necessary expertise to manage their security posture effectively.

Exclusive Europe Cyber Security Market Customer Landscape

The Europe cyber security market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

AO Kaspersky Lab - The company specializes in advanced cybersecurity solutions, providing endpoint protection, hybrid cloud security, anti-targeted attack platforms, and fraud prevention services to safeguard businesses against evolving digital threats.

The Europe cyber security market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AO Kaspersky Lab

- Atos SE

- BAE Systems Plc

- Capgemini Service SAS

- Check Point Software Technologies Ltd.

- Cisco Systems Inc.

- Darktrace Holdings Ltd.

- Deutsche Telekom AG

- ESET North America

- F Secure Corp.

- International Business Machines Corp.

- Orange Cyberdefense SA

- Palo Alto Networks Inc.

- Prosegur Compania de Seguridad SA

- S.C. BITDEFENDER S.R.L

- secunet Security Networks AG

- Sophos Ltd.

- Stormshield

- Symantec

- Trend Micro Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cyber Security Market In Europe

- In January 2024, IBM Security announced the acquisition of Reason Software, a leading behavioral analytics company, to strengthen its X-Force Threat Intelligence portfolio. The deal was valued at USD 400 million, as reported by Reuters (Reuters, 2024).

- In March 2024, Microsoft and Google joined forces to enhance their cloud security offerings. They announced a strategic partnership to integrate Microsoft's Azure Security Center with Google Cloud Platform, as stated in a Microsoft press release (Microsoft, 2024).

- In May 2024, CrowdStrike Holdings, Inc. Raised USD 1.1 billion in an initial public offering (IPO), making it the largest tech IPO of the year. The offering was oversubscribed, reflecting the growing demand for cybersecurity solutions, as reported by Bloomberg (Bloomberg, 2024).

- In February 2025, the European Union (EU) enacted the new Digital Services Act, which includes stricter cybersecurity regulations for digital service providers. The act aims to improve online safety and protect users' data, as outlined in an EU press release (EU, 2025).

Research Analyst Overview

The cybersecurity market continues to evolve, with new threats and vulnerabilities emerging constantly. Risk management frameworks, such as NIST and ISO, provide a systematic approach to identifying, assessing, and mitigating cyber risks. Zero trust security, for instance, has gained traction, shifting the focus from perimeter security to securing access to individual resources. Threat hunting strategies and intrusion detection systems, fueled by machine learning and artificial intelligence, are increasingly being used to proactively identify and respond to advanced threats. Data loss prevention and encryption methods are essential for safeguarding sensitive information. Predictive threat modeling and application security testing help identify vulnerabilities before they can be exploited.

Cybersecurity awareness training, behavioral analytics security, and social engineering defense are crucial components of a robust security strategy. Software defined perimeters, network security monitoring, secure coding practices, and blockchain security protocols offer additional layers of protection. Penetration testing services and vulnerability assessments help organizations identify and address weaknesses. Industry growth in cybersecurity is expected to reach double digits, with businesses investing heavily in advanced security technologies. For instance, a leading financial services company reported a 50% increase in phishing attack detection using a threat intelligence platform and multi-factor authentication. Endpoint detection response and incident response planning are also critical for minimizing the impact of cyber attacks.

Emerging threats are countered with advanced persistent threat detection and secure software development lifecycle. Key technologies such as endpoint detection and response system, security information and event management system, and data loss prevention implementation best practices are mainstream. The region is embracing zero trust architecture implementation, multi-factor authentication deployment strategies, effective incident response strategies, and ransomware attack mitigation techniques. Additionally, developers are trained in secure coding best practices for developers, while artificial intelligence for cybersecurity and machine learning for threat detection are redefining proactive defense mechanisms across the region.

Data breach notification and access control management are essential for maintaining regulatory compliance. Malware analysis techniques and ransomware prevention strategies are key to staying ahead of evolving threats. Security automation tools are transforming the landscape, streamlining processes and improving efficiency.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cyber Security Market in Europe insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

232 |

|

Base year |

2024 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10% |

|

Market growth 2025-2029 |

USD 33.89 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

9.4 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Europe

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -