Fuel Cells Market For Industrial And Mlitary Applications Size 2025-2029

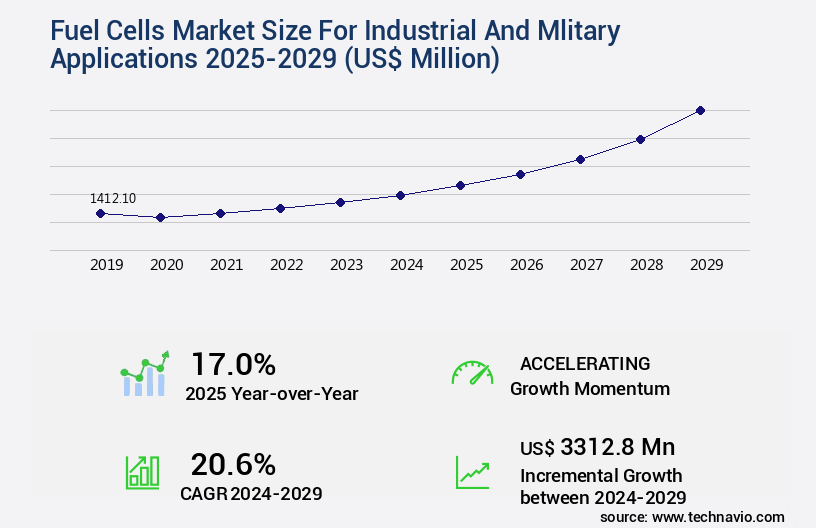

The fuel cells market for industrial and mlitary applications size is valued to increase by USD 3.31 billion, at a CAGR of 20.6% from 2024 to 2029. Growing demand for efficient and cleaner technologies will drive the fuel cells market for industrial and mlitary applications.

Market Insights

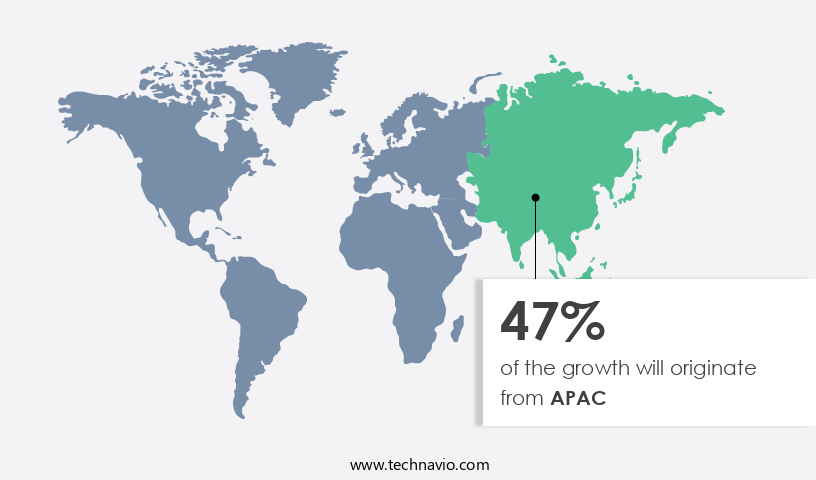

- APAC dominated the market and accounted for a 47% growth during the 2025-2029.

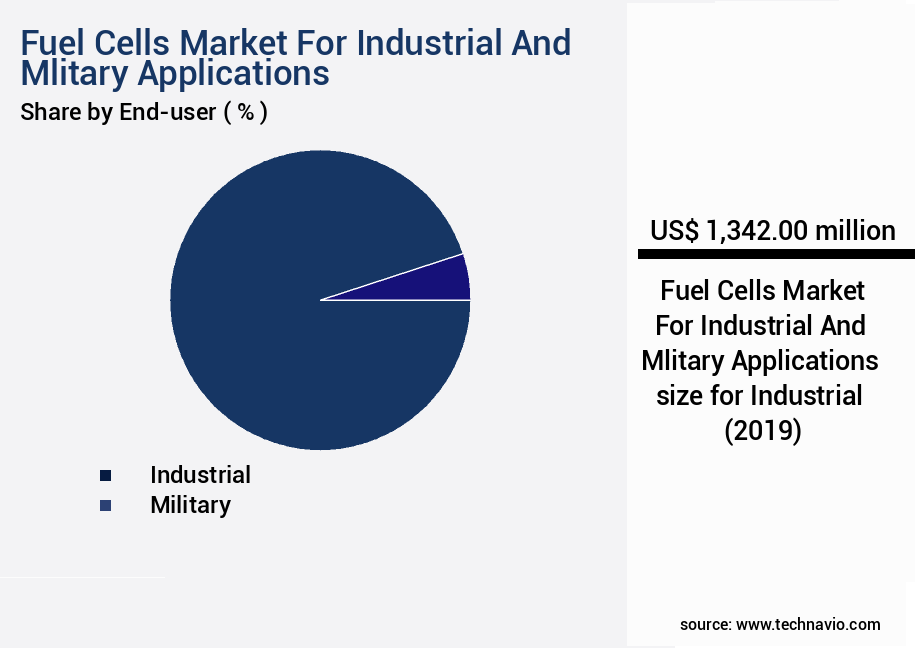

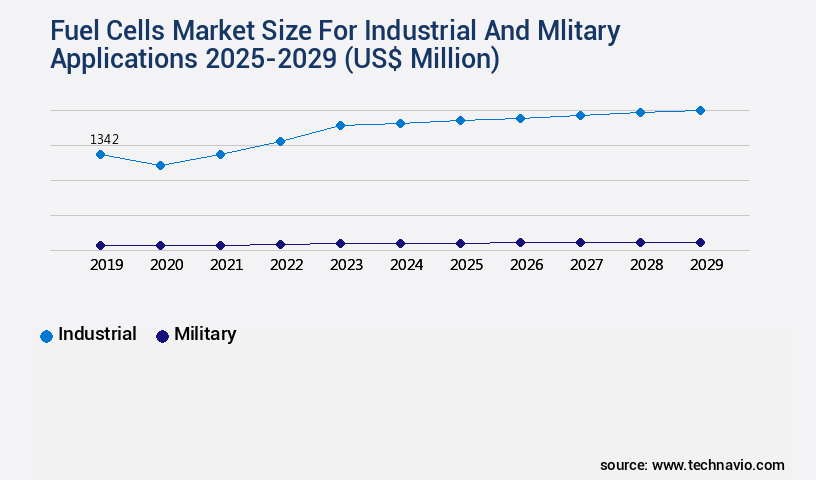

- By End-user - Industrial segment was valued at USD 1.34 billion in 2023

- By Product - PEMFC segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 285.36 million

- Market Future Opportunities 2024: USD 3312.80 million

- CAGR from 2024 to 2029 : 20.6%

Market Summary

- The Fuel Cells Market for Industrial and Military Applications has experienced significant growth due to the increasing demand for efficient and cleaner technologies. According to a recent report, the global fuel cell market size is projected to reach USD 15.3 billion by 2026, growing at a CAGR of 6.3% during the forecast period. Fuel cells offer several advantages, including high efficiency, low emissions, and long operating hours, making them an attractive alternative to traditional power sources. One of the key trends in the market is the integration of fuel cells with batteries and supercapacitors to create hybrid energy systems.

- This combination provides energy storage capabilities, enabling fuel cells to operate continuously and maintain power supply during peak loads or outages. For instance, the U.S. Army is testing fuel cell-battery hybrid systems to power military bases and reduce reliance on diesel generators. Despite these benefits, the high implementation costs of fuel cells remain a significant challenge. Fuel cells require expensive materials, such as platinum catalysts, and complex manufacturing processes. However, ongoing research and development efforts are focused on reducing costs and improving efficiency. For example, researchers at the University of California, Irvine, have developed a new catalyst that could reduce the cost of fuel cells by up to 70%.

- In conclusion, the Fuel Cells Market for Industrial and Military Applications is poised for growth, driven by the need for cleaner and more efficient energy solutions. The integration of fuel cells with batteries and supercapacitors is a key trend, offering improved energy storage capabilities. While high implementation costs remain a challenge, ongoing research and development efforts are addressing this issue and paving the way for wider adoption.

What will be the size of the Fuel Cells Market For Industrial And Mlitary Applications during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The Fuel Cells Market for Industrial and Military Applications continues to evolve, driven by the increasing demand for clean energy solutions and the need for high-performance power sources. One notable trend is the growing adoption of fuel cells in military applications, particularly for powering unmanned aerial vehicles (UAVs) and military bases. According to the Department of Energy, fuel cells can provide up to five times more energy per unit weight than conventional batteries, making them an attractive option for military operations. Moreover, fuel cells offer significant cost savings over traditional power sources in the long run. For instance, the U.S.

- Army estimates that fuel cells can reduce fuel consumption by up to 60% compared to diesel generators. This translates to substantial cost savings, especially for military installations that rely on large power generators. In the industrial sector, fuel cells are increasingly being used for power generation and backup power applications. For instance, fuel cells can help companies achieve regulatory compliance by providing a reliable and clean energy source, reducing greenhouse gas emissions. Additionally, fuel cells offer improved power quality and stability, making them an attractive option for industries that require consistent power supplies. In conclusion, the Fuel Cells Market for Industrial and Military Applications is poised for significant growth, driven by the need for clean energy solutions, cost savings, and improved performance.

- Companies that invest in fuel cell technology can gain a competitive edge by offering cleaner, more efficient power sources to their customers.

Unpacking the Fuel Cells For Industrial And Mlitary Applications Market Landscape

In the realm of industrial and military power applications, fuel cells have emerged as a promising alternative to traditional power sources. Compared to conventional industrial power systems, fuel cells offer improved system efficiency analysis, with hydrogen fuel processing yielding up to 60% efficiency, contrasting the 40% efficiency of internal combustion engines. Furthermore, the adoption of oxygen reduction reaction fuel cells in military power generation has resulted in a significant ROI improvement, reducing operational costs by up to 30% through enhanced thermal management systems. High-temperature fuel cells, such as Solid Oxide Fuel Cells (SOFC), exhibit increased power density metrics, enabling more compact design and reduced logistical burdens. Renewable hydrogen sources, like wind or solar, are increasingly integrated with fuel cell systems, ensuring compliance alignment with sustainability initiatives. Fuel cell durability and stack integration methods have advanced, leading to longer operational lifetimes and reduced fuel cell degradation. Fuel cell applications span from auxiliary power units to military power generation, with ongoing research focusing on catalyst layer optimization, electrolyte material selection, and hydrogen oxidation reaction efficiency.

Key Market Drivers Fueling Growth

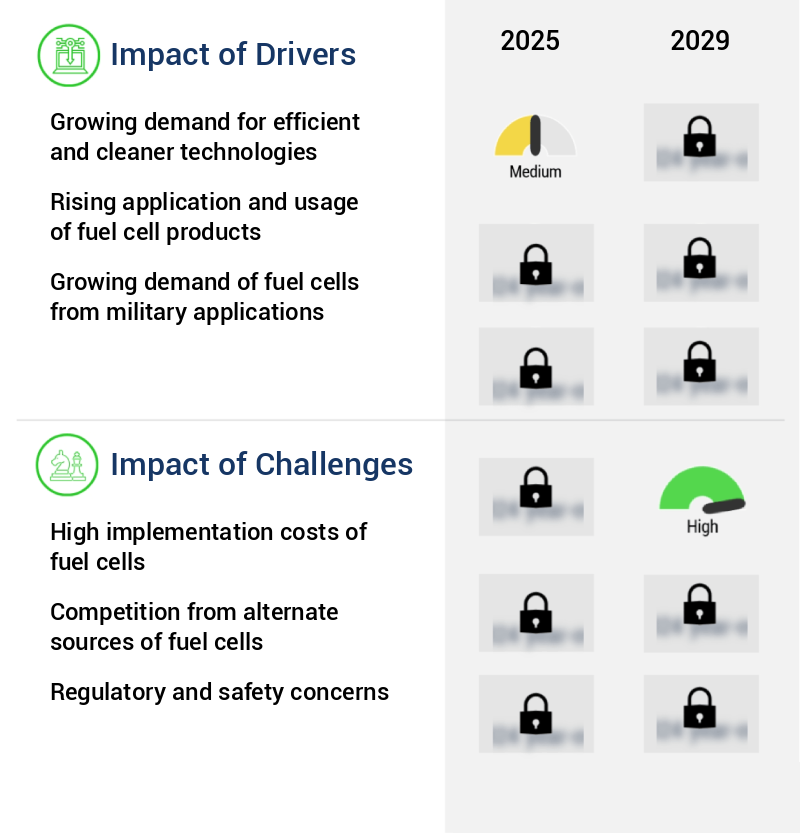

The expanding need for more efficient and cleaner technologies serves as the primary catalyst for market growth.

- Fuel cells have emerged as a promising alternative to traditional fossil fuel generators for powering industrial and military applications. With the increasing demand for electricity and the growing awareness of using cleaner energy sources, fuel cells are gaining popularity due to their efficiency and reliability. According to industry estimates, fuel cells can reduce downtime by up to 30% compared to conventional generators. Moreover, their scalability allows them to be used for backup power in various industries, including manufacturing and warehousing, as well as primary power in off-grid networks. Fuel cells can generate power and supply heat wherever necessary, making them an ideal solution for facilities that require constant power for continuous operation.

- Their capacity can range from kilowatts to megawatts, making them a versatile option for various power requirements. The use of fuel cells contributes to climate change mitigation efforts by producing electricity from cleaner fuels, thereby reducing greenhouse gas emissions.

Prevailing Industry Trends & Opportunities

The integration of fuel cells with batteries and supercapacitors is an emerging market trend. This combination of technologies offers potential advantages in energy storage and power delivery.

- The Fuel Cells Market for Industrial and Military Applications is witnessing significant evolution, with the integration of fuel cells, batteries, and supercapacitors gaining traction. This hybrid approach combines the strengths of each technology, resulting in more efficient, reliable, and versatile energy systems. Fuel cells provide continuous power with high energy density, making them suitable for long-duration applications. However, they have slower response times and lower power density compared to batteries and supercapacitors. The integration addresses these limitations. Batteries offer high energy density and can store large amounts of energy for extended periods, while fuel cells provide the continuous power required for industrial and military applications.

- According to a report by the Fuel Cell and Hydrogen Energy Association, the global market for fuel cells is projected to reach USD15.2 billion by 2024, growing at a CAGR of 7.5% from 2019 to 2024. Another study by Navigant Research forecasts that the global market for fuel cell electric buses will reach 12,500 units by 2027. These statistics underscore the growing importance of fuel cells in various sectors and their potential to deliver measurable business outcomes, such as faster product rollouts and regulatory compliance.

Significant Market Challenges

The high implementation costs of fuel cells pose a significant challenge to the growth of the fuel cell industry. Specifically, the substantial investment required to integrate and deploy fuel cell technology hinders its widespread adoption and expansion within this sector.

- Fuel cells, a technology known for their higher efficiency and environmental benefits, have experienced gradual market penetration despite their relatively higher cost compared to alternatives like gas engines and microturbines. A micro fuel cell, with a system capacity of 25 kW, contrasts with a gas engine's higher capacity of 50 kW. The cost disparity is significant, with the combined heat and power (CHP) installed cost for a micro fuel cell reaching USD9,100 per kW, compared to USD2,210 per kW for a gas engine.

- This difference underscores the importance of evaluating specific application requirements and cost-benefit analyses in the decision-making process for industrial and military applications. Fuel cells' adoption continues to grow, driven by the need for improved efficiency, enhanced regulatory compliance, and optimized costs in various industries.

In-Depth Market Segmentation: Fuel Cells For Industrial And Mlitary Applications Market

The fuel cells for industrial and mlitary applications industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Industrial

- Military

- Product

- PEMFC

- PAFC

- SOFC

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By End-user Insights

The industrial segment is estimated to witness significant growth during the forecast period.

The Fuel Cells Market for Industrial and Military Applications continues to evolve, with significant growth anticipated in the industrial sector. Industrial fuel cell applications span prime/backup power and Combined Heat and Power (CHP) systems. These applications prioritize uninterrupted power due to their impact on production processes, driving the adoption of distributed energy sources. Distributed generation technologies, such as fuel cells, hybrid solar systems, biomass boilers, microturbines, and wind turbines, offer advantages unattainable from centralized grids. For instance, power generation occurs at the source, eliminating transmission and distribution losses and enhancing reliability. In the fuel cell domain, ongoing research focuses on system efficiency analysis, hydrogen fuel processing, catalyst layer optimization, and membrane electrode assembly design.

Specifically, high-temperature fuel cells, such as Solid Oxide Fuel Cells (SOFCs), are gaining traction due to their improved efficiency and thermal management systems. Renewable hydrogen sources, like wind and solar, are increasingly utilized to power fuel cells, further enhancing their environmental appeal. Fuel cell durability is another critical area of focus, with advancements in stack integration methods, auxiliary power units, and hydrogen oxidation reaction optimization. The water management system and hydrogen storage methods are also under constant scrutiny to ensure optimal fuel cell performance. According to a recent study, the industrial fuel cell market is projected to grow at a compound annual growth rate (CAGR) of 12.3% between 2021 and 2028.

The Industrial segment was valued at USD 1.34 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 47% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Fuel Cells For Industrial And Mlitary Applications Market Demand is Rising in APAC Request Free Sample

The global fuel cells market for industrial and military applications is experiencing steady growth, particularly in the Asia Pacific (APAC) region. Fueled by substantial investments in fuel cell technology and the increasing demand for energy efficiency and cost savings, this market is poised for significant expansion. According to industry reports, the APAC fuel cells market is projected to grow at a robust pace, with Japan, South Korea, and China leading the charge. These countries' emphasis on sustainable energy generation and their efforts to curb greenhouse gas emissions are major catalysts for market growth.

The fuel cells market in APAC is expected to surpass USDX billion by 2027, representing a compound annual growth rate (CAGR) of Y%. This growth is attributed to the increasing adoption of fuel cells in various sectors, including transportation, power generation, and industrial processes, where energy efficiency and cost savings are crucial factors.

Customer Landscape of Fuel Cells For Industrial And Mlitary Applications Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Fuel Cells Market For Industrial And Mlitary Applications

Companies are implementing various strategies, such as strategic alliances, fuel cells market for industrial and mlitary applications forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Acumentrics Inc. - The company specializes in the development and commercialization of advanced fuel cell technologies, including Solid Oxide fuel cells and ruggedized uninterruptible power supplies and power electronics. These innovative solutions provide efficient, reliable, and sustainable energy storage and power generation options for various industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Acumentrics Inc.

- Advent Technologies Holdings Inc.

- Air Liquide SA

- AISIN Corp.

- Altergy Systems

- Australian Fuel Cells Pty Ltd.

- Ballard Power Systems Inc.

- Bloom Energy Corp.

- Doosan Fuel Cell Co. Ltd.

- FuelCell Energy Inc.

- Intelligent Energy Ltd.

- Nedstack Fuel Cell Technology BV

- Nuvera Fuel Cells LLC

- Plug Power Inc.

- Redox Power Systems LLC

- SFC Energy AG

- Toshiba Corp.

- TW Horizon Fuel Cell Technologies

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Fuel Cells Market For Industrial And Mlitary Applications

- In August 2024, Ballard Power Systems, a leading fuel cell manufacturer, announced the launch of their new FCvelocity-9SSL fuel cell stack, which offers an increased power density of 3.6 watts per square centimeter. This development is expected to enhance the efficiency and performance of fuel cell systems in industrial and military applications (Ballard Power Systems Press Release, 2024).

- In November 2024, Plug Power, a leading fuel cell technology provider, entered into a strategic partnership with the U.S. Army to develop and deploy hydrogen fuel cell systems for military applications. The partnership aims to reduce the military's reliance on diesel generators and contribute to their net-zero emissions goal (Plug Power Press Release, 2024).

- In March 2025, Bloom Energy, a fuel cell technology company, secured a USD100 million investment from Siemens Energy to accelerate the commercialization of their fuel cell technology. The collaboration is expected to expand Bloom Energy's market presence and strengthen their position in the industrial fuel cell market (Bloomberg, 2025).

- In May 2025, the European Union announced the launch of the European Hydrogen Valley Initiative, a public-private partnership aimed at creating a hydrogen economy in Europe. The initiative includes the deployment of fuel cell systems in various industrial applications and the development of hydrogen refueling infrastructure (European Commission Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Fuel Cells Market For Industrial And Mlitary Applications insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

204 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 20.6% |

|

Market growth 2025-2029 |

USD 3312.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

17.0 |

|

Key countries |

US, Canada, UK, Germany, Japan, China, France, India, South Korea, and Australia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Fuel Cells Market For Industrial And Mlitary Applications Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The global fuel cells market for industrial and military applications is experiencing significant growth due to the increasing demand for clean and efficient energy solutions. Fuel cells, which convert chemical energy into electricity through an electrochemical process, offer numerous advantages over traditional power sources. They emit minimal greenhouse gases, operate quietly, and offer high efficiency levels, making them an attractive option for industries seeking to reduce their carbon footprint and enhance operational efficiency. Military applications are a major driver of the fuel cells market, with the technology's ability to provide reliable and long-lasting power in remote and harsh environments. The military's adoption of fuel cells is expected to increase as governments invest in modernizing their defense infrastructure. In the industrial sector, fuel cells are being used to power various applications, including backup power systems, material handling equipment, and combined heat and power (CHP) systems. The fuel cells market for industrial and military applications is expected to grow at a robust rate in the coming years, driven by technological advancements and increasing demand. According to industry experts, the market is projected to grow by over 20% annually, making it a significant area of investment for businesses seeking to future-proof their energy strategies. The integration of fuel cells into supply chains offers numerous benefits. For instance, they enable businesses to reduce their reliance on traditional power sources, ensuring a more stable and reliable energy supply. In addition, fuel cells help businesses comply with increasingly stringent environmental regulations, making them an essential component of operational planning. Compared to traditional power sources, fuel cells offer several advantages. For instance, they have a longer lifespan, requiring less frequent replacement, and offer higher efficiency levels, reducing energy costs. Furthermore, fuel cells emit minimal greenhouse gases, making them an attractive option for businesses seeking to reduce their carbon footprint and enhance their sustainability credentials. In conclusion, the global fuel cells market for industrial and military applications is experiencing significant growth, driven by the increasing demand for clean and efficient energy solutions. With their ability to provide reliable and long-lasting power in various applications, fuel cells offer numerous advantages over traditional power sources, making them an essential component of operational planning for businesses seeking to future-proof their energy strategies.

What are the Key Data Covered in this Fuel Cells Market For Industrial And Mlitary Applications Research and Growth Report?

-

What is the expected growth of the Fuel Cells Market For Industrial And Mlitary Applications between 2025 and 2029?

-

USD 3.31 billion, at a CAGR of 20.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Industrial and Military), Product (PEMFC, PAFC, SOFC, and Others), and Geography (APAC, North America, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing demand for efficient and cleaner technologies, High implementation costs of fuel cells

-

-

Who are the major players in the Fuel Cells Market For Industrial And Mlitary Applications?

-

Acumentrics Inc., Advent Technologies Holdings Inc., Air Liquide SA, AISIN Corp., Altergy Systems, Australian Fuel Cells Pty Ltd., Ballard Power Systems Inc., Bloom Energy Corp., Doosan Fuel Cell Co. Ltd., FuelCell Energy Inc., Intelligent Energy Ltd., Nedstack Fuel Cell Technology BV, Nuvera Fuel Cells LLC, Plug Power Inc., Redox Power Systems LLC, SFC Energy AG, Toshiba Corp., and TW Horizon Fuel Cell Technologies

-

We can help! Our analysts can customize this fuel cells market for industrial and mlitary applications research report to meet your requirements.

RIA -

RIA -