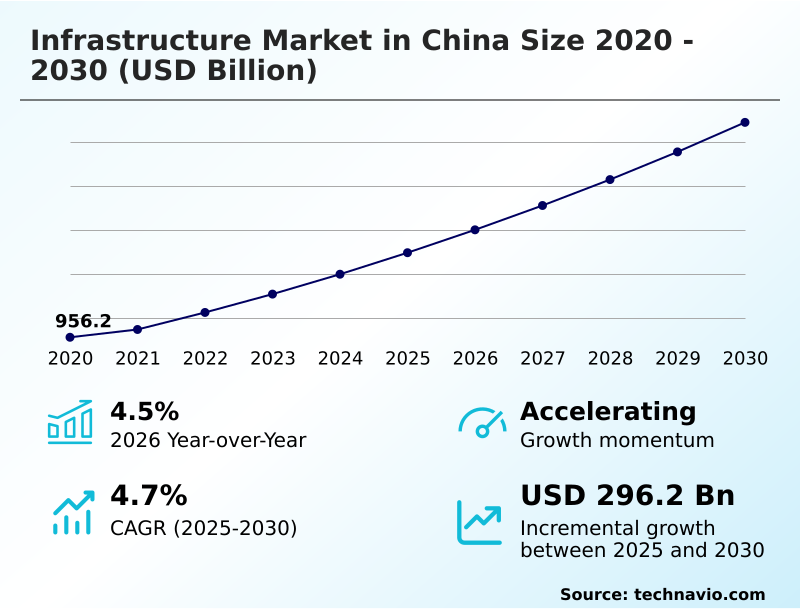

China Infrastructure Market Size 2026-2030

The china infrastructure market size is valued to increase by USD 296.2 billion, at a CAGR of 4.7% from 2025 to 2030. High-quality power grid modernization and ultra-high voltage infrastructure will drive the china infrastructure market.

Major Market Trends & Insights

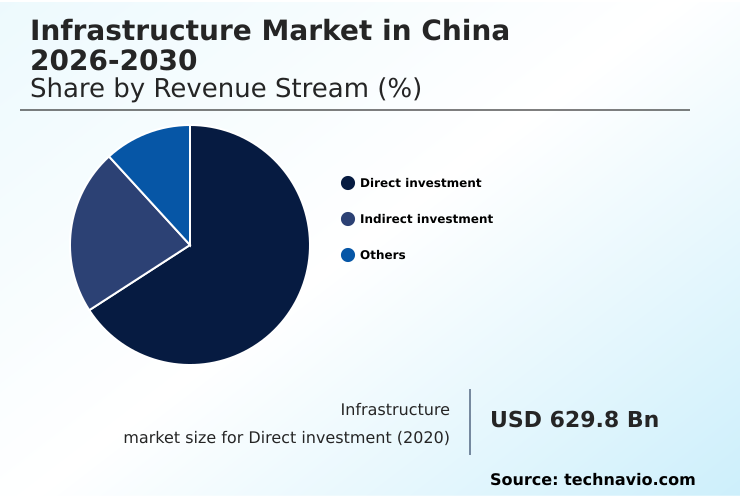

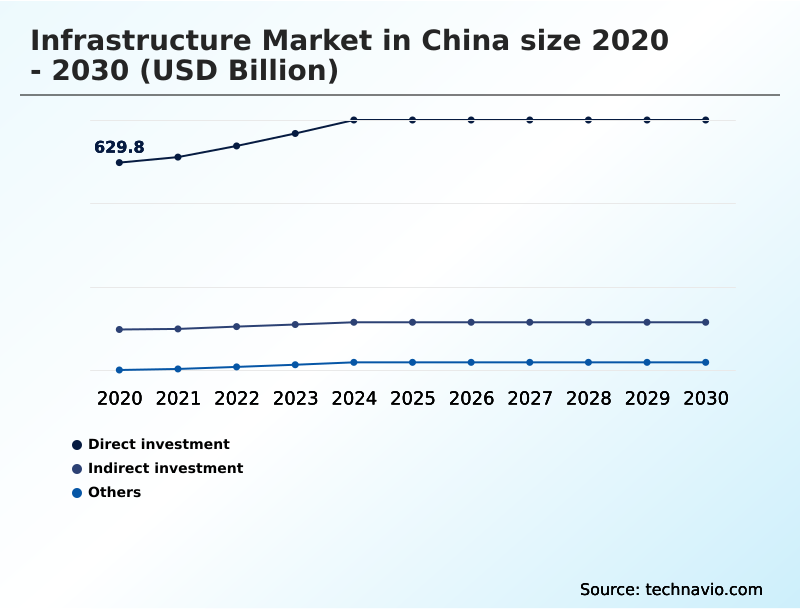

- By Revenue Stream - Direct investment segment was valued at USD 736 billion in 2024

- By Application - Transportation segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 488.4 billion

- Market Future Opportunities: USD 296.2 billion

- CAGR from 2025 to 2030 : 4.7%

Market Summary

- The infrastructure market in China is undergoing a significant transformation, pivoting from traditional civil engineering to an integrated system driven by digitalization and sustainability. This evolution prioritizes the development of new quality productive forces through assets like 5G networks, ultra-high-voltage power grids, and AI-ready hyper-scale data centers.

- A key driver is the strategic imperative to achieve carbon neutrality, which necessitates green energy megaprojects and a complete realignment of utility infrastructure. For instance, a logistics firm can leverage smart signaling and intelligent transport systems to optimize delivery routes, reducing fuel consumption and improving lifecycle efficiency. However, this transition is not without friction.

- The market grapples with systemic debt issues stemming from the decline of traditional land-based finance models, forcing a recalibration of funding mechanisms. The integration of building information modeling (BIM) and digital twin technology is becoming standard for managing project complexity, from autonomous underground construction to smart city platforms, ensuring that new assets are resilient and efficient.

What will be the Size of the China Infrastructure Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the China Infrastructure Market Segmented?

The china infrastructure industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Revenue stream

- Direct investment

- Indirect investment

- Others

- Application

- Transportation

- Social

- Utilities

- Manufacturing

- Extraction infrastructure

- Type

- Small and medium

- Large-scale

- Mega projects

- Geography

- APAC

- China

- APAC

By Revenue Stream Insights

The direct investment segment is estimated to witness significant growth during the forecast period.

Direct investment remains the dominant revenue stream, characterized by capital deployment from central and provincial governments into large-scale public works.

This approach funnels funds through state-owned enterprises for projects aligned with national strategies, such as developing AI-ready hyper-scale data centers and achieving regional connectivity.

The focus is shifting from traditional construction to high-tech new infrastructure, including ultra-high voltage infrastructure and extensive 5G networks. Investments in smart tunneling systems and building information modeling (BIM) are prioritized to enhance industrial productivity.

This strategic pivot is underlined by a commitment to increase fixed-asset investment by over 40% in key sectors during the current five-year plan, utilizing public-private partnership (PPP) models to leverage capital for high-quality development like transportation infrastructure development.

The Direct investment segment was valued at USD 736 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic direction of the infrastructure market in China is increasingly shaped by the impact of AI on smart city platforms, which are becoming central to urban management and resource optimization. A key focus is optimizing power grid modernization with AI, enabling better load balancing and integration of renewable energy sources.

- This focus on technological advancement is complemented by massive investments in physical networks, with high-speed rail for regional connectivity serving as a cornerstone for integrating economic zones and improving mobility. The expansion of digital infrastructure is also critical, and understanding the role of 5G networks in digital infrastructure is essential for developing next-generation services like autonomous transportation and IoT-enabled utilities.

- However, the market faces significant headwinds, particularly the challenges in land-based finance models, which have historically funded a majority of public works. This financial pressure forces a re-evaluation of project viability and funding mechanisms.

- Projects leveraging advanced technologies are showing greater resilience; for instance, initiatives using integrated digital platforms report lifecycle maintenance costs that are nearly 15% lower than those using traditional management methods. This demonstrates a clear shift toward smarter, more sustainable development frameworks that prioritize both technological innovation and fiscal stability.

What are the key market drivers leading to the rise in the adoption of China Infrastructure Industry?

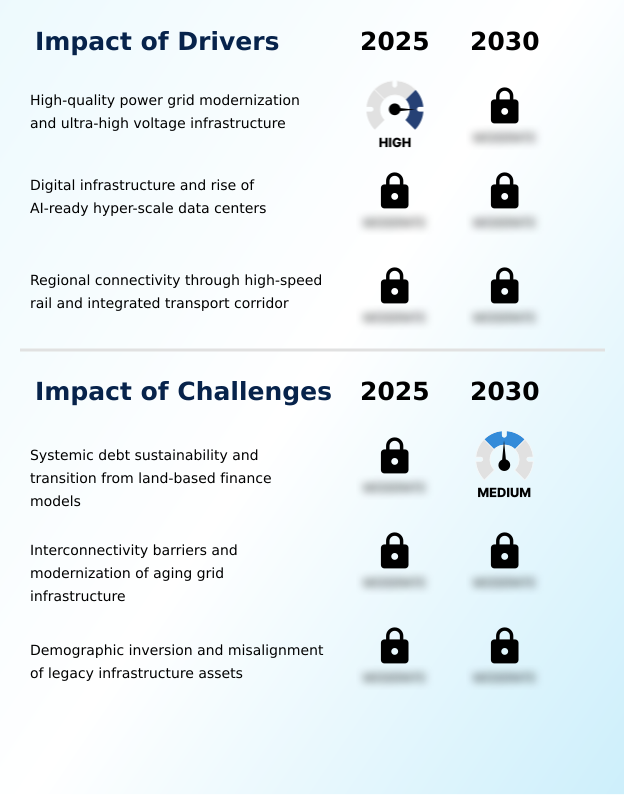

- Extensive modernization of the power grid and the construction of ultra-high voltage infrastructure are primary drivers stimulating market expansion.

- Market expansion is primarily driven by extensive grid modernization and the build-out of ultra-high voltage infrastructure. This is essential for connecting renewable energy sources to industrial hubs, ensuring a stable, decentralized energy mix and increasing grid capacity by over 25%.

- The rise of AI-ready hyper-scale data centers underpins the national push for digital infrastructure, with new facilities achieving 30% greater energy efficiency. Investments in high-speed rail connectivity and intelligent transport systems further fuel growth, creating an integrated transport corridor.

- This also involves advancing water conservancy systems, asset refurbishment, and ensuring robust power generation systems are in place, fostering a favorable fiscal environment for development.

What are the market trends shaping the China Infrastructure Industry?

- The market is increasingly shaped by the development of green energy megaprojects. This trend involves a strategic realignment of utility infrastructure to achieve national carbon neutrality goals.

- A definitive trend is the strategic pivot to green energy megaprojects and the comprehensive realignment of utility infrastructure. This involves constructing massive wind turbines and photovoltaic systems, supported by industrial-scale energy storage and high-voltage direct current (HVDC) transmission lines. This creates a decentralized energy mix and supports carbon neutrality goals.

- The integration of green logistics has been shown to reduce supply chain emissions by up to 20%. Concurrently, smart city platforms are advancing with multi-modal logistics optimization and smart signaling, which has improved urban traffic flow by 15% in pilot cities.

- This focus on telecom tower leasing and smart utility upgrades is reshaping the competitive landscape, incorporating engineering design services and cross-sea ferry engineering projects.

What challenges does the China Infrastructure Industry face during its growth?

- Systemic debt sustainability and the structural transition from land-based finance models represent a significant challenge to the industry's growth.

- A primary challenge is the structural shift away from land-based finance models, which has created a precarious fiscal environment, impacting project completion timelines by an average of 10% in some regions. The market also contends with interconnectivity barriers in aging infrastructure and the complexities of demographic inversion.

- Addressing systemic debt sustainability requires new approaches like sustainable financing and a more effective centralized bidding system. Efforts to manage these challenges through debt swaps have provided some relief, but the core issue of establishing new, reliable revenue streams remains a significant constraint, affecting everything from social infrastructure to manufacturing infrastructure and extraction infrastructure.

- Digital oversight is being implemented to improve efficiency and control costs.

Exclusive Technavio Analysis on Customer Landscape

The china infrastructure market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the china infrastructure market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of China Infrastructure Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, china infrastructure market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Analysis reveals a focus on delivering scalable cloud computing infrastructure and robust data center services, supporting enterprise-level digital transformation and AI-native applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- AECOM

- Alibaba Cloud

- Arup Group Ltd.

- Baidu Inc.

- BYD Co. Ltd.

- Caterpillar Inc.

- China Tower Corp. Ltd.

- GE Vernova Inc.

- Hitachi Ltd.

- Honeywell International Inc.

- Huawei Technologies Co. Ltd.

- JinkoSolar Holding Co. Ltd.

- Sany Heavy Industry Co. Ltd.

- Schneider Electric SE

- Siemens AG

- SZ DJI Technology Co. Ltd.

- Tencent Holdings Ltd.

- Zoomlion Industry Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in China infrastructure market

- In February 2025, The National Development and Reform Commission initiated an early-batch investment plan to accelerate key national projects, including modern transportation hubs and energy resiliency initiatives, aimed at stimulating economic momentum.

- In March 2025, China Railway Construction Corp. Ltd. secured bids for ten major domestic projects, such as the Guangzhou East Railway Station renovation and the Bomi-Ranwu Railway line, reinforcing its role in expanding the national high-speed rail network.

- In January 2025, The National Energy Administration reported that renewable sources now contribute to one-third of all domestic electricity use, validating the successful integration of large-scale wind and solar clusters into the national grid.

- In April 2025, S&P Global Ratings issued a report indicating that local governments would continue significant debt issuance to fund countercyclical fiscal spending, highlighting persistent fiscal pressures from the shift away from land-based finance models.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled China Infrastructure Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 196 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.7% |

| Market growth 2026-2030 | USD 296.2 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.5% |

| Key countries | China |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The infrastructure market in China is defined by a strategic transition toward high-technology assets and sustainable development, moving beyond traditional construction. This pivot is evident in the prioritization of smart grid systems, telecom network infrastructure, and advanced rail transportation solutions. The integration of industrial automation solutions and building management systems is now standard, enhancing operational efficiency.

- A core trend influencing boardroom decisions is the mandate for decarbonization, which drives investment in green energy megaprojects featuring wind turbines and large-scale power generation systems. For example, the deployment of intelligent transport systems has improved network throughput by over 20% without requiring new physical lanes.

- The market is supported by robust manufacturing of construction equipment, including hydraulic excavators and concrete machinery equipment, alongside innovations in power distribution systems. This evolution demands a focus on high-tech capabilities, from cloud computing infrastructure and smart building solutions to sophisticated industrial control solutions and shared communications infrastructure, all crucial for next-generation development.

What are the Key Data Covered in this China Infrastructure Market Research and Growth Report?

-

What is the expected growth of the China Infrastructure Market between 2026 and 2030?

-

USD 296.2 billion, at a CAGR of 4.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Revenue Stream (Direct investment, Indirect investment, and Others), Application (Transportation, Social, Utilities, Manufacturing, and Extraction infrastructure), Type (Small and medium, Large-scale, and Mega projects) and Geography (APAC)

-

-

Which regions are analyzed in the report?

-

APAC

-

-

What are the key growth drivers and market challenges?

-

High-quality power grid modernization and ultra-high voltage infrastructure, Systemic debt sustainability and transition from land-based finance models

-

-

Who are the major players in the China Infrastructure Market?

-

ABB Ltd., AECOM, Alibaba Cloud, Arup Group Ltd., Baidu Inc., BYD Co. Ltd., Caterpillar Inc., China Tower Corp. Ltd., GE Vernova Inc., Hitachi Ltd., Honeywell International Inc., Huawei Technologies Co. Ltd., JinkoSolar Holding Co. Ltd., Sany Heavy Industry Co. Ltd., Schneider Electric SE, Siemens AG, SZ DJI Technology Co. Ltd., Tencent Holdings Ltd. and Zoomlion Industry Co. Ltd.

-

Market Research Insights

- The market's dynamics are shifting towards high-quality development, emphasizing digital infrastructure and sustainable financing. The adoption of advanced digital oversight has improved project completion timelines by over 15% in complex urban settings. This pivot to high-tech integration is crucial for new quality productive forces, driving investments in energy resiliency projects and urban refinement.

- Furthermore, the focus on tech sovereignty has accelerated the development of localized smart utility upgrades, with early adopters reporting a 10% reduction in operational energy consumption. The transition away from traditional land-based finance models is being managed through new fiscal environments that prioritize asset refurbishment and lifecycle efficiency, supporting the creation of an integrated transport corridor.

We can help! Our analysts can customize this china infrastructure market research report to meet your requirements.

RIA -

RIA -