Europe Logistics Market Size 2026-2030

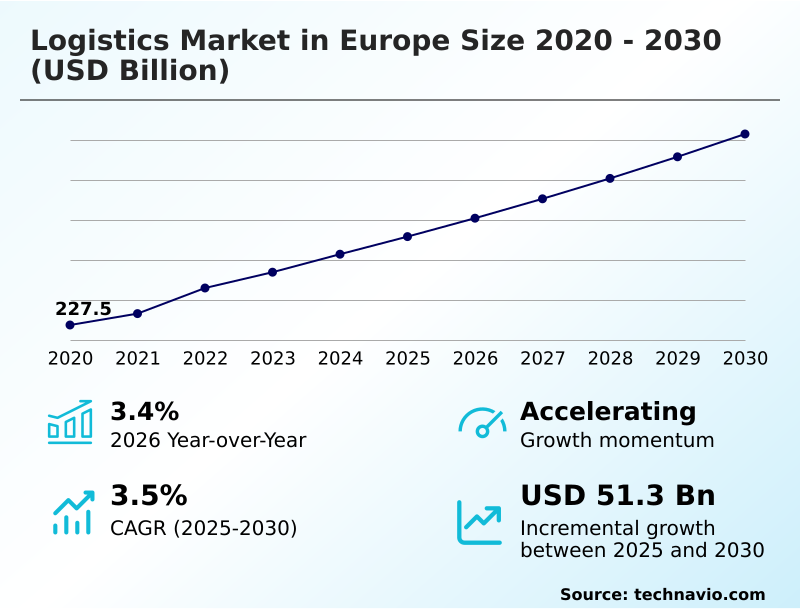

The europe logistics market size is valued to increase by USD 51.3 billion, at a CAGR of 3.5% from 2025 to 2030. Booming e-commerce industry in Europe will drive the europe logistics market.

Major Market Trends & Insights

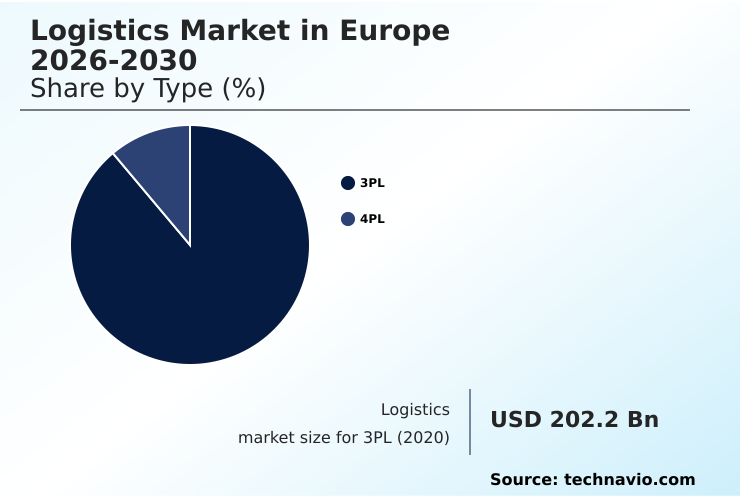

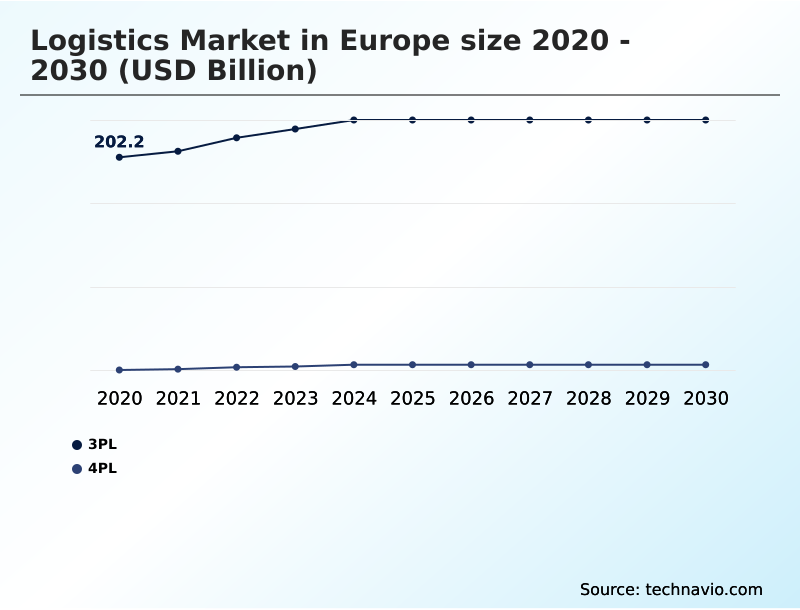

- By Type - 3PL segment was valued at USD 233.2 billion in 2024

- By End-user - Manufacturing segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 95.5 billion

- Market Future Opportunities: USD 51.3 billion

- CAGR from 2025 to 2030 : 3.5%

Market Summary

- The logistics market in Europe is a highly integrated sector defined by advanced infrastructure and complex operational demands. Growth is fueled by the expansion of cross-border e-commerce and the strategic outsourcing of supply chain functions to specialized third-party logistics (3PL) and fourth-party logistics (4PL) providers.

- A key trend shaping the industry is the rapid adoption of digital technologies, including real-time tracking and transportation management systems (TMS), to enhance supply chain visibility and efficiency. For instance, a manufacturing firm might partner with a 3PL to implement just-in-time (JIT) delivery, using shared data to synchronize component arrivals with production schedules, thereby minimizing inventory costs and improving responsiveness.

- However, the market also contends with significant challenges, such as the high operational costs associated with last-mile delivery, increasing environmental regulations that necessitate investments in sustainable logistics, and intense price competition. These dynamics push companies toward continuous innovation in areas like route optimization and automated warehousing to maintain a competitive edge while balancing service quality and profitability.

What will be the Size of the Europe Logistics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Europe Logistics Market Segmented?

The europe logistics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- 3PL

- 4PL

- End-user

- Manufacturing

- Automotive

- Consumer goods

- Retail industry

- Others

- Mode of transportation

- Roadways

- Waterways

- Railways

- Airways

- Geography

- Europe

- Germany

- UK

- France

- Europe

By Type Insights

The 3pl segment is estimated to witness significant growth during the forecast period.

The third-party logistics (3PL) segment is pivotal as businesses increasingly outsource supply chain functions to specialized partners. These providers deliver integrated services, including transportation, warehousing, and inventory management, enabling companies to focus on core competencies.

The complexity of modern supply chains, coupled with rising customer expectations for rapid delivery, drives reliance on 3PL expertise and infrastructure. Providers leverage advanced technologies for route optimization and real-time tracking to enhance operational performance.

Outsourcing to a lead logistics provider also offers scalability, allowing businesses to adapt to demand fluctuations without significant capital investment in fixed assets.

This strategic shift to a 3PL model has been shown to improve on-time delivery rates by up to 15%, making it a cornerstone of efficient supply chain management.

The 3PL segment was valued at USD 233.2 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the complexities of the modern supply chain requires a deep understanding of strategic choices, such as 3pl vs 4pl supply chain management, where the latter offers a more integrated, overarching control layer.

- A critical factor reshaping operations is the impact of automation on warehousing efficiency, with automated systems demonstrating processing speeds that are up to three times faster than manual methods, directly influencing order fulfillment capacity. The role of real-time tracking in freight forwarding has become non-negotiable, providing the transparency needed for dynamic decision-making and risk mitigation.

- For businesses engaged in online retail, optimizing cross-border e-commerce logistics is paramount to managing customs, duties, and customer expectations effectively. Concurrently, the challenges in last-mile delivery logistics, particularly in congested urban centers, demand innovative solutions to balance speed and cost.

- Overarching these operational concerns is the growing imperative for implementing sustainable logistics in retail, which not only addresses regulatory pressures but also resonates with an increasingly environmentally conscious consumer base. These interconnected elements are reshaping how companies design and execute their supply chain strategies.

What are the key market drivers leading to the rise in the adoption of Europe Logistics Industry?

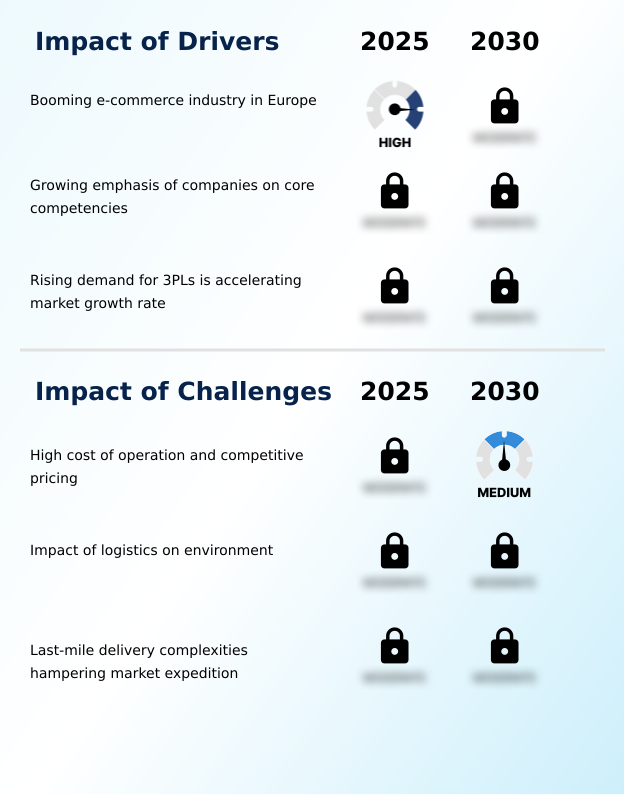

- The booming e-commerce industry across Europe is a key driver for the logistics market, fueling demand for efficient and scalable delivery solutions.

- Market growth is significantly propelled by the expansion of e-commerce and the strategic decision of companies to outsource non-core functions.

- The shift to third-party logistics (3PL) providers allows businesses to reduce fixed operational costs by an average of 15–20% while gaining access to specialized expertise in transportation and warehousing.

- This reliance on integrated logistics services is crucial as supply chains become more complex.

- The booming online retail sector has led to a 40% increase in parcel volumes in major urban centers, creating sustained demand for efficient e-commerce fulfillment and last-mile delivery.

- As a result, logistics service providers are expanding their value-added logistics services and investing in advanced technologies to enhance their capabilities and meet the evolving needs of their clients.

What are the market trends shaping the Europe Logistics Industry?

- A significant market trend is the increasing focus on customer-centric logistics. This shift prioritizes service design and execution to meet evolving consumer expectations for speed and transparency.

- Key trends are reshaping the market, with a strong emphasis on digital transformation and customer-centric models. The rise of omnichannel logistics is compelling businesses to unify physical and digital sales channels, leading to a 25% improvement in inventory accuracy for companies that have integrated their systems. This integration supports seamless e-commerce fulfillment and enhances the customer experience.

- Concurrently, the adoption of digital logistics platforms and advanced supply chain analytics is driving significant efficiency gains. For instance, predictive analytics for demand forecasting has improved accuracy by up to 18%, reducing instances of both overstocking and stock-outs. The focus on green logistics practices is also intensifying, with companies exploring sustainable solutions to meet both regulatory requirements and consumer expectations.

What challenges does the Europe Logistics Industry face during its growth?

- High operational costs, coupled with intense competitive pricing pressures, present a significant challenge affecting industry growth and profitability.

- The market faces considerable pressure from high operational costs and complex logistical hurdles, particularly in urban environments. Last-mile delivery, for instance, can account for over 50% of total shipping costs, driven by factors such as traffic congestion and failed delivery attempts.

- Concurrently, the push for environmental sustainability presents both financial and operational challenges; adopting electric vehicles for urban logistics can increase upfront capital expenditure by 35% per vehicle. These issues are compounded by intense pricing competition, which constrains profit margins. Furthermore, managing reverse logistics efficiently adds another layer of complexity, requiring robust systems to handle product returns without eroding profitability.

- These factors demand continuous innovation in operational strategies and technology adoption.

Exclusive Technavio Analysis on Customer Landscape

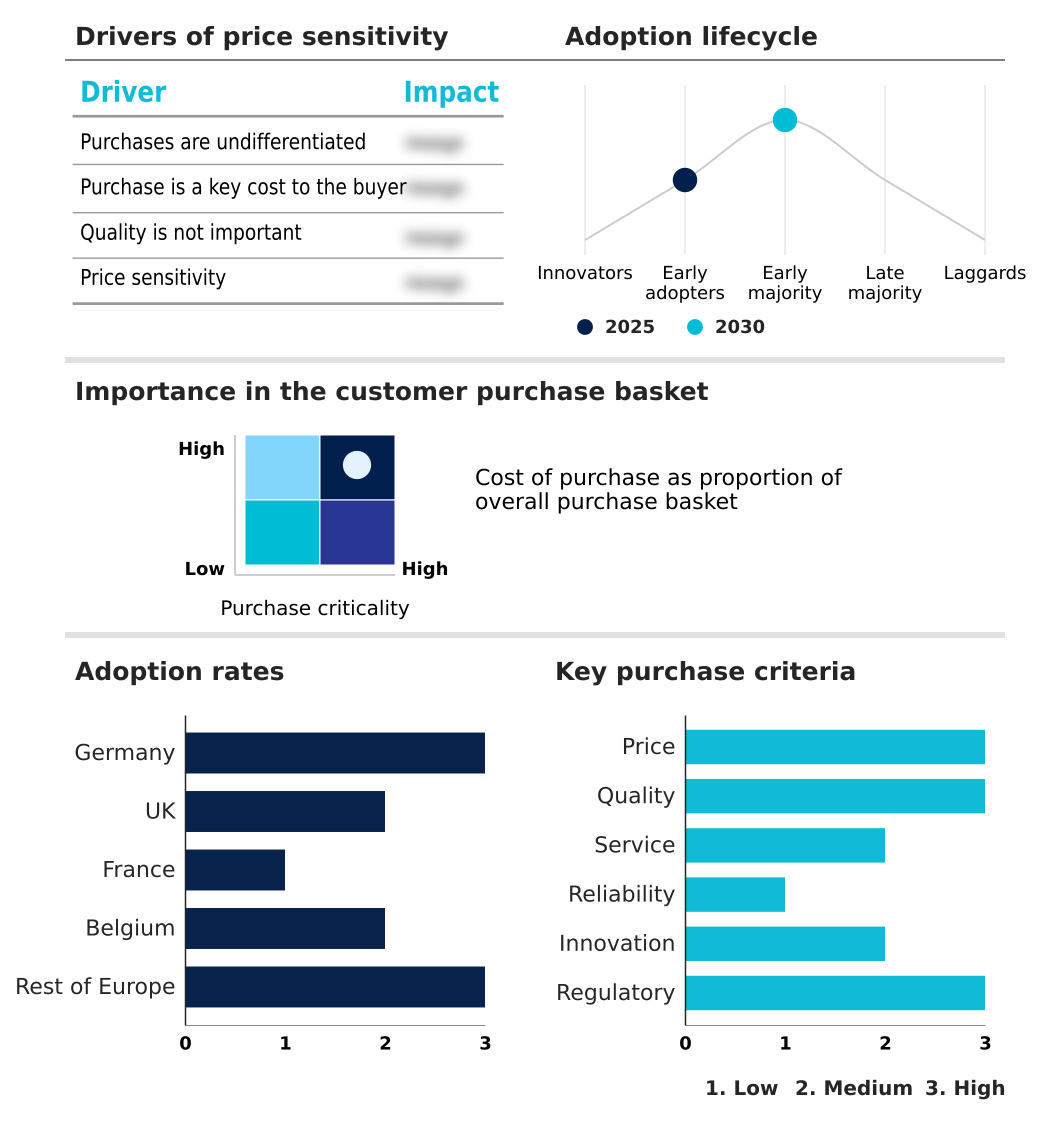

The europe logistics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the europe logistics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Europe Logistics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, europe logistics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Bollore Logistics - Offerings include integrated supply chain solutions, freight forwarding, and contract logistics, designed to enhance operational efficiency and visibility for clients across various industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bollore Logistics

- CEVA Logistics SA

- Correos

- Dachser SE

- DB Schenker

- DHL International GmbH

- DSV AS

- FM Logistic

- Gebruder Weiss

- General Logistics Systems BV

- GEODIS

- Hellmann Worldwide Logistics

- ID Logistics Group

- InPost SA

- Kuehne Nagel Management AG

- La Poste Group

- Poste Italiane SpA

- PostNL NV

- Rhenus SE and Co. KG

- XPO Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Europe logistics market

- In October 2024, Kuehne + Nagel announced a strategic partnership with a leading technology firm to integrate advanced AI-powered analytics into its supply chain visibility platform, enhancing predictive capabilities for its clients.

- In January 2025, XPO Inc. completed the acquisition of a specialized last-mile delivery company, strengthening its e-commerce fulfillment and urban logistics network across key European markets.

- In March 2025, DHL expanded its electric delivery fleet in several major European cities to advance its environmental objectives and address the complexities of urban delivery.

- In June 2025, DB Schenker announced the expansion of its contract logistics operations across multiple European countries to meet rising demand from e-commerce and manufacturing clients.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Europe Logistics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 214 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.5% |

| Market growth 2026-2030 | USD 51.3 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.4% |

| Key countries | Germany, UK, France, Belgium and Rest of Europe |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The logistics market in Europe is undergoing a significant transformation, driven by the convergence of digitalization and sustainability imperatives. Core operations are being redefined by the integration of a transportation management system (TMS) and a warehouse management system (WMS), which are essential for achieving end-to-end supply chain optimization.

- The adoption of advanced systems for route optimization and fleet management is no longer optional but a baseline requirement for competitive positioning. Firms leveraging integrated TMS platforms have reported a reduction in freight spend of up to 8% through better asset utilization. This trend is particularly evident in the management of last-mile delivery, where efficiency gains are critical.

- The market is also seeing a clear distinction between third-party logistics (3PL) and the more strategic fourth-party logistics (4PL) models, with the latter focusing on orchestrating complex networks. Key areas like contract logistics, freight forwarding, and automated warehousing are at the forefront of this evolution, pushing providers to innovate continuously to meet demands for greater supply chain visibility and resilience.

What are the Key Data Covered in this Europe Logistics Market Research and Growth Report?

-

What is the expected growth of the Europe Logistics Market between 2026 and 2030?

-

USD 51.3 billion, at a CAGR of 3.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (3PL, and 4PL), End-user (Manufacturing, Automotive, Consumer goods, Retail industry, and Others), Mode of Transportation (Roadways, Waterways, Railways, and Airways) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Booming e-commerce industry in Europe, High cost of operation and competitive pricing

-

-

Who are the major players in the Europe Logistics Market?

-

Bollore Logistics, CEVA Logistics SA, Correos, Dachser SE, DB Schenker, DHL International GmbH, DSV AS, FM Logistic, Gebruder Weiss, General Logistics Systems BV, GEODIS, Hellmann Worldwide Logistics, ID Logistics Group, InPost SA, Kuehne Nagel Management AG, La Poste Group, Poste Italiane SpA, PostNL NV, Rhenus SE and Co. KG and XPO Inc.

-

Market Research Insights

- The market is shaped by intense competitive dynamics and a strategic shift toward integrated logistics services. The adoption of end-to-end supply chain solutions is becoming standard as organizations seek to improve resilience and efficiency. For example, businesses leveraging digital logistics platforms report an average 15% reduction in administrative overhead compared to those using manual processes.

- Furthermore, implementing comprehensive supply chain analytics enables a 20% improvement in demand forecasting accuracy, directly impacting inventory carrying costs. This push for optimization is driven by the need for greater supply chain resilience in a volatile economic environment.

- Providers are responding by expanding their value-added logistics services and investing in smart warehousing to deliver measurable performance gains and secure long-term partnerships with clients.

We can help! Our analysts can customize this europe logistics market research report to meet your requirements.

RIA -

RIA -