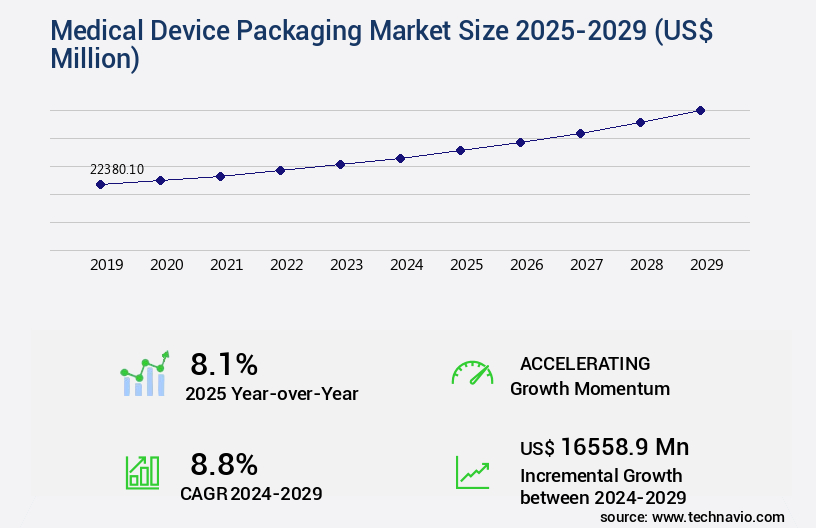

Medical Device Packaging Market Size 2025-2029

The medical device packaging market size is valued to increase by USD 16.56 billion, at a CAGR of 8.8% from 2024 to 2029. Growing adoption of medical devices will drive the medical device packaging market.

Market Insights

- Europe dominated the market and accounted for a 32% growth during the 2025-2029.

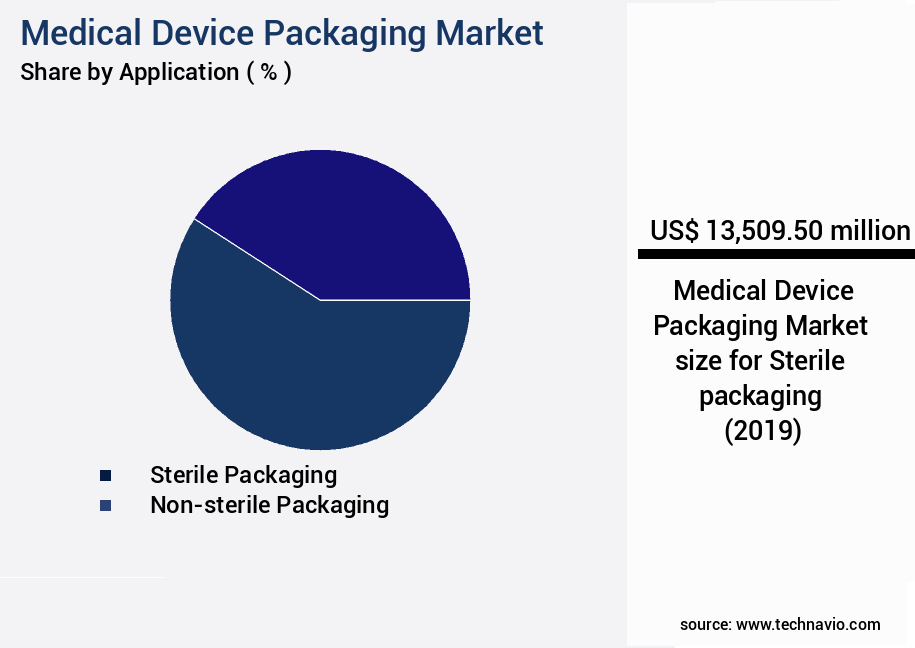

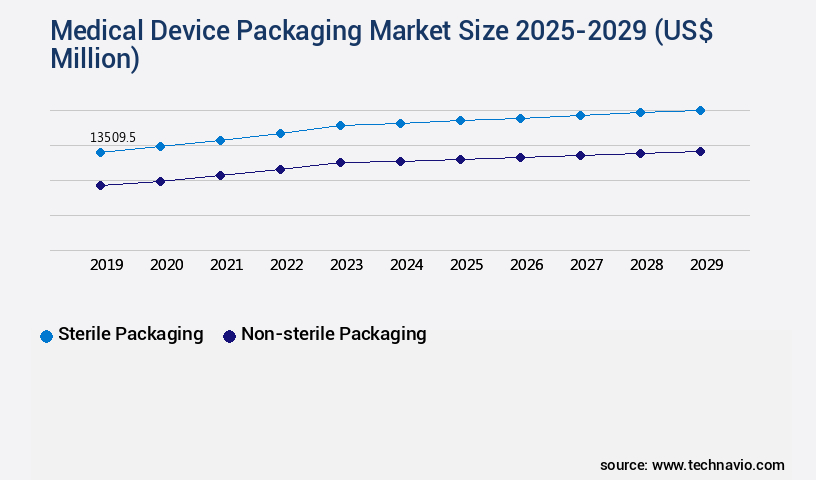

- By Application - Sterile packaging segment was valued at USD 13.51 billion in 2023

- By Product - Pouches segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 114.47 million

- Market Future Opportunities 2024: USD 16558.90 million

- CAGR from 2024 to 2029 : 8.8%

Market Summary

- Medical device packaging plays a pivotal role in ensuring the safety, efficacy, and sterility of healthcare products. The global market for medical device packaging is driven by the growing adoption of medical devices, particularly in emerging economies, and the technological advances in this field. Innovations such as active and intelligent packaging, which provide real-time monitoring of temperature, humidity, and other critical conditions, are gaining popularity. One significant trend in medical device packaging is achieving cost-effectiveness without compromising quality. For instance, supply chain optimization through efficient inventory management and lean manufacturing practices can lead to substantial savings. A leading medical device manufacturer reported a 15% reduction in packaging material costs by implementing a just-in-time inventory system.

- This not only improved operational efficiency but also ensured that the company remained compliant with regulatory requirements. Moreover, regulatory compliance continues to be a major challenge in the market. Strict regulations mandate that packaging materials meet specific standards to ensure the safety and efficacy of medical devices. For example, the European Union's Medical Devices Regulation (MDR) and the United States' Food and Drug Administration (FDA) have stringent guidelines for medical device packaging. Adhering to these regulations can be costly and time-consuming, but failure to do so can result in significant consequences, including product recalls and reputational damage. In conclusion, the market is witnessing significant growth due to the increasing adoption of medical devices, technological innovations, and the need for cost-effective and compliant solutions.

- Supply chain optimization and regulatory compliance are key challenges that medical device manufacturers must address to remain competitive in this market.

What will be the size of the Medical Device Packaging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with a focus on enhancing product protection, ensuring compliance, and improving efficiency. According to recent studies, the market is expected to grow by over 5% annually, underscoring its significance in the healthcare industry. This growth is driven by the increasing demand for advanced packaging solutions that offer extended shelf life, maintain closure integrity, and provide a microbial and gas barrier. Packaging validation plays a crucial role in this market, with companies investing in process validation, packaging testing, and good manufacturing practices to ensure patient safety. Packaging automation and label printing technologies are also gaining traction, streamlining production lines and reducing costs.

- Moreover, regulatory affairs are a top priority, with companies integrating barcode integration, design qualification, and regulatory compliance into their packaging strategies. Material science is at the forefront of innovation, with the development of barrier films and drug delivery systems that offer superior protection and functionality. RFID tagging and thermal printing are also becoming increasingly common, enabling real-time tracking and traceability. As budgeting and product strategy remain key boardroom-level decision areas, companies are turning to packaging solutions that offer cost savings, improved efficiency, and enhanced product protection.

Unpacking the Medical Device Packaging Market Landscape

The market encompasses a range of innovative solutions designed to ensure product traceability, integrity, and compliance in the healthcare sector. Peelable pouches and modified atmosphere packaging enhance supply chain efficiency by reducing damage during transportation. Package integrity testing, including leak testing methods and tamper evident seals, safeguards against contamination and ensures sterility assurance. Cleanroom validation and Tyvek material properties contribute to the production of pharmaceutical-grade packaging, aligning with ISO 11607 standards. Child-resistant closures and blister pack designs cater to safety requirements, while unit dose packaging and sterile drape systems promote sterility and aseptic conditions. Shelf life extension is a significant business outcome achieved through the use of high barrier films, oxygen scavengers, desiccant packs, and humidity indicators. Regulatory compliance is maintained through the implementation of sterile barrier systems, barrier film testing, and label integrity checks. Transport packaging solutions, such as perforated packaging and flexible film pouches, offer protection during transit while adhering to e-beam sterilization and material compatibility requirements. Gamma irradiation and tray sealing equipment further ensure the sterility and integrity of medical devices.

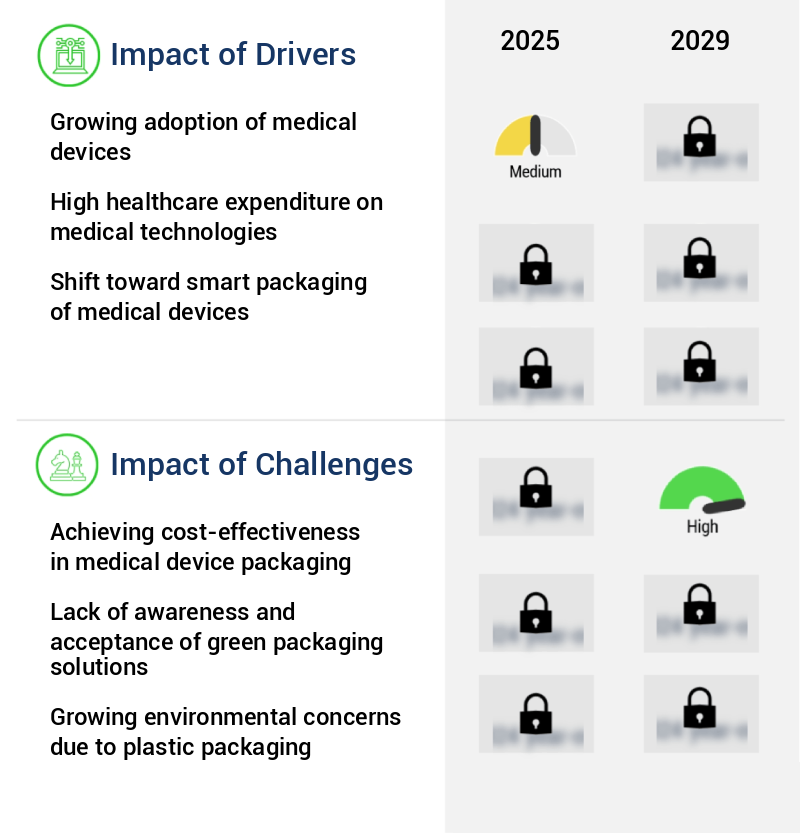

Key Market Drivers Fueling Growth

The increasing acceptance and implementation of medical devices serve as the primary catalyst for market growth. The growing acceptance and implementation of medical devices are the primary drivers propelling market expansion. The market's growth is predominantly fueled by the expanding adoption and utilization of medical devices.

- The market encompasses a diverse range of solutions, including trays, pouches, and clamshells, catering to various medical devices such as surgery equipment, technical aid products, intensive care units, and hygiene devices. The global demand for medical devices is projected to expand, fueled by the increasing aging population and the rising prevalence of chronic diseases. For instance, France, a leading medical device market, is anticipated to experience a moderate growth rate due to its robust regulatory environment and high-quality clinical research.

- Efficient market approval processes and cost-effectiveness are enticing medical device manufacturers to expand their market presence in advanced European countries like Germany. This dynamic market is poised to deliver significant benefits, including enhanced regulatory compliance and optimized costs, thereby underpinning its importance in the healthcare sector.

Prevailing Industry Trends & Opportunities

The trend in the market is being driven by technological advances. Technological innovations are shaping the future of medical device packaging.

- The market is experiencing significant evolution, driven by technological advancements and increasing demand across various sectors. Innovative packaging solutions are essential for protecting and preserving the functionality of medical devices, particularly in implantable devices and medical imaging equipment. For instance, hermetic packaging is widely used in implantable medical devices to safeguard electronic circuitry against the harsh environment of the human body. This technology is particularly important in miniaturized implantable devices. Furthermore, the adoption of PETG thermoform packaging, which functions effectively in both sterile and non-sterile environments, is expected to boost the market growth.

- This growth can be attributed to the need for faster product rollouts, regulatory compliance, and cost optimization in the healthcare industry.

Significant Market Challenges

In the medical device industry, ensuring cost-effectiveness in packaging is a critical challenge that significantly impacts growth. This requirement necessitates the implementation of efficient design and manufacturing processes while maintaining regulatory compliance and ensuring product safety.

- In the dynamic the market, companies are continually seeking cost-effective solutions to meet customer demands. A significant expense in medical device packaging is the choice of packaging materials. To minimize costs, companies prioritize materials that offer resistance to damage and maintain sterility throughout the product's life cycle. Another essential factor in achieving cost-effectiveness is managing the fluctuation in raw material and manufacturing costs, which collectively account for a substantial portion of production expenses.

- By focusing on these factors, medical device packaging providers can deliver sustainable and affordable solutions to their clients.

In-Depth Market Segmentation: Medical Device Packaging Market

The medical device packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Sterile packaging

- Non-sterile packaging

- Product

- Pouches

- Trays

- Clamshells

- Others

- End-user

- Hospital

- Diagnostic centers

- ASCs

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The sterile packaging segment is estimated to witness significant growth during the forecast period.

In the dynamic the market, maintaining product sterility and integrity is paramount. Sterile packaging, which acts as a protective barrier between devices and their environment, is crucial for invasive, implantable, or single-use products that come into contact with human tissue and fluids. Various materials, including foil packages, Tyvek pouches, and rigid packs, are employed for sterile device encasement. Tyvek, for instance, is favored due to its resistance to air and water vapor, ensuring microorganism contamination is prevented. In April 2023, DuPont invested over USD100 million into its Healthcare Industries business to expand Tyvek production capacity. Packaging methods encompass peelable pouches, modified atmosphere, cleanroom validation, tamper evident seals, and transport packaging.

Leak testing methods, such as mass flow decay, bubble leak testing, and helium leak detection, ensure package integrity. Regulatory compliance is a priority, with standards like ISO 11607 guiding label integrity, aseptic packaging, and barrier film testing. Oxygen scavengers, desiccant packs, and humidity indicators extend shelf life. Sterile barrier systems, pharmaceutical packaging, sterile drape systems, medical grade plastics, and high barrier films are integral components. E-beam sterilization, material compatibility, gamma irradiation, and tray sealing equipment further fortify the packaging process. Key trends include the use of child resistant closures, blister pack design, unit dose packaging, and supply chain integrity.

The Sterile packaging segment was valued at USD 13.51 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 32% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Medical Device Packaging Market Demand is Rising in Europe Request Free Sample

The European the market is a significant and evolving sector, with over 25,000 medical technology companies, the majority of which are small and medium enterprises (SMEs) that frequently require packaging solutions. This region, home to countries like Germany, the UK, Italy, Switzerland, France, and Spain, is expected to witness growth in the medical device packaging industry. The region's developed infrastructure and efficient logistics connectivity contribute to this expansion. The European the market's growth is further fueled by increasing healthcare expenditures and the presence of established industry players.

Germany leads the European market, generating the largest revenue share, followed closely by France and the UK. The importance of regulatory compliance and cost reduction in the medical device industry is driving the adoption of advanced packaging technologies, ensuring the safe and efficient transport and storage of medical devices.

Customer Landscape of Medical Device Packaging Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Medical Device Packaging Market

Companies are implementing various strategies, such as strategic alliances, medical device packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amcor Plc - This company specializes in innovative medical device packaging solutions, including dual-chamber pouches, grid-coated paper, and crystal shield medical laminates. Their offerings prioritize safety, sterility, and functionality for various medical applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- CCL Industries Inc.

- Constantia Flexibles Group GmbH

- DuPont de Nemours Inc.

- Gerresheimer AG

- Glenroy Inc.

- Healthcare Print and Packaging Ltd.

- KP Holding GmbH and Co. KG

- Life Science Outsourcing Inc.

- Oliver Healthcare Packaging Co.

- RENOLIT SE

- Riverside Medical Packaging Co. Ltd.

- rose plastic AG

- Sonoco Products Co.

- Sterimed

- West Pharmaceutical Services Inc.

- WestRock Co.

- Wipak Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Medical Device Packaging Market

- In August 2024, Medtronic plc, a leading medical technology, services, and solutions company, announced the launch of its new SteriFlo Advantage Sterilization System for medical device packaging. This innovative system, which utilizes ethylene oxide (EtO) sterilization, is designed to reduce cycle times and improve efficiency in sterilization processes (Medtronic Press Release, 2024).

- In November 2024, Amcor plc, a global packaging company, entered into a strategic partnership with Siemens Healthineers, a leading medical technology provider. The collaboration aimed to develop advanced, sustainable medical device packaging solutions using Amcor's innovative materials and Siemens Healthineers' expertise in medical technology (Amcor Press Release, 2024).

- In March 2025, Thermo Fisher Scientific Inc., a biotechnology product development and manufacturing company, completed the acquisition of Pall Corporation's Biotech and Medical Businesses. This acquisition expanded Thermo Fisher Scientific's portfolio in the market, adding capabilities in filtration, separation, and purification technologies (Thermo Fisher Scientific Press Release, 2025).

- In May 2025, the European Commission approved the use of a new type of medical device packaging material, PEEK-OPTIMA, for certain medical devices. This approval marked a significant shift towards the use of more sustainable and biocompatible materials in medical device packaging (European Commission Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Medical Device Packaging Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

225 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.8% |

|

Market growth 2025-2029 |

USD 16558.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

8.1 |

|

Key countries |

US, China, Germany, France, UK, India, Canada, Japan, Brazil, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Medical Device Packaging Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is a critical sector that ensures the safety and efficacy of medical devices by providing appropriate containment and protection. High barrier films are increasingly being used in medical device packaging due to their ability to maintain the sterility and integrity of sensitive components. The sterile barrier systems validation process is a rigorous testing regime to ensure the effectiveness of these films. Another trend in medical device packaging is the use of modified atmosphere packaging for pharmaceuticals and medical devices. This approach extends the shelf life of products by altering the atmospheric conditions within the packaging. E-beam sterilization and gamma irradiation are common sterilization methods for medical device components, with each having unique effects on packaging materials. Leak testing methods for sterile packaging are essential to maintain the integrity of the sterile barrier. Child-resistant closures are also crucial for medical products to prevent accidental exposure to children.

Aseptic packaging is a vital consideration for sensitive medical devices, ensuring the absence of contaminants during manufacturing, filling, and administration. Supply chain integrity is a significant concern in medical device packaging. Material compatibility testing protocols and ISO 11607 compliant packaging designs help ensure that the packaging materials do not adversely affect the medical devices or their performance. Shelf life extension strategies, such as the use of antimicrobial agents and improved packaging designs, are also essential. Packaging design for improved patient safety is a key focus area, with automated packaging systems and quality control measures becoming increasingly common. Good manufacturing practices and regulatory compliance are essential to ensure the safety and efficacy of medical devices. Thermal printing technology and RFID tagging are used for medical device labeling and traceability, while contract packaging services offer flexible solutions for medical device manufacturers.

What are the Key Data Covered in this Medical Device Packaging Market Research and Growth Report?

-

What is the expected growth of the Medical Device Packaging Market between 2025 and 2029?

-

USD 16.56 billion, at a CAGR of 8.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Sterile packaging and Non-sterile packaging), Product (Pouches, Trays, Clamshells, and Others), End-user (Hospital, Diagnostic centers, and ASCs), and Geography (Europe, North America, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing adoption of medical devices, Achieving cost-effectiveness in medical device packaging

-

-

Who are the major players in the Medical Device Packaging Market?

-

Amcor Plc, CCL Industries Inc., Constantia Flexibles Group GmbH, DuPont de Nemours Inc., Gerresheimer AG, Glenroy Inc., Healthcare Print and Packaging Ltd., KP Holding GmbH and Co. KG, Life Science Outsourcing Inc., Oliver Healthcare Packaging Co., RENOLIT SE, Riverside Medical Packaging Co. Ltd., rose plastic AG, Sonoco Products Co., Sterimed, West Pharmaceutical Services Inc., WestRock Co., and Wipak Group

-

We can help! Our analysts can customize this medical device packaging market research report to meet your requirements.

RIA -

RIA -