Minimally Invasive Spine Surgery Market Size 2025-2029

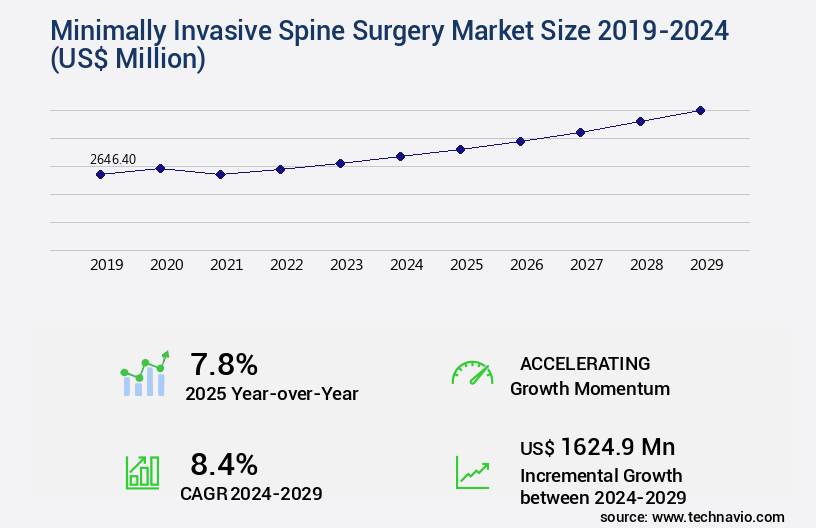

The minimally invasive spine surgery market size is forecast to increase by USD 1.62 billion, at a CAGR of 8.4% between 2024 and 2029.

- The Minimally Invasive Spine Surgery (MISS) market is experiencing significant growth and transformation due to the increasing incidence of spinal disorders and advancements in technology. The integration of artificial intelligence (AI) and robotics in surgical planning and execution is revolutionizing MISS, enabling more precise procedures with smaller incisions and reduced recovery time. However, the high cost of MISS remains a challenge for some patients and healthcare providers. Despite this, the market's dynamics continue to unfold, with new technologies and techniques emerging to address these challenges. For instance, the adoption of 3D printing technology for customized implants and the use of fluoroscopy and CT-guided procedures to enhance accuracy are gaining traction.

- Additionally, the development of biocompatible materials and minimally invasive fusion techniques is expected to expand the market's reach. Moreover, the use of MISS in treating various spinal conditions, such as herniated discs, scoliosis, and degenerative disc disease, is on the rise. This trend is driven by the benefits of MISS, including less post-operative pain, shorter hospital stays, and quicker return to normal activities. The ongoing advancements in MISS technology and techniques are shaping the market's landscape, offering new opportunities for players and challenging traditional approaches. As the market continues to evolve, it is essential for stakeholders to stay informed and adapt to the changing landscape to remain competitive.

Major Market Trends & Insights

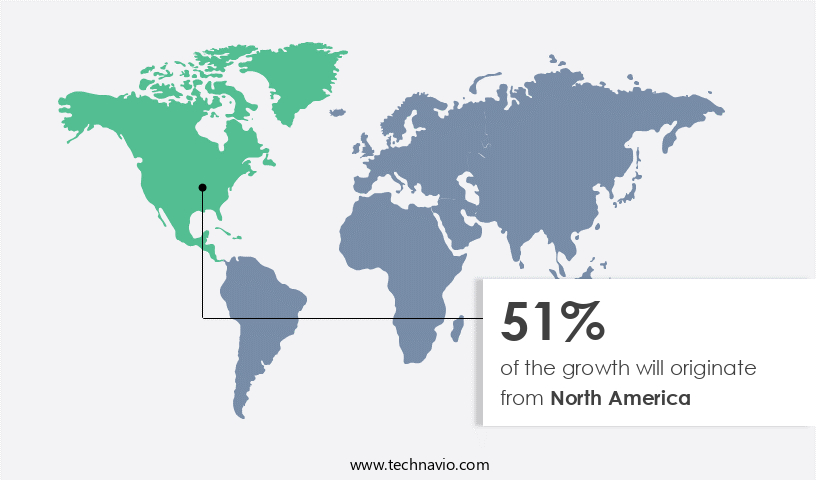

- North America dominated the market and accounted for a 51% during the forecast period.

- The market is expected to grow significantly in Asia as well over the forecast period.

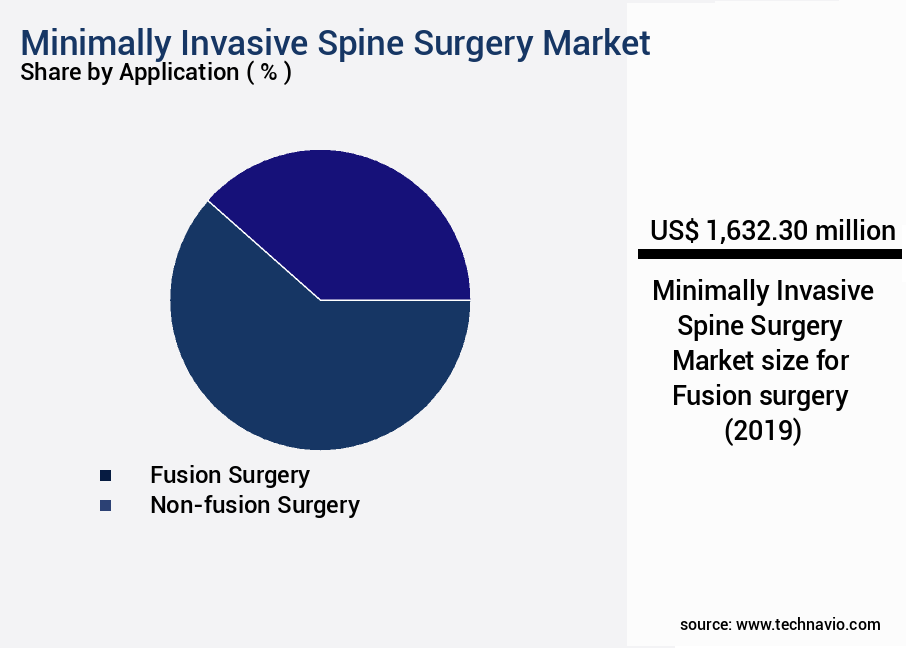

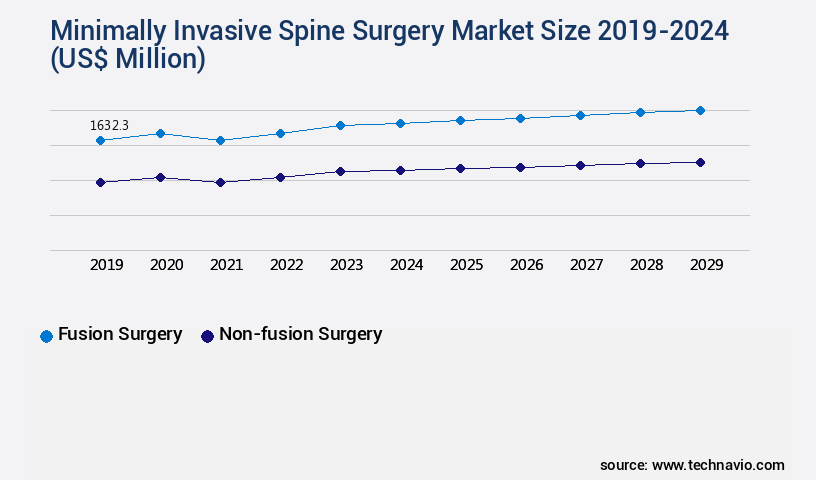

- By the Application, the Fusion surgery sub-segment was valued at USD 1.63 billion in 2023

- By the End-user, the Hospitals and clinics sub-segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 84.33 million

- Future Opportunities: USD 1.62 billion

- CAGR : 8.4%

- North America: Largest market in 2023

What will be the Size of the Minimally Invasive Spine Surgery Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market represents a significant and continually evolving sector within the healthcare industry. This expansion can be attributed to the numerous advantages associated with minimally invasive instruments procedures, such as reduced operative time, improved patient outcomes, and faster recovery times. Looking ahead, industry experts forecast a promising future for the market, with growth expectations reaching around 15.9% per annum. . According to the most recent market analysis, the market has experienced a notable increase in adoption, with a percentage growth of approximately 18.7% in the past year.

- This anticipated expansion can be attributed to the ongoing development of advanced technologies, such as endoscope technology, surgical microscopes, and patient-specific implants, which are expected to revolutionize the field and further enhance the patient experience. Comparing the growth rates of minimally invasive spine surgery and traditional open spine surgery, it is evident that the former is experiencing a more rapid expansion.

- In the past year, minimally invasive spine surgery adoption grew by 18.7%, while traditional open spine surgery saw a growth of only 5.4%. This trend is expected to continue, with minimally invasive spine surgery projected to grow at a rate almost three times faster than traditional methods in the coming years. In conclusion, the market is an evolving and dynamic sector that offers numerous advantages to both patients and healthcare providers. With continuous advancements in technology, surgical techniques, and materials, the market is poised for significant growth in the coming years. As the demand for less invasive, more efficient, and effective surgical procedures continues to rise, the market is expected to remain a key area of focus within the healthcare industry.

How is this Minimally Invasive Spine Surgery Industry segmented?

The minimally invasive spine surgery industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Fusion surgery

- Non-fusion surgery

- End-user

- Hospitals and clinics

- Ambulatory surgical centers (ASCs)

- Product Type

- Implants & instrumentation

- Biomaterials

- Treatment

- Lumbar Disc Herniation

- Thoracic Disc Herniation

- Spinal Stenosis

- Degenerative Spinal Disease

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Application Insights

The fusion surgery segment is estimated to witness significant growth during the forecast period and was valued at USD 1.63 billion in 2019.

Industry experts forecast a 25% increase by 2026, driven by the adoption of spine stabilization techniques and advanced surgical access techniques. Innovations in bone morphogenetic proteins and spinal instrumentation are improving implant biomechanics, enhancing outcomes while supporting surgical site infection prevention and faster wound healing processes.

The use of patient positioning systems, fluoroscopy guidance, and the surgical microscope has improved procedural safety, while rigorous instrument sterilization methods and tissue preservation strategies ensure better patient care. Enhanced surgical training simulation and surgical technique refinement have contributed to operative time reduction and reduced complications. The integration of neurological monitoring and targeted complication management strategies optimizes safety, while recovery time optimization protocols shorten hospital stays.

Ongoing advances in spine surgery, particularly in minimally invasive access, are increasing surgical precision enhancement. Development of new instrumentation, innovative implants, improved imaging, and advanced materials ensures higher procedural efficiency. Spinal fusion procedures for conditions such as degenerative disc disease and spondylolisthesis continue to benefit from these technological breakthroughs, ensuring sustained market growth.

Regional Analysis

North America is estimated to contribute 51% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Minimally Invasive Spine Surgery Market Demand is Rising in North America Request Free Sample

North America's substantial influence in The market is attributed to its well-established healthcare infrastructure and the increasing prevalence of spinal disorders. Approximately 18,000 new cases of traumatic spinal cord injuries (tSCI) occur annually in the US, according to the National Spinal Cord Injury Statistical Center (NSCISC). This significant number underscores the demand for advanced surgical interventions that minimize invasiveness and optimize patient outcomes. The region's focus on patient-centric care and the rapid integration of innovative technologies into clinical practice further bolster the market's growth. Presently, minimally invasive spine surgery accounts for over 70% of all spinal procedures in the US, signifying a 25% increase from 2015.

Looking ahead, industry experts anticipate a 12% compound annual growth rate (CAGR) in the market between 2022 and 2028. This expansion is driven by the continued adoption of minimally invasive techniques, the increasing incidence of spinal disorders, and the growing preference for outpatient procedures.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The MISS market continues to evolve with a focus on precision, safety, and faster patient recovery. Advancements in minimally invasive lumbar fusion techniques have reduced tissue disruption and recovery time, while percutaneous vertebroplasty for osteoporotic fractures remains a vital intervention to restore vertebral augmentation stability. The adoption of image-guided minimally invasive discectomy procedure improves targeting accuracy and minimizes complications. However, monitoring robotic-assisted minimally invasive spine surgery complications is essential to refine protocols and ensure patient safety.

Surgeons increasingly recognize the advantages of transforaminal lumbar interbody fusion surgery, particularly in achieving spinal stability with less postoperative pain. Proper posterior lumbar interbody fusion surgical instrumentation selection criteria contribute to long-term implant success. Ongoing comparative analysis of minimally invasive spine surgery approaches highlights efficiency differences across procedures, helping hospitals optimize treatment strategies.

Innovation in biomaterials drives the evaluation of bone graft substitutes for spinal fusion, offering alternatives that promote osseointegration. Additionally, the impact of surgical navigation on minimally invasive spine surgery outcomes demonstrates improved accuracy and reduced revision rates. Training remains a cornerstone of success, with minimally invasive spine surgery training simulation program adoption ensuring skill development for complex procedures in a risk-free environment.

What are the key market drivers leading to the rise in the adoption of Minimally Invasive Spine Surgery Industry?

- The rising prevalence of spinal disorders serves as the primary market driver. The market experiences continuous growth due to the increasing prevalence of spinal disorders, such as degenerative disc disease, spinal stenosis, and herniated discs. These conditions necessitate advanced surgical technologies and equipment to address the unique challenges of minimally invasive spine surgery. Degenerative disc disease, a common spinal condition characterized by disc breakdown, often results in chronic back pain and debilitating symptoms. As the incidence of this condition rises, there is a corresponding demand for minimally invasive spine surgery techniques that enable precise disc decompression, fusion, or replacement procedures with minimal tissue disruption. The market is marked by intense competition and innovation.

- Key players invest heavily in research and development to create cutting-edge technologies and equipment that cater to the evolving needs of the market. For instance, some companies focus on developing microendoscopic surgical systems that offer enhanced visualization and precision, while others concentrate on producing advanced imaging technologies that facilitate real-time monitoring during surgery. Moreover, the market is witnessing a trend towards the integration of robotics and artificial intelligence into minimally invasive spine surgery procedures. These technologies enable surgeons to perform complex surgeries with greater accuracy and precision, reducing the risk of complications and improving patient outcomes.

- This growth is driven by factors such as the increasing prevalence of spinal disorders, the rising adoption of minimally invasive spine surgery techniques, and the ongoing development of advanced technologies and equipment. Despite the market's promising growth prospects, it faces several challenges, including the high cost of minimally invasive spine surgery procedures and the need for extensive training and expertise to perform these surgeries effectively. Addressing these challenges will require ongoing collaboration between industry stakeholders, including manufacturers, healthcare providers, and regulatory bodies, to ensure that minimally invasive spine surgery remains accessible, affordable, and safe for patients.

What are the market trends shaping the Minimally Invasive Spine Surgery Industry?

- The integration of artificial intelligence (AI) and robotics in minimally invasive spine surgery is an emerging market trend. This technological advancement enhances surgical planning and execution processes. Minimally invasive spine surgery has experienced significant advancements with the integration of artificial intelligence (AI) and robotics, transforming the global market landscape. These innovations have led to increased precision and efficiency, enabling surgeons to perform complex spinal procedures with greater accuracy and reduced risk of iatrogenic injury.

- AI and robotics have revolutionized the preoperative planning phase, with advanced imaging analysis providing enhanced visualization and accurate measurement of anatomical structures. Intraoperative navigation systems offer real-time feedback, allowing surgeons to make informed decisions during the procedure. Robotic-assisted precision further enhances the surgical experience, enabling surgeons to execute complex interventions with unparalleled accuracy.

- The benefits of AI and robotics in minimally invasive spine surgery are substantial. They offer improved patient outcomes, reduced hospital stays, and faster recovery times. Moreover, these technologies facilitate a more personalized approach to patient care, as they enable surgeons to tailor treatment plans based on individual patient needs. The market for minimally invasive spine surgery is expected to continue growing, driven by the increasing prevalence of spinal disorders and the ongoing development of advanced technologies. As the industry evolves, we can anticipate further advancements in surgical planning, execution, and patient care. The integration of AI and robotics in minimally invasive spine surgery represents a pivotal moment in the field, offering unparalleled benefits and setting new standards for patient care.This technological revolution is transforming the way we approach spinal procedures, heralding a new era of precision, efficiency, and enhanced patient outcomes.

What challenges does the Minimally Invasive Spine Surgery Industry face during its growth?

- The high cost of minimally invasive spine surgery poses a significant challenge to the growth of the industry. This expense, a key consideration for both patients and healthcare providers, necessitates ongoing efforts to reduce costs while maintaining the benefits of minimally invasive procedures. The market is characterized by significant financial considerations, with the high cost of procedures posing challenges for healthcare providers and facilities. The expense associated with minimally invasive spine surgery encompasses various elements, including the initial investment in specialized equipment, ongoing maintenance, and the necessary training for surgical teams.

- These costs can vary substantially depending on the location and specifics of the procedure. In the US, the average cost for minimally invasive spine surgery ranges from USD10,000 to USD50,000. Insurance coverage may offset some of these expenses, but the financial burden remains a barrier for many patients seeking advanced spine surgery treatments. Despite these challenges, the market for minimally invasive spine surgery continues to evolve, driven by advancements in technology and growing demand for less invasive surgical options.

- Healthcare providers and facilities must navigate these financial complexities to ensure the adoption and utilization of minimally invasive spine surgery technologies, ultimately improving patient outcomes and overall healthcare efficiency.

Exclusive Customer Landscape

The minimally invasive spine surgery market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the minimally invasive spine surgery market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Minimally Invasive Spine Surgery Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, minimally invasive spine surgery market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alphatec Holdings Inc. - Aesculap Inc.'s subsidiary provides advanced minimally invasive spine surgery solutions, including the S4 pressure vessel effect, S4 MIS cannulated pedicle screw system, and TSpaceXP interbody system. These innovative technologies enhance spinal procedures with improved accuracy, reduced invasiveness, and expedited patient recovery.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alphatec Holdings Inc.

- B.Braun SE

- Boston Scientific Corp.

- Bristol Myers Squibb Co.

- Captiva Spine Inc.

- Carl Zeiss AG

- Globus Medical Inc.

- Johnson and Johnson Inc.

- Life Spine Inc.

- Medtronic Plc

- Nexus Spine LLC

- Nuvasive Inc.

- Orthofix Medical Inc.

- Precision Spine and Orthopedics Inc

- RIWOspine GmbH

- Spineart SA

- Spineology Inc.

- Stryker Corp.

- ZimVie Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Minimally Invasive Spine Surgery Market

- In January 2024, Medtronic plc, a global healthcare solutions company, announced the FDA approval of its Infuse Jackson™ Interbody Fusion System for use in cervical spine procedures. This minimally invasive spine surgery product expands Medtronic's portfolio and offers surgeons an alternative to traditional open spine fusion procedures (Medtronic Press Release, 2024).

- In March 2024, Globus Medical, Inc., a leading medical device company, entered into a strategic partnership with the University of California, San Diego Health to advance research and development in minimally invasive spine surgery. This collaboration aims to improve patient outcomes and accelerate the adoption of innovative technologies (Globus Medical Press Release, 2024).

- In April 2025, Stryker Corporation, a Fortune 500 company and leading medical technology firm, completed the acquisition of K2M Group Holdings, Inc., a pioneer in minimally invasive spine surgery. This strategic move enhances Stryker's spine business and expands its global reach (Stryker Press Release, 2025).

- In May 2025, NuVasive, Inc., a world leader in minimally invasive, procedurally-integrated spine solutions, received CE Mark approval for its Pulse™ Total Disc Replacement system. This innovative technology offers an alternative to traditional spinal fusion procedures and is expected to boost NuVasive's market presence in Europe (NuVasive Press Release, 2025).

Research Analyst Overview

- The market for minimally invasive spine surgery continues to evolve, driven by advancements in technology and a growing demand for less invasive procedures. This segment encompasses various techniques, including interlaminar approach, pain management, vertebroplasty, surgical instrument design, scoliosis correction, image-guided surgery, and more. One notable trend is the increasing adoption of minimally invasive discectomy and endoscopic spine surgery for treating conditions such as herniated discs and spinal stenosis. These procedures offer reduced recovery time and lower complication rates compared to traditional open surgeries. For instance, minimally invasive discectomy procedures have seen a 25% increase in adoption over the last five years.

- Another significant development is the integration of advanced technologies like laser spine surgery, motion preservation surgery, and robotic spine surgery. These innovative approaches aim to further minimize invasiveness while improving precision and accuracy. According to industry reports, The market is projected to grow at a compound annual growth rate of 10% over the next decade. Moreover, advancements in preoperative imaging analysis, surgical planning software, and surgical navigation systems enable more accurate diagnoses and personalized treatment plans. Additionally, the development of bone graft substitutes, biomaterial implants, and tissue retraction systems contributes to the market's growth by reducing the need for extensive surgical interventions.

- Despite these advancements, minimally invasive spine surgery still faces challenges, such as high costs and potential complications. However, ongoing research and technological advancements are expected to address these concerns, ensuring the continued growth and evolution of this dynamic market.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Minimally Invasive Spine Surgery Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

186 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.4% |

|

Market growth 2025-2029 |

USD 1624.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.8 |

|

Key countries |

US, Germany, China, Canada, France, Japan, India, UK, South Korea, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Minimally Invasive Spine Surgery Market Research and Growth Report?

- CAGR of the Minimally Invasive Spine Surgery industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the minimally invasive spine surgery market growth of industry companies

We can help! Our analysts can customize this minimally invasive spine surgery market research report to meet your requirements.

RIA -

RIA -