North America Corrugated Packaging Market Size 2024-2028

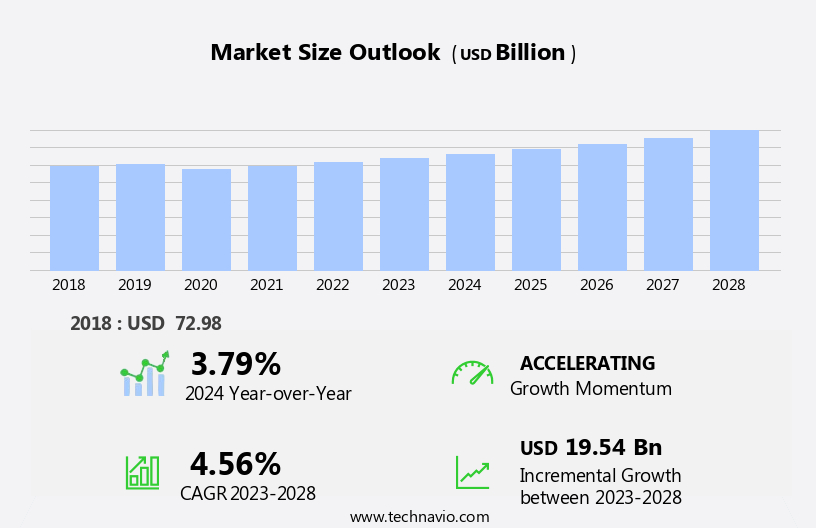

The north america corrugated packaging market size is forecast to increase by USD 19.54 billion, at a CAGR of 4.56% between 2023 and 2028.

- The market is experiencing significant growth, driven primarily by the surge in e-commerce sales. With the increasing preference for online shopping, there is a rising demand for robust and protective packaging solutions. Corrugated packaging, with its durability and versatility, is an ideal choice for e-commerce applications. Another trend shaping the market is the integration of smart technologies. The adoption of RFID tags and sensors in corrugated packaging enhances supply chain visibility and efficiency, enabling real-time tracking and monitoring of inventory. This not only improves logistics but also ensures product safety and customer satisfaction. However, the market is not without challenges.

- The volatility in raw material prices poses a significant threat to market stability. Fluctuations in the prices of paper, pulp, and other raw materials can impact the profitability of corrugated packaging manufacturers. To mitigate this risk, companies must adopt strategies such as long-term contracts with suppliers, price hedging, and diversification of raw material sources.

What will be the size of the North America Corrugated Packaging Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

- The North American corrugated packaging market is experiencing significant activity and trends, shaping the industry's future. Value-added packaging, featuring shipping labels, barcode technology, and RFID tags, enhances consumer experience and brand identity. Sustainable sourcing and circular economy packaging are key priorities, driving the use of recycled materials and reducing waste. Robotics in packaging and automation streamline production, while packaging simulation and design software optimize product protection and innovation. Tamper-evident packaging and intelligent packaging ensure product safety and freshness. Packaging certification and waste reduction are crucial for companies to meet regulatory requirements and consumer expectations.

- Protective packaging and green packaging solutions cater to various industries and applications. Packaging material recycling and post-consumer recycled content are essential for a more eco-friendly industry. Overall, these trends reflect the dynamic and innovative nature of the market.

How is this market segmented?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Food and beverages

- Electronics and electricals

- Transport and logistics

- Others

- Product

- Corrugated box

- Folding boxboard

- Package Type

- Single Wall Boards

- Double Wall Boards

- Triple Wall Boards

- End-User

- Retail

- Industrial

- Logistics

- Material

- Recycled Paper

- Virgin Paper

- Geography

- North America

- US

- Canada

- Mexico

- North America

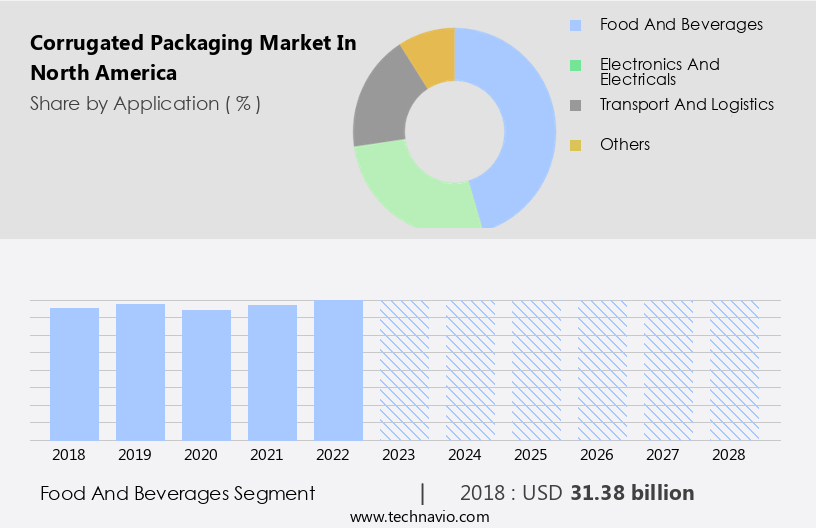

By Application Insights

The food and beverages segment is estimated to witness significant growth during the forecast period.

The market is experiencing notable growth due to the rising demand for electronic and electrical products. As the region's electronic and electrical industry expands, so does the need for secure and protective packaging solutions. This trend is particularly significant in the e-commerce sector, where efficient and safe distribution channels are crucial. Corrugated packaging offers numerous advantages, including moisture resistance, compression strength, and customizable designs, making it an ideal choice for protecting delicate electrical components during transit and storage. Additionally, its lightweight nature contributes to sustainability efforts. The market's evolution includes various flute types, finishing processes, and testing procedures, such as drop testing, burst testing, and moisture barrier testing, to ensure the highest quality standards.

Furthermore, the integration of biodegradable packaging options and advanced printing techniques, like offset and digital printing, caters to the evolving consumer preferences and packaging regulations. The corrugating machine, die cutting, and industrial packaging processes play a pivotal role in optimizing logistics and inventory management, while safety standards and stacking strength testing ensure the protection of various consumer goods, including food and consumer packaging.

The Food and beverages segment was valued at USD 31.38 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the North America Corrugated Packaging Market drivers leading to the rise in adoption of the Industry?

- The surge in e-commerce sales, resulting in heightened demand for corrugated packaging, serves as the primary market driver.

- The market is experiencing significant growth due to the increasing e-commerce sector. With e-commerce sales projected to reach approximately USD5.7 trillion in North America by 2022, surpassing the GDP of Germany and Japan, there is a rising demand for corrugated packaging. Factors such as the expanding e-commerce market, driven by rising smartphone penetration, increased affluence, and reduced data prices, provide opportunities for businesses of all sizes. Over 30 million small businesses in the US, many of which operate traditionally, can leverage e-commerce to expand their reach beyond local marketplaces. Corrugated packaging offers essential features for e-commerce, including moisture resistance, compression strength, and various flute types to accommodate different product shapes and sizes.

- Quality control and finishing processes ensure product protection during shipping. Optimizing logistics and inventory management through efficient packaging solutions can also help reduce shipping costs and improve overall supply chain performance. These factors make corrugated packaging a preferred choice for e-commerce businesses in North America.

What are the North America Corrugated Packaging Market trends shaping the Industry?

- The integration of advanced technologies, such as radio frequency identification (RFID) tags and sensors, is a significant market trend. These technologies enhance efficiency and accuracy in various industries, including supply chain management and manufacturing.

- The market is witnessing significant growth due to the integration of advanced technologies such as RFID tags and sensors. This innovation enhances supply chain management by enabling real-time tracking, authentication, and monitoring of products. By optimizing logistics, increasing inventory visibility, and maintaining product integrity during shipment, corrugated packaging producers offer a competitive advantage to organizations seeking efficiency and transparency in their operations. The e-commerce sector, in particular, benefits from precise and timely information on product location and condition, ensuring a reliable supply chain.

- Furthermore, the adoption of various printing techniques, including digital and offset, and the use of biodegradable materials align with the industry's focus on sustainability and reducing environmental impact. Drop testing and burst testing ensure the durability and strength of corrugated packaging, making it an ideal choice for industrial and retail applications. Die cutting and corrugating machines streamline production processes, further contributing to the market's growth.

How does North America Corrugated Packaging Market faces challenges face during its growth?

- The volatility in raw material prices poses a significant challenge to the industry's growth trajectory, necessitating careful cost management and strategic planning.

- The market faces significant challenges due to the volatility of raw material costs, primarily paper and cardboard. Unforeseen fluctuations in these inputs can significantly impact profitability and operational efficiency for manufacturers. For instance, an unexpected increase in paper pulp prices, a key raw material, can elevate production costs, affecting the entire cost structure of corrugated packaging. External factors, such as weather conditions affecting raw material cultivation and regional supply and demand dynamics, further complicate the situation. To remain competitive and ensure long-term sustainability, manufacturers must effectively manage these risks through strategic sourcing, pricing, and inventory management strategies. In the context of evolving market trends, corrugated packaging is increasingly being adopted for various applications, including pallet boxes, shipping containers, and e-commerce packaging.

- Advanced printing technologies, such as offset and digital printing, are being employed to enhance the visual appeal and functionality of these packages. Stringent safety standards are also driving the adoption of testing procedures like vibration testing to ensure product safety and integrity during transportation. Overall, the market continues to evolve, presenting both opportunities and challenges for market participants.

Exclusive North America Corrugated Packaging Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- Buckeye Corrugated Inc.

- Cascades Inc.

- DS Smith Plc

- Georgia-Pacific LLC

- Graphic Packaging Holding Co.

- Greif Inc.

- International Paper Co.

- Klabin SA

- MeadWestvaco Corp.

- Mondi Plc

- Nine Dragons Paper Holdings Ltd.

- Oji Holdings Corp.

- Packaging Corp. of America

- Pratt Industries Inc.

- Rengo Co. Ltd.

- Smurfit Kappa Group Plc

- Sonoco Products Co.

- Stora Enso Oyj

- WestRock Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Corrugated Packaging Market In North America

- In February 2023, Sealed Air Corporation, a leading player in the North American corrugated packaging market, announced the launch of its new Cryovac Duplex XTB vacuum packaging system. This innovative product is designed to increase productivity and reduce costs for food manufacturers by up to 50% compared to traditional vacuum packaging systems (Sealed Air Corporation, 2023).

- In May 2024, Ball Corporation and Smurfit Kappa, two major players in the North American corrugated packaging industry, announced their strategic partnership to expand their offerings in the beverage market. This collaboration will enable Ball to provide a more comprehensive range of sustainable packaging solutions to its customers, while Smurfit Kappa will benefit from Ball's expertise in beverage can production (Ball Corporation, 2024).

- In January 2025, Sonoco, a prominent player in the North American corrugated packaging market, completed the acquisition of MWI Corporation, a leading provider of flexible packaging solutions. This acquisition will enable Sonoco to expand its product portfolio and better serve its customers in the food, industrial, and consumer markets (Sonoco, 2025).

- In August 2025, the United States Environmental Protection Agency (EPA) introduced new regulations aimed at reducing the amount of corrugated packaging waste in landfills. The regulations mandate that corrugated packaging manufacturers use a minimum of 30% recycled content in their products by 2027. This initiative is expected to significantly boost the demand for recycled corrugated packaging in North America (EPA, 2025).

Research Analyst Overview

The market continues to evolve, driven by the diverse needs of various sectors. This dynamic industry encompasses entities focusing on pallet boxes, corrugated boxes, and shipping containers, among others. The continuous pursuit of safety standards and superior performance characterizes market activities. Compression strength, moisture resistance, and flute types are crucial considerations in the production process. Quality control and finishing processes, such as offset printing and digital printing, ensure the desired aesthetic and functional outcomes. E-commerce packaging, a significant application, necessitates vibration testing and edge protection for secure transit. Logistics optimization, inventory management, and supply chain management are essential aspects of the corrugated packaging market.

The industry's commitment to biodegradable packaging and environmental impact assessments reflects evolving consumer preferences and regulations. Industrial packaging applications require rigorous testing procedures, including drop testing, burst testing, and stacking strength testing. The corrugating machine, die cutting, and other manufacturing processes ensure the production of high-quality, customized packaging solutions. Flexographic printing, moisture barrier testing, and packaging design contribute to the industry's ongoing innovation. The corrugated packaging market's continuous dynamism underscores its relevance in various sectors, from retail to consumer goods and food packaging.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Corrugated Packaging Market in North America insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

151 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.56% |

|

Market growth 2024-2028 |

USD 19.54 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.79 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -