Digital Printing For Packaging Market Size 2026-2030

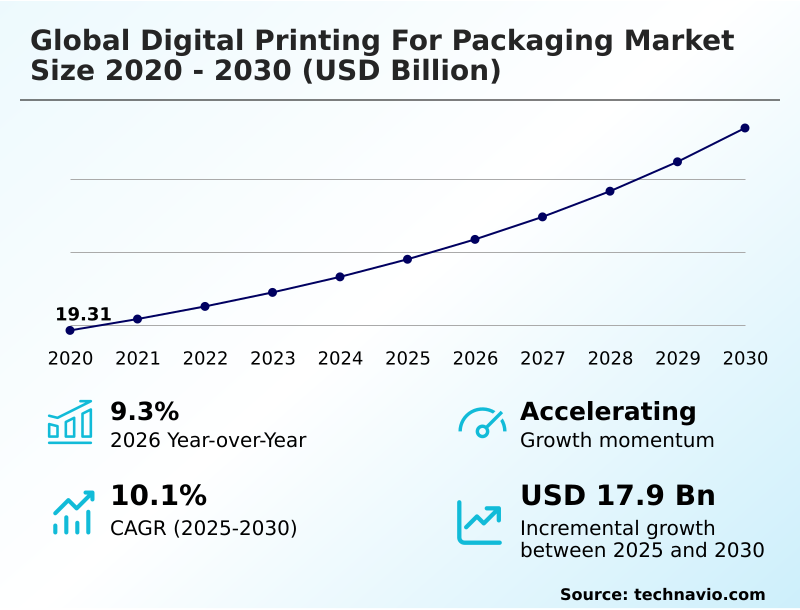

The digital printing for packaging market size is valued to increase by USD 17.90 billion, at a CAGR of 10.1% from 2025 to 2030. Escalating demand for hyper-personalization and scalable mass customization will drive the digital printing for packaging market.

Major Market Trends & Insights

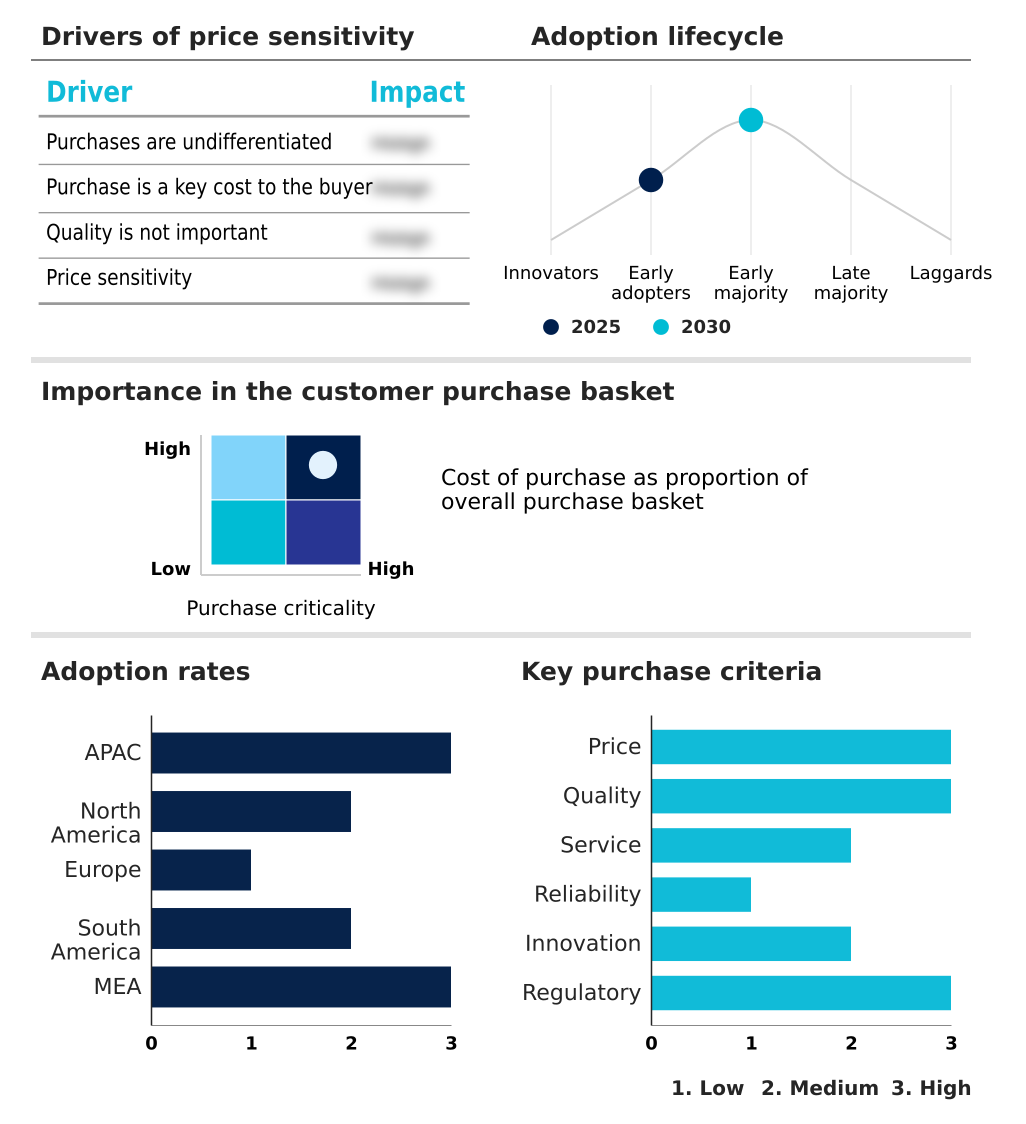

- APAC dominated the market and accounted for a 36.4% growth during the forecast period.

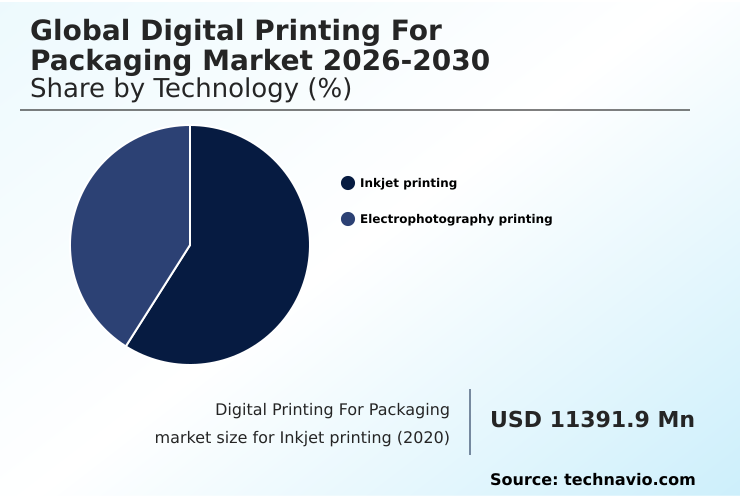

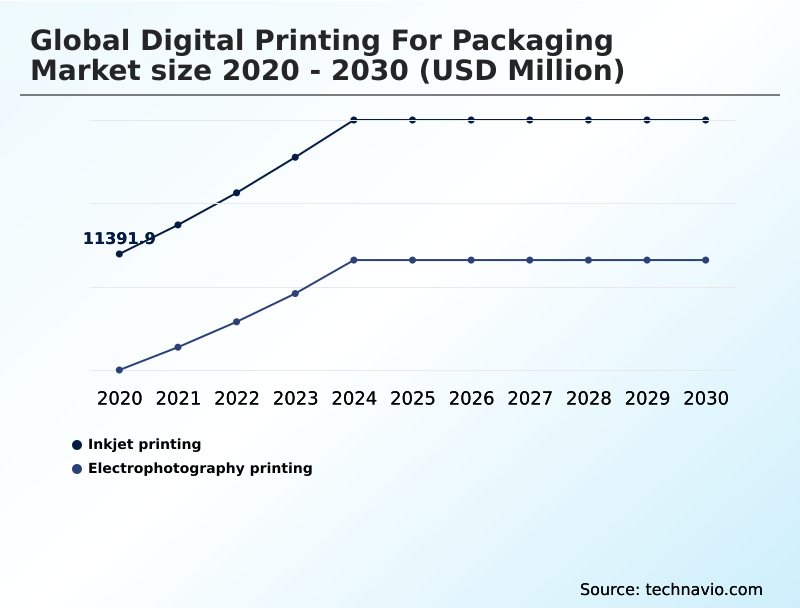

- By Technology - Inkjet printing segment was valued at USD 15.40 billion in 2024

- By Type - Labels segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 27.60 billion

- Market Future Opportunities: USD 17.90 billion

- CAGR from 2025 to 2030 : 10.1%

Market Summary

- The digital printing for packaging market is undergoing a significant transformation, driven by the need for greater supply chain agility and brand differentiation. Technologies such as high-speed inkjet and electrophotography are enabling on-demand production, which drastically reduces waste and inventory costs associated with traditional analog methods.

- This shift supports the growing demand for personalized and promotional packaging, especially within the e-commerce and fast-moving consumer goods sectors. For example, a beverage company can now execute a regional marketing campaign by printing unique codes on millions of labels, each linking to a different digital experience, without the massive overhead of plate changes.

- This capability facilitates just-in-time manufacturing and allows for rapid prototyping of new designs. However, challenges in achieving consistent color across diverse mono-material substrates and the high initial capital investment for digital press technology remain key considerations for converters.

- The integration of color management software and prepress automation is becoming critical to overcoming these hurdles and unlocking the full potential of digital workflows.

What will be the Size of the Digital Printing For Packaging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Digital Printing For Packaging Market Segmented?

The digital printing for packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Technology

- Inkjet printing

- Electrophotography printing

- Type

- Labels

- Flexible packaging

- Corrugated and folding cartons

- Others

- End-user

- Food and beverages

- Pharmaceutical

- Personal care and cosmetics

- Retail

- Others

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- APAC

By Technology Insights

The inkjet printing segment is estimated to witness significant growth during the forecast period.

Inkjet printing, a cornerstone of the digital printing for packaging market, is evolving through advancements in high-speed inkjet systems that enhance printhead longevity.

This non-contact technology is defined by superior nozzle density and drop placement accuracy, which are critical for achieving high-resolution graphics on diverse materials.

Innovations in pigment ink formulations have expanded its applicability, with automated color management ensuring brand integrity across production runs. For industrial applications, integrating these systems has led to a 15% increase in operational throughput.

The adaptability of small-batch production and rapid prototyping for packaging makes inkjet the preferred choice for sectors demanding both speed and premium branding without the constraints of traditional methods, supporting automated workflow integration and data-driven packaging.

The Inkjet printing segment was valued at USD 15.40 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 36.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Digital Printing For Packaging Market Demand is Rising in APAC Get Free Sample

The geographic landscape is increasingly influenced by regional e-commerce growth, particularly in APAC and North America, demanding sophisticated packaging solutions.

The adoption of liquid electrophotography and toner-based systems is critical for achieving the premium branding required in the luxury goods packaging and craft beverage labels markets.

In Europe, strict eco-labeling standards and regulatory compliance labeling are driving the use of narrow-web printing for artisanal product packaging. These regulations have spurred innovations that offer a 20% reduction in material waste.

Furthermore, direct-to-shape printing and digital embossing capabilities are enabling brand protection features and anti-counterfeiting solutions, which are vital for pharmaceutical and high-value goods. Integration of serialized security labels has improved supply chain traceability by over 95% in regulated industries.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the digital printing for packaging market increasingly revolves around a careful analysis of the cost of digital vs. analog printing, with many firms discovering that the benefits of variable data printing for targeted marketing campaigns outweigh the higher per-unit cost on long runs.

- The conversation is shifting toward the long-term ROI on industrial digital presses, which is heavily influenced by factors like integrating digital printing into existing workflows and the efficiency gained from automating prepress for digital packaging.

- Key applications showcase this evolution; for example, implementing serialization in pharmaceutical packaging is no longer optional, and high-speed inkjet for corrugated board is essential for optimizing the unboxing experience with digital print for direct-to-consumer brands. In parallel, the development of sustainable digital printing ink formulations is addressing digital printing for food packaging safety.

- Converters are focused on improving color consistency across substrates, particularly when tackling the challenges of digital printing on metallic foils. For flexible packaging, the debate between UV-curable vs. water-based inkjet inks continues, while digital printing for short-run flexible packaging becomes standard.

- Furthermore, right-size packaging automation with digital printing is reducing waste with on-demand packaging, and digital printing for personalized cosmetic boxes now incorporates advanced security features in digital packaging printing, a value-add that shows a higher return on investment compared to traditional decoration methods.

What are the key market drivers leading to the rise in the adoption of Digital Printing For Packaging Industry?

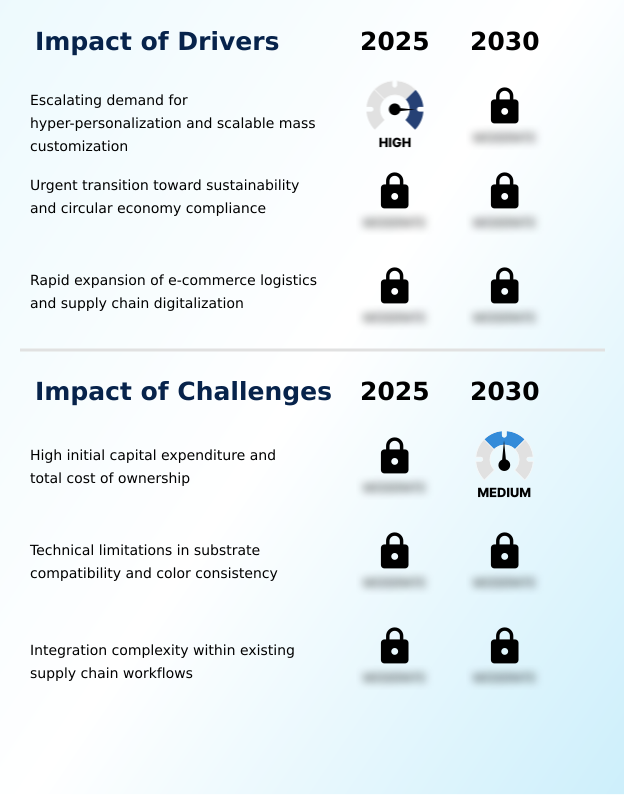

- The escalating demand for hyper-personalization and scalable mass customization is a primary driver fueling market growth.

- Market drivers are fundamentally tied to improving supply chain agility and achieving significant time-to-market reduction.

- The adoption of hybrid printing systems and digital finishing tools facilitates this by enabling on-demand printing and short-run production for applications like folding carton production and flexible packaging printing.

- Key technologies, including smart packaging integration and prepress automation, allow for efficient inventory management optimization, with some converters achieving a 30% decrease in obsolete stock.

- The demand for enhanced brand protection features has also accelerated the use of food-safe digital inks. These advancements are crucial for just-in-time manufacturing and supporting the intricate demands of label printing technology.

- Consequently, firms are realizing over a 20% improvement in production flexibility.

What are the market trends shaping the Digital Printing For Packaging Industry?

- The proliferation of personalized consumer engagement models is increasingly reliant on variable data printing strategies. This trend enables brands to deliver highly customized packaging at scale.

- Key market trends are centered on delivering personalized packaging through advanced digital press technology. The use of piezoelectric printheads and UV-curable inks is enabling custom packaging solutions with vibrant graphics and unique finishes. This shift supports variable data printing, allowing for mass customization in e-commerce packaging design and sustainable packaging printing.

- The electrophotography process, combined with precise color management software, ensures high-quality output for luxury goods packaging. Adoption of these technologies has improved time-to-market by up to 50% for short-run campaigns. Furthermore, the single-pass inkjet method is transforming corrugated box printing, with businesses reporting a 40% reduction in waste compared to conventional litho-lamination processes for comparable run lengths.

What challenges does the Digital Printing For Packaging Industry face during its growth?

- The high initial capital expenditure and total cost of ownership present a significant challenge to market adoption.

- Key challenges involve managing the complexities of new materials and ensuring circular economy compliance. While mono-material substrates and eco-labeling standards are key for sustainable goals, they demand advanced ink chemistries to ensure durability. The integration of GS1 Digital Link and digital watermarking for traceability adds a layer of technical difficulty.

- Additionally, the need for right-size packaging and automated sorting codes requires seamless automated workflow integration, which legacy systems often lack. This transition can lead to initial production slowdowns of up to 15%. Overcoming these issues is essential for consumer engagement strategies and meeting regulatory compliance labeling for promotional packaging.

- The high cost of specialized food-safe digital inks and eco-friendly printing inks also remains a barrier for smaller enterprises.

Exclusive Technavio Analysis on Customer Landscape

The digital printing for packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the digital printing for packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Digital Printing For Packaging Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, digital printing for packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Bobst Group SA - Provides advanced digital and hybrid systems for high-performance label and packaging production, integrating precision engineering with workflow automation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bobst Group SA

- Brother Industries Ltd.

- Canon Inc.

- Durst Group AG

- FUJIFILM Holdings Corp.

- Heidelberger Druckmaschinen AG

- HP Inc.

- Konica Minolta Inc.

- Kornit Digital Ltd.

- Kyocera Corp.

- Landa Corp. Ltd.

- Mark Andy Inc.

- Mimaki Engineering Co. Ltd.

- Ricoh Co. Ltd.

- Roland DG Corp.

- Screen Holdings Co. Ltd.

- Sharp Corp.

- Xeikon

- Xerox Holdings Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Digital printing for packaging market

- In October 2024, a leading digital press manufacturer announced the commercial launch of its new industrial-scale inkjet platform, specifically engineered for high-speed, single-pass printing on corrugated substrates, targeting the e-commerce packaging sector.

- In December 2024, a major packaging converter completed its acquisition of a specialized flexible packaging firm, a strategic move aimed at integrating advanced digital printing technologies and securing expertise in food-grade, sustainable packaging.

- In February 2025, a strategic partnership was formed between a top software provider and a digital press OEM to co-develop an AI-driven workflow automation suite designed to optimize prepress operations and reduce job setup times by up to 40% for digital packaging.

- In April 2025, following the finalization of new environmental regulations in Europe, a consortium of ink manufacturers unveiled a new line of certified compostable, low-migration UV inks, developed to meet circular economy standards for food and pharmaceutical packaging.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Digital Printing For Packaging Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.1% |

| Market growth 2026-2030 | USD 17904.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.3% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, South Africa, Saudi Arabia, UAE, Turkey and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The digital printing for packaging market is characterized by a decisive shift toward highly automated and data-driven production environments. Key technologies such as piezoelectric printheads and single-pass inkjet systems are enabling unprecedented speeds and precision. This technological maturation, marked by enhanced printhead longevity, nozzle density, and drop placement accuracy, allows for the widespread adoption of on-demand printing and short-run production.

- Boardroom decisions are now heavily influenced by the capabilities of digital press technology to facilitate variable data printing, which is crucial for personalization. The integration of color management software, prepress automation, and digital finishing tools into hybrid printing systems is becoming standard. These systems must handle diverse materials, requiring exceptional substrate compatibility and advanced pigment ink formulations.

- The move toward sustainable practices is driving demand for food-safe digital inks with low VOC emissions, suitable for mono-material substrates. For supply chain security, smart packaging integration with features like GS1 Digital Link, automated sorting codes, digital watermarking, and serialized security labels is critical.

- The market's evolution is further defined by advanced processes like electrophotography, liquid electrophotography, and toner-based systems, enabling applications from narrow-web printing to direct-to-shape printing and digital embossing with laser cutting integration for functional labeling. Firms leveraging automated color management report a 30% reduction in calibration time.

What are the Key Data Covered in this Digital Printing For Packaging Market Research and Growth Report?

-

What is the expected growth of the Digital Printing For Packaging Market between 2026 and 2030?

-

USD 17.90 billion, at a CAGR of 10.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (Inkjet printing, and Electrophotography printing), Type (Labels, Flexible packaging, Corrugated and folding cartons, and Others), End-user (Food and beverages, Pharmaceutical, Personal care and cosmetics, Retail, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating demand for hyper-personalization and scalable mass customization , High initial capital expenditure and total cost of ownership

-

-

Who are the major players in the Digital Printing For Packaging Market?

-

Bobst Group SA, Brother Industries Ltd., Canon Inc., Durst Group AG, FUJIFILM Holdings Corp., Heidelberger Druckmaschinen AG, HP Inc., Konica Minolta Inc., Kornit Digital Ltd., Kyocera Corp., Landa Corp. Ltd., Mark Andy Inc., Mimaki Engineering Co. Ltd., Ricoh Co. Ltd., Roland DG Corp., Screen Holdings Co. Ltd., Sharp Corp., Xeikon and Xerox Holdings Corp.

-

Market Research Insights

- Market dynamics are increasingly shaped by the pursuit of enhanced consumer engagement strategies, where custom packaging solutions are paramount. The adoption of data-driven packaging has demonstrated a 25% uplift in brand interaction metrics compared to static designs. This shift toward direct-to-consumer packaging is facilitated by just-in-time manufacturing, which reduces inventory holding costs by over 30%.

- Furthermore, inventory management optimization is achieved through small-batch production, allowing brands to respond to market changes with greater supply chain agility. Artisanal product packaging and craft beverage labels leverage these capabilities to compete with larger brands by offering premium branding and unique unboxing experience enhancement without requiring large-scale production runs.

We can help! Our analysts can customize this digital printing for packaging market research report to meet your requirements.

RIA -

RIA -