Portable Ultrasound Bladder Scanners Market Size 2024-2028

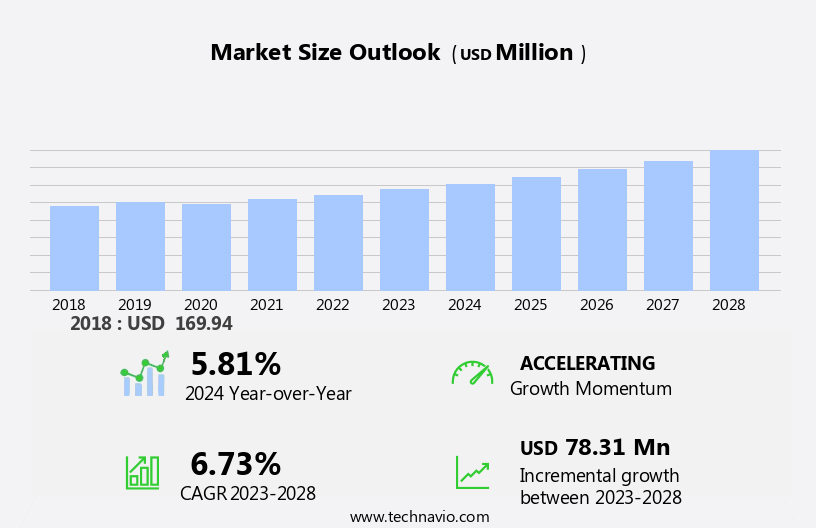

The portable ultrasound bladder scanners market size is forecast to increase by USD 78.31 million, at a CAGR of 6.73% between 2023 and 2028.

- The market is witnessing significant growth due to the rising prevalence of urological disorders, such as urinary tract infections, urethral trauma, and bladder volume measurement requirements in urological conditions. Additionally, the convenience and affordability of portable ultrasound devices compared to traditional ultrasound systems make them an attractive option for healthcare providers.

- Furthermore, the increasing online presence of these devices allows for easy access and purchase. However, the high costs associated with these devices may limit their adoption in certain settings. The market is expected to continue growing as technology advances, with features such as adjustable monitors and touch interfaces becoming more common. Incorporating these trends into business strategies will be essential for companies looking to succeed in this market.

What will be the Size of the Portable Ultrasound Bladder Scanners Market During the Forecast Period?

- The market is witnessing significant growth due to the increasing demand for non-invasive diagnostic tools in urology. These scanners play a crucial role in assessing bladder volume and detecting various urological conditions such as urinary incontinence, urinary tract infection, urethral trauma, and bladder cancer. Urological disorders affect millions of individuals in North America, leading to a high demand for point-of-care testing solutions. Portable ultrasound machines, equipped with advanced ultrasound probes and transducers, offer healthcare professionals the ability to perform bladder volume assessments quickly and accurately at the bedside or in an outpatient setting.

- Decentralized healthcare delivery is gaining popularity, and bladder scanners are becoming an essential component of diagnostic services in hospitals and clinics. These devices enable healthcare professionals to diagnose and monitor urological conditions without the need for invasive procedures, such as urinary catheters. The medical device industry continues to innovate, with portable ultrasound scanners featuring adjustable monitors, touch interfaces, and advanced imaging capabilities. These features enhance the user experience and improve diagnostic accuracy, making them indispensable tools for urologists and other healthcare professionals. Prostate enlargement is a common urological condition, and portable ultrasound bladder scanners play a significant role in diagnosing and monitoring its progression.

How is this Portable Ultrasound Bladder Scanners Industry segmented and which is the largest segment?

The portable ultrasound bladder scanners industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

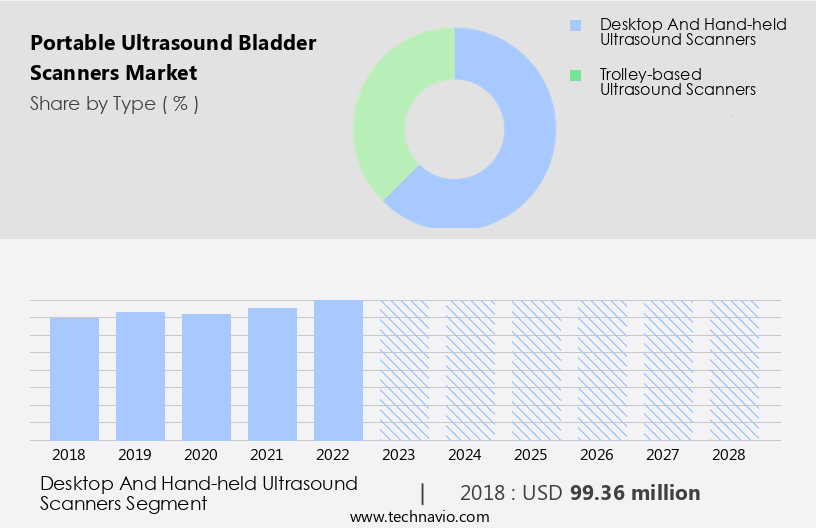

- Type

- Desktop and hand-held ultrasound scanners

- Trolley-based ultrasound scanners

- End-user

- Hospitals

- Diagnostic centers

- Others

- Geography

- North America

- US

- Asia

- China

- Japan

- Europe

- Germany

- UK

- Rest of World (ROW)

- North America

By Type Insights

- The desktop and hand-held ultrasound scanners segment is estimated to witness significant growth during the forecast period.

Portable ultrasound bladder scanners refer to compact, lightweight devices that utilize transducers and connect to compatible Android devices, such as desktops, laptops, and smartphones, via USB cable. These scanners' mobility enables physicians to conduct examinations anywhere within hospitals and healthcare settings. Ultrasound technology has seen significant advancements, leading to the miniaturization of machines into tablet and small desktop-sized devices. These hand-held ultrasound devices enhance diagnostic accuracy, complementing standard physical examinations for improved disease management. companies are investing in technology to produce cost-effective, solutions. Bladder cancer and chronic kidney disease are conditions that greatly benefit from the use of scanners in diagnostic centers, clinics, and hospitals.

These devices' accessibility and ease of use contribute to timely and accurate diagnoses, essential for effective treatment plans. Incorporating artificial intelligence into ultrasound technology further enhances diagnostic capabilities, enabling faster and more precise evaluations. Hand-held ultrasound scanners are essential tools for healthcare professionals, providing them with the ability to perform examinations on-the-go, ultimately improving patient care and outcomes. The market for these devices is growing, with several key players investing in research and development to offer advanced features and functionalities. As the demand for portable diagnostic solutions increases, the market for hand-held ultrasound scanners is expected to expand significantly.

Get a glance at the Portable Ultrasound Bladder Scanners Industry report of share of various segments Request Free Sample

The desktop and hand-held ultrasound scanners segment was valued at USD 99.36 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

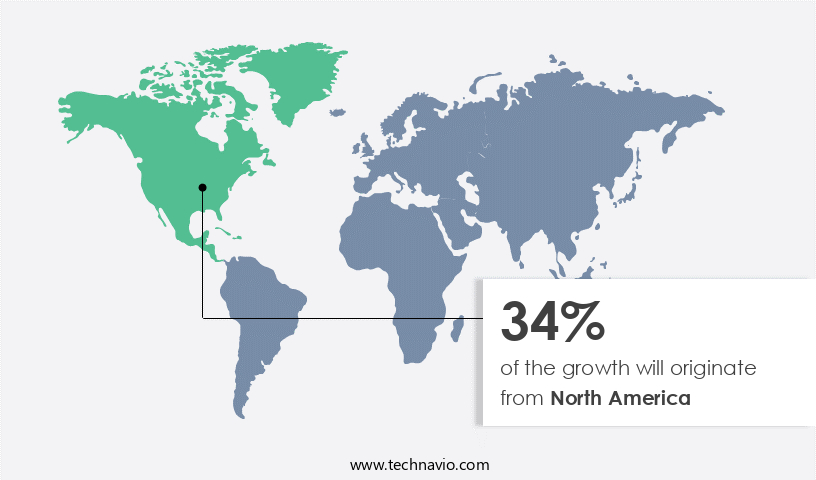

- North America is estimated to contribute 34% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

Portable ultrasound bladder scanners have gained significant attention In the healthcare industry due to their ability to diagnose various urological disorders, including urinary incontinence, non-invasively. These scanners offer point-of-care testing, making decentralized healthcare delivery more accessible. Bladder volume assessment is a common application of these devices, which is crucial for managing conditions such as prostate enlargement and kidney stones. These machines enable healthcare professionals to assess patients in real-time, enhancing diagnostic accuracy and improving patient care. These devices are essential tools for urologists and radiologists, offering a non-invasive alternative to traditional diagnostic methods.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Portable Ultrasound Bladder Scanners Industry?

The increasing prevalence of urological disorders is the key driver of the market.

- Portable ultrasound bladder scanners have gained significant attention in the medical devices industry due to their effectiveness in diagnosing and monitoring urological disorders, particularly urinary incontinence. The rising prevalence of this condition, which affects approximately 29% of women worldwide according to the National Institutes of Health, necessitates the use of advanced diagnostic tools like portable ultrasound bladder scanners.

- These scanners offer several advantages over traditional imaging methods such as MRI and CT scans, including portability, ease of use, and real-time imaging. Furthermore, the integration of multimodal imaging and emerging technologies like AI and robotics In these devices enhances their diagnostic capabilities, enabling healthcare providers to deliver superior patient care. The market for bladder scanners is poised for steady growth during the forecast period, driven by the increasing demand for non-invasive and cost-effective diagnostic solutions.

What are the market trends shaping the Portable Ultrasound Bladder Scanners Industry?

Increased online presence of portable ultrasonic bladder scanners is the upcoming market trend.

- Portable ultrasonic bladder scanners are essential medical devices used to assess bladder volume and diagnose various urological conditions, including urinary catheters, urinary tract infections, urethral trauma, and urological diseases. These devices offer healthcare professionals an adjustable monitor with a touch interface for ease of use. Manufacturers and distributors of these medical devices provide detailed product information on their e-commerce websites, enabling customers to compare specifications, read reviews, and make purchases online.

- Major online platforms, such as Amazon, eBay, and Alibaba, offer a wide selection of portable ultrasonic bladder scanners from various brands and sellers. Healthcare institutions and professionals can also purchase these devices from specialized medical equipment retailers and online marketplaces catering to their needs. Online transactions ensure secure and convenient purchasing options.

What challenges does the Portable Ultrasound Bladder Scanners Industry face during its growth?

High costs associated with ultrasound systems is a key challenge affecting the industry growth.

- Portable ultrasound bladder scanners are essential diagnostic tools In the healthcare industry, particularly for managing chronic diseases and promoting preventive healthcare. These ultrasonic diagnostic devices employ 3D technology to provide accurate and detailed images of the urinary bladder, enabling timely detection and treatment of various conditions.

- However, the upfront cost of acquiring these devices can be a significant investment for smaller healthcare providers, including clinics, outpatient centers, and home healthcare services. The expense includes the purchase price of the device, as well as necessary accessories and training. The high cost of ultrasound systems and related procedures is a primary challenge for the growth of the market. This can lead to increased patient costs, which may include the cost of the scanner, physician consultation fees, and additional diagnostic tests.

Exclusive Customer Landscape

The portable ultrasound bladder scanners market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the portable ultrasound bladder scanners market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, portable ultrasound bladder scanners market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AvantSonic Technology Co. Ltd

- Becton Dickinson and Company

- Butterfly Network Inc.

- dBMEDx Inc

- Direct Supply Inc.

- Echo Son SA

- EchoNous Inc.

- FUJIFILM Holdings Corp.

- General Electric Co.

- Infinium Medical Inc.

- Interson Corp

- Konica Minolta Inc.

- Koninklijke Philips N.V.

- Mindray Bio medical Electronics Co. Ltd.

- Sonoscanner SARL

- Sonostar Technologies Co. Ltd.

- SRS Medical

- Terason

- Vitacon

- Clarius Mobile Health Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Portable ultrasound bladder scanners have gained significant attention In the medical community due to their role as non-invasive diagnostic tools for various urological conditions. These scanners are essential in point-of-care testing, enabling decentralized healthcare delivery and improving patient care. Bladder volume assessment is a crucial application of portable ultrasound machines, aiding In the diagnosis of urinary incontinence, urinary retention, and other urological disorders. These devices are compact and easy to use, making them ideal for hospitals, diagnostic centers, and clinics. They provide real-time imaging using sound waves emitted by an ultrasound probe or transducer and received by a computer.

Further, the adjustable monitor with a touch interface allows sonographers to easily assess bladder volumes, detecting conditions such as prostate enlargement, kidney stones, bladder cancer, chronic kidney disease, and urinary tract infections. Portable ultrasound scanners offer advantages over invasive procedures like urine volume measurement and urinary catheterization. They are also more comfortable for patients, contributing to increased patient satisfaction. Furthermore, advancements in technology, such as 3D technology and artificial intelligence (AI), enhance the diagnostic capabilities of these devices, making them valuable investments for healthcare providers.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

158 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.73% |

|

Market Growth 2024-2028 |

USD 78.31 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.81 |

|

Key countries |

US, Germany, UK, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Portable Ultrasound Bladder Scanners Market Research and Growth Report?

- CAGR of the Portable Ultrasound Bladder Scanners industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Asia, Europe, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the portable ultrasound bladder scanners market growth of industry companies

We can help! Our analysts can customize this portable ultrasound bladder scanners market research report to meet your requirements.

RIA -

RIA -