Rear Spoiler Market Size 2024-2028

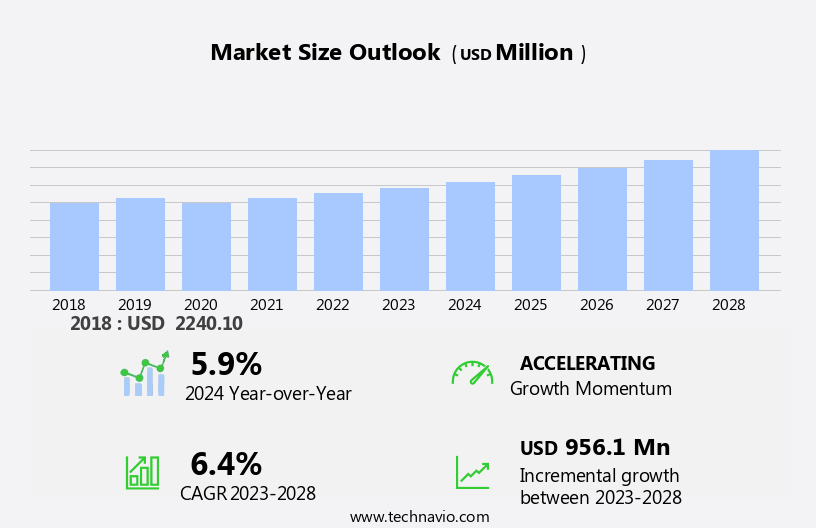

The rear spoiler market size is forecast to increase by USD 956.1 million at a CAGR of 6.4% between 2023 and 2028.

- The market has witnessed significant growth due to the increasing popularity of sports and luxury vehicles. The demand for lightweight rear spoilers, integrated into the design of common passenger vehicles, is a key trend driving market growth. Manufacturers like Plastic Omnium and SMP Automotive are leading the way in producing high-quality rear spoilers using advanced blow molding techniques for OEMs, including General Motors and other major automakers.

- Additionally, the use of raw materials, such as plastic, in rear spoiler production contributes to the reduction of vehicle weight, enhancing fuel efficiency and overall performance. This is particularly relevant to SUVs, Sport Utility Vehicles, Multi Utility Vehicles, and hatchbacks, where aerodynamic efficiency is increasingly important for fuel economy and overall vehicle performance. This market analysis report provides a comprehensive outlook on the growth factors, challenges, and future prospects of the market in the global vehicle production industry.

What will be the Size of the Market During the Forecast Period?

- The market represents a significant segment within the automotive industry, characterized by its wing-like design and functional benefits. Rear spoilers are essential components added to the rear end of vehicles to manipulate air movement and enhance vehicle performance. The primary functions of rear spoilers include increasing traction, reducing lift, and improving overall vehicle dynamics. These benefits are achieved through the application of various materials such as lightweight plastics, including abs plastic, fiberglass, silicon, and carbon fiber. The choice of material depends on factors like plasticity, shelf life, and cost. In the manufacturing process, raw materials are transformed into rear spoilers using techniques like blow molding, injection molding, and reaction injection molding.

- Additionally, these processes ensure the production of high-quality, precision-engineered components that meet the stringent requirements of original equipment manufacturers (OEMs) such as Plastic Omnium and SMP Automotive. Rear spoilers play a crucial role in vehicle aesthetics, providing an attractive and sleek appearance. They are increasingly being adopted by automakers to cater to the growing demand for fuel efficiency and emissions reduction.

- Furthermore, the motorsports industry has long recognized the benefits of rear spoilers in enhancing vehicle performance and visual appeal. The aftermarket for rear spoilers is also a thriving segment, with numerous consumers opting for customized designs to personalize their vehicles. The versatility of rear spoilers allows for various designs, catering to diverse preferences and vehicle types. In conclusion, the market continues to be an essential component of the automotive industry, driven by the demand for improved vehicle performance, fuel efficiency, and aesthetic appeal. The ongoing advancements in material science and manufacturing techniques ensure the continuous evolution of rear spoilers, making them an indispensable part of the automotive landscape.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

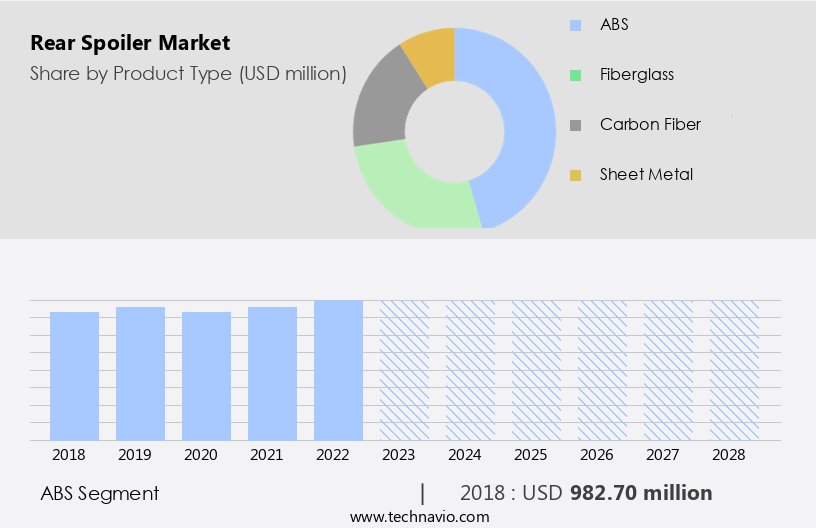

- Product Type

- ABS

- Fiberglass

- Carbon fiber

- Sheet metal

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Europe

- Germany

- South America

- Middle East and Africa

- APAC

By Product Type Insights

- The abs segment is estimated to witness significant growth during the forecast period.

Acrylonitrile Butadiene Styrene (ABS) is a widely used opaque thermoplastic and amorphous polymer. This polymer is primarily produced through the emulsion process, although a less common method known as continuous mass polymerization is also employed. ABS is renowned for its resistance to corrosive chemicals and physical impacts, making it an ideal material for various applications. ABS is highly valued for its ease of moldability and relatively low melting temperature, which simplifies its use in manufacturing processes such as injection molding and 3D printing via Fused Filament Fabrication (FDM) machines. Its structural strength is another key attribute, making it a preferred choice for various applications including rear spoilers, camera housings, protective housings, and packaging.

Additionally, ABS is a cost-effective, strong, and stiff plastic that performs well under external impacts. Its popularity is due in part to its versatility and the wide range of applications it can serve. In the automotive industry, ABS is frequently used in the production of hybrid vehicles, hatchbacks, SUVs, MPVs, and other types of vehicles to enhance their aesthetics while improving fuel efficiency and emissions reduction. Its use in motorsports is also common, as the material's strength and durability make it a valuable asset in high-performance environments. In the aftermarket sector, ABS is a popular choice for vehicle customization, particularly for the production of rear spoilers and other aerodynamic enhancements. Its ability to withstand external impacts and its resistance to chemicals make it a preferred material for these applications. Overall, ABS is a valuable polymer with a wide range of applications and benefits that make it a top choice for various industries and applications.

Get a glance at the market report of share of various segments Request Free Sample

The ABS segment was valued at USD 982.70 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

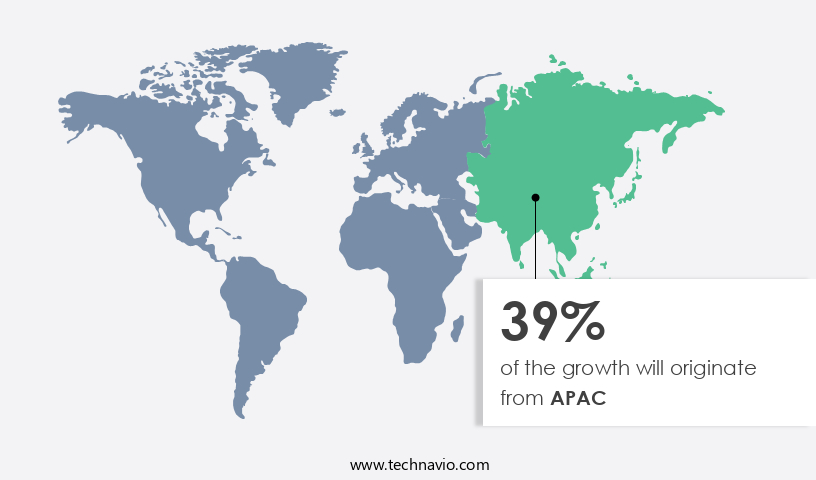

- APAC is estimated to contribute 39% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In the Asia Pacific region (APAC), China, India, South Korea, and Japan have emerged as key players in the global automotive industry, accounting for a significant portion of vehicle sales and production. The increasing demand for automobiles in these countries is expected to drive the market for rear spoilers in APAC. The region's infrastructure and industrialization developments have led to a growth in demand for Multi-Purpose Vehicles (MPVs) and Electric Vehicles (EVs). India, China, Japan, and Indonesia are projected to dominate new vehicle purchases worldwide in the coming years. The growing disposable income of people in these nations, due to improving economic conditions, is fueling this trend.

As a result, the market for rear spoilers in APAC is poised for steady growth. The market is expected to expand at a steady pace in the forecast period. In conclusion, the increasing sales of automobiles in APAC, particularly in countries like China, India, South Korea, and Japan, will create a substantial demand for rear spoilers. The region's economic growth and rising disposable income are expected to further boost this trend.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Rear Spoiler Market?

The high popularity of luxury vehicles is the key driver of the market.

- The market for automotive rear spoilers in the United States has experienced significant growth due to the increasing popularity of luxury vehicles. These vehicles, which are often equipped with advanced comfort and convenience features, offer enhanced value to consumers. One such feature that is increasingly becoming standard in luxury cars is the integrated rear spoiler. As a result, the expanding demand for luxury vehicles is propelling the growth of the market. Prominent automakers in the US market offering luxury vehicles include Audi, Daimler, BMW, and Jaguar Land Rover.

- Additionally, these companies cater to consumers seeking high-performance sedans and sports cars, many of which come with rear spoilers as standard or optional features. The rear spoiler's primary function is to manipulate air movement, creating traction and vertical force. Its wing-like design enhances the vehicle's aesthetic form while also improving its overall performance. Manufacturers use lightweight materials such as ABS plastic, fiberglass, silicon, and carbon fiber to create these spoilers, ensuring they are durable and long-lasting.

What are the market trends shaping the Rear Spoiler Market?

Rising demand for lightweight vehicles is the upcoming trend in the market.

- Rear spoilers are essential components of sports and luxury cars, contributing significantly to vehicle production. These aerodynamic accessories are manufactured using blow molding techniques, primarily from lightweight materials such as plastic. OEMs, including Plastic Omnium and SMP Automotive, are major suppliers of rear spoilers to Original Equipment Manufacturers like General Motors. Rear spoilers serve multiple purposes. Primarily, they help maintain vehicle stability at high speeds by reducing the lift force acting on the rear of the car.

- Additionally, they contribute to decreasing the car's drag, enhancing its overall performance and user experience. The lightweight nature of rear spoilers ensures that they do not add extra weight to the car, making it slightly lighter and more agile. Incorporating a rear spoiler into a car design is a strategic move to optimize its aerodynamic properties. By reducing the drag and enhancing stability, the driving experience is significantly improved, making the vehicle more responsive and enjoyable to handle.

What challenges does Rear Spoiler Market face during the growth?

Rising integrated spoilers on common passenger vehicles is a key challenge affecting the market growth.

- Rear spoilers have gained popularity in both the racing and automotive industries due to their contribution to vehicle aerodynamics. These add-ons are not exclusive to high-performance sports cars but have found their way into various passenger vehicles, including SUVs, Multi Utility Vehicles (MUVs), and hatchbacks. While these vehicles may already have a rigid chassis and suspension, rear spoilers provide additional benefits. Aerodynamics plays a crucial role in enhancing vehicle performance and safety. By reducing air drag, rear spoilers help improve fuel efficiency and stability at high speeds. Active aerodynamics, a more advanced version, adjusts the spoiler's angle based on vehicle speed for optimal airflow management.

- However, plasticity in materials used for manufacturing rear spoilers has made them cost-effective, allowing their integration into various vehicle types. The aesthetic appeal of these add-ons is an added bonus for consumers. Despite the widespread use of rear spoilers, it is essential to note that not all integrated designs offer significant aerodynamic benefits, and some may even negatively impact the vehicle's overall aerodynamics. In conclusion, rear spoilers have become a common feature in modern vehicle production, offering both functional and aesthetic benefits. While they contribute to improved vehicle performance and safety through aerodynamics, it is essential to consider their actual impact on fuel efficiency and stability when selecting a vehicle.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AISIN CORP.

- Albar Industries Inc.

- Changzhou Huawei Mold Co. Ltd.

- COMPAGNIE PLASTIC OMNIUM SE

- DAR Spoilers

- Dawn Enterprises Inc

- Dr. Ing. h.c. F. Porsche AG

- INOAC Corp.

- Magna International Inc.

- Plasman Plastics Inc.

- Polytec Holding AG

- PU Tech

- REHAU Ltd.

- Seibon International Inc.

- SMP Deutschland GmbH

- SRG Global Inc.

- Thai Rung Union Car Public Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is a significant segment in the automotive industry, focusing on the production and supply of wing-like structures installed at the rear end of vehicles. Rear spoilers are designed to manipulate air movement for improved vehicle performance and aesthetic appeal. These structures are made using various lightweight materials such as abs plastic, fiberglass, silicon, and carbon fiber, ensuring cost-effectiveness and longevity. Manufacturers employ techniques like blow molding, injection molding, and reaction injection molding to create rear spoilers for various vehicle types, including SUVs, sports utility vehicles, hatchbacks, multi-utility vehicles, and even luxury and sports cars. The use of rear spoilers in vehicle production enhances traction, reduces drag, and contributes to the overall vehicle aesthetics.

In the automotive realm, rear spoilers have gained popularity due to their role in enhancing fuel efficiency, reducing emissions, and improving vehicle dynamics. The market caters to both OEMs (original equipment manufacturers) and aftermarket buyers, with companies like Plastic Omnium and SMP Automotive leading the way in rear spoiler production. The market also extends to motorsports and performance tuning, where rear spoilers are essential for optimizing vehicle performance and visual appeal.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

138 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.4% |

|

Market growth 2024-2028 |

USD 956.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.9 |

|

Key countries |

China, US, Germany, Japan, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -