Smart City Platform Market Size 2024-2028

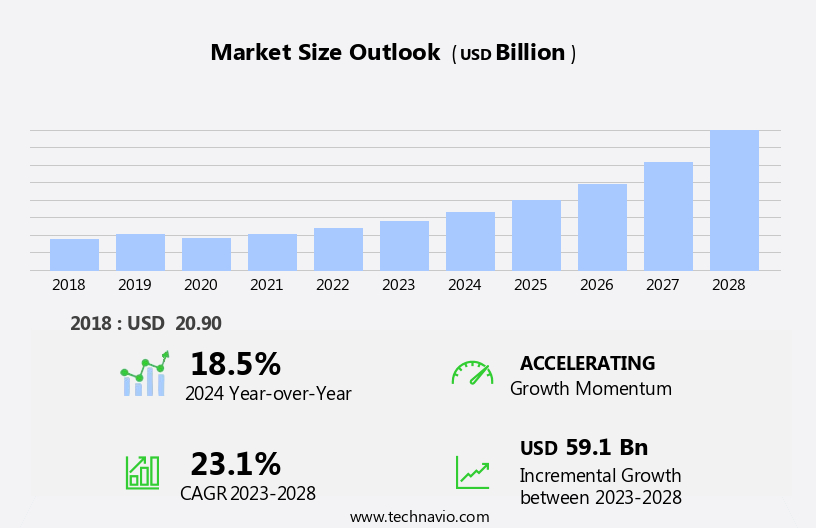

The smart city platform market size is forecast to increase by USD 59.1 billion at a CAGR of 23.1% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing demand for building automation and government initiatives aimed at developing smart cities. The need for efficient and connected urban infrastructure is driving market expansion. Security systems, powered by artificial intelligence (AI) and machine learning, are crucial for ensuring public safety and managing traffic flow. However, the market faces challenges in the form of high switching and installation costs, which may hinder the adoption of smart city platforms. These costs can be attributed to the complex nature of integrating various technologies and systems, as well as the need for specialized expertise.

- Despite this obstacle, companies can capitalize on the market's potential by focusing on cost-effective solutions and collaborating with industry partners to streamline implementation processes. By addressing these challenges, market players can effectively navigate the competitive landscape and capitalize on the opportunities presented by the growing demand for smart city technologies.

What will be the Size of the Smart City Platform Market during the forecast period?

- The market continues to evolve, driven by the integration of advanced technologies such as autonomous vehicles, smart city consortia, smart energy solutions, city planning, smart homes, Smart Lighting, real-time data, smart education, public transportation, predictive analytics, government services, open source, and artificial intelligence. renewable energy sources, traffic management, smart parking, smart metering, and smart waste management are also key components of this dynamic market. Smart city initiatives encompass city operations, smart infrastructure, smart mobility, citizen services, smart water, smart grid, electric vehicles, data analytics, smart buildings, edge computing, citizen engagement, data visualization, urban renewal, environmental monitoring, cloud computing, and smart retail.

- These technologies are transforming urban areas, improving energy efficiency, enhancing public safety, and promoting digital transformation. Open data, public-private partnerships, big data, green technology, urban planning, and urban development are essential elements of the smart city landscape. machine learning and predictive analytics enable traffic management, energy consumption optimization, and predictive maintenance of city infrastructure. Smart city awards recognize outstanding achievements in this field, fostering innovation and competition. Data privacy and security are critical concerns in the smart city context, ensuring the protection of citizens' personal information. Smart city indexes provide valuable insights into the progress and performance of various cities in implementing smart city initiatives. The ongoing unfolding of market activities and evolving patterns underscore the continuous dynamism of the market.

How is this Smart City Platform Industry segmented?

The smart city platform industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

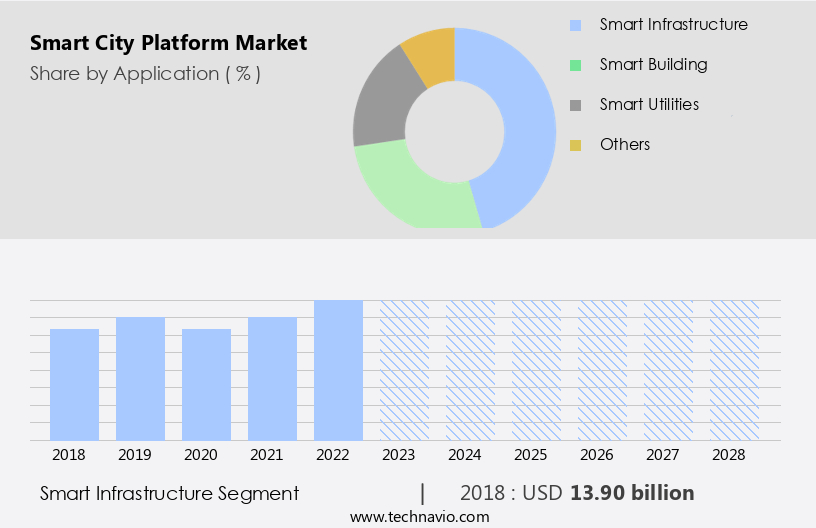

- Smart infrastructure

- Smart building

- Smart utilities

- Others

- Offering

- Connectivity management platforms

- Integration platforms

- Device management platforms

- Data management platforms

- Security platforms

- Services

- Professional services

- Managed services

- Component

- Software Platforms

- Hardware Solutions

- Services

- End-User

- Government

- Commercial Enterprises

- Residential Communities

- Geography

- North America

- US

- Canada

- South America

- Brazil

- Argentina

- Middle East and Africa

- UAE

- Europe

- Germany

- Spain

- UK

- APAC

- Japan

- Australia

- India

- Rest of World (ROW)

- North America

By Application Insights

The smart infrastructure segment is estimated to witness significant growth during the forecast period.

Smart infrastructures, encompassing energy, public transport, and public safety sectors, represent a harmonious blend of physical and digital systems. These infrastructures collect data through sensors, analyze it using artificial intelligence and machine learning, and provide real-time feedback for adaptability. The adoption of smart infrastructures is driven by the increasing industrial development, commercialization, and growing awareness of energy efficiency and building optimization. Smart cities, fueled by open data and public-private partnerships, are integrating these systems to create a more efficient and sustainable urban environment. Smart energy solutions, such as renewable energy and energy efficiency, play a crucial role in this transformation.

Smart grids and electric vehicles facilitate the integration of renewable energy sources into the power grid, while energy efficiency initiatives reduce overall consumption. Smart homes and buildings employ edge computing and data analytics to optimize energy usage and enhance occupant comfort. City planning and urban development are also benefiting from the integration of smart technologies. Predictive analytics and real-time data enable traffic management, Smart parking, and waste management, improving mobility and reducing congestion. Smart water systems ensure efficient water usage and monitoring, while smart retail and healthcare facilities leverage data visualization and citizen engagement to enhance services. Government services, including public transportation and citizen services, are being transformed through digital transformation and open data initiatives.

Smart city consortiums and initiatives are collaborating to create harmonious, immersive urban environments that prioritize energy efficiency, data privacy, and public safety. The future of smart cities lies in the seamless integration of these various systems and the continuous optimization of city operations and infrastructure.

The Smart infrastructure segment was valued at USD 13.90 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

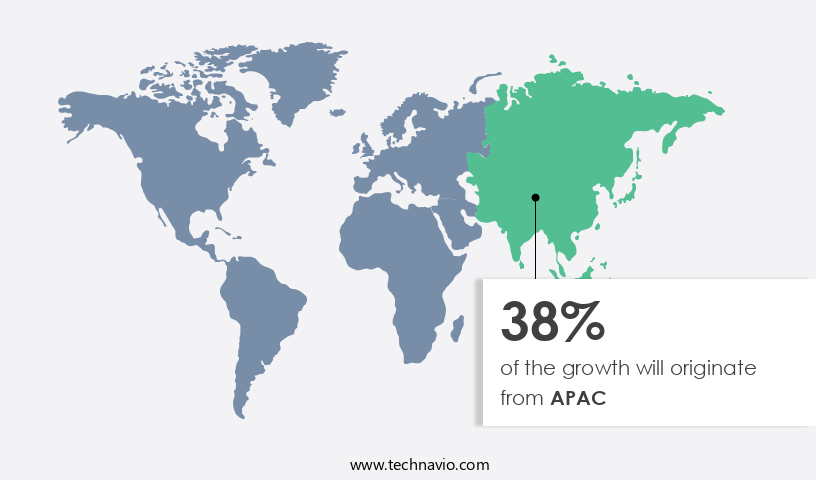

APAC is estimated to contribute 38% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the US and Canada, the market is experiencing significant growth due to increasing industrial and commercial expansion. Strict government regulations on energy conservation and the presence of numerous global companies are key drivers propelling the market forward. Major players in North America offering smart city solutions include Cisco and Microsoft, among others. With a large number of companies based in the US, competition is intensifying, leading to innovation. The US holds the largest market share, accounting for the majority of the market in the region. Smart city consortiums are collaborating to integrate various technologies such as artificial intelligence, machine learning, and predictive analytics into city planning.

Smart energy solutions are being implemented to optimize energy usage and promote renewable energy sources. Smart homes, buildings, and infrastructure are being developed to enhance citizen engagement and improve city operations. Real-time data analytics is enabling traffic management, public transportation, and smart parking systems. City services are being digitally transformed with smart water, waste management, and government services. Open data and public-private partnerships are fostering innovation in smart retail, healthcare, and education. Urban renewal projects are integrating smart technology for environmental monitoring and energy efficiency. cloud computing and edge computing are essential for managing and analyzing big data.

Smart mobility solutions, including electric vehicles and autonomous vehicles, are gaining popularity. Smart grid and smart lighting systems are being adopted to optimize energy consumption. Data privacy and public safety are crucial considerations in the digital transformation of cities. The smart city index is a measure of a city's progress towards becoming a smart city. In conclusion, the market in North America is witnessing a surge in activity, with various entities collaborating to create harmonious, efficient, and sustainable urban environments. Smart city initiatives are focusing on energy efficiency, digital transformation, and citizen services, with a strong emphasis on open data and green technology.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Smart City Platform Industry?

- The increasing demand for building automation serves as the primary market catalyst. Building Automation Software plays a crucial role in managing and optimizing the functioning of industrial, residential, and commercial buildings. This software acts as a control system to automate, regulate, and manage various subsystems in a building, ensuring adherence to predefined parameters. By integrating all components of a heating, ventilation, and air conditioning (HVAC) system into building management systems, organizations can achieve significant energy savings. Additionally, smart city initiatives, such as data analytics, citizen engagement, and environmental monitoring, are driving the adoption of building automation software. Edge computing and cloud computing technologies enable real-time data processing and analysis, leading to improved operational efficiency and enhanced user experiences.

- The integration of data visualization tools allows for better understanding and interpretation of complex data, facilitating informed decision-making. Furthermore, open data initiatives and smart retail, healthcare, urban renewal, and transportation systems are expanding the scope of building automation software applications. Overall, the market for building automation software is expected to grow as businesses continue to prioritize cost savings, energy efficiency, and advanced technologies to enhance their operations.

What are the market trends shaping the Smart City Platform Industry?

- Smart cities, driven by government initiatives, represent the current market trend. This emerging sector focuses on integrating technology into urban infrastructure and services to enhance efficiency and quality of life.

- Smart cities, fueled by public-private partnerships, are transforming urban areas into digitally connected and sustainable environments. Big data and green technology are at the core of these initiatives, enabling urban planning and development that prioritize energy efficiency and resource conservation. Governments worldwide are investing heavily in these projects to address the challenges of accommodating growth and ensuring sustainability. In this digital transformation, smart city plans focus on improving energy efficiency, waste management, and public safety. Big data analysis plays a crucial role in optimizing city services and infrastructure, enhancing the quality of life for residents. Data privacy and security are also essential considerations in these initiatives.

- Gulf and Asian countries are leading the way in smart city development, with a focus on expanding their economies and enhancing their tourism sectors. These countries' plans for smart cities prioritize energy optimization and sustainable urban development, making them attractive for businesses and investors. Through these initiatives, governments aim to provide more efficient services and greater satisfaction to their citizens, ensuring a more livable and sustainable urban environment. Smart city awards recognize and celebrate these achievements, further encouraging innovation and progress in this field.

What challenges does the Smart City Platform Industry face during its growth?

- The high switching costs and installation expenses represent significant challenges that hinder industry growth. These expenses, which include the time and resources required to transition from one solution or supplier to another, can deter businesses from adopting new technologies or services. Consequently, reducing these costs and streamlining the switching process could potentially accelerate industry expansion.

- The market encompasses various applications, including smart homes, public transportation, city planning, and energy management. companies are integrating advanced features such as predictive analytics, artificial intelligence, and real-time data to enhance the functionality of these systems. In the realm of energy management, smart grids and smart energy solutions enable efficient energy usage and demand response. However, the high initial investment required for implementing these systems, including the cost of autonomous vehicles, smart lighting, and government services, presents a significant barrier to adoption.

- The Smart City Consortium, an open-source collaborative platform, aims to address this challenge by promoting the sharing of best practices and resources among its members. The integration of smart education and open-source technology further enhances the potential of these systems to improve city infrastructure and services.

Exclusive Customer Landscape

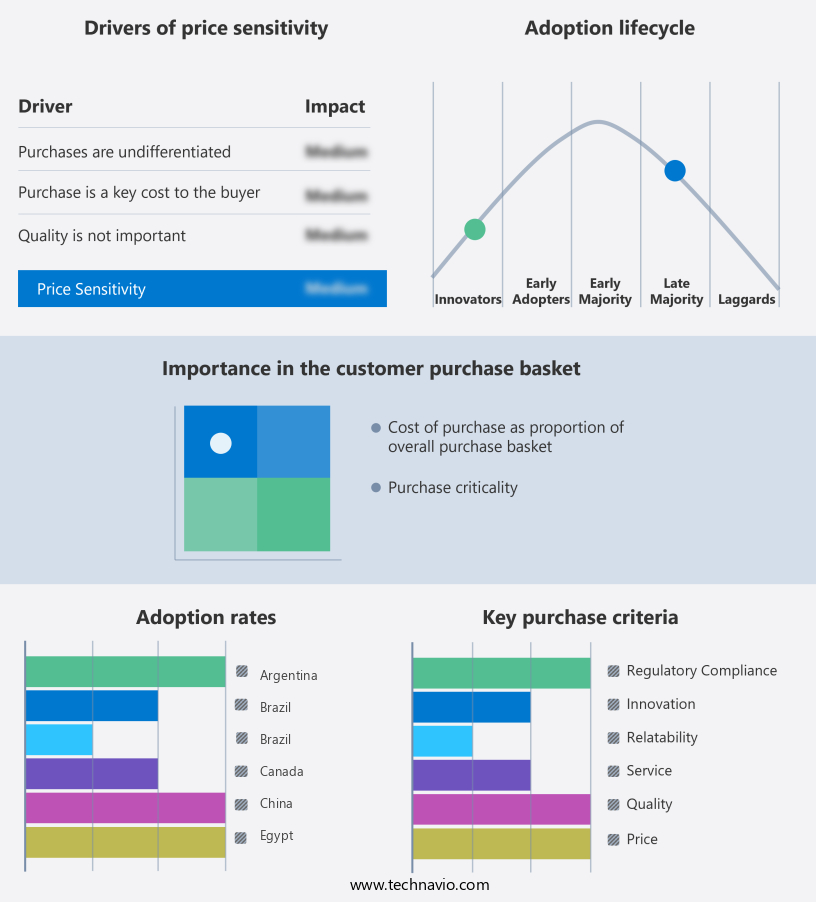

The smart city platform market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the smart city platform market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, smart city platform market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture plc - This company specializes in implementing advanced smart city platforms, such as ABB Ability Smart City Solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture plc

- Alibaba Group Holding Ltd.

- Cisco Systems Inc.

- Ericsson AB

- Fujitsu Ltd.

- General Electric Company

- Hitachi Ltd.

- Honeywell International Inc.

- Huawei Technologies Co. Ltd.

- IBM Corporation

- Intel Corporation

- Itron Inc.

- Microsoft Corporation

- Nokia Corporation

- Oracle Corporation

- SAP SE

- Schneider Electric SE

- Siemens AG

- Toshiba Corporation

- Vodafone Group plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Smart City Platform Market

- In February 2024, IBM announced the launch of its new Watson IoT for Cities platform, designed to help city administrators manage and analyze data from various smart city applications, including traffic management, public safety, and energy efficiency (IBM Press Release, 2024). This solution aims to improve urban infrastructure and enhance the quality of life for city residents.

- In June 2025, Siemens and Microsoft entered into a strategic partnership to integrate Siemens' MindSphere IoT operating system with Microsoft Azure to create a comprehensive smart city platform. This collaboration enables cities to manage their infrastructure more efficiently and effectively by combining Siemens' industrial expertise with Microsoft's cloud capabilities (Microsoft News Center, 2025).

- In October 2024, Cisco Systems invested USD1 billion in its IoT and digital transformation business, including its smart city initiatives. This significant investment demonstrates Cisco's commitment to expanding its presence in the smart city market and developing innovative solutions to address the challenges faced by urban areas (Cisco Press Release, 2024).

- In March 2025, the European Union approved the Smart Cities and Communities Mission, a â¬1.5 billion initiative aimed at creating 100 smart cities by 2030. This ambitious project will focus on energy efficiency, sustainable mobility, and digital transformation, and is expected to significantly boost the European smart city market (European Commission Press Release, 2025).

Research Analyst Overview

The smart city market is experiencing significant growth as urban areas seek to leverage technology for governance and sustainable development. Urban future lies in the implementation of smart city solutions, which integrate connected devices and real-time insights to enhance city operations and improve urban resilience. City data platforms form the backbone of this ecosystem, enabling Data Integration and operational efficiency. Smart city funding is a critical factor in deployment, with grants and investments driving innovation in urban technology trends. Urban analytics and digital cities are key components of smart city design, providing city leaders with the tools to make informed policy decisions and create a future-proof urban strategy.

Smart city regulations and architecture ensure the secure and ethical use of data, while urban technology trends focus on sustainability and innovation. The smart city ecosystem is transforming the urban landscape, with city transformation a priority for governments and businesses alike. Smart city policy and innovation are intertwined, with regulations guiding the deployment of smart city solutions and innovation driving city transformation. The future of cities lies in their ability to adapt and thrive in a digital age, with smart city design and architecture playing a crucial role in urban sustainability and resilience. City data platforms provide the foundation for real-time insights and operational efficiency, enabling city leaders to make informed decisions and improve the quality of life for urban residents.

Smart city implementation requires a holistic approach, with a focus on urban technology trends, sustainable development, and smart city regulations. Urban technology and smart city solutions are revolutionizing city services, from transportation and energy to public safety and waste management. The smart city ecosystem is a complex web of interconnected components, with city data platforms at its core. Smart city grants and investments are fueling innovation in urban technology, with a focus on improving city services and enhancing urban resilience. Smart city strategy and policy are essential for successful implementation, with a focus on data integration and operational efficiency.

Urban technology trends and smart city design are shaping the future of cities, with a focus on sustainability, resilience, and operational efficiency. Smart city architecture and urban analytics are critical components of this transformation, enabling city leaders to make informed decisions and create a smarter, more sustainable urban future.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Smart City Platform Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

148 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 23.1% |

|

Market growth 2024-2028 |

USD 59.1 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

18.5 |

|

Key countries |

US, Japan, UK, Germany, and Spain |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Smart City Platform Market Research and Growth Report?

- CAGR of the Smart City Platform industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the smart city platform market growth of industry companies

We can help! Our analysts can customize this smart city platform market research report to meet your requirements.

RIA -

RIA -