Smart Gun Market Size 2024-2028

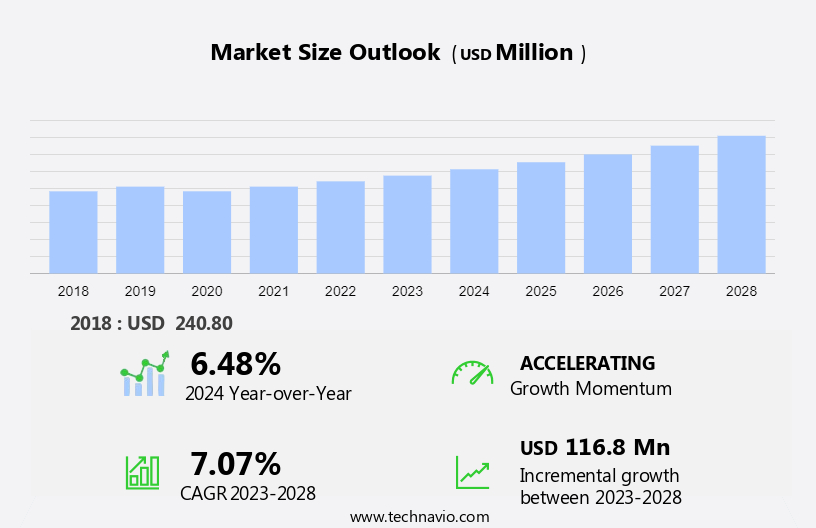

The smart gun market size is forecast to increase by USD 116.8 million, at a CAGR of 7.07% between 2023 and 2028.

- The market is experiencing significant growth due to the modernization of law enforcement capabilities. This trend is driven by the increasing demand for advanced technology to enhance public safety and security. Another key trend is the use of 3D printing technology and composite materials to manufacture smart guns. However, technical constraints remain a challenge for the market's growth. These challenges include the complexity of designing and manufacturing smart guns, as well as the need for extensive testing and certification. Despite these challenges, the market is expected to continue growing as the demand for more advanced and efficient firearms increases. Smart gun technology offers numerous benefits, including increased accuracy, improved safety features, and the potential for reduced gun-related accidents and crimes. As the market continues to evolve, it is essential for manufacturers to address these challenges and deliver innovative solutions to meet the growing demand for smart guns.

What will be the Size of the Market During the Forecast Period?

- The market encompasses a diverse range of defense systems, including computer-guided munitions and intelligent weapons, that leverage advanced technologies such as GPS, radio, infrared, laser, and satellite guidance systems for enhanced accuracy and lethality. The supply chain for these sophisticated defense systems involves a complex interplay of raw materials, logistics challenges, and various stakeholders. Defense companies and orders from governments and military organizations serve as the primary demand drivers for the market. Defense systems manufacturers and service providers play crucial roles in the production and maintenance of these advanced weapons. The operating performance of these systems hinges on the integration of various technologies, including external operating systems and safety features such as fingerprint scanners, biometric sensors, mechanical locks, and magnetic kits.

- The production of smart weapons requires a steady supply of specialized raw materials and components, which can pose logistical challenges due to their unique properties and the need for stringent quality control. The defense budget and arms transfer regulations further influence the market dynamics, with governments and military organizations prioritizing their spending on advanced defense technologies to maintain a strategic edge. The market is characterized by continuous innovation and technological advancements. Navigation satellites and cruise missiles are among the key applications of smart weapons technology, enabling precise targeting and enhanced operational capabilities. The integration of these advanced systems into defense arsenals requires a high degree of coordination and collaboration among various stakeholders, from raw material suppliers to defense organizations and service providers.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Technology

- RFID

- Biometrics

- Geography

- North America

- Canada

- US

- Europe

- Germany

- APAC

- South America

- Middle East and Africa

- North America

By Technology Insights

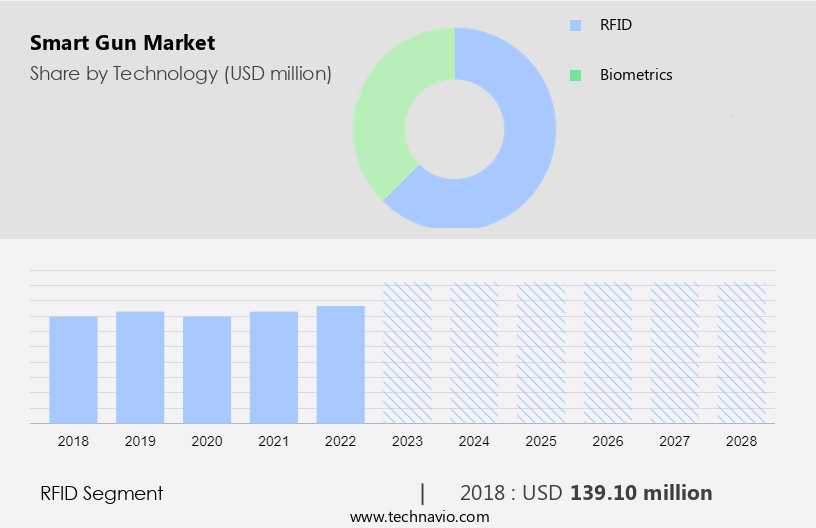

- The rfid segment is estimated to witness significant growth during the forecast period.

RFID smart guns utilize radio frequency identification (RFID) technology to ensure that only authorized users can access and fire the weapon. The gun's trigger is activated when an RFID-enabled object, such as a ring or watch, is placed within a few inches of the firearm. The gun's wireless RFID reader serves as the authentication system, comparing the radio frequency of the object and the gun. If a match is detected, the electromechanical components within the gun release the firing system, allowing the weapon to be discharged. The response time for activation depends on the specific electromechanical components used in the blocking system.

This technology offers enhanced safety and security in various applications, including law enforcement and personal use, reducing unintended shootings, suicides, and murders. RFID smart guns employ various authentication methods, such as fingerprint scanning and facial recognition systems, to ensure only the intended user can operate the firearm.

Get a glance at the market report of share of various segments Request Free Sample

The RFID segment was valued at USD 139.10 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

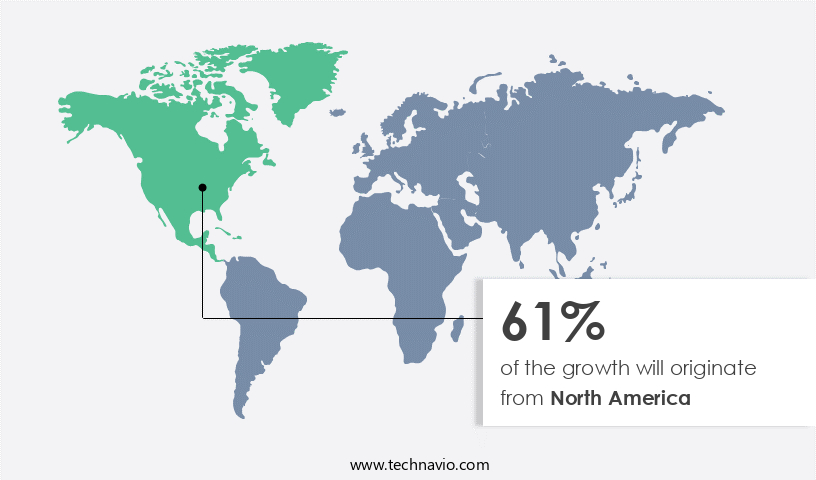

- North America is estimated to contribute 61% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The North American region, specifically the United States and Canada, dominates The market, accounting for over one-third of the total share. The demand for smart guns is driven by the need for increased gun safety and security, particularly in response to gun violence incidents. Governments in the region are investing significantly in the development of smart gun technology to minimize unauthorized use and reduce gun-related fatalities. Innovations in weapon platforms, including fingerprint scanners, biometric sensors, and mechanical locks, are key features that set North American smart guns apart. With advancements in weapon technology and modern warfare tactics, the defense budget continues to prioritize the integration of smart guns into military arsenals. The market is expected to grow steadily, driven by these factors and increasing regulatory compliance with arms transfer regulations.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of the Smart Gun Market?

Modernization of law enforcement capabilities is the key driver of the market.

- In response to the escalating concerns of gun violence, domestic disputes, organized crimes, and arms smuggling, there is a pressing demand for modernizing law enforcement capabilities. Smart weapons, equipped with advanced safety features such as fingerprint scanning, facial recognition systems, and mechanical locks, are gaining traction as a potential solution. The adoption of these intelligent weapons is being encouraged by governments to prevent misuse and collateral damage. The US defense budget for military modernization programs, including weapon technology, is on the rise. For instance, under the Assistance to States for Modernization of Police (ASMP) scheme, the Ministry of Home Affairs (MHA) is supplementing state efforts to modernize police forces with the latest defense systems and technology.

- The integration of artificial intelligence (AI), machine learning (ML), and electromagnetic (EM) waves into firearms is a significant development in this regard. Furthermore, the use of computer-guided munitions, GPS, radio, infrared, laser, and satellite guidance systems is becoming increasingly common in modern warfare tactics. The implementation of safety features like fingerprint scanners, biometric sensors, and mechanical locks is expected to reduce accidental use and misuse. The law enforcement segment is a major consumer of these smart weapons, with a significant number of orders placed by law enforcement agencies. The market for smart weapons is expected to grow, driven by increasing military spending, the need for high precision arms, and the integration of technology into defense systems.

- The use of radar, positioning systems (GPS), and platform categories, including land, maritime, and airborne, is also expanding. The market dynamics for smart weapons are influenced by factors such as defense spending, military modernization programs, and information technology services. The integration of wireless equipment, tactical radios, electronic systems, night vision devices, electronic warfare, microwave weapons, and surveillance systems is further fueling the growth of the market.

What are the market trends shaping the Smart Gun Market?

The use of 3D (3 Dimensional) printing technology and composite materials is the upcoming trend in the market.

- The Market encompasses the supply chain of advanced defense systems, including high precision arms and intelligent weapons. Raw materials and logistics challenges are critical factors in this market, as defense companies and orders from defense systems manufacturers and service providers require stringent operating performance. The integration of technology, such as fingerprint scanning, facial recognition systems, and artificial intelligence (AI) in weapons, is transforming warfare and addressing concerns of collateral damage in conflicts. In the US, military spending on modernization programs and information technology services, including wireless equipment, tactical radios, and electronic systems, is driving the demand for smart guns.

- The Law Enforcement segment, which focuses on reducing deaths, gun violence, suicides, and accidental deaths, is a significant consumer of smart guns. These weapons incorporate safety features like fingerprint sensors, biometric sensors, mechanical locks, magnetic kits, and arms transfer regulations. Advancements in technology, such as additive manufacturing (3D printing), are revolutionizing the manufacturing process for these weapons. Companies like LodeStar Works are leading the way in developing smart guns using 3D printing technology, integrating GPS, radio, infrared, laser, satellite guidance systems, and external operating systems. This technology not only enhances the lethality of weapons but also ensures safety through computer-guided munitions, radar, and positioning systems.

What challenges does the Smart Gun Market face during its growth?

Technical constraints with smart gun technology is a key challenge affecting the market growth.

- The market encompasses the supply chain of advanced defense systems, including high precision arms and smart guns. Raw material sourcing and logistics challenges are crucial factors in this industry, with defense companies and orders from defense systems manufacturers and service providers shaping market dynamics. Operating performance in warfare scenarios is a primary concern, as collateral damage and military spending influence market growth. In the law enforcement segment, gun violence remains a significant issue, with deaths from firearms including suicides, murders, and accidental deaths. Smart guns, equipped with technology such as fingerprint scanning, facial recognition systems, and electromagnetic (EM) waves, aim to reduce accidental use and misuse.

- Companies like LodeStar Works are at the forefront of this innovation, utilizing fingerprint sensors, artificial intelligence (AI), and machine learning (ML) to enhance gun safety. However, smart guns face challenges in reliability and durability, as they incorporate numerous electromechanical components. Traditional firearms, which have proven durability, are contrasted with the advanced technology of smart guns. Maintenance and repair of these advanced systems are also essential considerations, as conventional guns are often neglected in this regard. The Market is further characterized by the development of computer-guided munitions, GPS, radio, infrared, laser, satellite guidance systems, and lethality enhancement features.

- External operating systems, intelligent weapons, and modern warfare tactics, including long-range hypersonic missile systems and missiles, munitions, guided rockets, and guided projectiles, are integral to the market landscape. Defense spending and military modernization programs are significant drivers for the Market, with information technology services, wireless equipment, tactical radios, electronic systems, night vision devices, electronic warfare, microwave weapons, and surveillance systems all contributing to market growth. The land, maritime, and airborne categories are essential markets for smart weapons, with various platforms requiring advanced defense systems for protection.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Biofire Technologies Inc.

- General Dynamics Corp.

- Identilock LLC

- Lockheed Martin Corp.

- Lodestar Works Inc.

- Northrop Grumman Corp.

- O.F. Mossberg and Sons Inc.

- SimonsVoss Technologies GmbH

- Smart Gunz LLC

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a wide range of advanced defense systems designed to enhance the capabilities of traditional firearms and munitions. These intelligent weapons incorporate various technologies such as fingerprint scanning, facial recognition systems, and artificial intelligence (AI) to improve accuracy, safety, and efficiency. In this article, we will delve into the market dynamics and logistical challenges associated with the production and deployment of smart weapons. The production of smart weapons relies on a complex supply chain involving various raw materials and components. Defense companies and service providers collaborate to develop and manufacture these advanced systems. The procurement of raw materials, such as electromagnetic (EM) waves, GPS, radio, infrared, laser, and satellite guidance systems, plays a crucial role in ensuring the timely delivery of these sophisticated weapons.

The logistical challenges in the market are substantial due to the high-tech nature of these systems. The transportation, storage, and maintenance of smart weapons require specialized expertise and infrastructure. Defense systems manufacturers must adhere to strict regulations regarding arms transfer to ensure the security and safety of these advanced technologies. Defense systems manufacturers invest heavily in research and development to create intelligent weapons that can adapt to modern warfare tactics. These companies focus on improving lethality, accuracy, and safety features, such as fingerprint scanners, biometric sensors, mechanical locks, and magnetic kits. The operating performance of these weapons is critical in various land, maritime, and airborne applications.

Smart weapons have become an essential component of modern warfare, enabling high-precision arms that minimize collateral damage. These weapons are designed to reduce the risk of civilian casualties and improve the overall effectiveness of military operations. The use of computer-guided munitions, GPS, and radar systems enables accurate targeting and reduces the reliance on human intervention. The law enforcement segment of the market is also growing, with an increasing focus on reducing gun violence and improving public safety. Smart guns, which incorporate various safety features like fingerprint sensors and biometric identification systems, are gaining popularity among law enforcement agencies. These weapons aim to prevent unauthorized use, misuse, and accidental discharge, ultimately reducing the number of deaths, suicides, murders, and accidental deaths caused by firearms.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

140 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.07% |

|

Market Growth 2024-2028 |

USD 116.8 million |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

6.48 |

|

Key countries |

US, Germany, Austria, Canada, and Israel |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -