Steel Fire Sprinkler Pipes Market Size 2026-2030

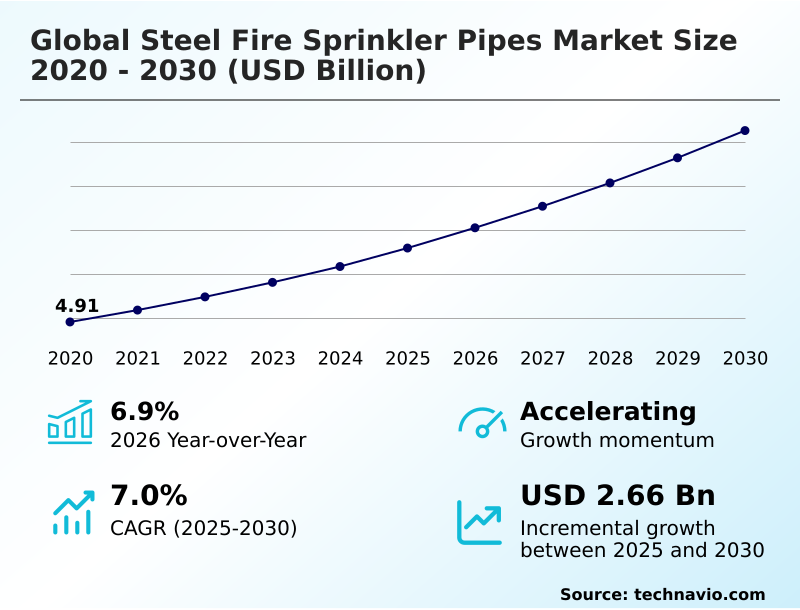

The steel fire sprinkler pipes market size is valued to increase by USD 2.66 billion, at a CAGR of 7% from 2025 to 2030. Implementation of enhanced fire safety codes will drive the steel fire sprinkler pipes market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 45.5% growth during the forecast period.

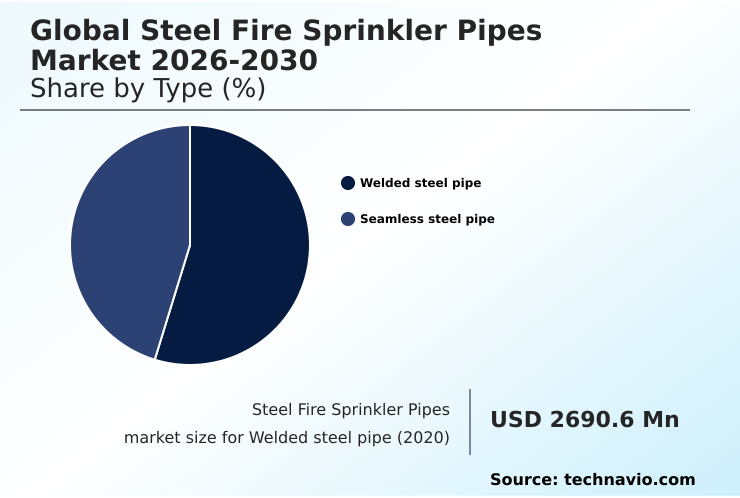

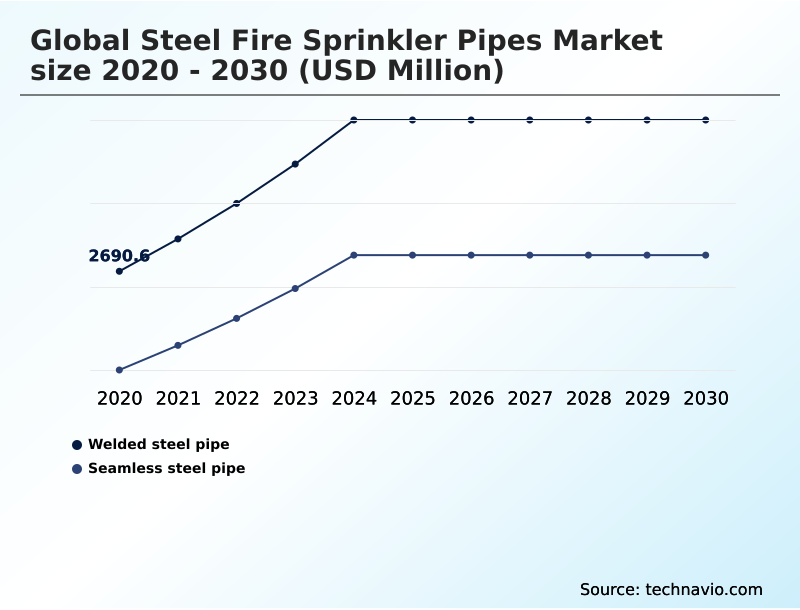

- By Type - Welded steel pipe segment was valued at USD 3.41 billion in 2024

- By End-user - Commercial segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 4.34 billion

- Market Future Opportunities: USD 2.66 billion

- CAGR from 2025 to 2030 : 7%

Market Summary

- The steel fire sprinkler pipes market is integral to modern safety infrastructure, underpinned by stringent regulations and the continuous expansion of urban and industrial construction.

- Key drivers include the mandatory enforcement of fire codes, which necessitates the use of robust materials like steel for their superior heat resistance and structural integrity in applications ranging from high-rise building risers to complex industrial facilities. A significant trend is the shift toward sustainable manufacturing, with a focus on reducing the carbon footprint of steel production.

- Simultaneously, the integration of smart technologies, such as iot-enabled pipe sensors, is transforming system maintenance from a reactive to a predictive model. However, the market grapples with challenges like raw material price volatility and competition from alternative materials in certain applications.

- For instance, a construction firm developing a commercial complex must balance the upfront cost of premium galvanized steel coating for a dry pipe fire system against the long-term maintenance savings, while ensuring strict adherence to ul certification standards and fm global approval, which is a critical operational scenario reflecting these market dynamics.

What will be the Size of the Steel Fire Sprinkler Pipes Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Steel Fire Sprinkler Pipes Market Segmented?

The steel fire sprinkler pipes industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Welded steel pipe

- Seamless steel pipe

- End-user

- Commercial

- Industrial

- Residential

- Material

- Black steel

- Galvanized steel

- Stainless and alloy steel

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Type Insights

The welded steel pipe segment is estimated to witness significant growth during the forecast period.

The welded steel pipe segment maintains a dominant market position due to its cost-effectiveness and broad applicability in standard fire protection systems. Manufacturing processes, particularly electric resistance welding (erw), are faster and less resource-intensive than those for seamless alternatives.

This makes welded pipes the preferred choice for commercial and residential buildings requiring nfpa 13 compliance without extreme pressure demands.

The uniform surface quality of this non-combustible piping material facilitates easier threading and grooved-end pipe design, with grooved mechanical couplings accelerating installation times and reducing labor costs by up to 25%.

Advancements in welding technology have enhanced the reliability of this fire suppression infrastructure, which can be further improved with epoxy pipe linings and other corrosion-resistant coatings to extend system longevity in wet pipe fire system environments.

The Welded steel pipe segment was valued at USD 3.41 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 45.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Steel Fire Sprinkler Pipes Market Demand is Rising in APAC Get Free Sample

The geographic landscape is diverse, with APAC poised to contribute approximately 45.5% of the market's incremental growth, driven by massive urbanization and industrial hazard protection requirements in new manufacturing hubs.

In this region, demand for welded steel pipe and pre-fabricated piping solutions is high.

In contrast, North America is characterized by a mature market focused on fire safety retrofitting and upgrades to existing commercial and industrial facilities, often specifying heavy-wall steel piping.

European markets prioritize sustainable steel manufacturing and adherence to environmental product declaration (epd) standards, favoring suppliers using fossil-free steel production methods.

Across all regions, the push for giga-project safety standards and the development of energy transition project safety systems are creating demand for high-performance alloy steel composition and specialized corrosion resistant technologies to ensure long-term reliability and compliance.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic planning for fire protection requires a nuanced understanding of specific application demands, influencing decisions across a spectrum of solutions. For projects involving steel pipe for high-rise buildings, engineers must consider both pressure ratings and seismic requirements for fire sprinkler pipes.

- The debate over seamless vs welded pipe for industrial use is critical in environments like chemical processing plants, where system integrity is paramount. In colder climates, specifying galvanized pipe for dry sprinkler systems is standard practice to prevent freezing-related failures.

- A major focus is on corrosion resistance in wet pipe systems, where microbiologically influenced corrosion prevention techniques are essential for extending asset life. In fact, selecting the appropriate coated steel pipe for chemical processing plants can improve system longevity by over 40% compared to a non-specialized choice.

- Modern facilities also have unique needs; esfr sprinkler system pipe requirements are vital for fire protection in automated warehouses, while steel pipe for cleanroom fire protection is specified in high-tech manufacturing, including fire safety in electric vehicle factories. The adoption of iot monitoring for fire sprinkler pipes enables predictive maintenance, a key trend for steel pipe selection for data centers.

- The push for sustainable steel pipes for green buildings is influencing procurement, while the need for retrofitting buildings with steel sprinkler pipes creates a steady secondary market. Adherence to nfpa standards for steel sprinkler pipes and sourcing astm a795 certified sprinkler pipe are non-negotiable for compliance, especially in the hospitality sector safety and for high-pressure steel pipe for deluge systems.

- Ultimately, the choice between black steel vs galvanized steel pipes comes down to a lifecycle cost analysis for each specific environment.

What are the key market drivers leading to the rise in the adoption of Steel Fire Sprinkler Pipes Industry?

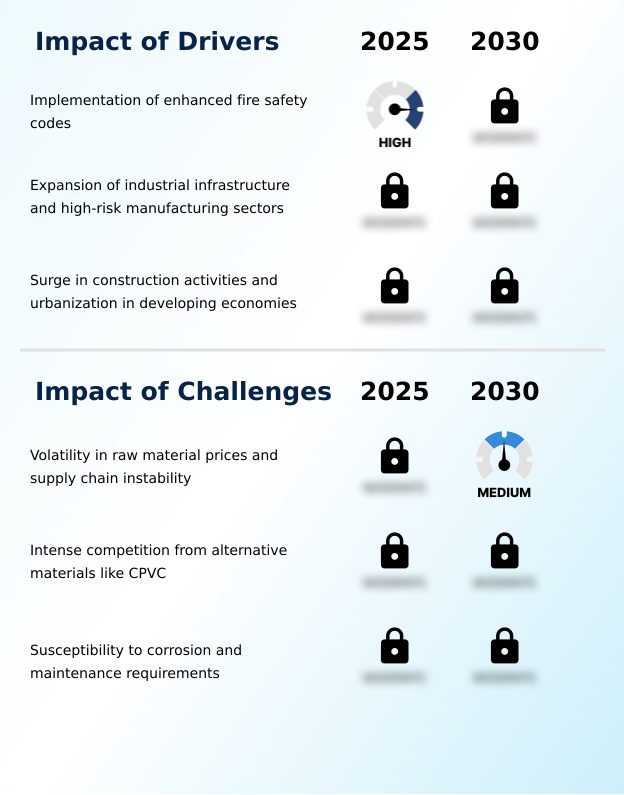

- The primary driver for the market is the widespread implementation of enhanced fire safety codes and stringent building regulations globally.

- Market growth is fundamentally driven by the stringent enforcement of building safety regulations and a global construction boom in key sectors.

- The mandatory adoption of automatic fire suppression systems in new commercial and high-rise residential buildings has created a baseline of consistent demand. Compliance with nfpa 13 standards is non-negotiable in many regions, driving sales of certified piping materials.

- The expansion of industrial infrastructure, where facilities require high-pressure capacity systems for industrial hazard protection, has increased demand for heavy-wall steel piping by over 10% in emerging industrial zones.

- Furthermore, a surge in fire safety retrofitting projects, spurred by insurance mandates and updated codes, provides a stable secondary market.

- This is particularly evident in urban infrastructure safety initiatives, where the reliability of steel as a non-combustible piping material is paramount for protecting high-density populations.

What are the market trends shaping the Steel Fire Sprinkler Pipes Industry?

- The market is increasingly shaped by the acceleration of sustainable manufacturing practices. Concurrently, the development of advanced corrosion-resistant technologies is becoming a critical focus for enhancing system longevity.

- Key market trends are converging around sustainability and digitalization, fundamentally reshaping system design and specification. The push for sustainable steel manufacturing is driving demand for materials with verifiable environmental product declaration (epd) credentials, with some projects achieving a 15% lower carbon footprint by specifying fossil-free steel production.

- Concurrently, the integration of iot-enabled pipe sensors and smart monitoring integration is enabling predictive maintenance for pipes. This shift toward digital building solutions facilitates real-time pipe wall integrity monitoring, reducing unexpected system failures by over 20%. These corrosion resistant technologies and high-purity steel piping are becoming essential for high-value assets.

- Furthermore, developments in hot-dip galvanization and advanced corrosion-resistant coatings are extending the operational life of fire suppression infrastructure, aligning with green building goals.

What challenges does the Steel Fire Sprinkler Pipes Industry face during its growth?

- A key challenge affecting industry growth is the significant volatility in raw material prices, compounded by persistent supply chain instability.

- The primary market challenges revolve around economic volatility and material science limitations. The price of core raw materials has shown fluctuations of up to 25% in a single quarter, creating significant margin pressure for manufacturers of products like stainless steel variants and those using alloy steel composition. This instability, coupled with logistical disruptions, complicates project budgeting and timelines.

- Simultaneously, the industry faces intense competition from alternative materials, particularly in the residential and light-commercial sectors, where plastic-based systems can offer lower installation costs.

- A persistent technical hurdle is the susceptibility of steel to microbiologically influenced corrosion (mic), a factor that can increase total system lifecycle costs by 15% due to the need for nitrogen inerting technology or specialized epoxy pipe linings. This vulnerability requires continuous innovation in seismic bracing for pipes and coatings to maintain a competitive edge.

Exclusive Technavio Analysis on Customer Landscape

The steel fire sprinkler pipes market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the steel fire sprinkler pipes market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Steel Fire Sprinkler Pipes Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, steel fire sprinkler pipes market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Apollo Pipes Ltd. - Key offerings include engineered steel fire sprinkler pipes and grooved fittings, designed to meet stringent fire protection application standards for robust system integration and superior performance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Apollo Pipes Ltd.

- ArcelorMittal SA

- ASC Engineered Solutions

- Atkore Inc.

- Bull Moose Tube Co.

- Engineered Fire Piping

- Hi Tech Pipes Ltd.

- InfraBuild Trading Pty Ltd.

- Johnson Controls International

- LINHUI

- Mueller Industries Inc.

- Nucor Corp.

- Southern Steel Berhad

- Tata Steel Ltd.

- Tenaris SA

- Tianjin Profound MT Co. Ltd.

- Victaulic Co.

- World Iron and Steel Co. Ltd

- Zekelman Industries

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Steel fire sprinkler pipes market

- In August 2024, a major CPVC systems manufacturer introduced a high-performance product line, increasing competition against steel pipes in light-hazard applications by offering enhanced temperature resistance.

- In October 2024, India's Ministry of Housing and Urban Affairs approved a new phase of smart city projects, creating a government mandate for automatic sprinkler systems in certain residential high-rises.

- In January 2025, a leading North American trade authority imposed new tariffs on imported steel products, directly increasing the cost of steel fire sprinkler pipes for distributors and end-users.

- In March 2025, the European Union passed a new directive within the EPBD recast, which included mandates for upgraded fire safety measures in building renovations, boosting orders for carbon steel pipes.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Steel Fire Sprinkler Pipes Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 292 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7% |

| Market growth 2026-2030 | USD 2664.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.9% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The steel fire sprinkler pipes market is evolving beyond material sales into a landscape defined by lifecycle value and regulatory compliance. A critical boardroom-level consideration is balancing capital expenditures on advanced systems against long-term operational costs.

- For example, investing in systems utilizing nitrogen inerting technology and advanced antimicrobial pipe coatings can initially increase project costs but yield significant savings by mitigating the risk of microbiologically influenced corrosion (mic), which can lead to premature system failure.

- The adoption of grooved mechanical couplings over traditional welding methods can reduce installation labor costs by up to 30%, directly impacting project profitability. The market is increasingly segmented by application-specific demands, from high-pressure seamless steel pipe for industrial hazard protection and water-foam fire systems to cost-effective welded steel pipe for standard commercial wet pipe fire systems.

- Adherence to standards like astm a795, ul certification standards, and fm global approval is paramount, driving demand for quality-assured black steel material, galvanized steel coating, and specialized epoxy pipe linings. The choice between a pre-action sprinkler system, dry pipe fire system, or deluge fire system further dictates the specification, from schedule 10 pipe specification to schedule 40 pipe specification.

What are the Key Data Covered in this Steel Fire Sprinkler Pipes Market Research and Growth Report?

-

What is the expected growth of the Steel Fire Sprinkler Pipes Market between 2026 and 2030?

-

USD 2.66 billion, at a CAGR of 7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Welded steel pipe, and Seamless steel pipe), End-user (Commercial, Industrial, and Residential), Material (Black steel, Galvanized steel, and Stainless and alloy steel ) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Implementation of enhanced fire safety codes, Volatility in raw material prices and supply chain instability

-

-

Who are the major players in the Steel Fire Sprinkler Pipes Market?

-

Apollo Pipes Ltd., ArcelorMittal SA, ASC Engineered Solutions, Atkore Inc., Bull Moose Tube Co., Engineered Fire Piping, Hi Tech Pipes Ltd., InfraBuild Trading Pty Ltd., Johnson Controls International, LINHUI, Mueller Industries Inc., Nucor Corp., Southern Steel Berhad, Tata Steel Ltd., Tenaris SA, Tianjin Profound MT Co. Ltd., Victaulic Co., World Iron and Steel Co. Ltd and Zekelman Industries

-

Market Research Insights

- The market dynamics are defined by a push for greater efficiency and safety, driven by stringent building safety regulations. The adoption of smart monitoring integration allows for predictive maintenance for pipes, which has been shown to reduce catastrophic system failures by over 20%.

- In construction, the use of off-site construction methods and pre-fabricated piping solutions accelerates project timelines significantly, with grooved mechanical couplings reducing installation labor by up to 30% compared to traditional welding. This focus on operational efficiency is critical for urban infrastructure safety, particularly in the development of super-tall structure systems and data center fire systems.

- Stakeholders are balancing the need for certified piping materials with the demand for cost-effective, rapid deployment in a competitive environment, where the choice of material directly impacts both initial investment and long-term asset protection.

We can help! Our analysts can customize this steel fire sprinkler pipes market research report to meet your requirements.

RIA -

RIA -