Storage Area Network (SAN) Market Size 2024-2028

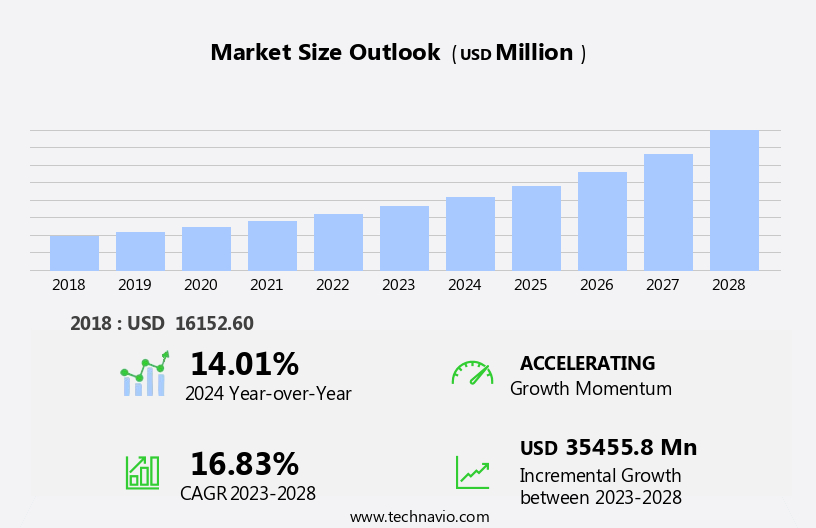

The storage area network (san) market size is forecast to increase by USD 35.46 billion, at a CAGR of 16.83% between 2023 and 2028.

- The market is experiencing significant growth, driven primarily by the increasing need for data backup and redundancy in the context of digital transformation. Businesses are increasingly adopting digital strategies, leading to an explosion of data. SAN technology offers a scalable, flexible, and high-performance solution for managing this data, making it an essential component of modern IT infrastructure. However, this market is not without challenges. Cybersecurity threats pose a significant obstacle, with SANs being a prime target due to their critical role in data management.

- Ensuring the security of SANs is a top priority for organizations, requiring significant investment in cybersecurity solutions and best practices. Additionally, the complexity of SANs can make implementation and management challenging, necessitating specialized expertise and resources. Companies seeking to capitalize on the opportunities presented by the SAN market must navigate these challenges effectively, investing in robust security measures and building a skilled workforce.

What will be the Size of the Storage Area Network (SAN) Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, with dynamic market activities unfolding across various sectors. Hybrid cloud storage solutions are increasingly adopted, integrating SAN with cloud storage for enhanced performance and flexibility. Data management remains a key focus, with de-identification, backup, and retention strategies being continually refined. Software-defined storage and data deduplication are transforming the landscape, enabling optimization of data center infrastructure. Multi-cloud storage and performance tuning are also gaining traction, allowing businesses to manage and distribute data more efficiently. Network Attached Storage (NAS) and Object Storage are complementing SAN, offering different access methods and use cases. Data compression, compression, and archiving are essential for capacity planning and cost optimization.

Security remains a top priority, with encryption, masking, and compliance measures being implemented to protect sensitive data. Disaster recovery and data governance are crucial components of a robust data management strategy. File and block level storage, as well as flash storage, offer varying benefits depending on the application. Storage analytics, auditing, and tiered storage solutions provide valuable insights for capacity planning and performance monitoring. Fibre Channel and Ethernet technologies continue to shape the market, while hyperconverged infrastructure and SAN switches offer streamlined management and consolidation. The ongoing evolution of SAN market is driven by the continuous pursuit of improved performance, cost savings, and enhanced security.

How is this Storage Area Network (SAN) Industry segmented?

The storage area network (san) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Component

- Hardware

- Software

- Services

- Technology

- Fiber channel

- Fiber channel over ethernet

- Infiniband

- iSCSI protocol

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

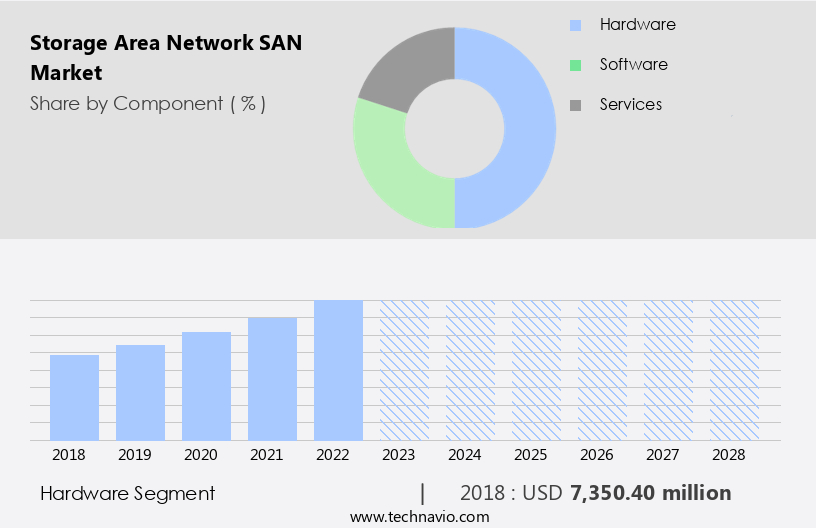

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The market encompasses hardware, software, and services that interconnect storage devices and servers. Hardware components, a crucial part of this infrastructure, consist of fiber channels and related hardware such as hubs, switches, gateways, directors, and routers. The market's growth is driven by the escalating demand for data backup and high-speed networking. Additionally, the ongoing digital transformation worldwide is anticipated to significantly boost the hardware segment's expansion. Data backup and disaster recovery are essential functions in today's business environment, necessitating the need for efficient and reliable storage solutions. Software-defined storage, data deduplication, compression, and tiered storage are some advanced technologies enhancing data backup and recovery capabilities.

Furthermore, data security, compliance, and governance are critical concerns, leading to the adoption of data encryption, masking, and access control mechanisms. Network Attached Storage (NAS) and Cloud Storage offer alternative storage architectures to SAN. Multi-cloud storage and hybrid cloud strategies are gaining traction, necessitating seamless integration and optimization of various storage systems. Performance tuning, monitoring, and analytics tools enable organizations to optimize their storage infrastructure and ensure high throughput and low latency. Capacity planning, consolidation, and cost optimization are essential aspects of managing storage infrastructure. Flash storage, solid-state drives, and storage arrays are some technologies addressing these concerns.

Data archiving, migration, and lifecycle management are also vital functions, ensuring data availability and accessibility while minimizing storage costs. In conclusion, the SAN market is dynamic and evolving, with various technologies and trends shaping its growth. The increasing adoption of advanced storage solutions, the growing importance of data security and compliance, and the ongoing digital transformation are key drivers of market expansion.

The Hardware segment was valued at USD 7.35 billion in 2018 and showed a gradual increase during the forecast period.

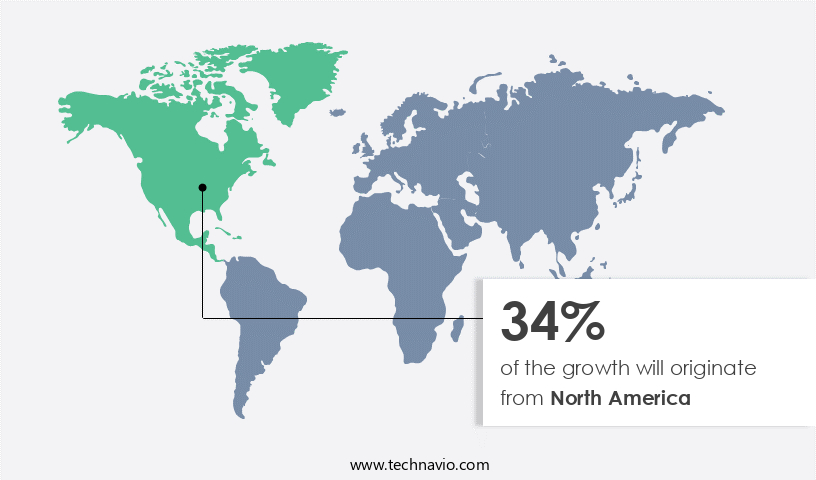

Regional Analysis

North America is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is experiencing significant growth, particularly in North America, driven by the adoption of SAN technology among small and medium-sized enterprises (SMEs). SAN offers advantages such as low power consumption and improved write speed, making it an attractive solution for businesses seeking to optimize their data infrastructure. SMEs face constant pressure to upgrade and stay competitive, and the increasing prevalence of IoT and third-platform technologies like cloud computing and analytics are compelling organizations to invest in IT solutions. SAN technology is also gaining traction in data center infrastructure due to its ability to provide high-performance, scalable storage solutions.

Multi-cloud storage and hybrid cloud storage are emerging trends, as businesses seek to leverage the benefits of both private and public cloud storage. Performance tuning and monitoring are essential for ensuring optimal storage throughput, while data security remains a top priority. Software-defined storage, data deduplication, compression, and data retention are key technologies that enable storage optimization and cost savings. Data de-identification and masking are crucial for data security and compliance with regulations such as GDPR and HIPAA. Capacity planning and disaster recovery are also critical considerations for businesses seeking to ensure business continuity. Flash storage, solid-state drives, and storage arrays are popular choices for businesses seeking high-performance storage solutions.

Tiered storage, fibre channel, and object storage are other technologies that offer different benefits depending on the specific use case. Storage analytics and auditing are essential for gaining insights into storage usage and identifying opportunities for improvement. In conclusion, the SAN market is evolving rapidly, driven by the need for high-performance, scalable, and cost-effective storage solutions. SAN technology offers numerous benefits, including improved write speed, low power consumption, and data security. The adoption of SAN is being fueled by the increasing prevalence of IoT, cloud computing, and analytics, as well as the need for data compliance and disaster recovery.

Storage optimization, cost savings, and performance tuning are key priorities for businesses seeking to maximize the value of their storage investments.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Storage Area Network (SAN) Industry?

- The surge in digital transformation has led to a heightened requirement for data backup and redundancy, serving as the primary driver for market growth in this sector.

- The SAN market is experiencing significant growth due to the increasing demand for robust data storage and backup solutions in various industries. Digital transformation has led to an escalating need for data governance, recovery, and migration, driving the adoption of SAN technology. SAN solutions, which enable block and file level storage, are particularly valuable in sectors such as healthcare, IT, telecom, and BFSI, where large volumes of data require centralized and secure storage. SAN's ability to offer tiered storage, flash storage, storage analytics, and storage auditing further enhances its appeal. Tiered storage allows organizations to manage their data based on access frequency and importance, optimizing storage utilization and reducing costs.

- Flash storage delivers high storage throughput, making it ideal for handling large, complex workloads. Storage analytics and auditing capabilities enable organizations to monitor and manage their storage infrastructure more effectively. Hyperconverged infrastructure and object storage are emerging trends in the SAN market. Hyperconvergence simplifies IT infrastructure by integrating storage, compute, and networking into a single solution. Object storage, on the other hand, offers a scalable, cost-effective, and flexible alternative to traditional file and block storage. Fibre Channel remains the dominant SAN technology due to its high performance, reliability, and scalability. However, iSCSI and NAS are gaining popularity due to their cost-effectiveness and ease of implementation.

- Overall, the SAN market is poised for growth, driven by the increasing demand for efficient, scalable, and secure data storage and management solutions.

What are the market trends shaping the Storage Area Network (SAN) Industry?

- Digital transformation is currently experiencing significant growth, making it a prominent trend in the market. This surge in digital adoption is driven by advancements in technology and the increasing demand for remote work and online services.

- Enterprises are modernizing their data centers to accommodate the increasing volumes of machine-critical workloads generated by advanced technologies such as AI, machine learning, and IoT. Software-defined solutions, including Storage Area Networks (SAN), are becoming essential to meet the high bandwidth requirements of these workloads. SAN solutions offer several advantages over Wide Area Networks (WAN), including lower latency and higher data transfer rates. The demand for SAN is expected to surge as enterprises seek to optimize their storage costs and increase storage capacity. SAN solutions enable the use of various storage technologies, including solid state drives and disk drives, to cater to different storage needs.

- Moreover, SAN offers advanced features such as storage security, data encryption, data masking, and storage virtualization to ensure data protection and privacy. Storage controllers play a crucial role in managing the SAN infrastructure, enabling efficient data transfer between servers and storage arrays. Tape storage continues to be an essential component of SAN solutions for long-term data retention and backup. However, the increasing adoption of cloud storage and object storage solutions may impact the future of tape storage in SAN environments. In conclusion, the increasing digital transformation of enterprises and the growing need for high bandwidth and data traffic are driving the demand for SAN solutions.

- SAN offers several advantages, including cost optimization, data security, and efficient data transfer, making it an essential component of modern data center infrastructure.

What challenges does the Storage Area Network (SAN) Industry face during its growth?

- Cyber security challenges represent a significant obstacle to the growth of various industries, necessitating continuous efforts to enhance protective measures and mitigate potential risks.

- In today's business landscape, enterprises face increasing challenges in safeguarding their sensitive data, particularly in industry verticals such as finance and healthcare. Strict data protection regulations, like the General Data Protection Regulation (GDPR), demand robust security measures to protect customer information. However, Storage Area Networks (SANs), a popular storage solution, come with potential security risks. In March 2023, Western Digital Corp. Experienced a network security breach, resulting in the theft of approximately ten terabytes of data, including customer information. To mitigate such risks, enterprises are turning to advanced security solutions. Hybrid cloud storage, software-defined storage, and network attached storage are gaining popularity due to their data security features.

- Additionally, data de-identification, data backup, data deduplication, data retention, and storage optimization techniques are essential for effective storage management. Cloud storage solutions offer data compression and encryption for enhanced security. Utilizing storage management software can further optimize storage performance and ensure data integrity. In conclusion, implementing these solutions can help businesses maintain data security while complying with regulatory requirements. Recent research indicates that the adoption of these advanced storage solutions is on the rise, offering enterprises a more secure and efficient way to manage their data.

Exclusive Customer Landscape

The storage area network (san) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the storage area network (san) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, storage area network (san) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arista Networks Inc. - The company specializes in implementing advanced storage area networks utilizing Arista Networks' 7500R datacenter switch. This solution enhances data accessibility and efficiency, enabling seamless integration of various data types and applications. By leveraging Arista's cutting-edge technology, businesses can ensure uninterrupted data flow, improved performance, and enhanced security. Our storage area network infrastructure offers scalability, flexibility, and reliability, empowering organizations to manage their data effectively and adapt to evolving business needs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arista Networks Inc.

- ATTO Technology Inc.

- Broadcom Inc.

- Cisco Systems Inc.

- Citrix Systems Inc.

- DataCore Software Corp.

- Dell Technologies Inc.

- Fujitsu Ltd.

- Hewlett Packard Enterprise Co.

- Hitachi Ltd.

- Infinidat Ltd.

- IntelliMagic BV

- International Business Machines Corp.

- Lenovo Group Ltd.

- Marvell Technology Inc.

- NEC Corp.

- NetApp Inc.

- Nutanix Inc.

- Oracle Corp.

- StoneFly

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Storage Area Network (SAN) Market

- In February 2024, Dell Technologies introduced their new Unity XC series of midrange all-flash and hybrid storage arrays, which include built-in SAN functionality (Dell Technologies Press Release). This expansion of their Unity product line caters to the growing demand for flexible and scalable storage solutions.

- In July 2024, IBM and Cisco Systems announced a strategic partnership to develop and sell integrated storage solutions based on IBM's FlashSystem and Cisco's UCS fabric (IBM Press Release). This collaboration aims to provide customers with a more efficient and seamless storage experience, combining IBM's storage expertise and Cisco's networking capabilities.

- In October 2024, NetApp completed the acquisition of SolidFire, a leading provider of all-flash storage systems, for approximately USD870 million (NetApp SEC Filing). This acquisition strengthens NetApp's position in the all-flash storage market and allows them to offer more diverse and advanced solutions to their customers.

- In March 2025, Hitachi Vantara launched its Virtual Storage Platform F Series, featuring advanced data management capabilities and support for both Fibre Channel and iSCSI protocols (Hitachi Vantara Press Release). This new product line addresses the evolving needs of businesses, enabling them to manage their data more effectively and efficiently.

Research Analyst Overview

- The market is witnessing significant trends and innovations, shaping the future of data storage solutions. SAN technology facilitates storage clustering, enabling organizations to consolidate multiple storage systems into a single, manageable infrastructure. Data replication ensures business continuity by synchronizing data across different locations, enhancing data availability and disaster recovery capabilities. Storage efficiency is a critical concern, with companies focusing on developing advanced protocols and data lake solutions to optimize storage utilization. Machine learning and artificial intelligence are increasingly being integrated into storage systems for automation and predictive analytics, driving storage innovation. Data center fabrics, edge computing, and high-performance computing are transforming the storage landscape, necessitating higher storage density and power consumption management.

- Data protection regulations, privacy, and sovereignty are driving the need for robust data security measures and industry standards. Storage upgrades, data analytics platforms, and data warehouse solutions are essential components of modern data management strategies. Cooling technologies and storage automation are addressing the challenges of managing growing data volumes and power consumption. The storage company landscape is competitive, with ongoing consolidation and partnerships shaping the industry. Big data storage, data synchronization, and data integrity are key considerations for businesses adopting SAN technology. Regulatory compliance, certification, and data privacy are essential aspects of implementing and maintaining a reliable and secure storage infrastructure.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Storage Area Network (SAN) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

175 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 16.83% |

|

Market growth 2024-2028 |

USD 35455.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

14.01 |

|

Key countries |

US, UK, Canada, Germany, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Storage Area Network (SAN) Market Research and Growth Report?

- CAGR of the Storage Area Network (SAN) industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the storage area network (san) market growth of industry companies

We can help! Our analysts can customize this storage area network (san) market research report to meet your requirements.

RIA -

RIA -