US Smart Education Market Size 2024-2028

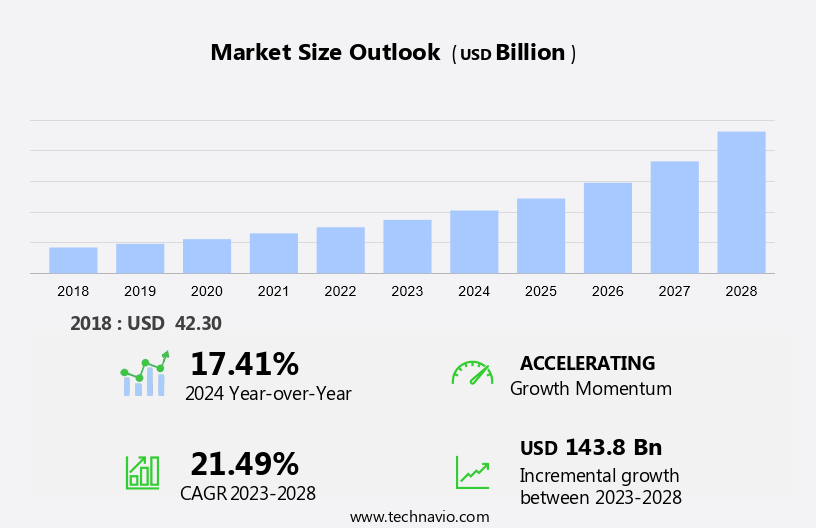

The US smart education market size is forecast to increase by USD 143.8 billion at a CAGR of 21.49% between 2023 and 2028.

- The smart education market In the US is witnessing significant growth due to the implementation of advanced technologies In the academic sector. One of the key drivers is the enhancement of the learning process through personalized and interactive approaches. Another trend is the rise of Education 4.0, which integrates technology into all aspects of education, from delivery to assessment. However, challenges persist, such as the need for adequate infrastructure and funding, data security concerns, and the digital divide that hinders equal access to technology-enabled education. Despite these challenges, the market is expected to continue growing as technology becomes increasingly integral to modern education. The implementation of AI and machine learning in education, for instance, offers immense potential for improving student outcomes and streamlining administrative tasks. In summary, the smart education market In the US is poised for growth, driven by the benefits of technology in education, while addressing the challenges to ensure equitable access and effective implementation.

What will be the size of the US Smart Education Market during the forecast period?

- The smart education market in the global arena is experiencing significant growth, with the education sector increasingly embracing technology to enhance student learning experiences. This trend is driven by various factors, including favorable government initiatives to integrate technology into classrooms and corporate fundings for advanced training programs. The market encompasses a range of software and services, including instructional software, online learning environments, interactive whiteboards, tablets, computers, and mobile educational applications.

- Moreover, emerging technologies such as artificial intelligence, machine learning, virtual reality, e-learning methods, gamification, and interactive learning techniques are revolutionizing the educational field. Corporate organizations are also investing In these technologies to develop effective training programs for their workforce. Overall, the smart education market is poised for continued expansion, offering innovative solutions to meet the evolving needs of students and educators alike.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Academics

- Corporate

- Component

- Service

- Software

- Hardware

- Geography

- US

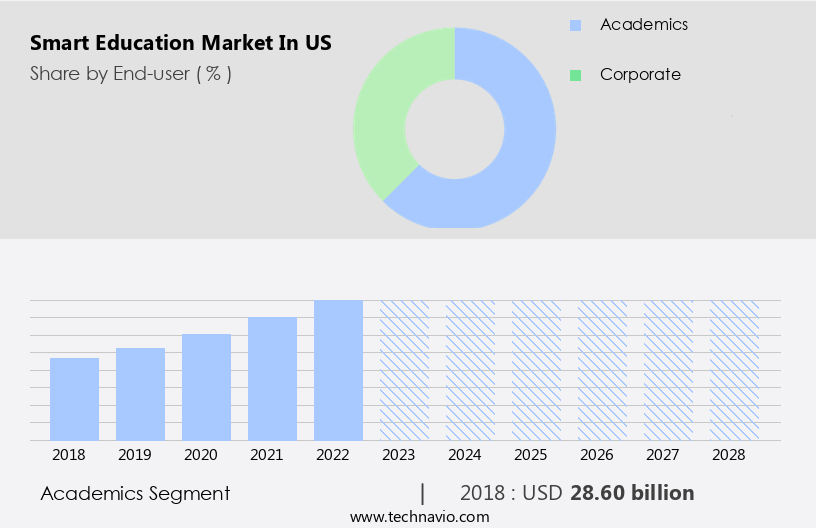

By End-user Insights

- The academics segment is estimated to witness significant growth during the forecast period.

The K-12 segment of the US smart education market is experiencing significant growth due to favorable government initiatives and increasing corporate investments. Traditional K-12 education has historically focused on rote memorization and individual learning, but there is a shift towards more interactive and collaborative approaches. This transition requires teachers to possess digital skills and an understanding of effective teaching methods. The education sector is integrating software, services, and hardware, including simulation-based learning, social learning, blended learning, adaptive learning, and collaborative learning. Corporations are also investing in virtual classrooms, virtual desktop infrastructure, and remote browser isolation for their training programs.

However, high-speed internet, digital education, cloud computing technology, and virtual environments are enabling real-world scenario-based learning in healthcare, aviation, engineering, and other industries. The service segment, including educational content providers, is a key contributor to the market's growth. The use of artificial intelligence, machine learning, virtual reality, and personalized learning approaches is transforming student learning in classrooms and online environments.

Get a glance at the market share of various segments Request Free Sample

The academics segment was valued at USD 28.60 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of US Smart Education Market?

Learning process enhancements in academic sector is the key driver of the market.

- The US education sector is experiencing significant transformation through technology, with favorable government initiatives and corporate fundings driving innovation. Hardware, software, and services are key areas of investment, enabling the adoption of advanced educational technologies. Interactive whiteboards, tablets, computers, and instructional software are commonplace in classrooms. Virtual classrooms, virtual desktop infrastructure, and high-speed internet facilitate online learning environments. Simulation-based learning, social learning, blended learning, adaptive learning, collaborative learning, and personalized learning approaches are revolutionizing academics for both corporates and students. Virtual reality, artificial intelligence, and machine learning are enhancing teaching strategies.

- Moreover, virtual environments provide real-world scenarios for healthcare, aviation, engineering, and other industries. Digital education, cloud computing technology, and online assessments with automated grading and data analytics offer data-driven insights. Multinational companies are investing in educational content, simulation-based learning, and microlearning for their training programs. Service segment providers offer remote browser isolation, containerized application streaming, and VPNs for secure access to educational content. Government-driven initiatives and corporate organizations are embracing digital teaching methods, including gamification and mobile educational applications. Social media platforms are being used for collaborative learning and academic training programs. The education field is evolving, with students and instructors adapting to these new learning modes and analytics to optimize student learning.

What are the market trends shaping the US Smart Education Market?

Rise of education 4.0 is the upcoming trend In the market.

- The smart education market In the US is experiencing significant growth due to favorable government initiatives and corporate fundings. Industry 4.0, which involves automation technologies, simulation, analytics, and cloud computing, is driving the need for upgraded skills In the workforce. In response, educational institutions and corporate organizations are revamping their curriculum and training methods to align with industry best practices. The smart education system plays a crucial role in this transformation. It enables institutions and organizations to develop customized courses and content based on the latest industry trends. Software, services, hardware, and hardware suppliers, software developers, content providers, and portable communication devices are key players in this market. Smart education encompasses various learning modes, including simulation-based learning, social learning, blended learning, adaptive learning, collaborative learning, and personalized learning approaches. Online assessments, automated grading, data analytics, teaching strategies, and interactive whiteboards, tablets, computers, and instructional software are integral components of smart education.

- Additionally, virtual classrooms, virtual desktop infrastructure, telecom, media and entertainment, remote browser isolation, containerized application streaming, and data-driven insights are also essential technologies in the smart education market. Virtual reality, artificial intelligence, machine learning, colleges, institutions, high-speed internet, and digital education are transforming the educational field. The service segment, which includes educational content, learning analytics, academic training programs, social media platforms, and virtual environments, is a significant contributor to the market's growth. Corporate organizations are increasingly investing in training programs that employ interactive learning techniques, mobile educational applications, gamification, and e-learning methods. Overall, the smart education market In the US is poised for growth, driven by the need for upgraded skills In the workforce and the adoption of advanced technologies in education and training.

What challenges does US Smart Education Market face during the growth?

Implementation challenges is a key challenge affecting the market growth.

- The education sector In the US is experiencing significant advancements driven by favorable government initiatives and corporate fundings. Smart education, which encompasses software, services, hardware, simulation-based learning, social learning, blended learning, adaptive learning, collaborative learning, and virtual classrooms, is transforming the academic and corporate landscapes. Technologies like virtual desktop infrastructure, telecom, media and entertainment, remote browser isolation, and containerized application streaming are integral to this transformation. Data-driven insights and personalized learning approaches are enabling more effective teaching strategies. Online assessments, automated grading, data analytics, and machine learning are streamlining academic processes. Virtual reality, artificial intelligence, and machine learning are providing real-world scenarios for healthcare, aviation, engineering, and other industries. Colleges and institutions are adopting high-speed internet, digital education, and cloud computing technology to enhance learning environments. Despite these advancements, challenges remain.

- Further, the integration of new digital technologies into existing IT systems necessitates careful planning and execution. Ensuring adequate internet connectivity, network stability, and hardware capabilities are essential. Additionally, the education field is embracing interactive whiteboards, tablets, computers, instructional software, and online learning environments to cater to the diverse needs of learners. Corporate organizations are investing in training programs using e-learning methods, interactive learning techniques, and mobile educational applications. Gamification is also gaining popularity in both academic and corporate settings. The service segment, including hardware suppliers, software developers, content providers, and portable communication devices, is a key player in this evolving market.

Exclusive US Smart Education Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, market growth and forecasting, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adobe Inc.

- Alphabet Inc.

- Anthology Inc.

- Cengage Learning Holdings II Inc.

- Chegg Inc.

- Cisco Systems Inc.

- Cornerstone OnDemand Inc.

- D2L Inc.

- Echo360

- Fujitsu Ltd.

- Hon Hai Precision Industry Co. Ltd.

- Instructure Holdings Inc.

- Intel Corp.

- International Business Machines Corp.

- MAXHUB

- Meta Platforms Inc.

- Microsoft Corp.

- Pearson Plc

- Samsung Electronics Co. Ltd.

- zSpace Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The education sector in various industries is witnessing a significant shift towards smart technologies, with a focus on enhancing the learning experience and improving educational outcomes. This trend is driven by several factors, including the increasing availability of high-speed internet and advancements in software, services, and hardware. One of the key areas of growth in smart education is simulation-based learning. This approach allows learners to experience real-world scenarios in a controlled environment, enabling them to develop practical skills and gain a deeper understanding of complex concepts. Social learning, another emerging trend, facilitates collaboration and interaction among learners, fostering a more engaging and effective learning experience. Blended learning, which combines traditional classroom instruction with online learning, is also gaining popularity. Adaptive learning, which uses data analytics to personalize learning approaches, is helping learners progress at their own pace and achieve better learning outcomes. Collaborative learning, which encourages group work and peer-to-peer interaction, is fostering a more engaging and effective learning environment.

Moreover, the use of artificial intelligence and machine learning in education is another area of significant growth. These technologies are being used to develop personalized learning approaches, automate grading, and provide data-driven insights to instructors and learners. Virtual reality and virtual classrooms are also being adopted to create interactive learning experiences and simulate real-world environments. The education sector is seeing significant investment from both academics and corporations. Corporate organizations are investing in training programs to upskill their workforce and remain competitive In the digital age. Multinational companies are partnering with educational institutions to develop customized academic training programs. The service segment, which includes software developers, content providers, and hardware suppliers, is a key player In the smart education market. They are developing innovative solutions to meet the evolving needs of learners and instructors. Virtual private networks (VPNs) and remote browser isolation are being used to ensure secure and reliable access to online learning environments.

Thus, containerized application streaming and data analytics are being used to optimize learning experiences and improve educational outcomes. The use of portable communication devices, such as tablets and computers, is also on the rise in smart education. Interactive whiteboards and instructional software are being used to create engaging and interactive learning environments. Online assessments and automated grading are helping instructors to assess learner progress more effectively and efficiently. The education sector is also seeing significant investment from the telecom, media and entertainment, and healthcare industries. High-speed internet and digital teaching are being used to provide remote learning opportunities to students in rural and underserved areas. Virtual environments are being used to simulate real-world scenarios for healthcare professionals and aviation pilots. In summary, the smart education market is experiencing significant growth, driven by factors such as government initiatives, corporate fundings, and advancements in technology. The use of simulation-based learning, social learning, blended learning, adaptive learning, collaborative learning, and personalized learning approaches are transforming the way we learn and teach. The education sector is seeing significant investment from various industries, and the use of artificial intelligence, machine learning, virtual reality, and virtual classrooms is revolutionizing the way we learn and interact.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

139 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 21.49% |

|

Market growth 2024-2028 |

USD 143.8 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

17.41 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across US

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -