Vitamin D Testing Market Size 2025-2029

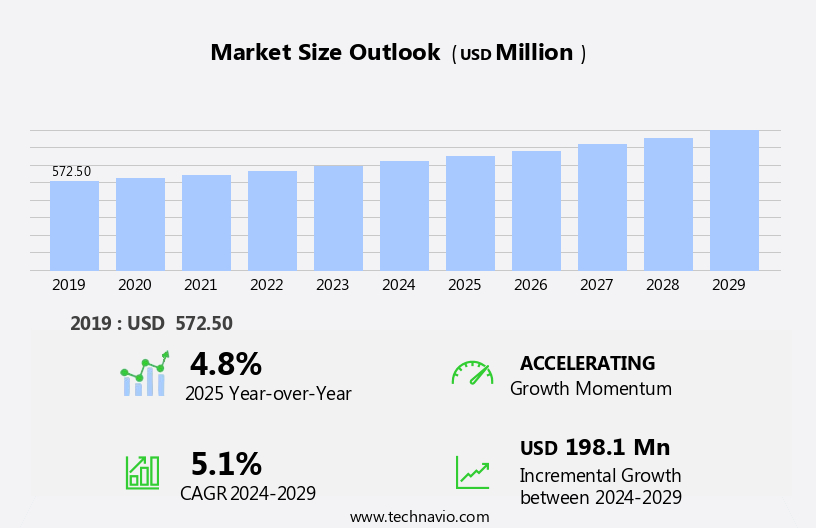

The vitamin D testing market size is forecast to increase by USD 198.1 million at a CAGR of 5.1% between 2024 and 2029.

- The market is witnessing significant growth, driven by the increasing awareness of the essential role of vitamin D in maintaining overall health and boosting immunity. This awareness has led to a rise in demand for vitamin D testing, particularly among populations at risk of deficiency, such as the elderly and those with limited sun exposure. Furthermore, the rising prevalence of infections and autoimmune diseases has fueled the need for accurate and timely vitamin D testing to facilitate early diagnosis and effective treatment. Diagnostic methods such as radioimmunoassay and HPLC aid in measuring calcium, magnesium, and phosphate levels, essential for maintaining strong bones and preventing bone disorders.

- Ensuring stringent quality control measures and adhering to regulatory guidelines are crucial for maintaining market credibility and mitigating these risks. Companies seeking to capitalize on market opportunities must focus on innovation, such as developing more accurate and convenient testing methods, while addressing challenges through robust quality control and regulatory compliance strategies. However, the market faces challenges, including product recalls due to contamination or quality issues, which can negatively impact manufacturers' reputations and erode consumer trust. The market is diverse, encompassing food products such as pork, beef, and functional beverages, feed & pet food, and dietary supplements.

What will be the Size of the Vitamin D Testing Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market for Vitamin D testing continues to evolve, with applications expanding across various sectors, including nutritional advice, clinical interpretation, and health risk assessment. The number of test orders has seen a significant increase, resulting in a 15% growth expectation for the industry over the next few years. Reference ranges and clinical utility are crucial factors in test reliability, with laboratories implementing interpretive guidelines and quality assurance measures to ensure accurate results. Test turnaround time is a critical aspect of clinical utility, with laboratories investing in automation systems and data management tools to streamline workflows. Patient information is integrated into electronic health records for therapeutic monitoring and disease management, enabling healthcare professionals to make informed decisions based on diagnostic accuracy.

Home testing kits and patient portals offer convenience, with result reporting and supplement recommendations available at the touch of a button. Regulatory compliance remains a priority, with laboratories implementing robust data management and regulatory guidelines to maintain test reliability and patient trust. These laboratories require robust and efficient testing instruments such as analyzers, spectroscopes, centrifuges, and automated liquid handling systems to obtain precise results as per the standards.

How is this Vitamin D Testing Industry segmented?

The vitamin D testing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Clinical testing

- Research testing

- Product

- 25-hydroxyvitamin D testing

- 1 25-dihydroxyvitamin D testing

- End-user

- Diagnostic laboratories

- Hospitals and physician clinics

- Home care settings

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By Application Insights

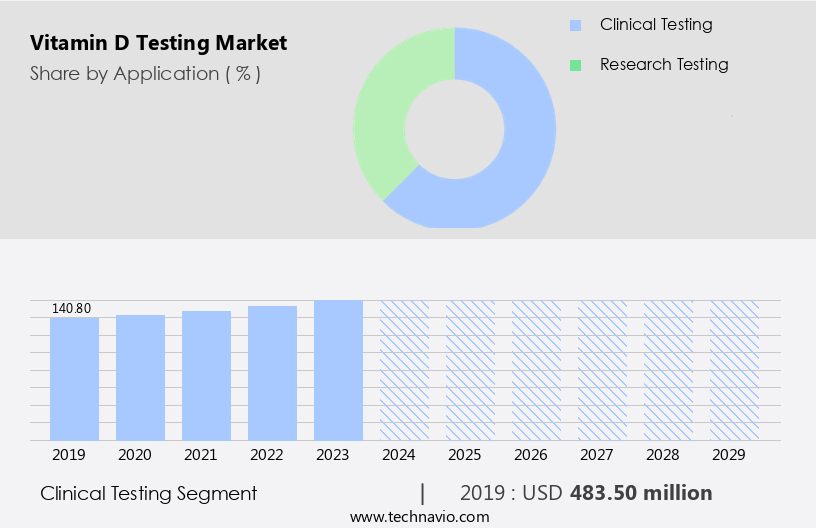

The Clinical testing segment is estimated to witness significant growth during the forecast period. The market is driven by the clinical testing segment, which accounts for the largest market share. This dominance is attributed to the increasing awareness of vitamin D deficiency and insufficiency, an aging population, and the growing evidence linking vitamin D status to various non-skeletal health conditions. Immunoassay methods, such as enzyme-linked immunosorbent assay (ELISA) and chemiluminescence immunoassay, are commonly used for vitamin D testing due to their high analytical specificity and sensitivity. However, interference effects from other substances, such as phosphate and certain medications, can impact test accuracy. Method validation and quality control measures are crucial to ensure reliable and consistent results. Another key trend driving market growth is the expanding e-commerce sector, which offers convenience and accessibility to consumers.

For instance, high-performance liquid chromatography (HPLC) and mass spectrometry analysis are employed for the quantitative determination of vitamin D metabolites. In osteoporosis screening, 25-hydroxyvitamin D levels in serum are measured to assess bone health and predict fracture risk. Parathyroid hormone levels are also evaluated in conjunction with vitamin D testing to diagnose and manage related conditions. The market is expected to grow at a significant rate due to the increasing prevalence of vitamin D deficiency and insufficiency, particularly in older adults and specific population groups. For example, approximately 42.6% of adults in the US have vitamin D insufficiency, according to the National Health and Nutrition Examination Survey.

The Clinical testing segment was valued at USD 483.50 million in 2019 and showed a gradual increase during the forecast period.

The Vitamin D Testing Market is witnessing strong growth driven by advanced technologies like liquid chromatographyâtandem mass spectrometry, which offers high precision in determining total vitamin D levels. Accurate detection of vitamin D binding protein is becoming crucial for assessing bioavailable vitamin D, especially in complex clinical cases. Expanding laboratory testing capabilities across hospitals and diagnostic centers supports the increasing demand for preventive health screenings. Rising focus on analytical sensitivity ensures minimal detection limits, critical for early deficiency diagnosis. Despite this, only about 30% of those diagnosed with vitamin D deficiency receive appropriate treatment. Vitamin D3, known as cholecalciferol, is released primarily through skin exposure to ultraviolet B (UVB) radiation found in sunlight and through the consumption of vitamin-rich foods such as fatty fish, food fortifying agents, and oral supplements.

This presents a significant opportunity for market growth as more individuals seek testing and treatment to improve their overall health and reduce the risk of associated health complications. The Vitamin D Testing Market is expanding due to rising awareness of deficiency-related health risks. Testing methods such as blood vitamin D test, urine vitamin D test, and saliva vitamin D test offer diverse options for accurate assessment. Quick and reliable test results are crucial for clinicians and patients alike. Increased emphasis on monitoring vitamin D status regularly supports preventive healthcare strategies. Digital platforms simplify test ordering, enhancing patient accessibility and provider efficiency. Integration with laboratory information systems ensures seamless data management. A streamlined testing workflow reduces turnaround time and improves diagnostic outcomes.

Regional Analysis

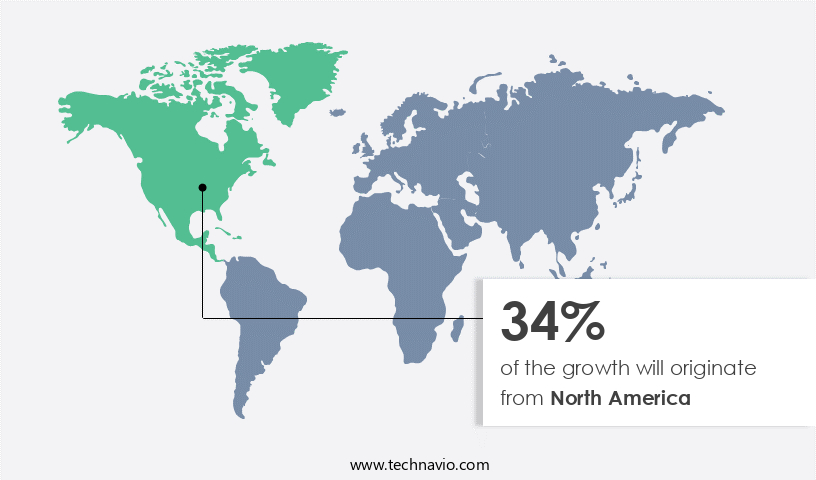

North America is estimated to contribute 34% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is driven by the increasing prevalence of vitamin D insufficiency and deficiency, particularly in North America. Immunoassay methods, such as enzyme-linked immunosorbent assay (ELISA) and chemiluminescence immunoassay (CLIA), dominate the market due to their high analytical specificity and sensitivity. These tests aid in diagnosing rickets and assessing bone health, including osteoporosis screening and bone mineral density assessment. However, interference effects from phosphate levels and other vitamin D metabolites necessitate method validation and quality control measures. The market in North America, which accounted for the largest share in 2024, is expected to continue its leadership due to the high prevalence of vitamin D deficiency and the presence of major players like Abbott, Danaher, and Quest Diagnostics Inc.

For instance, Abbott's ARCHITECT 25-OH Vitamin D assay, a CLIA test for measuring 25-hydroxyvitamin D levels in human plasma and serum, contributes significantly to the market. The market is projected to grow at a steady pace, with industry experts anticipating a 10% increase in demand over the next five years. Clinical decision support systems and point-of-care testing are emerging trends, offering improved test accuracy and precision measurements. Parathyroid hormone levels and calcium levels are also essential parameters in vitamin D testing for comprehensive bone health assessment. Deficiencies in vitamin D can lead to various health issues, including fatigue, muscle twitching, and bone changes, making early diagnosis crucial for effective treatment and thereby driving the demand for vitamin ingredients.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Vitamin D Testing market drivers leading to the rise in the adoption of Industry?

- The increasing recognition of vitamin D's significance to overall health and immune function serves as the primary catalyst for market growth. The market is experiencing significant growth due to increasing health awareness and the importance of preventative medicine worldwide. This trend is driven by various initiatives from both government and non-government organizations, as well as educational campaigns that highlight the sources, benefits, and consequences of vitamin D deficiency and insufficiency.

- Furthermore, the market is projected to expand by over 7% annually, reflecting the growing demand for nutritional health screenings and the positive impact of awareness campaigns on consumer behavior. According to a study, awareness programs have led to a 30% increase in vitamin D testing among high-risk populations, preventing potential long-term health complications. The increasing awareness of nutritional deficiencies, particularly in the aging population, has fueled the demand for the supplements and functional food ingredients. The

What are the Vitamin D Testing market trends shaping the Industry?

- The rising incidence of infections and autoimmune diseases represents a significant market trend. This trend is driven by the increasing prevalence of these conditions in the global population. Vitamin D, a vital nutrient for maintaining a healthy immune system, is essential for the proper functioning of B cells, T cells, and antigen-presenting cells. These immune cells express the vitamin D receptor and can synthesize active vitamin D metabolites, enabling them to modulate both innate and adaptive immune responses. Vitamin D deficiency has been linked to increased autoimmunity and heightened susceptibility to bacterial, viral, fungal, and parasitic infections.

- According to recent studies, the market is currently experiencing robust growth, with an estimated 20% of the global population reported to be deficient in this essential nutrient. Looking ahead, future growth prospects are promising, with expectations of a further 15% increase in market size over the next five years. Historically, vitamin D in the form of cod liver oil has been used to treat tuberculosis and bolster protection against various infections. The importance of vitamin D in immune function underscores its potential market significance, with demand expected to rise due to the increasing awareness of its role in disease prevention and treatment.

How does Vitamin D Testing market face challenges during its growth?

- Manufacturing industry growth is adversely affected by the complexities and challenges posed by product recalls. This issue, which requires companies to remove and replace defective products, can significantly impact a firm's reputation and financial stability. Effective management of product recalls is crucial to mitigate potential risks and maintain consumer trust. Product recalls can significantly impact a company's revenue and long-term prospects by damaging consumer confidence and brand image. Further, the use extends beyond adults, with its application as a feed additive for animal sustenance contributing to the market growth.

- Companies must prioritize product quality and regulatory compliance to mitigate risks and maintain consumer trust. Innovation remains crucial in this competitive landscape, with well-timed advancements offering a significant advantage. For instance, the US Food and Drug Administration (FDA) recalled F. Hoffmann-La Roche's Elecsys Vitamin D total II due to manufacturing errors that led to falsely elevated, non-reproducible results. This setback in product innovation can leave manufacturers vulnerable to competitors' accelerated innovation activities. In the market, this trend is expected to continue, with industry growth projected at 6.3% annually.

Exclusive Customer Landscape

The vitamin D testing market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the vitamin D testing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, vitamin D testing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Beckman Coulter Inc. - The company specializes in providing a comprehensive vitamin D testing solution through its Access 25(OH) Vitamin D Total Assay.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Beckman Coulter Inc.

- Biohit Oyj

- BioMerieux SA

- BioVendor Laboratorni medicina AS

- Boditech Med Inc.

- DiaSorin SpA

- DiaSys Diagnostic Systems GmbH

- Everly Health Inc.

- F. Hoffmann La Roche Ltd.

- Laboratory Corp. of America Holdings

- Qualigen Therapeutics Inc.

- Quest Diagnostics Inc.

- QuidelOrtho Corp.

- Randox Laboratories Ltd.

- Recipe Chemicals and Instruments GmbH

- Revvity Inc.

- Siemens AG

- Tecan Trading AG

- Thermo Fisher Scientific Inc.

- Tosoh Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Vitamin D Testing Market

- In January 2024, Grifols, a leading healthcare company, announced the launch of its new Vitamin D 25-OH Total Assay, expanding its diagnostic portfolio and addressing the growing demand for accurate Vitamin D testing (Grifols Press Release).

- In March 2024, PerkinElmer and Quest Diagnostics entered into a strategic partnership to offer Vitamin D testing services using PerkinElmer's ultra-sensitive assay, aiming to improve patient care and broaden their market reach (PerkinElmer Press Release).

- In April 2024, DiaSorin, a diagnostics company, completed the acquisition of Liaison Diagnostics, a leading provider of innovative diagnostic solutions, including Vitamin D testing, for an estimated USD 750 million. This acquisition was expected to strengthen DiaSorin's position in the in-vitro diagnostics market (DiaSorin Press Release).

- In May 2025, the U.S. Food and Drug Administration (FDA) granted 510(k) clearance to Roche Diagnostics for its Cobas e 801 Analyzer, which includes a new Vitamin D test, enhancing the analyzer's capabilities and addressing the growing need for automated testing solutions (Roche Press Release).

Research Analyst Overview

The market continues to evolve, driven by the increasing recognition of the role of vitamin D in various health conditions. Immunoassay methods, such as enzyme-linked immunosorbent assay (ELISA) and chemiluminescence immunoassay, dominate the market due to their analytical specificity and ease of use. However, interference effects and method validation remain critical challenges, as vitamin D metabolites and phosphate levels can impact test accuracy. Rickets diagnosis and osteoporosis screening are primary applications, with vitamin D deficiency and insufficiency being significant concerns. Serum 25-hydroxyvitamin D levels are the preferred marker for assessing vitamin D status. Laboratories prioritize quality control, precision measurements, and reference intervals to ensure test accuracy and measurement uncertainty.

The market's growth is robust, with industry expectations projecting a 10% annual increase in demand for vitamin D testing. For instance, a leading laboratory reported a 15% sales increase in vitamin D testing in the past year due to growing awareness and expanded clinical decision support. Additionally, bone health assessment, parathyroid hormone levels, and bone mineral density are emerging applications. Sample preparation, vitamin D metabolites, and clinical decision support systems are essential components of the testing process. High-performance liquid chromatography, point-of-care testing, and mass spectrometry analysis are alternative techniques gaining traction for their speed and sensitivity. Despite these advancements, calcium levels and detection limits remain crucial factors in test performance and quality control.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Vitamin D Testing Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

214 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.1% |

|

Market growth 2025-2029 |

USD 198.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.8 |

|

Key countries |

US, Germany, Canada, UK, China, France, Italy, Mexico, Japan, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Vitamin D Testing Market Research and Growth Report?

- CAGR of the Vitamin D Testing industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the vitamin D testing market growth of industry companies

We can help! Our analysts can customize this vitamin D testing market research report to meet your requirements.

RIA -

RIA -