Blue Hydrogen Market Size 2024-2028

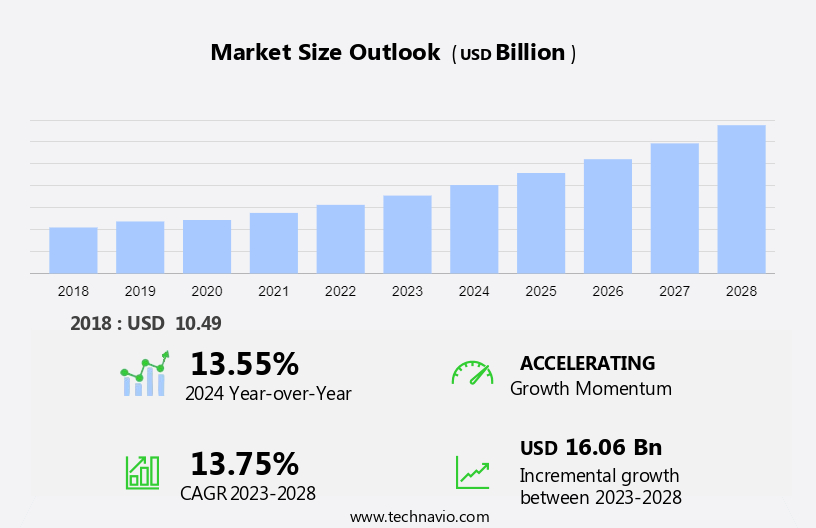

The blue hydrogen market size is forecast to increase by USD 16.06 billion at a CAGR of 13.75% between 2023 and 2028. The market is experiencing significant growth due to several key drivers. Heavy industries are increasingly turning to hydrogen as a cleaner alternative to traditional fossil fuels for processes such as hydrogen blending in natural gas networks and chemical production. Environmental regulations are pushing for decarbonization, making hydrogen an attractive option for reducing carbon emissions. However, the high costs associated with producing blue hydrogen through Steam Methane Reforming (SMR) from natural gas remain a challenge. The hydrogen-based economy is gaining traction as a viable solution for reducing greenhouse gas emissions and transitioning away from traditional energy sources. As the focus on clean energy continues to grow, the market for blue hydrogen is expected to expand, providing opportunities for growth in the chemical and industrial sectors.

The blue hydrogen market is experiencing significant growth as this low-carbon transportation fuel gains traction in various sectors, including petroleum refineries, transportation, and power generation. Hydrogen-based fuels are becoming increasingly popular as the world transitions towards sustainable energy sources and decarbonization. Petroleum refineries are integrating hydrogen into their processes to reduce carbon emissions. Hydrogen can be used in refineries for synfuel production, ammonia production, and methanol production, thereby enhancing their overall efficiency and sustainability. Moreover, hydrogen can help refineries meet environmental regulations and emissions targets. In the transportation sector, hydrogen is gaining momentum as a clean fuel for fuel cell electric vehicles (FCEVs).

Additionally, the establishment of hydrogen refueling stations is essential for the widespread adoption of FCEVs. These stations will enable long-range travel and faster refueling times compared to battery electric vehicles. Power generation is another sector that can benefit significantly from hydrogen. Hydrogen can be used in combined heat and power (CHP) systems and power generation plants to produce electricity with minimal carbon emissions. Additionally, hydrogen can be used in natural gas networks as a clean-burning fuel, reducing the carbon footprint of the energy sector. The shift towards hydrogen-based fuels is driven by the need to decarbonize industries and reduce carbon emissions.

Further, carbon pricing, direct air capture, and sustainable practices are some of the initiatives being implemented to achieve this goal. Hydrogen can help industries meet their emissions targets while maintaining their operations, making it an attractive alternative to fossil fuels. The blue hydrogen market is expected to grow as more industries adopt this clean fuel. Hydrogen can be used in various industrial processes, including steel production and chemical manufacturing, to reduce carbon emissions. Furthermore, hydrogen can be used as a feedstock in the production of ammonia and methanol, which are essential chemicals in various industries. In conclusion, the blue hydrogen market is poised for growth as it offers a viable solution for reducing carbon emissions in various sectors. Hydrogen can help petroleum refineries, transportation, and power generation industries meet their decarbonization targets while maintaining their operations. The establishment of hydrogen refueling stations and the integration of hydrogen into industrial processes will further accelerate the growth of the market.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Technology

- Steam methane reforming

- Gas partial oxidation

- Auto thermal reforming

- End-user

- Petroleum refinery

- Chemical industry

- Power generation

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- France

- APAC

- China

- Middle East and Africa

- South America

- North America

By Technology Insights

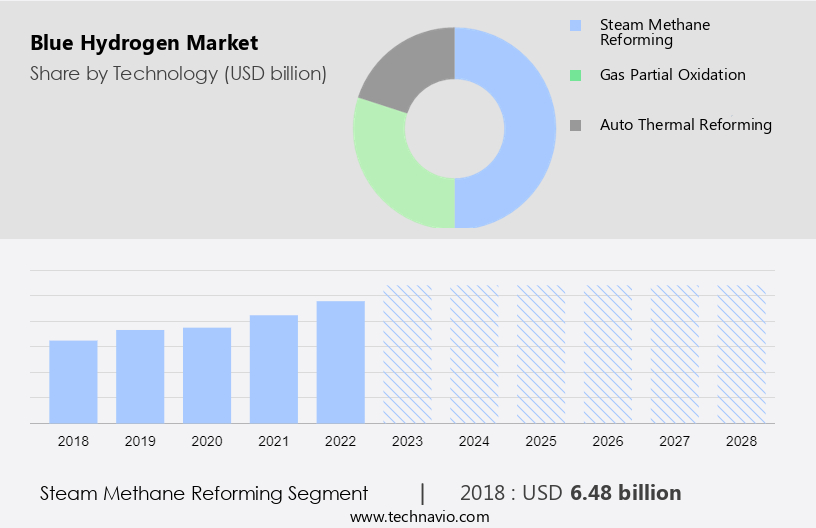

The steam methane reforming segment is estimated to witness significant growth during the forecast period. Steam methane reforming (SMR) is a process that converts natural gas into methane through the application of steam and a catalyst, typically made up of copper, nickel, and zinc. The resulting reaction produces hydrocarbon gases, including hydrogen, carbon monoxide, and water. The carbon monoxide is subsequently converted into carbon dioxide, releasing more hydrogen as a byproduct. This hydrogen, known as "blue hydrogen," is produced with lower carbon emissions and at a more affordable cost compared to gas partial oxidation and auto thermal reforming. For instance, Canada generates approximately 2-3 million tons of hydrogen annually through the SMR process of natural gas.

Carbon capture storage (CCS) technology is often employed in conjunction with blue hydrogen production to further reduce emissions. Synfuels, such as ammonia and methanol, can also be produced using blue hydrogen as a feedstock, contributing to sustainable practices within the petroleum refinery industry.

Get a glance at the market share of various segments Request Free Sample

The steam methane reforming segment accounted for USD 6.48 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

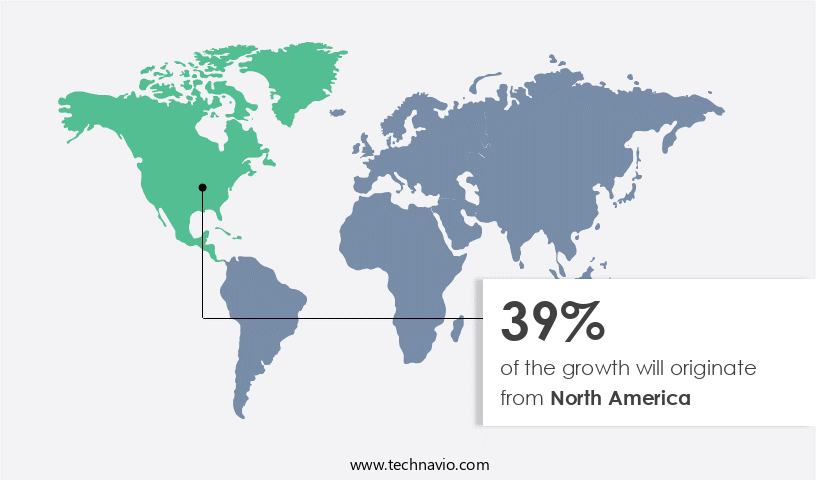

North America is estimated to contribute 39% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

Blue hydrogen is gaining traction as a low-carbon alternative to traditional hydrogen production methods in various industries across North America. Key players like Air Products are leading the charge in this space, utilizing renewable energy initiatives to produce industrial gases more sustainably. The US and Canada are at the forefront of this market, with the US accounting for a significant portion due to government incentives and industrial demand. Sectors such as chemical, fertilizer, refinery, fuel cell, and metal processing are expected to drive the growth of the market in North America.

Further, in the transportation sector, the US is a major player, with a focus on fuel-cell electric vehicles (FCEVs), fuel-cell electric buses, and material-handling vehicles. The adoption of blue hydrogen is not only environmentally friendly but also economically viable, making it an attractive option for industries looking to reduce their carbon footprint. The North American market is projected to expand steadily during the forecast period, driven by these factors.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Increasing government focus on adoption of clean hydrogen is the key driver of the market. Blue hydrogen, derived from petroleum refineries, is gaining significant attention as a low-carbon transportation fuel and for power generation. Fossil fuels continue to dominate the energy sector, and blue hydrogen, produced through steam methane reforming with captured carbon dioxide, offers a potential solution to reduce carbon emissions. The market for hydrogen-based fuels is witnessing growth due to increasing government initiatives and policies. For instance, the European Union's Hydrogen Strategy aims to create a clean hydrogen market and promote the production of blue hydrogen using renewable energy sources. In July 2020, the European Commission established the European Clean Hydrogen Alliance, which includes approximately 1,700 participants from various sectors, to foster the development of a European hydrogen sector and encourage the use of clean hydrogen for a sustainable transition.

The alliance's goal is to make hydrogen a viable alternative to traditional fossil fuels in transportation and power generation. Blue hydrogen's potential as a low-carbon fuel for transportation and power generation is driving the growth of refueling stations and hydrogen production facilities. The increasing demand for hydrogen as a fuel source is expected to create new opportunities for market participants and investors. According to recent market research, The market is projected to grow at a steady pace in the coming years. Key players in the market include major energy companies, technology providers, and infrastructure developers.

Market Trends

Growing adoption of fuel cell-powered vehicles is the upcoming trend in the market. The transport sector in the United States accounted for approximately 25-30% of the country's total CO2 emissions in 2021, primarily due to the combustion of fossil fuels. Among this, around 75% of the CO2 emissions from the transport sector originated from road vehicles, including cars, trucks, buses, and two-wheelers. In response to growing environmental concerns and stringent regulations, there is a significant shift towards sustainable technologies in the transport sector. One such technology gaining widespread adoption is fuel cells. Fuel cells are an emerging solution in the transport sector, with various original equipment manufacturers (OEMs) in the electric vehicle (EV) and material-handling equipment industries adopting this technology.

Fuel cells offer extended range and/or propulsive power to vehicles such as material-handling equipment, fuel cell electric vehicles (FCEVs), trucks, buses, trains, and autonomous vehicles. The hydrogen required for fuel cells is primarily produced through Steam Methane Reforming (SMR) in heavy industries. The hydrogen produced is then blended into natural gas networks, facilitating the transition towards a hydrogen-based economy. This decarbonization process is crucial for reducing greenhouse gas emissions and meeting environmental regulations. The adoption of fuel cells in the transport sector is expected to significantly contribute to the reduction of CO2 emissions and the promotion of a sustainable future.

Market Challenge

High costs associated with production of blue hydrogen is a key challenge affecting the market growth. Blue hydrogen, produced through water electrolysis with natural gas and carbon capture utilization, functions as a synthetic energy carrier in the transition towards net zero emissions. The production costs for blue hydrogen vary significantly, with estimates ranging from USD 1 to USD 4 per kilogram. This economic infeasibility is primarily due to the substantial capital expenditure (CAPEX) required for the production equipment. Key components of blue hydrogen production include the reformer unit, steam turbine, balance of plant, and other technology-specific units, such as steam methane reforming (SMR) and autothermal reforming (ATR). Renewable electricity procurement costs also contribute to the overall production cost.

In the UK, for instance, blue hydrogen production costs were approximately 35%-40% higher than anticipated prices in 2021. Energy efficiency and low-carbon technologies are crucial in reducing energy losses and greenhouse emissions associated with blue hydrogen production. Enhancing the efficiency of hydrogen refueling stations and optimizing the production process can help mitigate these concerns and make blue hydrogen a more economically attractive option for the energy sector.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Air Liquide SA: The company offers blue hydrogen that can be used in fuel cells to generate heat and electricity, and it is also a useful raw material for many industrial sectors.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Air Products and Chemicals Inc.

- Ceres Power Holdings plc

- CERTIFHY CONSORTIUM

- Chart Industries Inc.

- Cummins Inc.

- Equinor ASA

- Exxon Mobil Corp.

- Iwatani Corp.

- Linde Plc

- Messer SE and Co. KGaA

- Mitsubishi Corp.

- Nel ASA

- Orsted AS

- Shell plc

- Siemens AG

- Uniper SE

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Hydrogen is gaining significant attention as a low-carbon transportation fuel and a synthetic energy carrier for power generation. Petroleum refineries are exploring the production of hydrogen through various methods such as steam methane reforming, auto thermal reforming, and water electrolysis to reduce their carbon footprint and meet emissions targets. Hydrogen refueling stations are being established to cater to the growing demand for hydrogen-based fuels in transportation. The power generation sector is also embracing hydrogen as a clean energy source, with hydrogen-based fuels offering net zero emissions and high energy efficiency. The use of hydrogen in industrial processes, including chemical production, synfuel production, ammonia production, and methanol production, is expected to increase as part of the transition to a hydrogen-based economy.

Further, heavy industries are also turning to hydrogen as a low-carbon alternative to fossil fuels for decarbonization. Hydrogen blending in natural gas networks is another approach to reduce carbon emissions in the energy sector. Environmental regulations and emissions targets are driving the adoption of low-carbon technologies and sustainable practices in the production of hydrogen. The fueling segment of the hydrogen market is expected to grow significantly as the clean hydrogen economy gains momentum. The production methods for hydrogen, including methane reforming and water electrolysis, are being optimized for energy efficiency and reduced energy losses. The integration of renewable energy initiatives and carbon capture storage is also crucial for the sustainable production of hydrogen.

Additionally, the transition to a hydrogen-based economy offers significant potential for reducing carbon emissions and mitigating climate change. The use of hydrogen as a clean fuel in transportation and industrial processes is a key component of the clean energy transition. The adoption of low-carbon hydrogen production methods and sustainable practices is essential for the long-term success of the market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

172 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 13.75% |

|

Market growth 2024-2028 |

USD 16.06 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

13.55 |

|

Regional analysis |

North America, Europe, APAC, Middle East and Africa, and South America |

|

Performing market contribution |

North America at 39% |

|

Key countries |

US, China, Germany, UK, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Air Liquide SA, Air Products and Chemicals Inc., Ceres Power Holdings plc, CERTIFHY CONSORTIUM, Chart Industries Inc., Cummins Inc., Equinor ASA, Exxon Mobil Corp., Iwatani Corp., Linde Plc, Messer SE and Co. KGaA, Mitsubishi Corp., Nel ASA, Orsted AS, Shell plc, Siemens AG, and Uniper SE |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -