Enterprise App Store Market Size 2026-2030

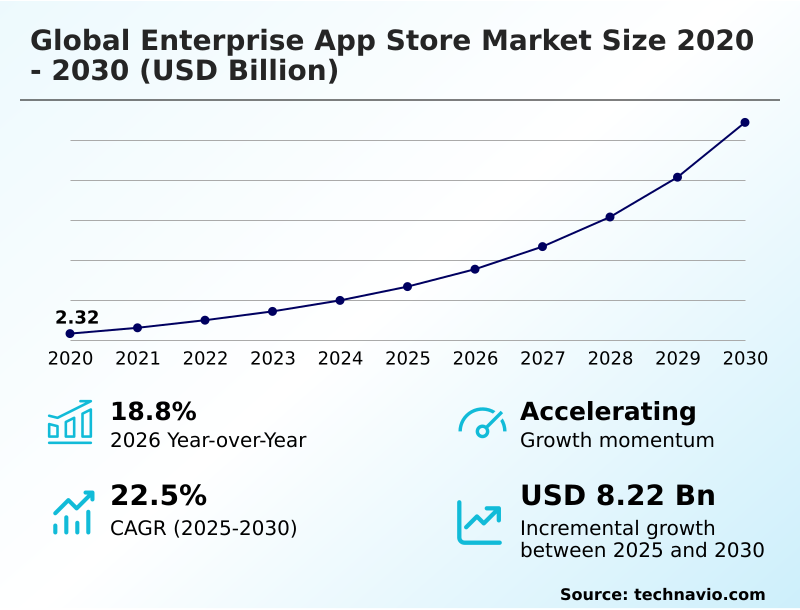

The Enterprise App Store Market size was valued at USD 4.67 billion in 2025, growing at a CAGR of 22.5% during the forecast period 2026-2030.

Major Market Trends & Insights

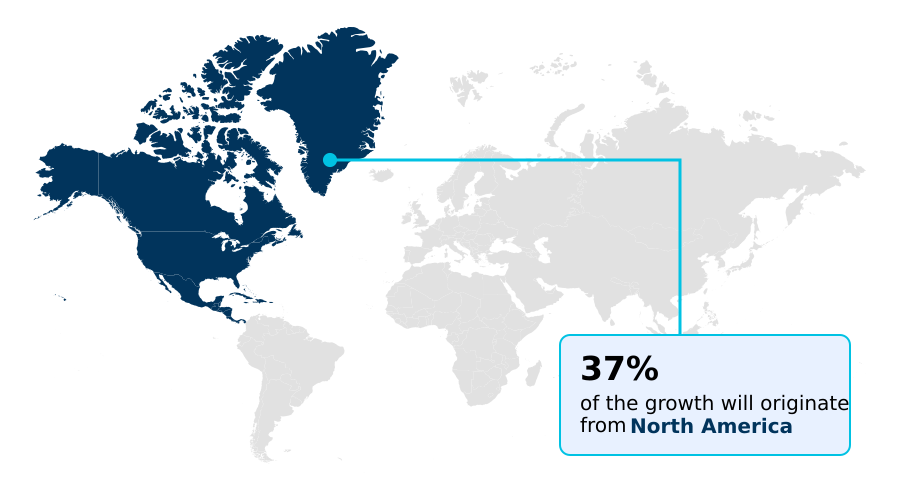

- North America dominated the market and accounted for a 36.9% growth during the forecast period.

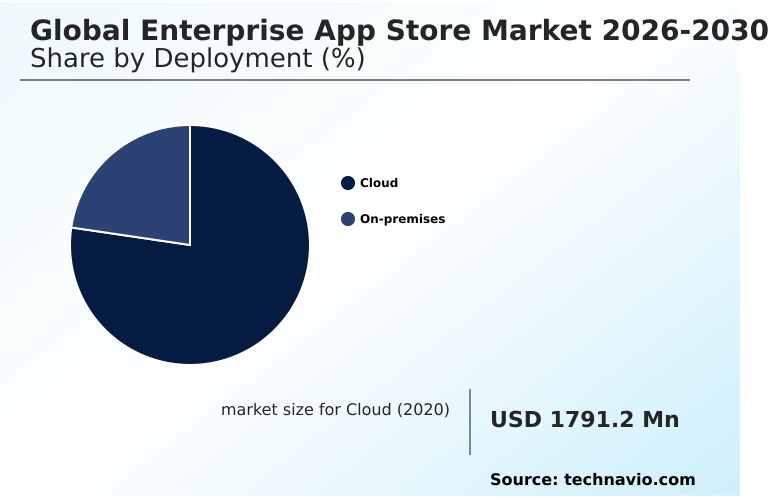

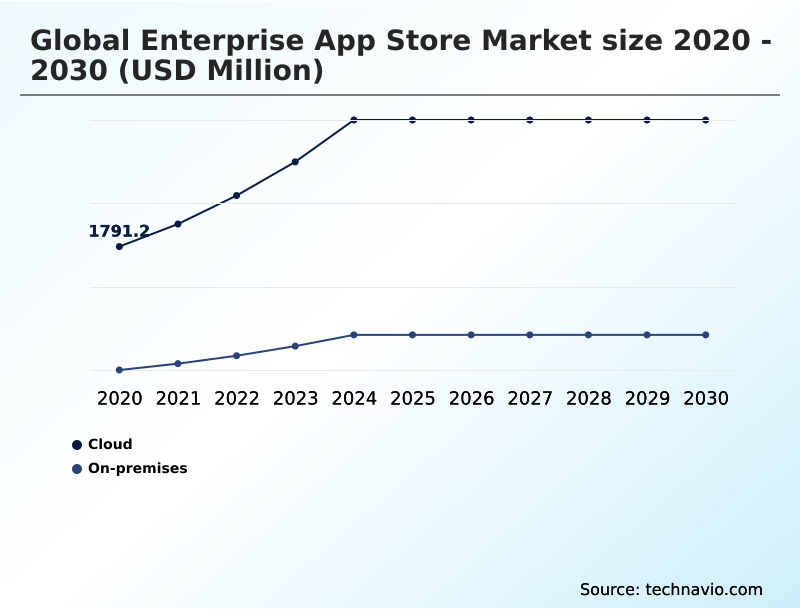

- By Deployment - Cloud segment was valued at USD 3.09 billion in 2024

- By Type - Large enterprises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 10.57 billion

- Market Future Opportunities 2025-2030: USD 8.22 billion

- CAGR from 2025 to 2030 : 22.5%

Market Summary

- The enterprise app store market is expanding at a significant rate, with a year-over-year growth of 18.8%, reflecting its critical role in modern IT governance.

- In a typical business scenario, a multinational corporation streamlines its software procurement for over 50,000 employees by replacing decentralized purchasing with a single, curated app store, reducing onboarding time by 40% and cutting redundant license costs. This shift is primarily driven by the proliferation of cloud-native infrastructure, which demands centralized management to maintain security and efficiency.

- However, the market faces a significant challenge from fragmented data sovereignty regulations across regions, which complicates the creation of a unified global application catalog. This regulatory complexity can increase administrative overhead by up to 25%, as organizations must ensure every application complies with local data laws, such as GDPR in Europe.

- Consequently, the enterprise app store evolves as a strategic tool for balancing employee self-service with stringent corporate control and compliance.

What will be the Size of the Enterprise App Store Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Enterprise App Store Market Segmented?

The enterprise app store industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- Cloud

- On-premises

- Type

- Large enterprises

- SMEs

- Platform

- iOS

- Windows

- Android

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

How is the Enterprise App Store Market Segmented by Deployment?

The cloud segment is estimated to witness significant growth during the forecast period.

The cloud segment is the largest, representing over 78% of the market by 2026, due to its scalability and lower upfront costs compared to on-premises solutions.

Large enterprises dominate adoption, but SMEs are the fastest-growing segment, leveraging enterprise app stores to access sophisticated tools without large IT teams.

From a platform perspective, effective unified endpoint management and mobile device management are critical, as they form the basis for enforcing security policies.

Functionally, these stores are essential for effective software asset management and license compliance tracking, with role-based access control and single sign-on integration ensuring that users only access approved applications.

This centralized approach to enterprise software procurement streamlines operations and enhances security through granular access controls across infrastructure-as-a-service platforms.

The Cloud segment was valued at USD 3.09 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Enterprise App Store market is rising in the leading region?

North America is estimated to contribute 36.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Enterprise App Store Market demand is rising in North America Request Free Sample

North America dominates the market, contributing 36.9% to the incremental growth, a rate approximately 14% higher than APAC's contribution.

This lead is driven by early adoption of cloud infrastructure and a mature enterprise mobility management culture in countries like the United States, which alone accounts for a substantial portion of regional demand.

In contrast, Europe focuses heavily on data privacy, leveraging private cloud marketplaces to ensure compliance.

A key difference is the prevalence of a bring-your-own-device policy in North America, which necessitates a different application lifecycle management strategy compared to regions with stricter corporate device mandates.

The use of a digital workspace platform with cross-platform compatibility and high-assurance applications is becoming standard, supported by a robust identity management framework and public cloud integration.

What are the key Drivers, Trends, and Challenges in the Enterprise App Store Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Organizations evaluating the difference between an enterprise app store vs public app store often find the former provides a 50% greater degree of security and control. The primary value lies in creating a secure channel for curated applications, which is essential for enabling secure app distribution for remote workforce models that have seen a 70% increase in adoption.

- Implementing best practices for enterprise app store governance is no longer optional; it is central to mitigating risks from unvetted software and managing SaaS sprawl. A key component of this governance is measuring ROI of an enterprise app store, where metrics go beyond cost savings to include productivity gains and reduced security incidents.

- A common challenge involves integrating custom apps into enterprise stores, a process that requires clear API documentation and streamlined workflows to be successful. Without a well-defined strategy for managing these custom applications, companies risk creating isolated data silos, undermining the goal of a unified software ecosystem.

- Ultimately, a properly managed enterprise store becomes a strategic asset, balancing the flexibility users demand with the security and oversight the organization requires, turning IT from a gatekeeper into an enabler of business agility.

What are the key market drivers leading to the rise in the adoption of Enterprise App Store Industry?

- The market is primarily driven by the widespread proliferation of cloud-native infrastructure and microservices architecture, which necessitates centralized application management.

- The primary market driver is the architectural shift to a cloud-native architecture, enabling organizations to achieve 30% faster application deployment times compared to monolithic systems.

- This move toward microservices-based applications and containerization technology allows for greater agility and scalable software deployment.

- The integration of generative AI through a sophisticated workflow automation engine is also a major force, with autonomous AI agents automating tasks that previously required significant human intervention, improving operational efficiency by over 20%.

- This centralized administrative control within a unified digital workspace facilitates API-driven integration and agentic workflow deployment, creating a more cohesive and automated enterprise technology stack.

What are the market trends shaping the Enterprise App Store Industry?

- A primary market trend is the strategic convergence of FinOps with marketplace procurement governance. This integration positions enterprise app stores as central tools for managing technology expenditures.

- A dominant trend is the integration of finops principles, which has led to a 15% improvement in budget predictability for early adopters. This strategic procurement governance allows enterprises to align software acquisition with financial objectives, directly addressing challenges of uncontrolled SaaS spending.

- The democratization of development through a low-code development platform is also reshaping the landscape, with a 25% increase in internally developed applications being distributed through these stores. This empowers non-technical staff to create and share tools, fostering a consumer-grade user experience and accelerating digital transformation initiatives.

- By leveraging a self-service software portal, companies can manage software-as-a-service environments effectively, optimizing software license optimization and reducing technical debt.

What challenges does the Enterprise App Store Industry face during its growth?

- A key challenge restraining market growth is the fragmented landscape of regulatory compliance and data sovereignty requirements across different regions.

- A significant challenge is navigating the complex web of data sovereignty compliance, which can increase app deployment timelines by up to 40% due to varied regional requirements. This necessitates a robust application vetting process and regulatory compliance automation to maintain a resilient cybersecurity posture against evolving threats.

- The proliferation of shadow IT, often stemming from interoperability constraints between core systems, remains a key vulnerability that a zero trust security model aims to address through secure software distribution. Organizations struggle with mobile application security and aim to avoid vendor lock-in by adopting more flexible platforms.

- Failure to manage these security and compliance issues can negate the agility benefits that enterprise app stores are designed to provide.

Exclusive Technavio Analysis on Customer Landscape

The enterprise app store market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the enterprise app store market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Enterprise App Store Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, enterprise app store market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

42Gears Mobility Systems Ltd. - Offerings focus on unified platforms for curated software aggregation, secure application distribution, and centralized lifecycle management within enterprise ecosystems.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 42Gears Mobility Systems Ltd.

- AppDirect Inc.

- Appian Corp.

- BlackBerry Ltd.

- Broadcom Inc.

- Citrix Systems Inc.

- Codeproof Technologies Inc.

- Esper.io Inc.

- IBM Corp.

- Ivanti Software Inc.

- Matrix42 GmbH

- Microsoft Corp.

- Miradore Oy

- Mitsogo Inc.

- Oracle Corp.

- Relution GmbH

- SAP SE

- Sophos Group Ltd.

- SOTI Inc.

- Zoho Corp. Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Application Software industry, the increasing adoption of cloud-based and subscription-based software delivery models reinforces the role of enterprise app stores as the central management plane for controlling SaaS subscriptions and implementing FinOps strategies.

- The rising automation of business processes through technologies like RPA and BPM has led to the creation of specialized categories within enterprise app stores for deploying pre-vetted autonomous AI agents and agentic workflow deployment tools.

- Heightened data security concerns associated with cloud services have positioned enterprise app stores as a critical security layer, providing a single point for a resilient cybersecurity posture and centralized administrative control to mitigate shadow IT risks.

- The push for advanced analytics in enterprises has driven demand for curated app stores that can securely deliver and manage sophisticated business intelligence tools, ensuring data governance and compliance through a self-service software portal.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Enterprise App Store Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 282 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 22.5% |

| Market growth 2026-2030 | USD 8217.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 18.8% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Egypt and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The enterprise app store ecosystem is a complex network where cloud deployments account for over 75% of the market, highlighting a major shift from on-premises solutions. Technology suppliers, including major cloud infrastructure providers and OS developers, provide the foundational platforms.

- Upon this foundation, solution providers such as unified endpoint management (UEM) specialists and enterprise software vendors like SAP and Oracle build and offer their curated marketplaces. These are distributed through direct sales channels and system integrators to end-users, primarily large enterprises and SMEs.

- A key interaction involves the rigorous application vetting process, where apps are checked for security and compliance, a function that has reduced security incidents from unvetted software by an average of 30% for adopting firms.

- Regulatory bodies and standards organizations indirectly influence the ecosystem by setting data privacy and security benchmarks that all stakeholders must adhere to, ensuring a governed, secure environment for software distribution.

What are the Key Data Covered in this Enterprise App Store Market Research and Growth Report?

-

What is the expected growth of the Enterprise App Store Market between 2026 and 2030?

-

The Enterprise App Store Market is expected to grow by USD 8.22 billion during 2026-2030, registering a CAGR of 22.5%. Year-over-year growth in 2026 is estimated at 18.8%%. This acceleration is shaped by proliferation of cloud-native infrastructure and microservices architecture , which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud, and On-premises), Type (Large enterprises, and SMEs), Platform (iOS, Windows, and Android) and Geography (North America, Europe, APAC, South America, Middle East and Africa). Among these, the Cloud segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, South America and Middle East and Africa. North America is estimated to contribute 36.9% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Egypt and Israel, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is proliferation of cloud-native infrastructure and microservices architecture , which is accelerating investment and industry demand. The main challenge is fragmented regulatory compliance and data sovereignty requirements , creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Enterprise App Store Market?

-

Key vendors include 42Gears Mobility Systems Ltd., AppDirect Inc., Appian Corp., BlackBerry Ltd., Broadcom Inc., Citrix Systems Inc., Codeproof Technologies Inc., Esper.io Inc., IBM Corp., Ivanti Software Inc., Matrix42 GmbH, Microsoft Corp., Miradore Oy, Mitsogo Inc., Oracle Corp., Relution GmbH, SAP SE, Sophos Group Ltd., SOTI Inc. and Zoho Corp. Pvt. Ltd.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape of the enterprise app store market is defined by platform consolidation, with the top 5 vendors accounting for over 60% of market share. Key players like Microsoft and SAP are enhancing their offerings by embedding AI and automation directly into their marketplaces.

- For instance, Microsoft's integration of Copilot into its Azure Marketplace enables intelligent application discovery and governance, while SAP Store focuses on providing a curated selection of industry-specific extensions. These developments directly address enterprise demand for greater efficiency and streamlined workflow interoperability, allowing businesses to deploy complex solutions more rapidly. This strategic focus helps organizations manage the proliferation of SaaS tools.

- However, vendors still face the challenge of navigating complex technical debt within customer environments, which can slow down the adoption of new, integrated platform features.

We can help! Our analysts can customize this enterprise app store market research report to meet your requirements.

RIA -

RIA -