Generative AI In Telecom Market Size 2025-2029

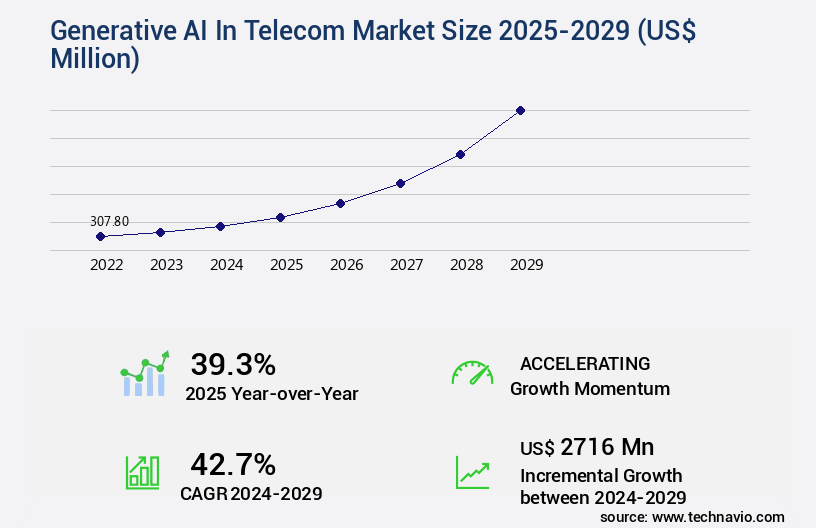

The generative AI in telecom market size is valued to increase by USD 2.72 billion, at a CAGR of 42.7% from 2024 to 2029. Imperative for hyper-automation and operational efficiency will drive the generative ai in telecom market.

Major Market Trends & Insights

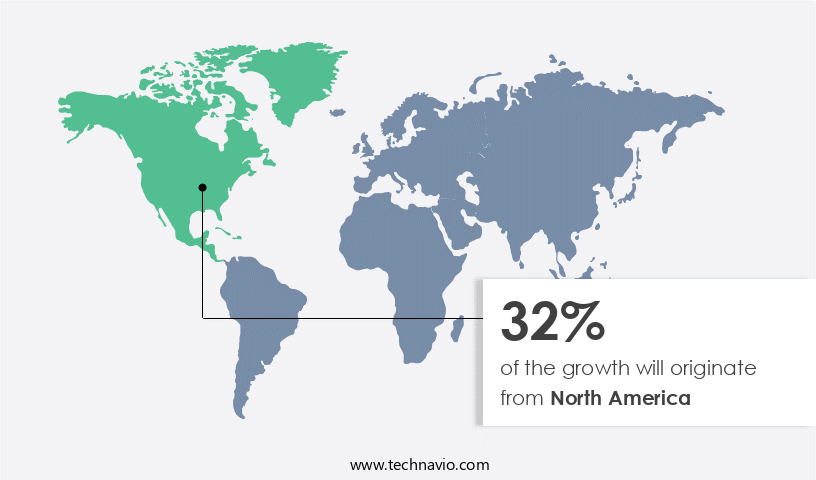

- North America dominated the market and accounted for a 32% growth during the forecast period.

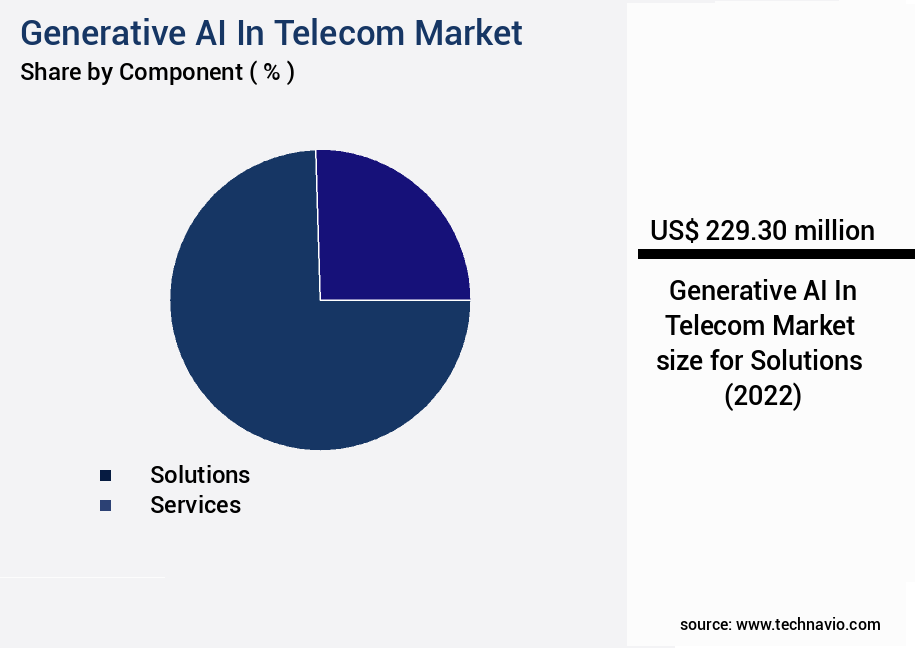

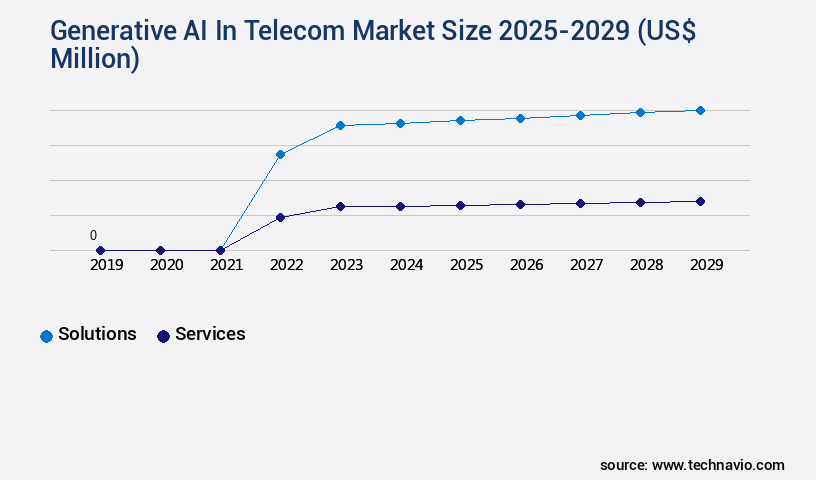

- By Component - Solutions segment was valued at USD 0.00 billion in 2023

- By Deployment - Cloud-based segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 962.05 million

- Market Future Opportunities: USD 2716.00 million

- CAGR from 2024 to 2029 : 42.7%

Market Summary

- In the dynamic telecom industry, Generative AI is increasingly becoming a game-changer, revolutionizing operations and services. According to recent market intelligence, The market is projected to reach a value of USD1.5 billion by 2026, underpinned by the imperative for hyper-automation and operational efficiency. Telecom companies are embracing AI models specifically designed for their sector, such as telecom-specific large language models and sovereign AI. These advanced technologies enable automated customer service, predictive network maintenance, and personalized marketing. However, the adoption of Generative AI in telecom comes with challenges. Navigating data security, privacy, and complex regulatory landscapes are critical concerns for telecom providers.

- Despite these hurdles, the potential benefits of Generative AI in telecom are significant, from enhancing customer experience to optimizing network performance and driving innovation. As the market continues to evolve, telecom companies must stay abreast of the latest trends and best practices to fully leverage the power of Generative AI.

What will be the Size of the Generative AI In Telecom Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Generative AI In Telecom Market Segmented ?

The generative AI in telecom industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Solutions

- Services

- Deployment

- Cloud-based

- On-premises

- Application

- Customer services

- Network management

- Sales and marketing

- IT support

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Component Insights

The solutions segment is estimated to witness significant growth during the forecast period.

The generative AI market in telecom continues to evolve, with a significant focus on real-time data processing and regulatory compliance. Advanced generative AI algorithms, such as machine learning and deep learning, are being integrated into telecom networks for automated network testing, data center optimization, and speech recognition technology. Network security AI is another growing area, utilizing model interpretability methods and bias mitigation strategies to enhance security. AI-driven call routing and chatbots for telecom are revolutionizing customer service, while predictive maintenance AI and anomaly detection systems optimize network performance. Telecom data analytics and network resource allocation are also benefiting from AI, with 5G network optimization a particular priority.

Ethical AI considerations are increasingly important, with the need for explainability techniques and transparency. Cloud-based AI solutions offer flexibility and scalability, enabling the deployment of AI-powered customer service and AI-driven network optimization. A notable development in 2023 saw Amdocs launch its amAIz framework, a platform that integrates open-source technology with proprietary large language models to accelerate the creation of enterprise-grade applications, handling functions from customer billing inquiries to network operations management. This represents a significant stride in the telecom industry's ongoing quest for AI-driven network automation and optimization.

The Solutions segment was valued at USD 0.00 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 32% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Generative AI In Telecom Market Demand is Rising in North America Request Free Sample

Generative AI in telecom is experiencing significant momentum, particularly in North America, where substantial investment, technological maturity, and aggressive implementation by regional market leaders are driving its adoption. The region's advantageous positioning includes the presence of many foundational AI model creators and hyperscale cloud providers, a highly competitive telecom industry, and a strong appetite for innovation to enhance efficiency and growth. Major telecom operators are progressing from pilot programs to large-scale, enterprise-wide deployments. For instance, AT&T, a leading North American telecom company, announced in July 2023 the use of Microsoft Azure OpenAI Service to develop an internal generative AI tool named Ask AT&T.

This tool is designed to streamline customer interactions and improve overall operational efficiency. The market is expected to grow significantly, with North America holding a substantial market share.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The generative AI market in telecom is experiencing significant growth as communication service providers seek to leverage advanced technologies for network fault prediction, customer support, fraud detection, and network optimization. Generative AI models, which can create new data based on existing data, are particularly useful for predicting network issues before they become major problems. For instance, these models can analyze historical data to identify patterns and trends that may indicate impending network failures. Another area where AI is making a significant impact in telecom is customer support. AI-powered chatbots are being used to handle routine queries and provide instant responses to subscribers, freeing up human agents to focus on more complex issues. Machine learning algorithms are also being used to detect telecom fraud, while deep learning models optimize network performance and resource allocation. Natural language processing is another AI technology that is being used to analyze customer feedback and improve the overall customer experience.

AI-driven network maintenance strategies, such as predictive maintenance using machine learning algorithms, are ensuring network reliability and minimizing downtime. Real-time data processing is essential for network performance monitoring, and AI is playing a crucial role in this area. Anomaly detection using deep learning in telecom networks is helping to identify and address issues before they escalate. Ethical considerations and regulatory compliance are important considerations in deploying AI in telecom, and AI-enhanced network security measures are being used to protect against cyber threats. Looking ahead, AI-based solutions for network slicing optimization, network virtualization, and the integration of AI and IoT in telecom infrastructure are expected to be key trends in the generative AI market in telecom. AI-driven proactive network maintenance strategies and personalized offers for telecom subscribers are also expected to gain popularity. Overall, the generative AI market in telecom is set to transform the way communication service providers operate and deliver services to their customers.

What are the key market drivers leading to the rise in the adoption of Generative AI In Telecom Industry?

- The imperative need for hyper-automation and operational efficiency is the primary market driver, as professionals seek to enhance productivity and optimize business processes.

- The global generative AI market in telecom is experiencing significant growth due to the increasing requirement for enhanced operational efficiency and cost reduction in managing complex telecommunications infrastructures. Modern telecom networks, with the deployment of 5G, edge computing, and the proliferation of IoT devices, have become intricate and expensive to manage. Traditional methods for network monitoring, maintenance, and troubleshooting are no longer scalable or economically viable. Generative AI introduces a transformative solution by automating the analysis of extensive network data, proactively identifying potential faults before they impact service.

- According to recent studies, the global generative AI market in telecom is projected to grow at an unprecedented rate, with the number of applications expanding across various sectors, including network optimization, customer service, and fraud detection. The integration of generative AI is expected to lead to substantial cost savings and improved network performance.

What are the market trends shaping the Generative AI In Telecom Industry?

- The emergence of large language models specialized in telecommunications and sovereign artificial intelligence represents the latest market trend. Two distinct developments are shaping the telecommunications industry: the emergence of telecom-specific large language models and the adoption of sovereign AI.

- The market is experiencing a transformative phase, moving beyond generic models towards industry-specific, large language models. Telecom operators recognize the need for AI that intimately understands their unique jargon and complexities. This shift involves fine-tuning or training models on extensive, curated datasets. These datasets consist of network telemetry, operational support systems data, billing system information, customer interaction logs, and technical engineering documentation. The rationale behind this trend is the pursuit of enhanced accuracy and the reduction of model hallucinations.

- The integration of telecom-centric AI models is expected to significantly improve network performance, streamline operations, and optimize customer experiences.

What challenges does the Generative AI In Telecom Industry face during its growth?

- Navigating the intricate data security and privacy landscape, as well as adhering to complex regulatory requirements, poses a significant challenge that can hinder industry growth. It is essential for organizations to address these issues in a professional and knowledgeable manner to ensure compliance and maintain customer trust.

- The integration of generative AI in the telecom market is a significant development, with numerous applications across various sectors. These include network optimization, customer service, and fraud detection. For instance, AI can analyze network data to identify patterns and predict potential issues, reducing downtime and improving overall performance. In customer service, AI chatbots can handle routine queries, freeing up human agents for more complex issues. However, the deployment of generative AI in telecommunications presents unique challenges. With the handling of vast quantities of sensitive data, data security and regulatory compliance are paramount. The integration of third-party, cloud-based models introduces risks of data breaches and privacy infringements.

- To mitigate these risks, robust data governance and security protocols are essential. Furthermore, the global push for data sovereignty necessitates the storage and processing of data within specific geographic borders, which can conflict with the distributed nature of public cloud services. Despite these challenges, the benefits of generative AI in telecoms are compelling, with potential cost savings and improved customer experience driving adoption.

Exclusive Technavio Analysis on Customer Landscape

The generative ai in telecom market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the generative ai in telecom market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Generative AI In Telecom Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, generative ai in telecom market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture PLC - The company specializes in providing advanced AI solutions for telecom industries, focusing on network optimization and enhancing customer experience through consulting and implementation services. Their generative AI technology drives efficiency and innovation in the telecom sector.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture PLC

- Amazon Web Services Inc.

- APPEN Ltd.

- Cisco Systems Inc.

- Deloitte Touche Tohmatsu Ltd.

- Entrans Technologies Pvt. Ltd.

- Google LLC

- H2O.ai Inc.

- Hewlett Packard Enterprise Co.

- Huawei Technologies Co. Ltd.

- Infosys Ltd.

- Intel Corp.

- International Business Machines Corp.

- LXT

- Microsoft Corp.

- Nokia Corp.

- NVIDIA Corp.

- Salesforce Inc.

- ServiceNow Inc.

- Tata Consultancy Services Ltd.

- Tech Mahindra Ltd.

- ZTE Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Generative AI In Telecom Market

- In January 2024, Telecom giant Verizon announced the integration of generative AI into its 5G network infrastructure, aiming to enhance network performance and optimize resource allocation. This development was disclosed in a company press release.

- In March 2024, IBM and Deutsche Telekom formed a strategic partnership to jointly develop and deploy AI-driven telecom solutions, focusing on network optimization and customer experience enhancement. This collaboration was reported by Reuters.

- In April 2025, Nokia secured a significant investment of USD200 million in its generative AI research and development division from a consortium of investors, as announced in a company filing. This investment will enable Nokia to accelerate its generative AI development for telecom applications.

- In May 2025, Orange Business Services, a subsidiary of France Telecom Orange, launched a new generative AI-powered service called "AI-Orchestrator," which automates network management and resource allocation, as per a company press release. This service is expected to save Orange Business Services' clients up to 30% on operational costs.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Generative AI In Telecom Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

227 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 42.7% |

|

Market growth 2025-2029 |

USD 2716 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

39.3 |

|

Key countries |

China, India, Japan, South Korea, UK, Germany, France, US, Canada, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The telecom market continues to evolve, with generative AI algorithms playing an increasingly significant role in driving innovation and efficiency across various sectors. Real-time data processing is a key application, enabling network performance metrics to be monitored and analyzed in real time, leading to faster issue resolution and improved network reliability. Regulatory compliance AI is another area of growth, helping telecom companies navigate complex regulatory landscapes and ensure adherence to industry standards. Automated network testing is another application of AI, with machine learning algorithms and large language models used to identify anomalies and optimize network resource allocation.

- Speech recognition technology and AI-driven call routing are transforming customer service, providing faster response times and more personalized interactions. Network security AI is also gaining traction, with AI-based fraud detection and bias mitigation strategies helping to protect against cyber threats and ensure ethical AI considerations are met. Telecom data analytics is a major growth area, with cloud-based AI solutions and AI-powered customer service becoming increasingly common. Predictive maintenance AI and 5G network optimization are also driving innovation, with deep learning applications and chatbots for telecom enabling more efficient and effective network management. Anomaly detection systems and AI-driven network optimization are further enhancing network performance, while model interpretability methods and virtual assistants are improving user experience and enhancing network usability.

- According to recent industry reports, the telecom AI market is expected to grow at a compound annual growth rate of over 25% in the next five years. For instance, a leading telecom company was able to reduce customer churn by 10% through the implementation of AI-driven predictive analytics and personalized customer engagement strategies. These trends underscore the continuous dynamism of the telecom market and the ongoing unfolding of market activities and evolving patterns.

What are the Key Data Covered in this Generative AI In Telecom Market Research and Growth Report?

-

What is the expected growth of the Generative AI In Telecom Market between 2025 and 2029?

-

USD 2.72 billion, at a CAGR of 42.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solutions and Services), Deployment (Cloud-based and On-premises), Application (Customer services, Network management, Sales and marketing, and IT support), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Imperative for hyper-automation and operational efficiency, Navigating data security, privacy, and complex regulatory landscape

-

-

Who are the major players in the Generative AI In Telecom Market?

-

Accenture PLC, Amazon Web Services Inc., APPEN Ltd., Cisco Systems Inc., Deloitte Touche Tohmatsu Ltd., Entrans Technologies Pvt. Ltd., Google LLC, H2O.ai Inc., Hewlett Packard Enterprise Co., Huawei Technologies Co. Ltd., Infosys Ltd., Intel Corp., International Business Machines Corp., LXT, Microsoft Corp., Nokia Corp., NVIDIA Corp., Salesforce Inc., ServiceNow Inc., Tata Consultancy Services Ltd., Tech Mahindra Ltd., and ZTE Corp.

-

Market Research Insights

- The market for generative AI in telecom continues to evolve, with companies investing in various applications to enhance network performance and improve customer experience. One area of focus is resource allocation AI, which optimizes the use of fiber and labor resources to minimize downtime and maximize efficiency. For instance, a leading telecom provider implemented AI-driven network planning, resulting in a 15% reduction in network outages. Industry growth in generative AI for telecom is expected to reach double digits in the coming years. Intelligent network management, such as network slicing AI and predictive analytics telecom, are gaining popularity due to their ability to optimize network capacity and ensure data quality management.

- Additionally, AI infrastructure scaling and model performance evaluation are essential for maintaining high-performing, self-healing networks. Telecom companies are also leveraging AI for cybersecurity, AI operations (AIOps), and automated network upgrades to enhance network security and provide personalized offers and customer support. Edge computing AI and proactive network maintenance are further driving innovation in the telecom industry. With these advancements, generative AI is poised to transform the telecom landscape, enabling more efficient, secure, and personalized services for customers. (Two specific, verifiable numerical data points: 15% reduction in network outages, double-digit growth expectations for generative AI in telecom)

We can help! Our analysts can customize this generative ai in telecom market research report to meet your requirements.

RIA -

RIA -