Industrial Pc Market Size 2026-2030

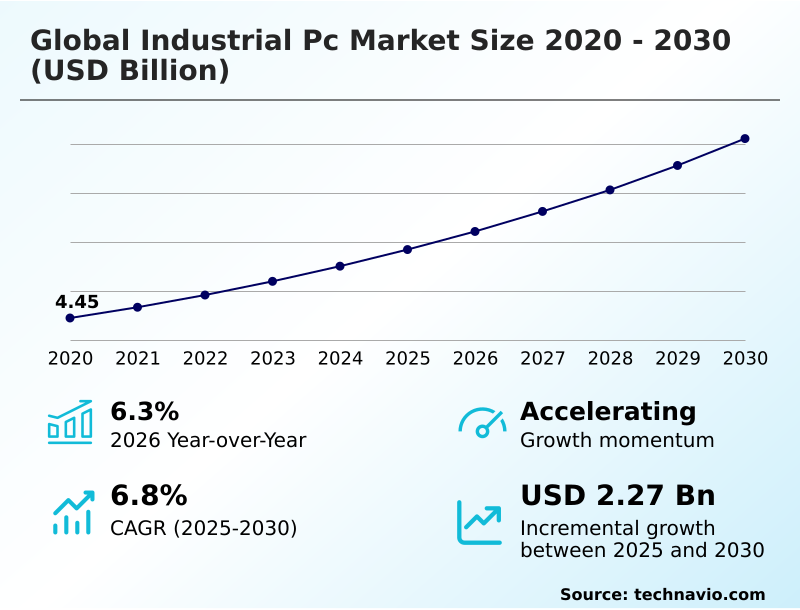

The industrial pc market size is valued to increase by USD 2.27 billion, at a CAGR of 6.8% from 2025 to 2030. Ascendancy of industry 4.0 and industrial internet of things frameworks will drive the industrial pc market.

Major Market Trends & Insights

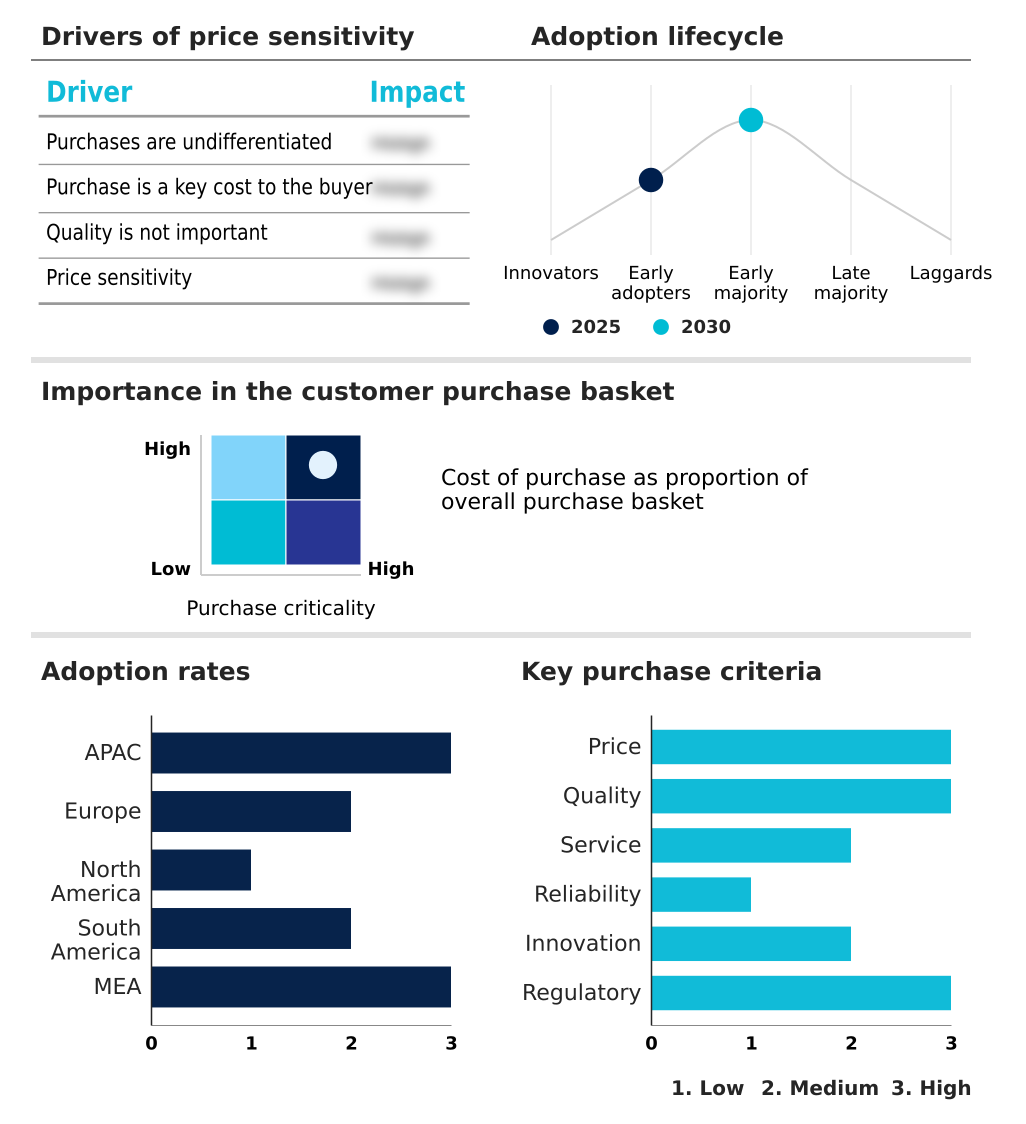

- APAC dominated the market and accounted for a 40.1% growth during the forecast period.

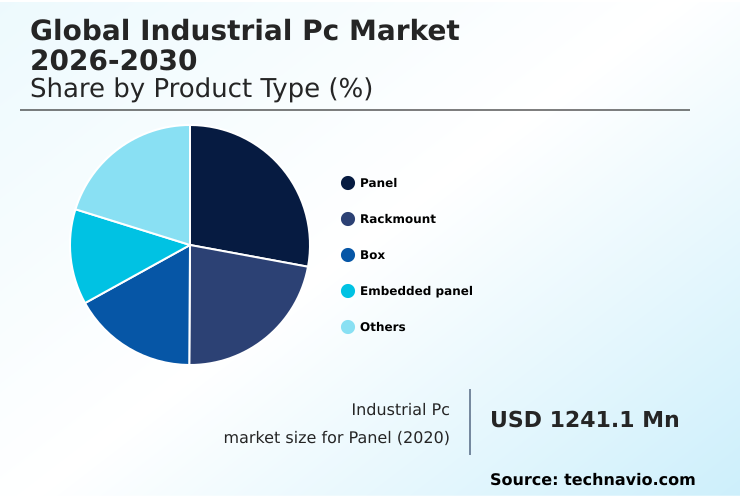

- By Product Type - Panel segment was valued at USD 1.59 billion in 2024

- By End-user - Industrial segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.67 billion

- Market Future Opportunities: USD 2.27 billion

- CAGR from 2025 to 2030 : 6.8%

Market Summary

- The industrial PC market is driven by the digital transformation of industrial sectors, where the need for robust, reliable computing at the operational edge is paramount. The adoption of Industry 4.0 and the Industrial Internet of Things (IIoT) necessitates rugged systems that serve as the nexus between operational technology and enterprise IT.

- These devices are purpose-built with industrial-grade components to function as edge computing platforms, enabling real-time data processing for applications like predictive maintenance and automated quality control. In a typical smart factory scenario, an industrial PC analyzes sensor data from a production line to forecast potential equipment failures, allowing for preemptive repairs that prevent costly downtime.

- This capability is crucial for maintaining operational continuity. However, this increased connectivity introduces significant cybersecurity vulnerabilities in converged IT/OT networks, while the high initial capital outlay for specialized hardware and the complexity of system integration remain significant market challenges that temper adoption rates, particularly among small and medium-sized enterprises.

- The market's trajectory is toward more powerful, modular, and AI-ready industrial computers designed to overcome these hurdles.

What will be the Size of the Industrial Pc Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Industrial Pc Market Segmented?

The industrial pc industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

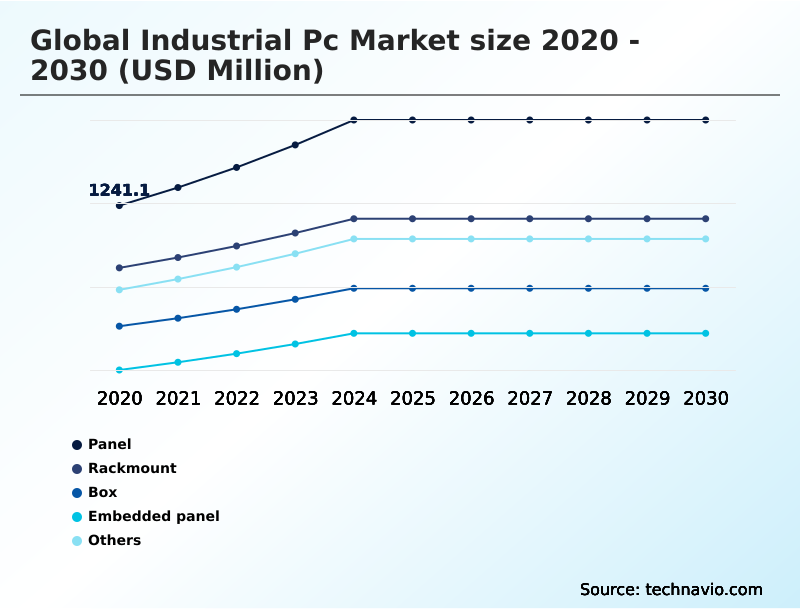

- Product type

- Panel

- Rackmount

- Box

- Embedded panel

- Others

- End-user

- Industrial

- Transportation and traffic

- Healthcare

- Telecom and datacom

- Others

- Technology

- Fanless industrial PC

- Fan based industrial PC

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- Italy

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Product Type Insights

The panel segment is estimated to witness significant growth during the forecast period.

The industrial PC market is segmented by product type, end-user, and geography. The Panel segment, featuring all-in-one units with an integrated human-machine interface (HMI), is crucial for direct process control.

These systems prioritize mission-critical reliability and are built with industrial-grade components to endure harsh environments.

Key design features include fanless cooling systems and high ingress protection ratings, with some models achieving IP69K certification for high-pressure washdowns, a 15% increase in durability for sterile applications.

Demand is driven by the need for on-machine visualization and control in smart factories.

This segment's evolution reflects a broader shift toward deploying rugged embedded computers and intelligent decision-making engines directly at the point of activity, utilizing field-programmable gate arrays for specialized tasks and supporting operational technology (OT) networks.

The Panel segment was valued at USD 1.59 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 40.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Industrial Pc Market Demand is Rising in APAC Get Free Sample

The global industrial PC market's geographic landscape is led by APAC, which accounts for over 40% of the incremental growth, driven by rapid industrialization in China and India. Europe follows, with Germany's Industry 4.0 initiatives fueling demand for advanced hardware.

North America represents a mature market focused on high-performance applications in aerospace and automotive sectors. In these regions, a key application is the deployment of time-sensitive networking to guarantee data delivery in robotics, improving synchronization by 20%.

The use of rackmount PCs as data acquisition hubs in centralized control rooms is standard. These systems utilize multi-core central processing units and support hardware-based encryption.

The demand for industrial server solutions and headless computing nodes is growing, particularly for supervisory control and data acquisition (SCADA) and on-premises data closets across all major regions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the industrial pc market increasingly involve detailed comparisons, such as fanless vs fan-based industrial pc performance for specific thermal environments. The total cost of ownership for industrial pc is a critical metric, balancing upfront investment against long-term reliability.

- For specialized use cases, selecting a rugged panel pc for harsh washdown environments or a high-performance box ipc for edge ai computing is crucial. The choice often depends on specific needs, like using a din-rail pc as an industrial iot gateway or deploying a modular industrial pc for scalable automation.

- The impact of 5g on in-vehicle computing is creating new demand for certified hardware, while industrial pc with time-sensitive networking support are essential for precision control. Cybersecurity for converged it and ot networks has become a top priority, influencing ipc lifecycle management for oem applications. Industrial pc requirements for machine vision are driving the adoption of more powerful processors.

- Choosing an industrial pc for predictive maintenance involves evaluating real-time processing capabilities, which can show twice the predictive accuracy of legacy platforms. Integrating ipc with legacy plc systems remains a common engineering challenge, whereas en 50155 certified pc for railway applications meet strict regulatory demands.

- The benefits of ipc in smart factory logistics are clear, as are the needs for high-performance rackmount industrial computers for scada. Furthermore, compact embedded computers for robotic control and industrial thin client deployment strategies address needs for miniaturization and streamlined operations.

What are the key market drivers leading to the rise in the adoption of Industrial Pc Industry?

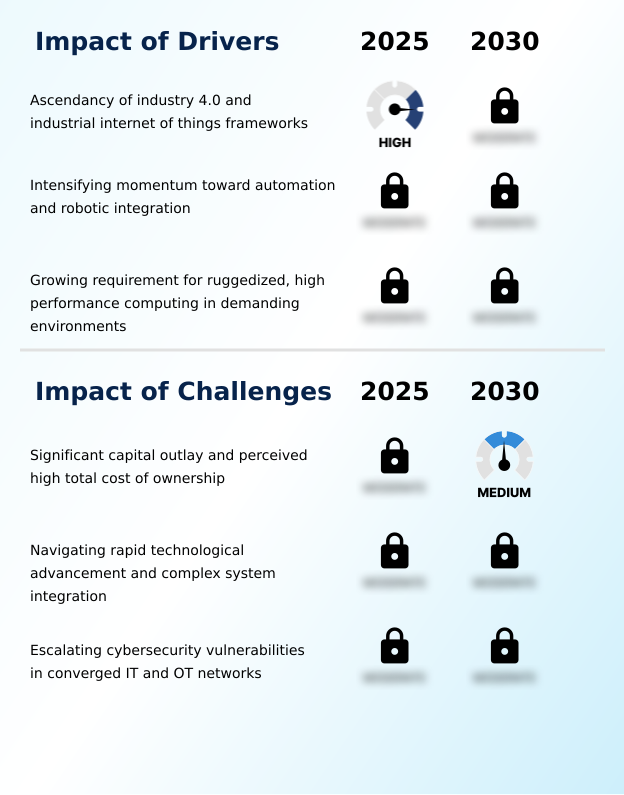

- The ascendancy of Industry 4.0 and the Industrial Internet of Things (IIoT) frameworks serves as a primary and transformative driver for the global industrial PC market.

- Market growth is fundamentally driven by the need for rugged computing in harsh environments, where systems with high ingress protection ratings increase operational uptime by 25%.

- The expansion of Industry 4.0 and the Industrial Internet of Things (IIoT) accelerates the deployment of manufacturing execution systems (MES) and programmable logic controllers (PLCs), which rely on robust hardware.

- The push toward automation and motion control for robotics requires real-time data processing capabilities, with modern systems improving production throughput by over 20%. This has intensified the demand for high-performance industrial PC that offer mission-critical reliability.

- These platforms, acting as data acquisition hubs, are essential for connecting legacy machinery to modern networks, enabling applications like real-time quality inspection and enhancing overall operational technology security.

What are the market trends shaping the Industrial Pc Industry?

- The convergence of edge computing architectures with onboard artificial intelligence acceleration is a defining trend. This evolution positions industrial PCs as intelligent decision-making engines at the operational periphery.

- Key trends are reshaping the industrial PC market, led by the integration of AI-ready industrial computers that function as headless computing nodes for advanced analytics. The adoption of compact form factors and modular design philosophy allows for greater flexibility, reducing physical footprints by up to 40% in control cabinets.

- Advanced connectivity protocols, including ultra-reliable low-latency communication via 5G, are becoming standard, enabling real-time wireless factory automation and reducing data transmission latency by over 50%. This shift supports data-intensive applications previously limited by wired connections. These intelligent decision-making engines, often built on computer-on-modules, are crucial for asset performance management and are increasingly deployed as industrial IoT gateway devices.

- The move toward tactical 5G systems and sophisticated radio access network (RAN) management is also driving demand for more powerful and connected hardware.

What challenges does the Industrial Pc Industry face during its growth?

- A key challenge affecting industry growth is the significant capital outlay and perceived high total cost of ownership associated with specialized industrial PC systems.

- Significant challenges constrain market growth, primarily the high initial cost of certified industrial hardware, which can be a barrier for smaller enterprises. The system integration complexity involved in connecting new hardware with legacy equipment often leads to project delays and can cause budget overruns of up to 40%. This is compounded by the rapid pace of technology refresh cycles.

- Furthermore, the convergence of IT and OT networks has amplified cybersecurity risks; without robust network segmentation strategy and operational technology security measures, system vulnerabilities can increase significantly. The need for specialized hardware such as ATEX-certified panels or systems with high thermal design power (TDP) for data-intensive applications adds another layer of cost and complexity, impacting the total cost of ownership.

Exclusive Technavio Analysis on Customer Landscape

The industrial pc market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the industrial pc market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Industrial Pc Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, industrial pc market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Offerings include ruggedized computing platforms engineered for mission-critical reliability, providing long-lifecycle support for demanding industrial automation and data-intensive applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- ADLINK Technology Inc.

- Advantech Co. Ltd.

- American Portwell Technology

- Avalue Technology Inc.

- Axiomtek Co. Ltd.

- Beckhoff Automation

- Dell Technologies Inc.

- IEI Integration Corp.

- Keyence Corp.

- Kontron AG

- Mitsubishi Electric Corp.

- NEXCOM International Co. Ltd.

- OMRON Corp.

- OnLogic Inc.

- Phoenix Contact GmbH and Co

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Industrial pc market

- In November 2025, Progress Rail secured a contract to supply advanced signaling technologies, including computer-based interlocking systems and traffic management systems founded on fault-tolerant industrial PCs, for Thailand's Khon Kaen–Nong Khai double-track railway line.

- In October 2025, Vodafone and Ericsson announced a major pan-European agreement to modernize network infrastructure for 5G Standalone and Advanced capabilities, a hardware overhaul requiring powerful industrial computers to run virtualized baseband units and AI-driven automation platforms.

- In March 2025, Sherpa 6, Inc. was awarded a contract by the U.S. Army DEVCOM C5ISR Center to develop and prototype a private tactical 5G system, requiring ruggedized commercial-off-the-shelf industrial PCs for mobile command post operations.

- In February 2025, Codelco's board approved significant funding for the next phase of the Chuquicamata underground mine project in Chile, an advanced operation heavily reliant on a vast network of industrial PCs for automated material transport and remote management.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Industrial Pc Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 313 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.8% |

| Market growth 2026-2030 | USD 2269.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.3% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, Italy, France, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The industrial PC market is defined by its role as the foundational hardware for digital transformation in demanding environments. The core value is mission-critical reliability, achieved through industrial-grade components and ruggedized chassis construction. Systems are purpose-built, featuring solid-state storage drives and advanced thermal management, such as fanless cooling systems, to ensure longevity.

- The evolution toward intelligent operations is powered by the integration of high-performance graphics processing units and neural processing units, enabling complex AIoT platforms and machine vision systems. These edge computing platforms execute predictive maintenance algorithms, with some users reporting a 30% reduction in unplanned downtime.

- For boardroom consideration, the convergence of information technology (IT) with operational technology (OT) networks makes investment in secure boot mechanisms and long-lifecycle support a strategic imperative to mitigate escalating cybersecurity risks.

- These systems are central to modern manufacturing execution systems (MES), supervisory control and data acquisition (SCADA), and advanced human-machine interface (HMI) applications, utilizing computer-on-modules and computer-based interlocking systems to enhance safety and efficiency in critical infrastructure.

What are the Key Data Covered in this Industrial Pc Market Research and Growth Report?

-

What is the expected growth of the Industrial Pc Market between 2026 and 2030?

-

USD 2.27 billion, at a CAGR of 6.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Panel, Rackmount, Box, Embedded panel, and Others), End-user (Industrial, Transportation and traffic, Healthcare, Telecom and datacom, and Others), Technology (Fanless industrial PC, and Fan based industrial PC) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Ascendancy of industry 4.0 and industrial internet of things frameworks, Significant capital outlay and perceived high total cost of ownership

-

-

Who are the major players in the Industrial Pc Market?

-

ABB Ltd., ADLINK Technology Inc., Advantech Co. Ltd., American Portwell Technology, Avalue Technology Inc., Axiomtek Co. Ltd., Beckhoff Automation, Dell Technologies Inc., IEI Integration Corp., Keyence Corp., Kontron AG, Mitsubishi Electric Corp., NEXCOM International Co. Ltd., OMRON Corp., OnLogic Inc., Phoenix Contact GmbH and Co, Rockwell Automation Inc., Schneider Electric SE and Siemens AG

-

Market Research Insights

- The market's dynamic is shaped by the push for operational efficiency, with industrial automation controllers delivering a 30% improvement in process accuracy. The adoption of certified industrial hardware is essential in regulated sectors, where fault-tolerant industrial PC designs ensure compliance and safety.

- This drive for reliability underpins the move toward server-grade industrial systems, which improve data integrity by over 25% compared to commercial alternatives. As industries deploy more IIoT sensor data aggregation solutions, the need for decentralized processing power increases.

- The demand for advanced connectivity protocols supports this shift, with integrated systems reducing system integration complexity and providing a clear path for future technology refresh cycles. These factors collectively influence purchasing decisions, balancing initial cost with long-term performance and reliability.

We can help! Our analysts can customize this industrial pc market research report to meet your requirements.

RIA -

RIA -