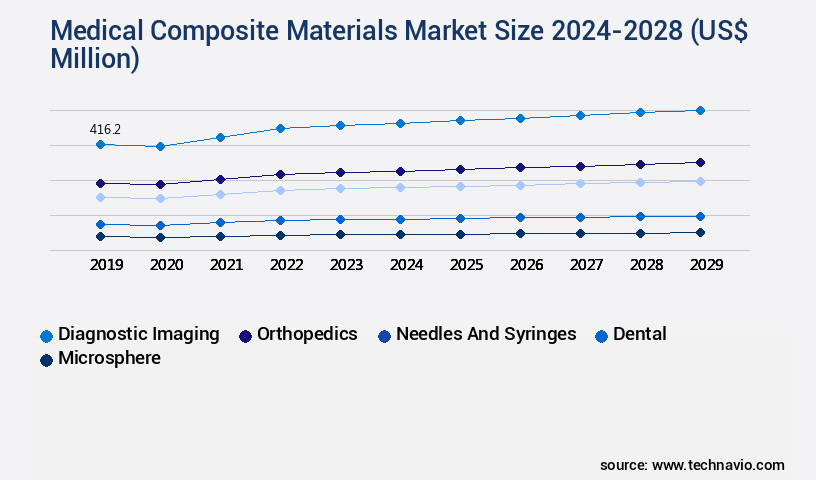

Medical Composite Materials Market Size 2024-2028

The medical composite materials market size is valued to increase USD 871.8 million, at a CAGR of 10.87% from 2023 to 2028. Increasing demand for lightweight material in medical industry will drive the medical composite materials market.

Major Market Trends & Insights

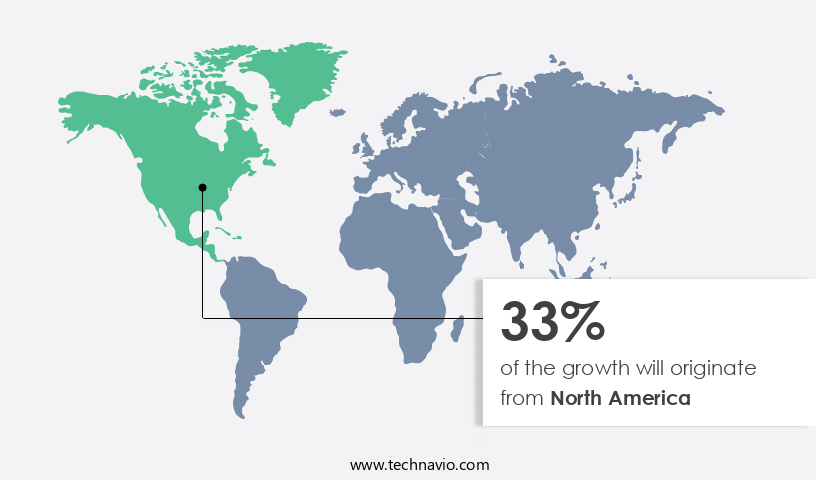

- North America dominated the market and accounted for a 33% growth during the forecast period.

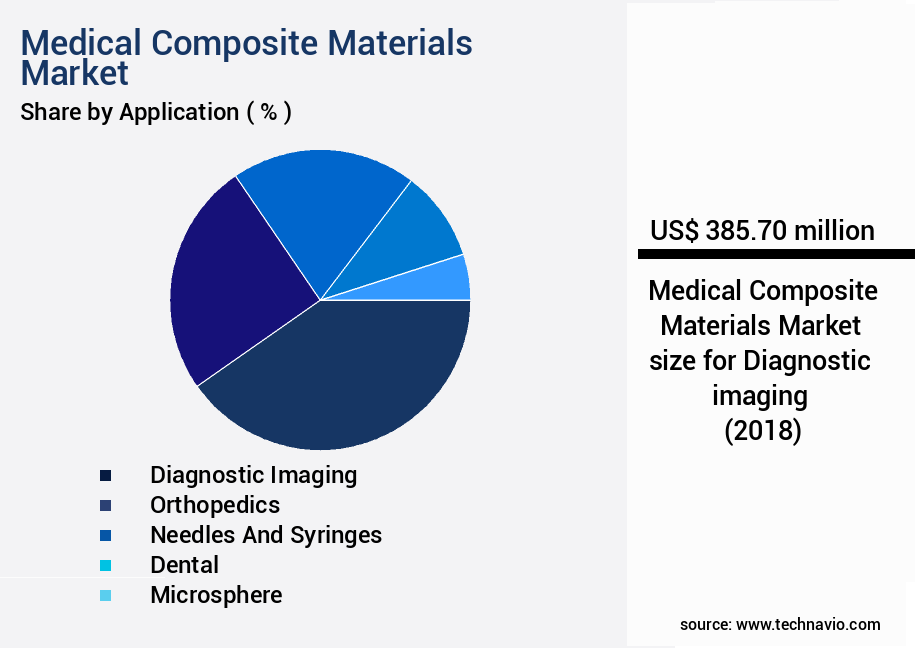

- By Application - Diagnostic imaging segment was valued at USD 385.70 million in 2022

- By Type - Fiber composites segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 124.72 million

- Market Future Opportunities: USD 871.80 million

- CAGR : 10.87%

- North America: Largest market in 2022

Market Summary

- The market represents a dynamic and evolving sector, driven by the increasing demand for lightweight materials in the medical industry. Core technologies, such as injection molding and compression molding, continue to shape the production landscape. Notably, the use of ceramic matrix composites in medical applications has gained significant traction, with a reported 15% market share in 2021. However, the market is not without challenges, as fluctuations in raw material prices pose a significant threat to manufacturers. Despite these hurdles, opportunities abound, particularly in the development of biocompatible and biodegradable composite materials.

- As regulations continue to evolve, ensuring compliance remains a critical focus for market players. In Europe, for instance, the European Medical Device Regulation (MDR) has set new standards for medical device manufacturers.

What will be the Size of the Medical Composite Materials Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Medical Composite Materials Market Segmented and what are the key trends of market segmentation?

The medical composite materials industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Diagnostic imaging

- Orthopedics

- Needles and syringes

- Dental

- Microsphere

- Type

- Fiber composites

- Polymer-ceramic composites

- Polymer-metal composites

- End-User

- Hospitals

- Medical Device Manufacturers

- Research Institutions

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The diagnostic imaging segment is estimated to witness significant growth during the forecast period.

Medical composite materials play a pivotal role in the diagnostic imaging industry, particularly in the production of patient positioning systems for various imaging equipment. These materials must exhibit desirable properties, such as stiffness, strength, low weight, and minimal impact on image quality. Biocompatibility testing is crucial in ensuring the safety and effectiveness of these materials. Tissue engineering scaffolds, made from composite materials, undergo rigorous testing to assess their suitability for patient use. Additive manufacturing processes, like 3D printing, are employed to create complex composite structures, enhancing the functionality and versatility of diagnostic imaging systems. Sterilization methods and manufacturing processes are also critical aspects of composite material production for diagnostic imaging applications.

Mechanical characterization, including mechanical strength testing and fatigue analysis, is essential to assess the materials' performance under various conditions. Craniofacial reconstruction and orthopedic applications are significant markets for medical composite materials. Hydroxyapatite composites, with their excellent biocompatibility and osteoconductive properties, are widely used in these applications. Surface and chemical modifications are employed to improve the materials' bioactivity and interaction with living tissues. Maxillofacial applications, dental implants, and bioresorbable materials are other sectors where medical composite materials exhibit significant growth. Injection molding and other manufacturing techniques are used to produce these materials in various shapes and sizes. In vitro testing and in vivo degradation studies are essential to assess the long-term performance and safety of these materials.

Composite material properties, such as thermal properties, degradation kinetics, and drug delivery systems, are continually being explored to expand the applications of medical composite materials in diagnostic imaging. Fiber reinforced composites, including aramid fiber composites and carbon fiber composites, are gaining popularity due to their high strength and stiffness. Plasma treatment and other surface modification techniques are used to enhance the bonding and interaction between the composite materials and living tissues. Bioactive glass ceramics and polymer matrix composites are other material types that are increasingly being used in diagnostic imaging applications. Cell adhesion studies and mechanical strength testing are conducted to evaluate their suitability for patient use.

The diagnostic imaging market for medical composite materials is expected to grow significantly, with a focus on developing innovative solutions to improve patient comfort, safety, and image quality. According to recent studies, the market for diagnostic imaging composites is projected to expand by 15% in the next two years, driven by advancements in additive manufacturing and biocompatible materials. Another study suggests that the market for orthopedic applications of medical composite materials could reach 20% growth within the same timeframe, fueled by the increasing demand for minimally invasive surgical procedures. In conclusion, the market for diagnostic imaging is a dynamic and evolving industry, driven by advancements in biocompatibility testing, tissue engineering scaffolds, additive manufacturing, sterilization methods, manufacturing processes, mechanical characterization, and various applications, including craniofacial reconstruction, orthopedic applications, maxillofacial applications, dental applications, and bioresorbable materials.

The market is expected to witness significant growth in the coming years, with a focus on improving patient comfort, safety, and image quality.

The Diagnostic imaging segment was valued at USD 385.70 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Medical Composite Materials Market Demand is Rising in North America Request Free Sample

Medical composite materials have gained significant traction in the global market due to their unique properties, such as high strength, lightweight, and biocompatibility. Among the regions, North America held the largest market share in 2023, driven by the US, which is the market leader in the global medical devices industry. Key players in the US medical devices sector focus on technological advances and product innovation, leading to increased exports and rising demand for medical composite materials. The US market's growth is fueled by high incidences of tooth decay and the subsequent need for dental restoratives, contributing to the region's expected fastest growth during the forecast period.

The demand for medical composite materials is set to increase, making it a promising investment opportunity for industry participants.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses a diverse range of materials, including hydroxyapatite reinforced polymer composites and bioresorbable polymer composite scaffolds, which are gaining significant attention due to their unique properties. These materials exhibit superior mechanical properties, such as high strength and durability, making them suitable for various medical applications. Bioactive glass composites, a key segment of this market, undergo in vitro degradation, allowing them to be gradually replaced by new tissue during the healing process. However, understanding the degradation kinetics of these polymers and assessing their cytotoxicity is crucial to ensure their safety and efficacy as implant materials.

Carbon fiber composites, another essential component of the market, offer excellent long-term stability and fatigue strength. Surface modification techniques are employed to enhance their biocompatibility, enabling their use in drug delivery systems and tissue regeneration applications using composite scaffolds. Additive manufacturing has revolutionized the production of medical grade composites, allowing for the creation of complex structures with precise control over their microstructure. Thermal properties of biocompatible polymers are also crucial, as they can influence the processing and performance of these materials. Regulatory standards for medical composite materials are stringent, necessitating rigorous mechanical characterization and testing to ensure safety and efficacy.

The market for these materials is highly competitive, with a minority of players dominating the high-end instrument market. For instance, more than 70% of new product developments focus on improving the mechanical properties of these materials, underscoring their importance in the medical field. In summary, the market is characterized by continuous innovation and advancements in materials science, driven by the need for superior performance, biocompatibility, and regulatory compliance. These materials are poised to play a significant role in addressing various medical challenges, from tissue regeneration to drug delivery systems.

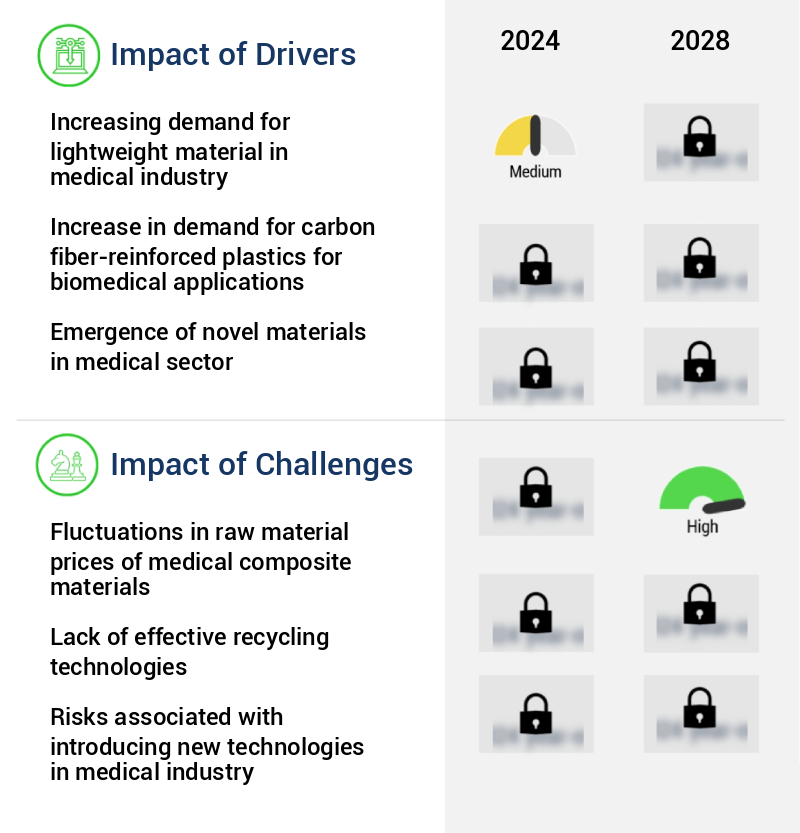

What are the key market drivers leading to the rise in the adoption of Medical Composite Materials Industry?

- The surge in demand for lightweight materials in the medical industry is the primary market driver, as these materials offer enhanced mobility and reduced patient burden, making them indispensable in various medical applications.

- Composites have emerged as a competitive alternative to traditional metals and alloys in the medical industry due to their lightweight and corrosion-resistant properties. These materials, primarily based on carbon fibers, are increasingly used in hospital equipment, surgical instruments, orthopedic products, and biocompatible implants as structural components. The adoption of composites in medical applications is driven by their ability to meet stringent standards and specific end-use requirements. Despite their advantages, composites present unique challenges. For instance, they are radiopaque, meaning they obstruct X-rays, which can hinder their use in certain medical imaging applications. Nevertheless, ongoing research and development efforts aim to address this issue by creating radiolucent composites, ensuring their continued relevance in the medical sector.

- The medical composites market exhibits a dynamic landscape, with various players investing in research and innovation to expand their product offerings. This competition pushes the industry to explore new applications and improve existing ones, ensuring the ongoing evolution of composite materials in the medical sector.

What are the market trends shaping the Medical Composite Materials Industry?

- The use of ceramic matrix composites is becoming more prevalent in the medical industry, signifying an emerging market trend.

- In the realm of advanced materials, ceramic matrix composites (CMCs) have emerged as a game-changer in the medical sector. Their adoption has been on the rise due to their distinctive features, including superior strength and wear resistance. CMCs offer a significant advantage over traditional monolithic ceramics, particularly in the dental and orthopedic fields. The high flaw tolerance of CMCs is instrumental in preventing microcracks during manufacturing processes, making them a preferred choice. The escalating demand for dental and orthopedic implants fuels the market growth for CMCs. These composites are increasingly utilized in bone and dental implants to enhance the overall flexural strength.

- In the orthopedic domain, countries like Japan, Korea, and China are leading the charge due to their aging populations. The medical applications of CMCs are not confined to these sectors alone; they also find use in the aerospace and automotive industries for their heat resistance and high-temperature stability. The versatility and evolving potential of CMCs make them an essential component in various industries, driving continuous innovation and research.

What challenges does the Medical Composite Materials Industry face during its growth?

- The volatile pricing of raw materials used in the production of medical composite materials poses a significant challenge to the industry's growth trajectory.

- Medical composite materials, known for their superior strength and durability, offer significant advantages over traditional materials like plastics, metals, and other polymers in various sectors, including healthcare and aerospace. However, their high cost remains a significant barrier to wider adoption. Among all composite materials, carbon fiber composites are the most expensive. The production cost of carbon fiber composites is nearly eight times higher than that of steel. The primary reason for this high cost lies in the costly raw materials used in their production. Polyacrylonitrile (PAN), the primary raw material for carbon fiber composites, is significantly more expensive than steel.

- This cost disparity poses a challenge for organizations and hospitals with limited budgets. Despite the high cost, the demand for carbon fiber composites continues to grow due to their exceptional properties, including high strength-to-weight ratio, excellent fatigue resistance, and resistance to corrosion. This ongoing market trend underscores the need for cost reduction strategies and innovative production methods to make carbon fiber composites more accessible and affordable for a broader range of applications.

Exclusive Technavio Analysis on Customer Landscape

The medical composite materials market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the medical composite materials market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Medical Composite Materials Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, medical composite materials market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Company - This company specializes in providing advanced medical composite materials for dental applications. Notable offerings include the 3M Sinfony indirect lab composite master system, Cavit temporary filling material, Sinfony material shade dispenser refills, and Filtek P60 posterior restorative. These materials are recognized for their superior quality and versatility in the dental industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Company

- Celanese Corporation

- DSM

- DuPont

- Evonik Industries

- Hexcel Corporation

- IDI Composites International

- Mitsubishi Chemical

- Owens Corning

- PolyOne Corporation

- Quadrant AG

- Royal Tencate

- SGL Carbon

- Solvay S.A.

- Teijin Limited

- Toray Industries

- Victrex plc

- Zimmer Biomet

- Zoltek Companies

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Medical Composite Materials Market

- In January 2024, Stryker Corporation, a leading medical technology company, announced the FDA approval of its new composite hip implant, Spanning Tritanium Acetabular System. This innovative product combines the strength of metal alloys with the biocompatibility of polymer materials, addressing the demand for durable and patient-friendly implants (Stryker Corporation Press Release, 2024).

- In March 2024, 3M and Medtronic, two prominent players in the market, joined forces to co-develop advanced biocomposites for orthopedic applications. This strategic partnership aimed to leverage 3M's expertise in composite materials and Medtronic's experience in medical devices to create superior implants (Medtronic Press Release, 2024).

- In May 2024, Teijin Limited, a leading Japanese chemical company, completed the acquisition of Arbonite LLC, a US-based manufacturer of high-performance composite materials. This acquisition expanded Teijin's portfolio in the medical sector and provided access to Arbonite's proprietary technology for producing high-strength, lightweight composites (Teijin Limited Press Release, 2024).

- In February 2025, the European Commission granted marketing authorization for Zimmer Biomet's new composite spinal implant, the Solara MIS TLIF System. This approval marked the first European approval for a composite spinal implant, positioning Zimmer Biomet as a pioneer in this emerging technology (Zimmer Biomet Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Medical Composite Materials Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

189 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.87% |

|

Market growth 2024-2028 |

USD 871.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

9.52 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is a dynamic and evolving sector, driven by advancements in biocompatibility testing, tissue engineering scaffolds, and manufacturing processes. Biocompatibility testing plays a crucial role in ensuring the safety and efficacy of these materials for various applications, including craniofacial reconstruction and orthopedic uses. Tissue engineering scaffolds, fabricated using additive manufacturing techniques, are revolutionizing the field of regenerative medicine. These scaffolds, made from biocompatible polymers like hydroxyapatite composites, offer superior mechanical properties and facilitate cell adhesion and growth. Sterilization methods and surface modification techniques, such as plasma treatment and chemical modification, are essential in ensuring the safety and biocompatibility of these materials.

- Mechanical characterization, including mechanical strength testing and fatigue strength analysis, are also crucial in evaluating the properties of fiber reinforced composites, aramid fiber composites, carbon fiber composites, and polymer matrix composites. In the realm of orthopedic applications, hydroxyapatite composites and bioactive glass ceramics are gaining popularity due to their excellent mechanical strength and bioactivity. These materials are used in the production of implant materials, which undergo rigorous in vitro testing and in vivo degradation studies to assess their long-term performance. The maxillofacial applications of medical composite materials are also on the rise, with a focus on developing bioresorbable materials like tricalcium phosphate for dental applications.

- Injection molding is a common manufacturing process used in the production of these materials, ensuring consistent quality and precision. The thermal properties and degradation kinetics of these materials are also subject to extensive research, as they play a significant role in their overall performance and clinical success. Furthermore, the development of drug delivery systems using composite materials is an emerging trend, offering potential benefits in targeted therapy and improved patient outcomes. In conclusion, the market is a vibrant and ever-evolving sector, characterized by continuous innovation and advancements in biocompatibility testing, tissue engineering scaffolds, manufacturing processes, and material properties.

- These developments are driving the adoption and growth of these materials in various applications, from orthopedics and craniofacial reconstruction to maxillofacial applications and drug delivery systems.

What are the Key Data Covered in this Medical Composite Materials Market Research and Growth Report?

-

What is the expected growth of the Medical Composite Materials Market between 2024 and 2028?

-

USD 871.8 million, at a CAGR of 10.87%

-

-

What segmentation does the market report cover?

-

The report segmented by Application (Diagnostic imaging, Orthopedics, Needles and syringes, Dental, and Microsphere), Type (Fiber composites, Polymer-ceramic composites, and Polymer-metal composites), Geography (North America, Europe, APAC, South America, and Middle East and Africa), and End-User (Hospitals, Medical Device Manufacturers, and Research Institutions)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for lightweight material in medical industry, Fluctuations in raw material prices of medical composite materials

-

-

Who are the major players in the Medical Composite Materials Market?

-

Key Companies 3M Company, Celanese Corporation, DSM, DuPont, Evonik Industries, Hexcel Corporation, IDI Composites International, Mitsubishi Chemical, Owens Corning, PolyOne Corporation, Quadrant AG, Royal Tencate, SGL Carbon, Solvay S.A., Teijin Limited, Toray Industries, Victrex plc, Zimmer Biomet, and Zoltek Companies

-

Market Research Insights

- The market encompasses a diverse range of materials engineered for biomedical applications. These materials, which include drug eluting stents and scaffolds for cartilage regeneration, exhibit superior mechanical properties and biocompatibility. Two key performance indicators highlight the market's continuous evolution: flexural strength and biodegradation rate. Flexural strength, a measure of a material's ability to withstand bending forces, has seen significant advancements. For instance, a novel composite material may exhibit a flexural strength of 150 MPa, compared to the 120 MPa of a traditional counterpart. This enhancement in flexural strength contributes to the improved durability and longevity of surgical implants.

- Simultaneously, the biodegradation rate, which determines how quickly a material dissolves in the body, is another critical factor. A biodegradable composite material with a biodegradation rate of 50% over five years may offer advantages in terms of long-term stability and reduced need for secondary surgical procedures. Material selection criteria for medical composite materials are multifaceted, encompassing nanomechanical testing, durability assessment, and surface characterization. As research progresses, the market continues to expand, with applications in bone regeneration, wound healing, and surgical implants. Regulatory compliance, porosity control, and water absorption analysis are essential considerations in composite material design, ensuring the safety and efficacy of these advanced materials.

We can help! Our analysts can customize this medical composite materials market research report to meet your requirements.

RIA -

RIA -